RHP - The Market Is Crashing: Here's What I Am Buying

- REITs are the cheapest they have been in years.

- We believe that the market has overreacted to inflation, recession, and interest rate concerns.

- We highlight some of our top picks.

The market continued to decline in June and opportunities are now abundant.

The broader REIT market is down ~20% YTD, and as you can see from the table below, there are a lot of individual names that are down over 30% from their recent highs:

REITs that are down the most (R. Paul Drake via High Yield Landlord)

{kind=link}

Interestingly, many of the highest-quality REITs are actually down the most. Blue-chips like Public Storage ( PSA ), American Tower ( AMT ), and Prologis ( PLD ) are down ~30%, which really tells you how pessimistic investors have become.

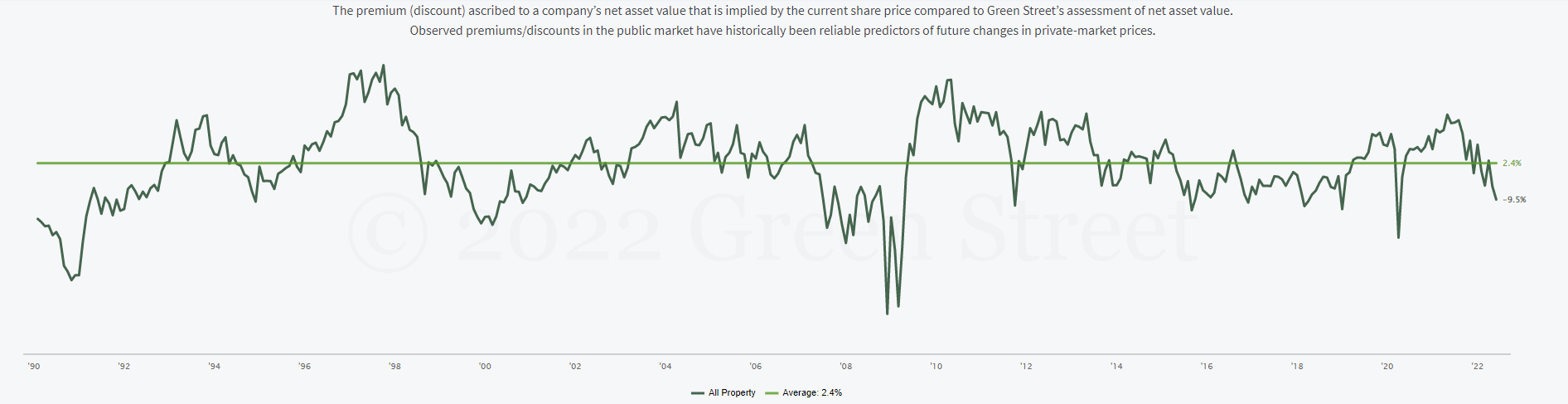

According to Green Street Advisors, REITs are currently the cheapest they have been since the beginning of the pandemic, if you ignore the initial crash that happened in March 2020:

REITs are the cheapest in years (Green Street Advisors)

{kind=link}

Typically, REITs trade at a small premium to net asset value, or NAV in short, but today, they are priced at a 10% discount on average. That's based on calculations from Green Street Advisors, which is notorious for being conservative and forward-looking with its NAV estimates.

If you used the consensus NAV estimates of regular analysts, the average discount to NAV would expand closer to 15% and it is not uncommon to find even high-quality REITs trading at greater than 20% discounts.

BSR Real Estate Investment Trust ( OTCPK:BSRTF /HOM.U) is a good example. It owns affordable apartment communities in rapidly growing Texan markets and it is currently hiking its rents by ~20% as leases expire. Despite that, it is priced at a near 30% discount to NAV, which is quite spectacular. Essentially, what this means is that you get to buy high-quality real estate at ~70 cents on the dollar, and you get professional management, diversification, and liquidity for free on top of that. Here is a picture of Satori Frisco Apartments, a community-owned by BSR located in Frisco, Texas:

Apartment community (BSR REIT)

I like to use BSR as an example because it owns some of the most sought-after properties in commercial real estate, and yet, it is still heavily discounted so you can imagine what this means for other REITs.

