PLYM - The Low Hanging Fruit Phenomenon As Taught By Life Storage

2023-06-28 10:33:43 ET

Summary

- When a company is operating flawlessly, the upside might already be priced in.

- It tends to be the flawed companies that get bought out.

- Be careful with double accounting on earnings multiples.

Life Storage ( LSI ) serves as an excellent case study in what I call the low hanging fruit phenomenon where almost paradoxically, poor operations represent opportunity rather than risk. We will describe the phenomenon in more detail later, but let me begin with some background on the self-storage sector.

Self-storage is a unique sector in that it is one of the few areas that is still operated terribly. Most other sectors execute within a small to medium margin of operational optimization.

- Nearly every large apartment community uses the same price optimization software. They have on-site repairmen to both increase the speed and mitigate cost of repairs.

- Nearly every U.S. farmer uses optimized planting and harvesting techniques. The ratios of the various cereal grains planted each year make sense for the forecasted weather and prices.

- Warehouses are managed to minimize downtime between tenants with landlords reaching out to both current and prospective tenants well in advance of lease expiry.

In contrast, a large portion of self-storage has glaring operational flaws.

- Lack of proper advertising to make customers aware of a property’s existence

- Deferred capex

- Failure to upgrade to digital locks

These errors exist because of how fragmented the industry is. Rather than being owned by a professional institution whose sole purpose is to run such properties, the majority of self-storage has been owned historically by individuals for whom it is just a side project. In some cases, the owners might not even live in the same state as the self-storage property they operate which limits their ability to give the property operations the needed TLC.

Framed another way, compared to other sectors, the self-storage sector has a tremendous amount of low hanging fruit. Almost paradoxically, the weak starting point has allowed it to be among the best performing sectors.

{kind=link}

The REITs came in and gobbled up poorly operated properties and by managing them properly could effectively double their NOI in a short time period. The net result was an impressive ROIC.

So that is the low hanging fruit opportunity that has historically existed between the small individual sellers and the big institutional buyers.

Today is a different story. The main self-storage REITs are now too big to really buy properties from individuals. It simply would not move the needle.

As such, they have moved on to a different form of low hanging fruit – the operational delta between the REITs. Extra Space Storage ( EXR ) and CubeSmart ( CUBE ) are the top tier operators while Public Storage ( PSA ) and LSI operate at institutional caliber, but sloppily.

PSA is too big to buy, so EXR is buying LSI. As they merge, EXR will bring property operations to its standard and collect a nice gain. I don’t see a great investment opportunity here though as EXR trades at a fairly high multiple and self-storage as an industry is becoming oversupplied. Additionally, the arbitrage gap we discussed in a previous article has largely closed.

{kind=link}

Instead, I see a great case study in the concept of double accounting with regard to well operated companies.

The double accounting phenomenon

There is no doubt that a well operated company is worth more than a poorly operated company. However, the market seems to be double accounting the quality difference.

For simplicity let us consider 2 companies which each have a $1 million self-storage property.

- The poorly operating company nets $60,000 per year in FFO

- The well executing company nets $100,000 per year in FFO

If these companies trade at the same FFO multiple, the market is already giving credit to the stronger company for the extra FFO it is gleaning through its better operations.

That, in my opinion, would be correct valuation.

