WNC - The Manitowoc Company: Expect Outperformance To Continue

Summary

- The Manitowoc Company continues to post attractive sales growth and improving bottom line results.

- This has helped the firm to outperform the market more broadly in recent months.

- With how cheap shares still are, that upside potential could still continue moving forward.

Ideally, when we make an investment, we would like for that investment to generate a positive return. But, unfortunately, that does not always happen. A good consolation prize to this, however, can be to own an asset that generates a loss but a loss that is smaller than what the market's loss has been. In recent months, one example I could point to where this has been the case involves a firm called The Manitowoc Company ( MTW ). This enterprise is focused on the production and sale of a portfolio of various equipment, such as mobile hydraulic cranes, lattice boom crawler cranes, boom trucks, tower cranes, and more. Shares have experienced downside over the past few months, but that downside has been far better than with the broader market has experienced. This can be chalked up to robust fundamental performance, both on the company's top line and its bottom line. Add on top of this the fact that shares of the business are still trading on the cheap, and I would make the case that investors might be wise to consider keeping their stake in the business for now.

The picture is improving

Back in April of 2022, I wrote an article discussing the investment worthiness of The Manitowoc Company. In that article, I acknowledged that shares of the business were cheap and offered attractive upside potential. This was in spite of the fact that the historical financial performance of the business had been quite lumpy. Normally, a firm as cheap as this would likely have warranted a ‘strong buy’ rating. But because of the fundamental volatility, I decided to opt framework conservative assessment and rated it a ‘buy’ to reflect my belief that shares should at least outperform the broader market for the foreseeable future. Since then, that is precisely what has happened, even though performance might not have been as great as investors would have hoped. You see, since the publication of that article, the S&P 500 has plunged 8.3%. By comparison, The Manitowoc Company has generated a loss for investors of only 2.4%.