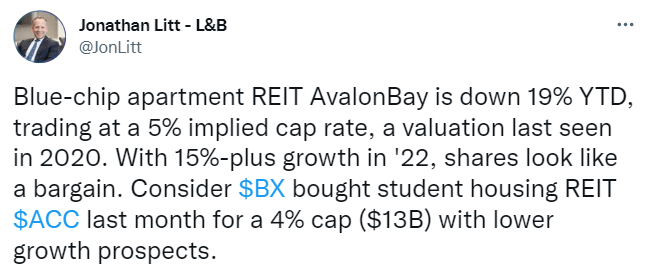

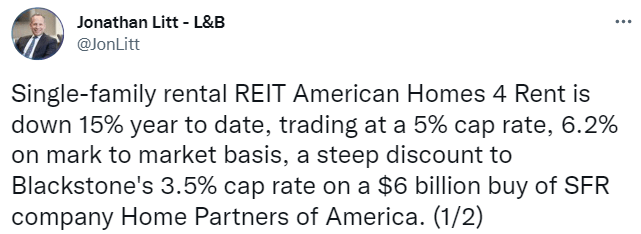

Jonathan Liss, the founder of Land & Buildings (one of the biggest activist REIT hedge funds in the world), has been tweeting about the numerous opportunities in the REIT sector over the past weeks. Here are a few of his tweets regarding BX , ACC , AVB , RHP , and AMH :

AVB is undervalued (Jonathan Litt via Twitter)

{kind=link}

RHP is undervalued (Jonathan Litt via Twitter)

{kind=link}

AMH is undervalued (Jonathan Litt via Twitter)

{kind=link}

What's my point here?

Now is arguably the best time in years to buy REITs.

The only time REITs were cheaper in recent years was early into the pandemic, but the uncertainty was also much greater back then. We were quite literally in survival mode, locked inside, tenants weren't paying rents in some cases, and the GDP dropped by 33% at one point, the worst contraction in history.

In comparison, today's uncertainty is much more bearable.

Yes, inflation is high, but that actually benefits REITs. Their debt is being inflated away, rents are growing the fastest in years or even decades in some cases, and the replacement value of properties is also rising.

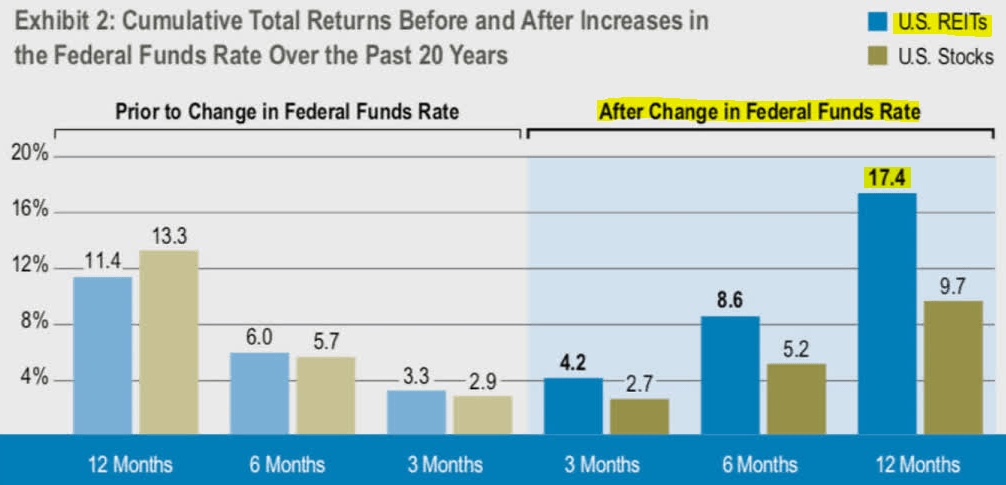

Interest rates are also rising, but since REIT balance sheets are the strongest ever, the impact on interest expense is not significant. In any case, the positive impact of high inflation is much greater than the negative impact of rising interest rates and this is why REITs typically perform so well when rates rise due to inflation:

REITs outperform when inflation is high (NAREIT) REITs outperform during times of rising interest rates (Cohen & Steers)

{kind=link}

But what if we go into a recession? It is a real possibility. But as we have tried to remind you, the impact of a 1-2 year recession should be minimal on the value of properties since their valuations should be based on decades of future expected cash flow. 1-2 years just isn't that meaningful.