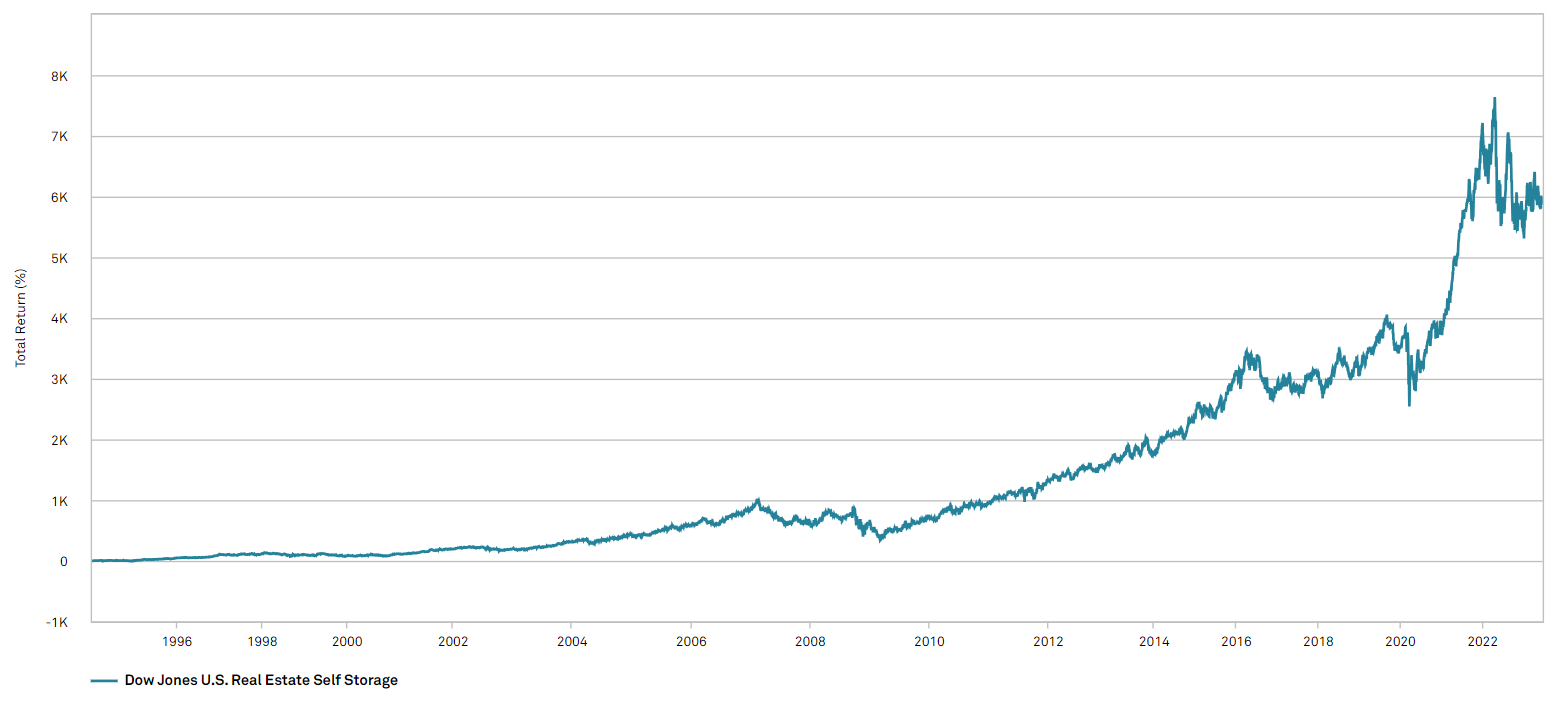

In practice, however, the market actually trades the better operating company at a higher multiple. Note below how through most of the last 10 years, EXR (the good operator) has traded at a higher multiple than the self-storage index while LSI (the weaker operator) has largely traded at a discounted multiple to the index.

{kind=link}

So not only is EXR earning more FFO from its properties, but then the market is paying more for each dollar of FFO it is making.

That is double accounting.

Low hanging fruit is not necessarily a bad thing. It should not be punished with a lower multiple. The key to using this for investing opportunity is to recognize when the low hanging fruit will be harvested. Here are some examples:

Facebook ( META ) was operating inefficiently with far more employees than it needed. In 2023 it commenced the “year of efficiency,” trimmed the fat, and this happened.

{kind=link}

The same thing happened in one of our REITs, Iron Mountain ( IRM ) which also had too many middle management type employees. It engaged in what it termed “Project Summit” and got rid of its bloat resulting in annual savings somewhere in the ballpark of $300 million. It too surged on the efficiency improvement.

{kind=link}

The lesson

It is unequivocally better for a company to run efficiently, but quite often in the market efficient operations are overly rewarded and inefficiency is overly punished.

One can spot the pricing of being overly rewarded or punished when the earnings multiple is impacted on top of the earnings themselves being impacted.

In those cases, where the market is double accounting, it can be opportunistic to buy the company with the low hanging fruit. The key is just to make sure it is inefficiency of a nature that can be fixed.