{kind=link}

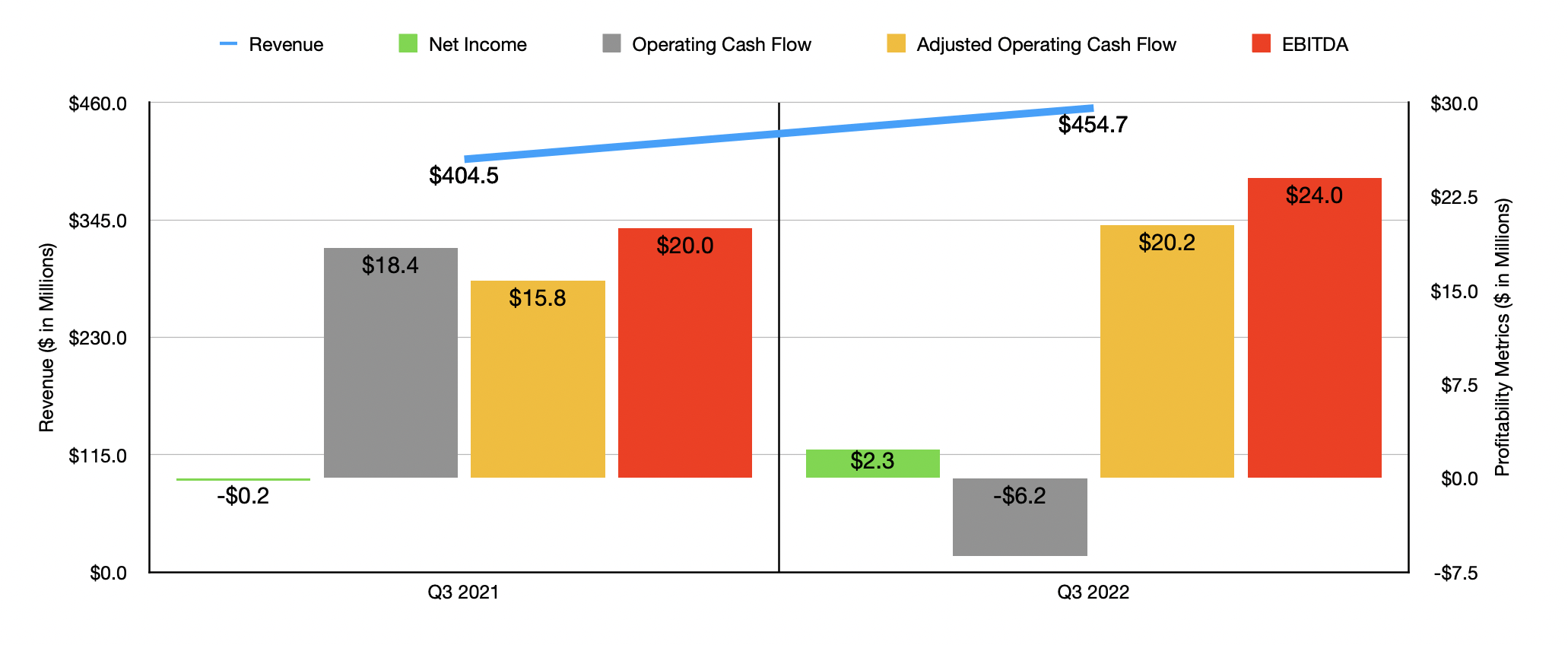

To understand why The Manitowoc Company has held up far better than the market has, we need only look at data covering the third quarter of its 2022 fiscal year . This is the most recent quarter for which data is available. During that time, sales came in at $454.7 million. That's 12.4% higher than the $404.5 million reported one year earlier. The vast majority of this sales increase came from its Americas operations, with revenue spiking 25.1% from $190.6 million to $238.5 million. This rise, management said, was largely due to higher non-new machine sales and pricing actions. The company did not say exactly how much of the increase was driven by acquisitions. But they did say that this played a role in the higher machine sales. Sales also rose to the tune of 6.9% in the EURAF (Europe and Africa) market, also because of higher prices, as well as because of higher new machine sales. The only weakness the company experienced was in its MEAP (Middle East and Asia/Pacific) business, with revenue dropping 12.5% from $63.9 million to $55.9 million. This decrease, management said, was because of lower new machine sales and foreign currency fluctuations. Some of this was offset by higher pricing.

Bottom line results for the company also improved during this time. Net income went from negative $0.2 million to $2.3 million. Operating cash flow actually worsened, falling from $18.4 million to negative $6.2 million. But if we adjust for changes in working capital, it would have risen from $15.8 million to $20.2 million. Meanwhile, EBITDA rose from $20 million to $24 million. Outside of profitability, we should also be paying attention to the orders and backlog data reported by the company. To be clear, during the third quarter, orders of $472 million came in lower than the $540.6 million reported the same time one year earlier. This could be a sign of weakness around the corner. Considering what's going on with the global economy, this would not be a surprise. Even though this is the case, overall backlog of $943.4 million is higher than the $890.6 million the company had in the third quarter of its 2021 fiscal year. This means that the company has some time before it experiences a decline in revenue.

