VTI - The Market Thinks The Fed Hasn't Done Enough

2023-09-21 13:13:02 ET

Summary

- The Fed decided to hold off on a rate hike in September, with expectations of only 2 rate cuts in 2024.

- Some FOMC members believe the neutral rate is higher than previously thought, according to the rise in the central tendency of the long run rate.

- Based on the bond market's reaction in less than 24 hours, it seems clear the Fed hasn't done enough.

Unsurprisingly, the Fed decided to skip the rate hike in September. The dot plot came in much more hawkish than expected, as the Fed now only sees two rate cuts in 2024, which is down from 4 rate cuts in June. More surprising than that was that the central tendency of the long-run rate rose, suggesting that some FOMC members are starting to believe the neutral rate is higher than previously thought.

Powell commented two times during the press conference that the neutral rate for the economy may prove to be higher than thought. But it seems clear that the Fed isn't quite sure where the neutral rate is. If the Fed isn't sure where the neutral is, then how can the Fed be sure that policy is sufficiently restrictive to achieve its 2% inflation target?

The Market Forecasts Even Higher Inflation

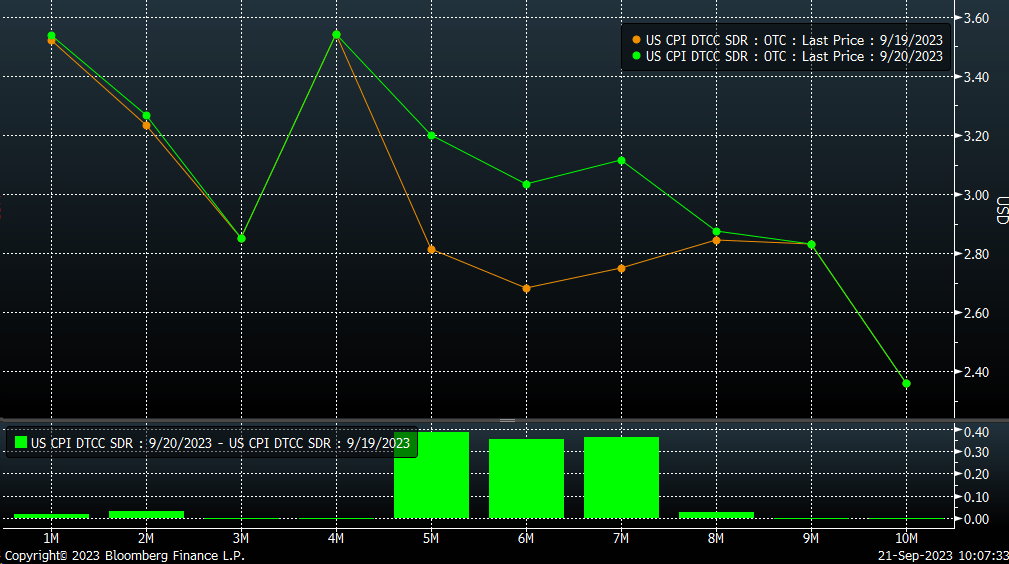

At least, at first blush, it doesn't seem like the inflation swap market thinks monetary policy is sufficiently restrictive. Because headline inflation swaps now expect CPI to be above 3% for the next 6 out of 7 months. CPI Swaps now see headline CPI above 3% in September, October, December, January, February, and March. The astonishing part is that on September 19, just one day earlier, Headline CPI was expected to be below 3% in January, February, and March. Indeed, it is not what one would expect to see if the market thought the Fed was over-tightening.