Opportunities versus that which will not be fixed

Among REITs there is quite a bit of punishing in terms of FFO multiple for those which operate at a high G&A load as a percentage of revenue. It is a classic double accounting as the high G&A already hurts absolute FFO and then the market trades it at a lower price per dollar of FFO.

So among this group, which are opportunities and which are doomed to go unfixed?

I think it comes down to the nature of the high G&A as a percentage of revenue. If it comes from management being greedy and entrenched, that is a hard fix.

The RMR managed REITs will continue to be RMR managed and the external manager will continue to extract value from the REITs into its own pockets. The same could be said for the American Realty family of companies as recently written about by Ross Bowler.

In contrast, some other companies have high G&A load for much more innocent reasons with the most common cause being very small size. This is where the opportunity lies because many of these are great companies and the low hanging fruit is easily picked over time simply by the company growing.

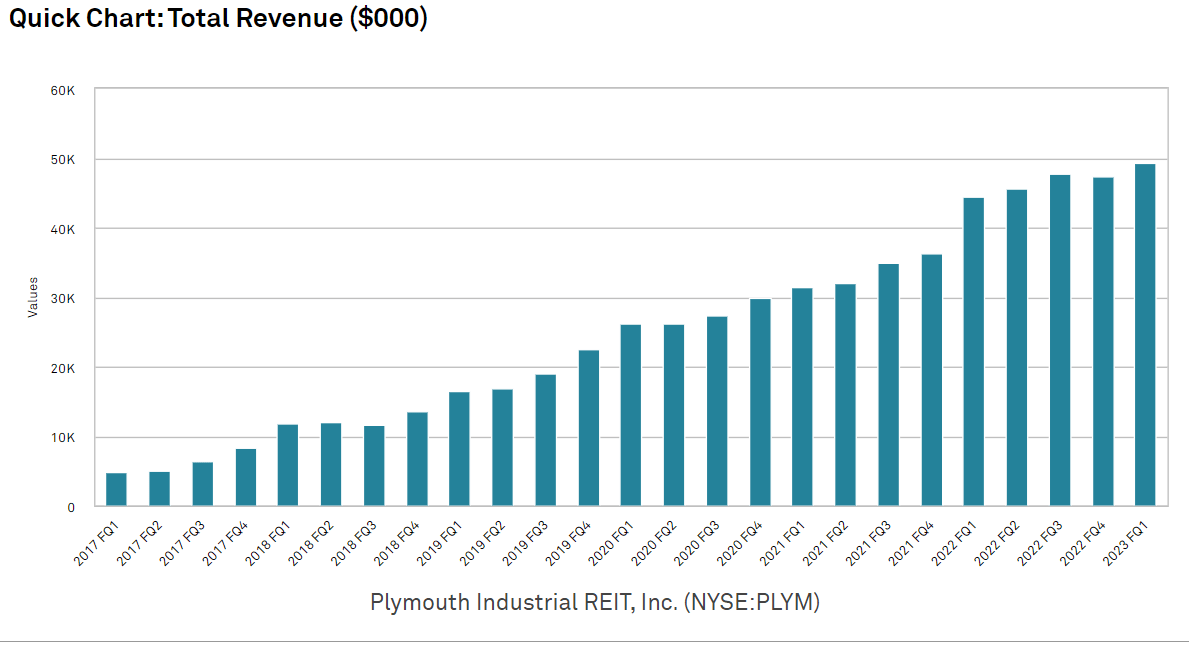

A recent example of this category would be Plymouth Industrial REIT ( PLYM ) which was fundamentally a strong company but was subscale and the market traded it at half the multiple of industrial REIT peers.

It grew.

{kind=link}

G&A as a percentage of revenue dropped from almost 20% in 2017 to around 7% as of most recent quarter. A natural efficiency of scale.

2 more REITs are presently undergoing a similar efficiency from scale transformation:

We own both. We know the management teams well and they are in the process of achieving efficient scale. As they grow they present the opportunity of both the FFO/share increasing and the multiples increasing as the market stops double accounting for the inefficiency of being subscale.

Wrapping it up

While LSI is no longer opportunistic, it teaches a valuable lesson in efficiency improvement which reveals other opportunities. When we see low hanging fruit we pick it.

For further details see:

The Low Hanging Fruit Phenomenon As Taught By Life Storage