{kind=link}

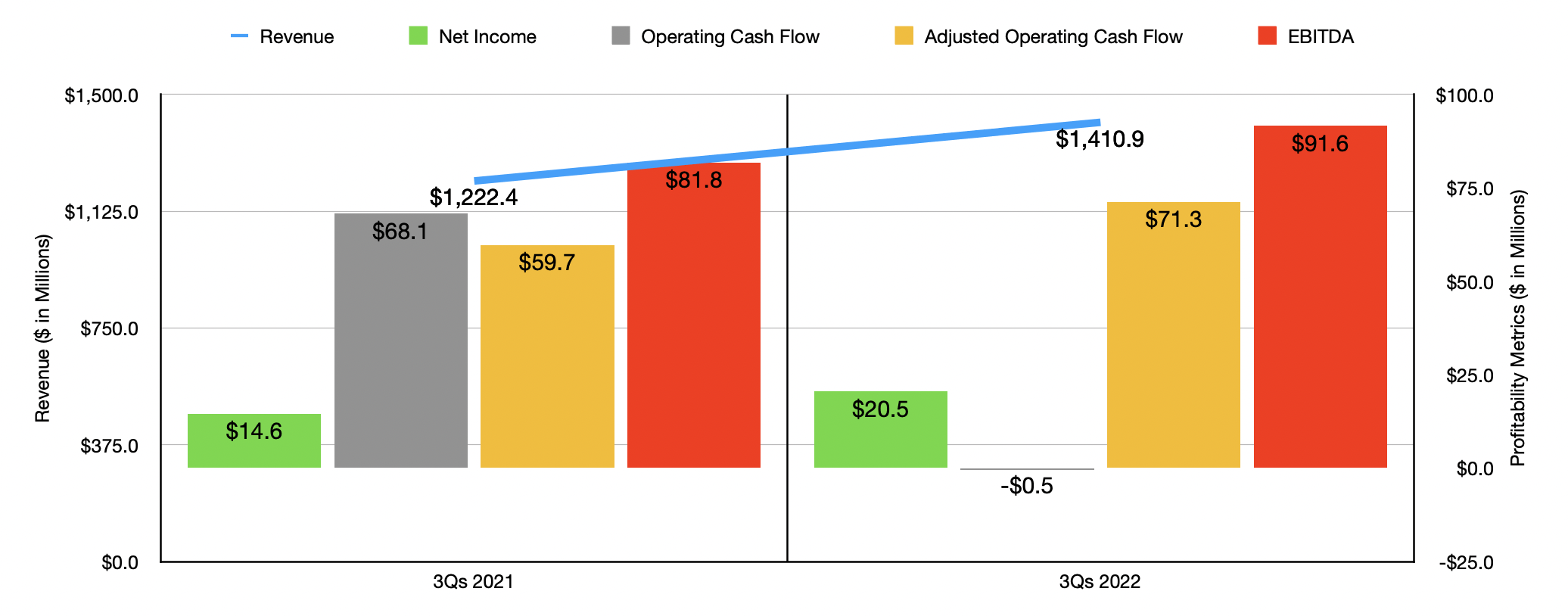

For the first nine months of 2022, the results looked remarkably similar to what they looked in the third quarter alone. Revenue of $1.41 billion came in 15.4% higher than the $1.22 billion reported one year earlier. Net income for the company expanded from $14.6 million to $20.5 million. Once again, operating cash flow was down, having fallen from $68.1 million to negative $0.5 million. But on an adjusted basis, it rose nicely from $59.7 million to $71.3 million. And finally, EBITDA for the business expanded from $81.8 million to $91.6 million.

When it comes to 2022 in its entirety, we won't know what the end result will have been until management reports. But we do know that, as of the third quarter, they were forecasting overall sales of between $2 billion and $2.2 billion. The company also said that EBITDA would be between $130 million and $160 million, very likely coming in near the low end of that range. Earnings per share, meanwhile, were expected to be between $0.65 and $1.35. Given the vast range of earnings there, I don't see valuing the company on this basis to be all that reliable. Instead, we should value it based on the aforementioned EBITDA figure, as well as on operating cash flow. According to my estimate, for 2022, that metric should come in at around $87.3 million.