{kind=link}

Not Restrictive Enough

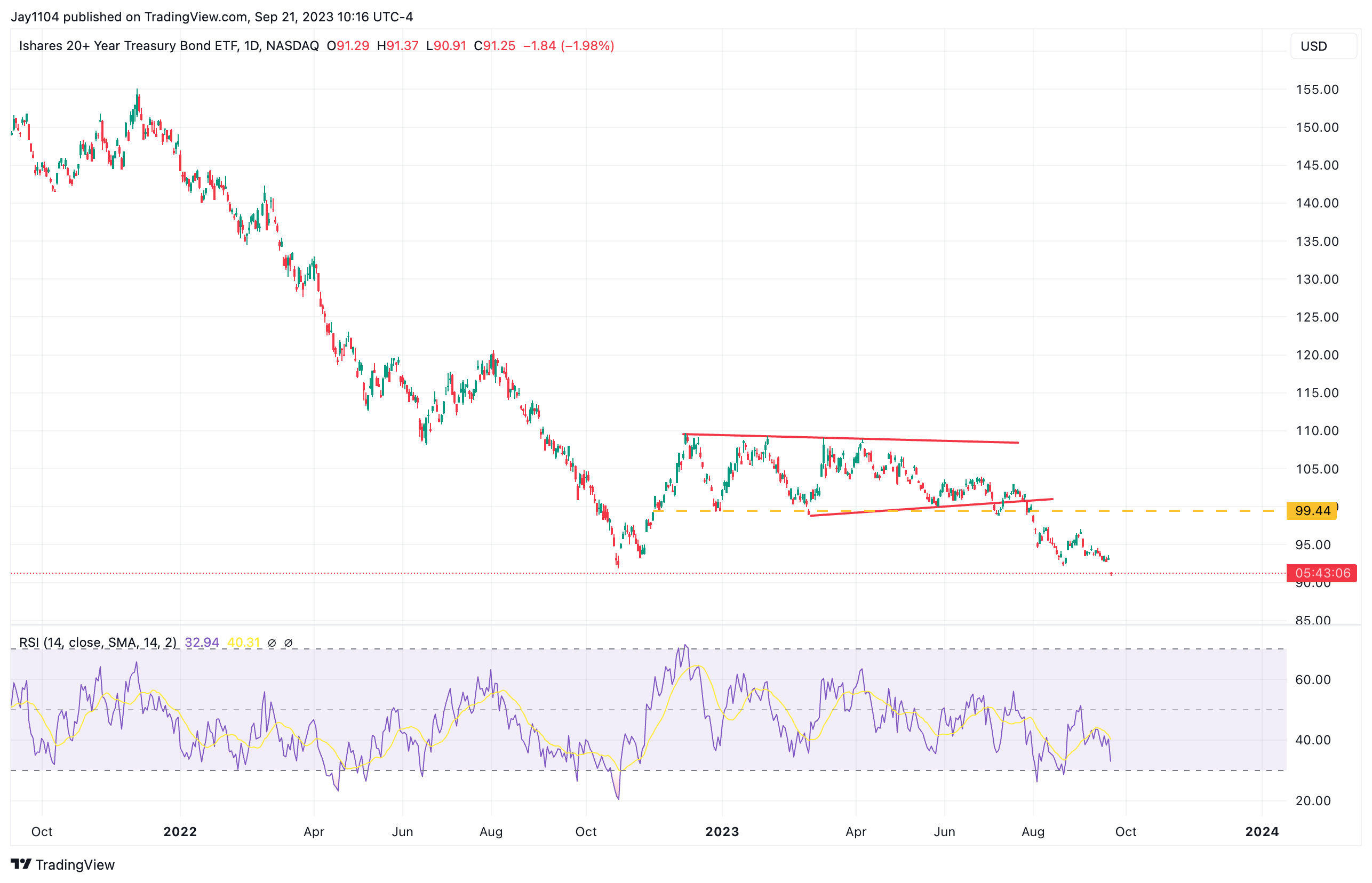

Additionally, we have seen rates across the entire nominal yield curve move beyond October 2022 highs, which shouldn't be surprising, as this has been my main focus for months . Because the economy has held up better than expected, inflation has remained stickier than predicted, and commodities like oil and gasoline have risen. This has sent ETFs like the iShares 20+ Year Treasury Bond ETF ( TLT ) to fresh 52-week lows.