Moreover, REITs generally enjoy better downside protection during late cycles and recessions since they often have multi-year leases that protect their cash flow and rents don't change dramatically from one year to another. Today, REITs should be even more resilient since their balance sheets are stronger than ever before:

REITs outperform during recessions (Cohen & Steers)

This is why I believe that now is a great time to accumulate REITs.

Their valuations have recently dropped to the lowest in years, despite strong fundamentals and the tailwind of high inflation.

The REIT market is now offering good real estate that's professionally managed, diversified, and liquid at up to a 50% discount because of near-term concerns that won't last forever.

Of course, we cannot time the market, and prices could dip lower before they recover, but I don't recall ever buying REITs at such valuations and not profiting in the long run.

Therefore, we will continue to execute our accumulation strategy .

We are considering buying more shares of a lot of REITs, but here is our top priority:

- Apartment REITs: Today, our largest apartment REIT holdings ( AVB ; CPT ; etc.) are deeply undervalued relative to their NAV even as their rents are growing the fastest in years or even decades. We believe that they provide some of the best risk-to-reward in today's environment because they are great inflation, interest rate, and recession hedges. Inflation hedges because they can bump rents rapidly as replacement values go up and inflation hurts new development projects. Interest rate hedges because it increases the cost of homeownership and results in a growing pool of renters. And recession hedges because everyone needs a roof over their head. Priced at a steep discount, we will continue to scoop these up.

- Alexandria Real Estate Equities, Inc. ( ARE ): ARE is remarkably cheap right now for a blue-chip, rapidly growing REIT. The company has a clear path to high single-digit FFO per share growth for years to come as it bumps the rents of its expiring leases that are deeply below market. The management expects to increase rents on expiring leases by up to 35% in 2022 as there is significant demand for life-science properties. At the same time, ARE continues to develop new assets at high yields, unlocking the value of its land bank that's largely ignored by investors. Yet, the company is now priced at a 6% FFO yield, the lowest valuation in a long time.

- Medical Properties Trust, Inc. ( MPW ): The company is now near the cheapest it has been since the beginning of the pandemic, trading at 11x AFFO and a 7.2% dividend yield. The market appears to worry about MPW's long triple-net leases. Typically, such leases only have limited contractual rent growth, which can become a problem during times of high inflation. But MPW is different. It actually has CPI adjustments in its leases and this should result in an acceleration in its rent growth in the coming years. Therefore, the recent sell-off makes little sense. It also does not help that short sellers continue to spread rumors about the health of its largest tenants as well as the management of the company, which are unfounded in my opinion. I will send an email to the management team to organize an interview for members of High Yield Landlord. If you have any questions for them, let me know in the comment section below.

- STORE Capital Corporation ( STOR ): We already mentioned STOR earlier. In short, this is arguably the best business model of all net lease REITs and you can now buy it at its highest yield ever (if you ignore the temporary crash of early 2020 when everything was shut down). The yield is nearly 6%, which is extraordinary for a REIT of this quality. Just the yield and growth alone should result in 12-15% annual returns. That's ignoring the 50%+ upside potential from multiple expansion.

- Outfront Media Inc. ( OUT ): The billboard REIT is now 40% below pre-pandemic levels, even despite the fact that its business has almost fully recovered from the crisis. If we experience a recession in the near term, its business could suffer a bit, but the long-term value of the business is largely unchanged, and it is now priced at a steep discount due to the excessive focus on short-term results. The upside potential is 50-100% as it recovers and while you wait, you earn a 7%+ dividend yield.

Bottom Line

If you missed the bargains of the early covid-19 crash, now you are essentially given a second chance, so don't miss it.

Opportunities are abundant and the time to be greedy is when others are fearful.

You can expect us to make a lot more portfolio additions in the coming weeks and months.

For further details see:

The Market Is Crashing: Here's What I Am Buying