{kind=link}

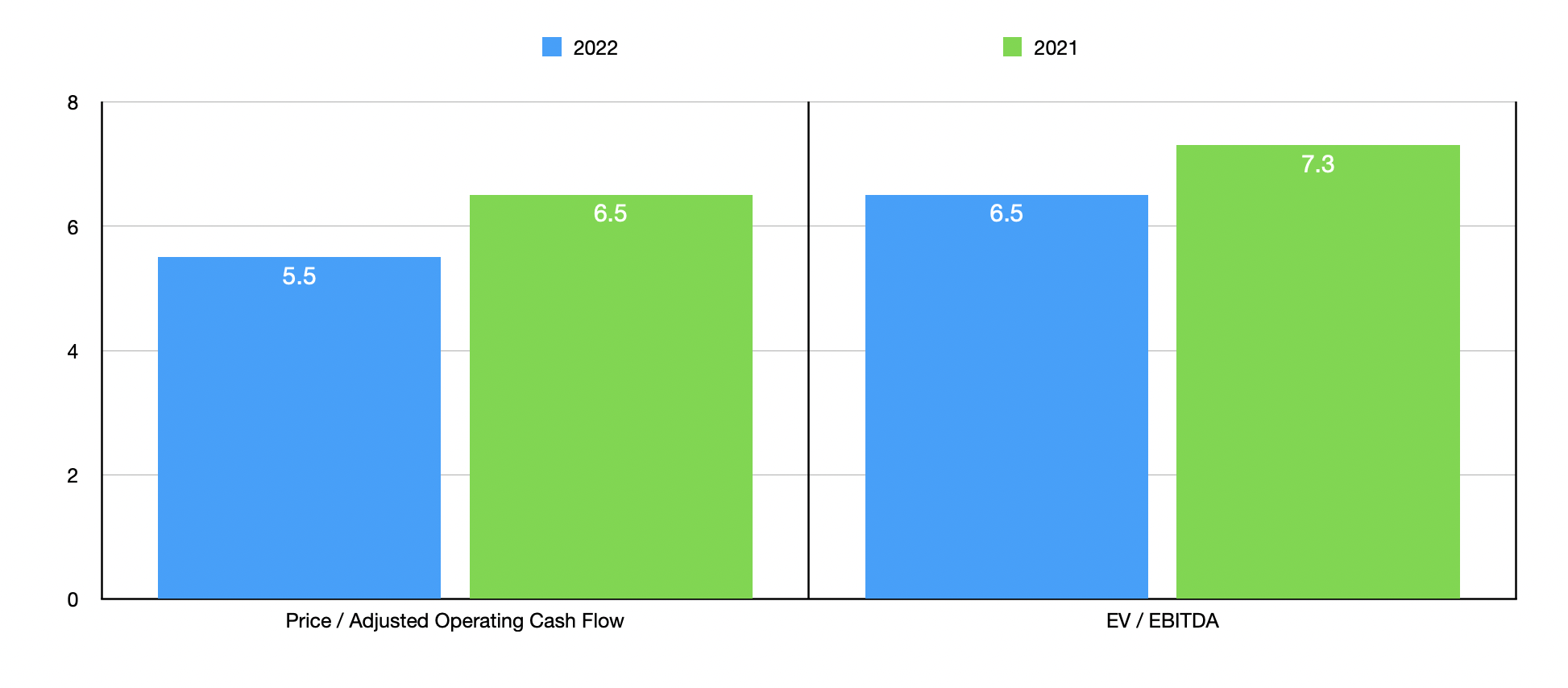

Based on these figures, The Manitowoc Company is trading at a price to adjusted operating cash flow multiple of 5.5. The EV to EBITDA multiple for the company is only slightly higher at 6.5. By comparison, using the data for the 2021 fiscal year would yield multiples of 6.5 and 7.3, respectively. As part of my analysis, I also compared the business to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 7.4 to a high of 51.2. Using the EV to EBITDA approach, the range was from 7.4 to 15. In both of these cases, our prospect was the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| The Manitowoc Company |

| 5.5 |

| 6.5 |

| Terex Corp ( TEX ) |

| 51.2 |

| 9.6 |

| Wabash National ( WNC ) |

| 11.0 |

| 7.7 |

| Allison Transmission Holdings ( ALSN ) |

| 7.4 |

| 7.4 |

| Trinity Industries ( TRN ) |

| 20.4 |

| 14.0 |

| Westinghouse Air Brake Technologies ( WAB ) |

| 20.1 |

| 15.0 |

Takeaway

The data available to us today suggests to me that The Manitowoc Company may experience a patch of weakness at some point in the not-too-distant future. This may scare some investors away. However, the firm is doing better than it was in the past and shares are trading on the cheap. Even if the stock becomes a bit pricier from a valuation perspective, I would find it difficult to imagine a scenario where shares are overvalued. Because of this, I still do believe the ‘buy’ rating I assigned the company previously is appropriate at this moment.

For further details see:

The Manitowoc Company: Expect Outperformance To Continue