{kind=link}

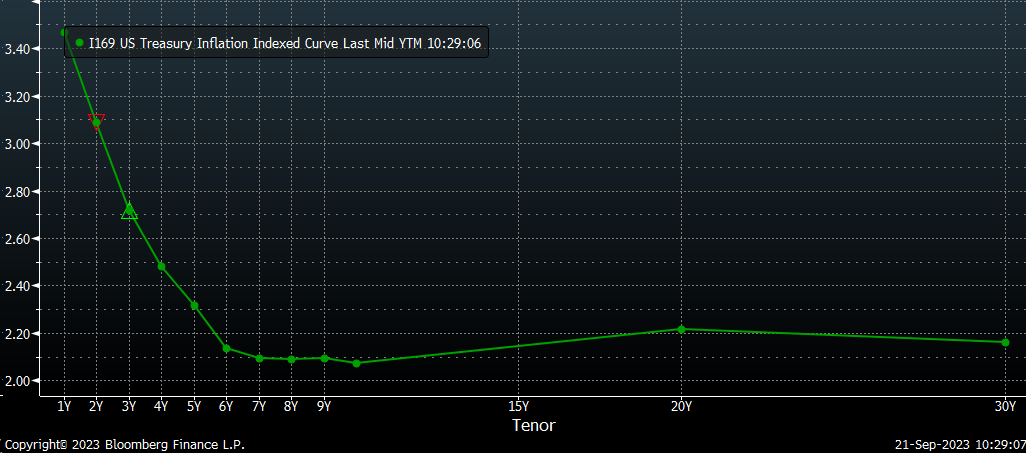

In the meantime, real yields have also exploded higher, with the 10-year real yield now trading at 2.1%, which again points to higher nominal rates over a longer period, and that monetary policy at the current level doesn't seem to be restrictive enough to sufficiently bring inflation down to the Fed's 2% target.

The TIPS curve is now trading easily above 2%, and one has to think this is the market's way of saying that rates are not sufficiently restrictive and the Fed's targeted rates for beyond 2024 are too low.

{kind=link}

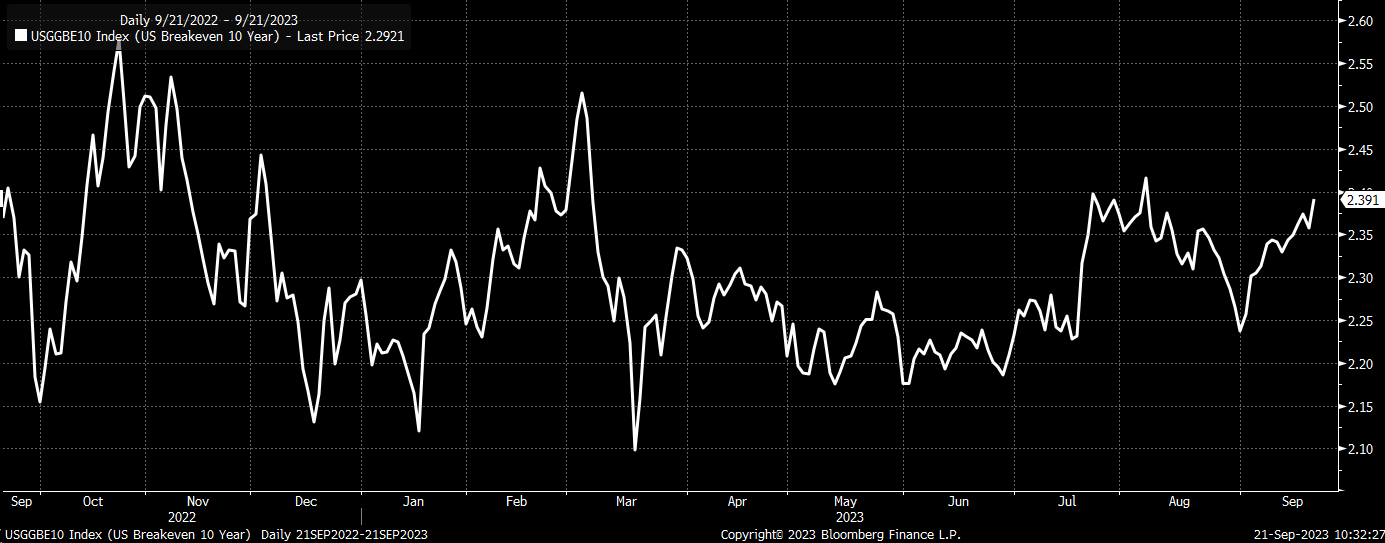

This is because 10-year break even's are rising and trading back to 2.4%. Inflation expectations should be falling at this point, with nearly 550 bps of rates in the past 18 months; if the market believed the Fed was restrictive, inflation expectations should fall, but instead, they are rising. The market seems to be signaling that the Fed hasn't raised rates enough and that the Fed's projected policy path will not be restrictive for long enough.

{kind=link}

Pain For Stock Yet To Come

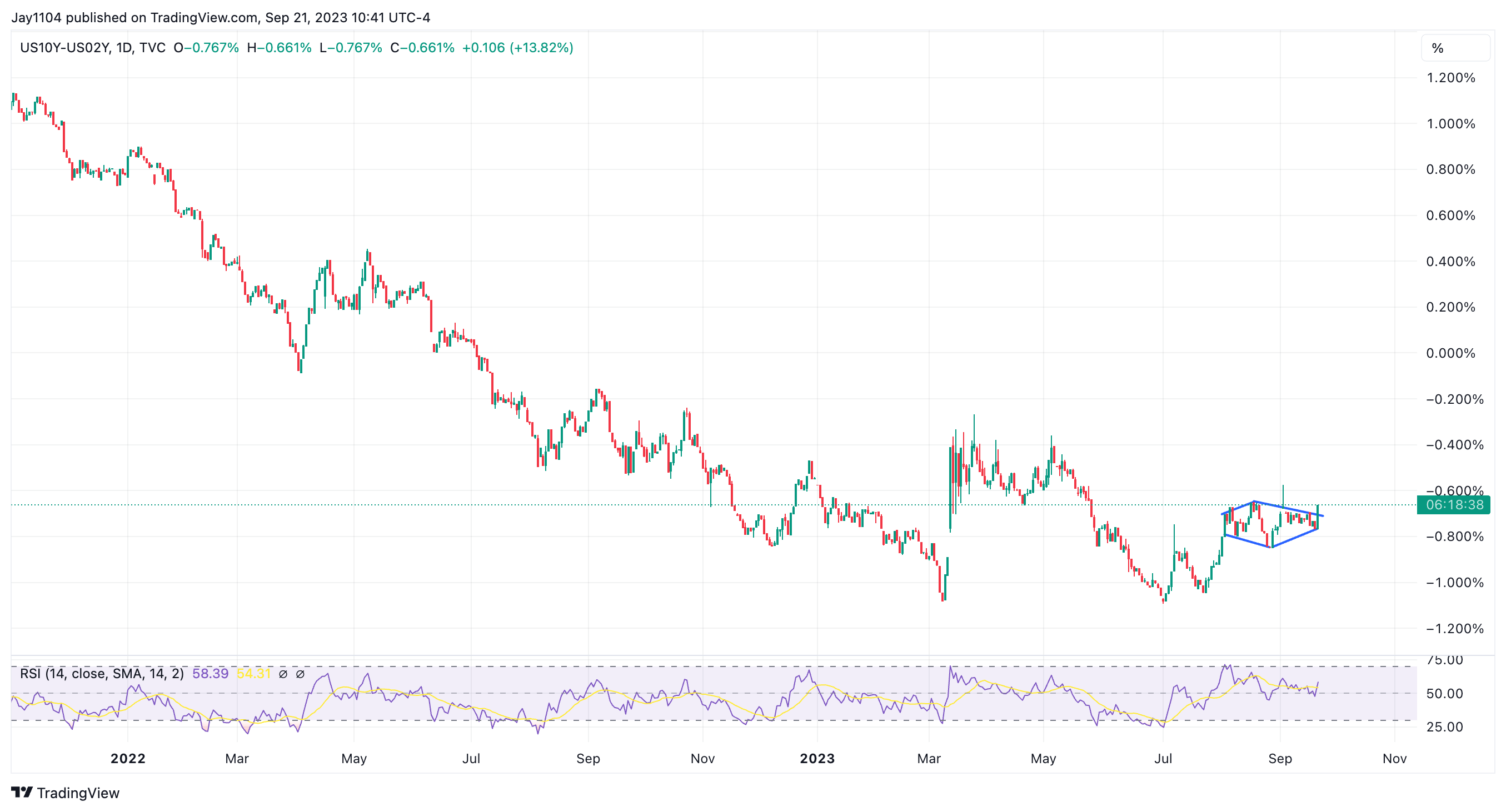

So what appears to be happening now is that the bond market will do the work for the Fed. Bond rates in nominal and real terms will keep rising until they have reached a point where they ring out all of the inflation, and unfortunately, that means that the yield curve will have to re-steepen, with the 10-year rising to the 2-year. That won't be a recessionary signal either; that will be a bear steepen-er and a painful process for the equity market.

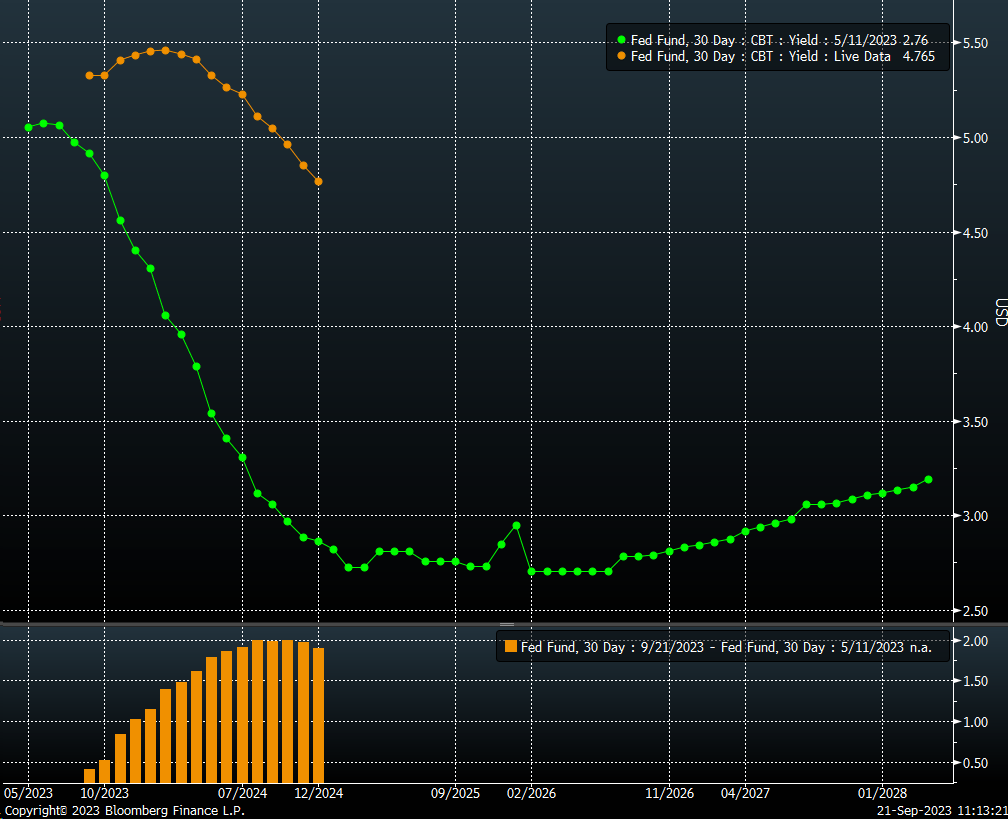

Mainly because following the May FOMC meeting, the equity market had it stuck in its head that the Fed would start to cut rates aggressively in 2024. Back then, the Fed Fund Futures saw December 2024 rates at around 2.87%; today, those same contracts trade at 4.77%, 190 bps higher, yet stock prices are higher than in May.

{kind=link}

The equity market either ignored or forgot about the most significant risk, which I have noted, which wasn't a recession but higher Fed Funds rates and, more importantly, higher rates at the back of the curve, and that is precisely what we are now seeing take place.

{kind=link}

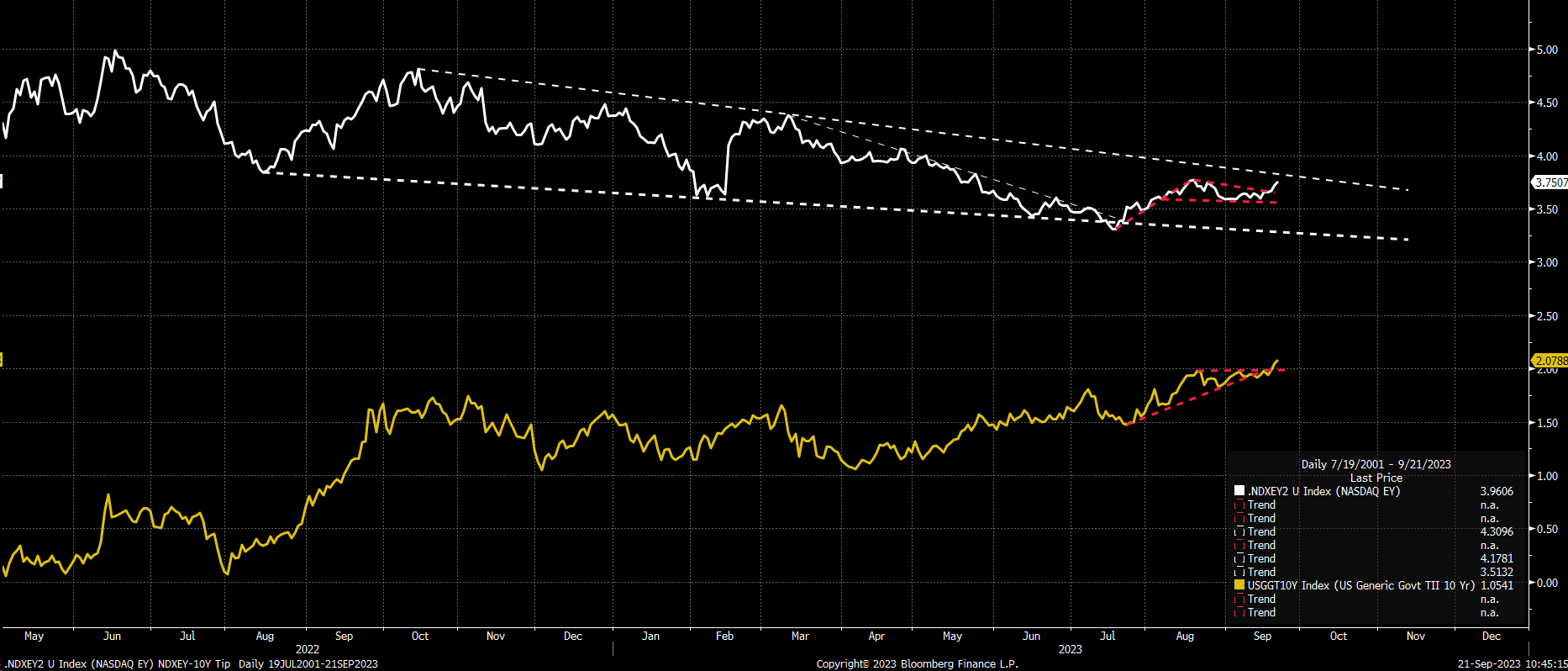

This means that stocks should fall because, at the end of the day, if all yields rise, the stock market's earnings yield also needs to increase. The earnings yield of the NASDAQ 100 has been steadily falling despite the 10-year real yield steadily rising since April. But it seems stocks finally woke up because, since the end of July, the earnings yield of the NASDAQ has again been increasing with the 10-year real yield.

{kind=link}

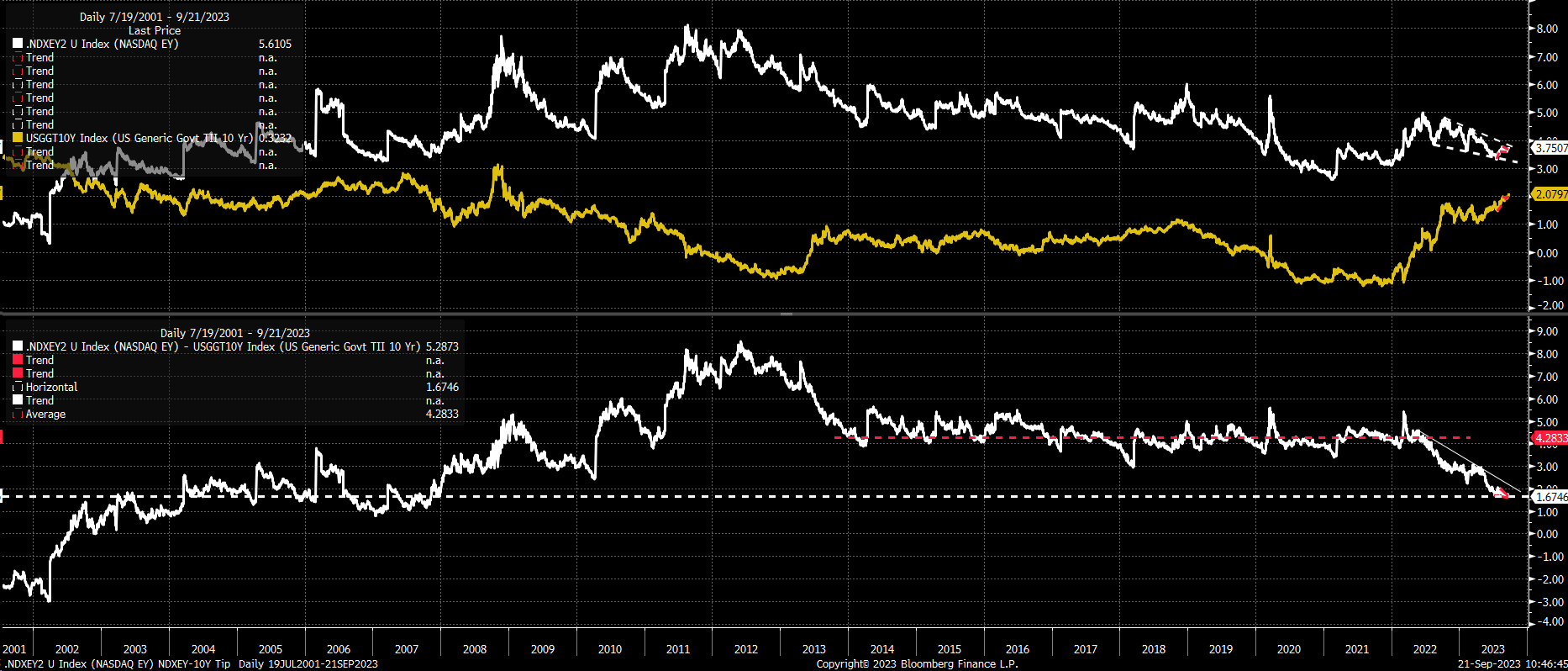

But the bigger question is the spread between stocks and bonds, which narrowed to just 1.7%, a level not seen since the mid-2000s. The spread doesn't have to widen by much to inflict severe pain on the NASDAQ 100. If the spread widens by 110 bps to 2.8%, which is where it was in May, it could result in a more than 20% decline in the Nasdaq 100. Even at the April spread of 2.8%, it would still be well below its historical average of 4.4% over the past ten years, which would still be 260 bps higher.

{kind=link}

If the Nasdaq 100 earnings yield rose from its current 3.75% to 4.85%, it would be like the P/E ratio falling to 20.6 from its current 26.7, equal to a decline in the P/E ratio of 22.7%. If the Nasdaq 100 earnings yield climbs by 260 bps to 6.35% from the current 3.75%, that would be like the P/E ratio falling to 15.7, which means the multiple contracts are 41%.

Just by looking at how the bond market is responding to the FOMC meeting on Wednesday, it seems crystal clear that rates want to go higher, and higher rates mean lower prices for almost everything, yes, stocks, too.

For further details see:

The Market Thinks The Fed Hasn't Done Enough