DCBO - The Momentum Shift: Docebo Is Losing Its Pace

2023-05-17 09:43:32 ET

Summary

- While Q1 2023 results showed significant revenue growth, Docebo's pace of expansion seems to be slowing.

- Customer acquisition, while still ongoing, is showing a downward trend compared to previous years.

- Despite now generating consistent profits, Docebo's performance on the 'Rule of 40' benchmark suggests it may not be meeting Wall Street's expectations.

Docebo Inc. ( DCBO ), a dynamic tech firm, has swiftly carved out a significant niche for itself in a relatively short time. However, recent quarterly results reveal that it's grappling with the challenges of a tough economic climate and is now facing a challenging future.

Strong Growth

Docebo, a rapidly expanding SaaS company hailing from Toronto, has carved out a niche for itself in the learning management systems [LMS] sector. Their specialty? Helping organizations train their workforce efficiently and effectively. Just look at the numbers - Docebo's revenues have skyrocketed from under $10 million in 2016 to a staggering $143 million last year.

It's not just about the growth, though. The company has garnered a reputation for its innovative AI-powered, cloud-based platform. This platform has wooed some of the industry's top players, including heavyweights like Amazon Web Services (AWS), Thomson Reuters (TRI), HP Inc. (HPQ), and BMW (BMWYY).

Moreover, Docebo's customer base is impressive and continually expanding, now boasting more than 3,500 clients. They keep adding new significant customers each quarter, a testament to the strength of their product, in my opinion.

{kind=link}

Image Source: DCBO Investor Presentation

Financial Highlights: A Closer Look

Docebo's recent quarterly results , released last week, showcased decent revenue and earnings growth, coupled with significant additions to its client roster. In Q1 2023, the company saw a 29% surge in revenues compared to the same period last year, hitting $41.5 million. In constant currency terms, this translates to a 32% rise.

The company operates on a subscription-based business model, with subscription revenues typically accounting for over 90% of total revenues. In the previous quarter, subscription revenues climbed 33% to $38.8 million, making up 94% of total revenues.

Docebo has been intently working on bolstering its profitability. The company has a history of losses, but its recent focus on enhancing profits is evident in its results. In my opinion, this turnaround ability, even amidst a challenging economic landscape, is one of Docebo's key strengths. The company reported a GAAP profit of $1.24 million for Q1-2023, a significant turnaround from a loss of nearly $7 million the previous year. After adjusting for one-off items, the company swung to an EBITDA of $2.2 million from a loss of $1.3 million a year earlier. Its adjusted net profit stood at $0.09 per share, a stark improvement from an adjusted loss of $0.05 per share a year earlier.

Losing Steam

In my view, Docebo is on the right trajectory. However, the speed of progress may not be up to the expectations of shareholders. When we contrast the company's current performance with previous quarters, it's clear that while its bottom line has improved, it's also feeling the pinch of the economic slowdown.

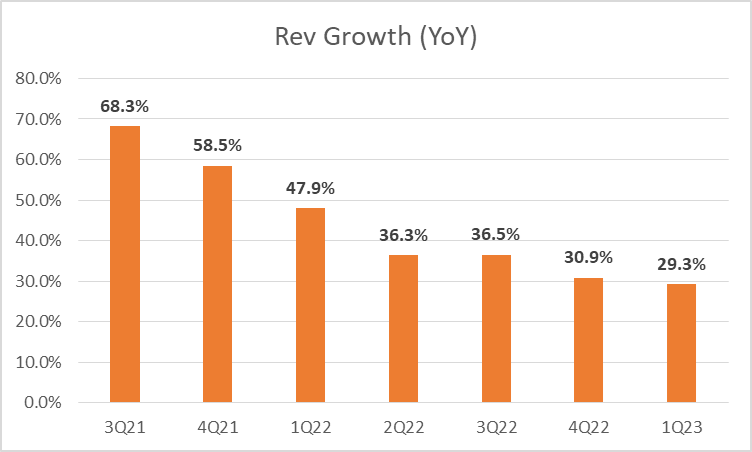

Docebo has consistently delivered double-digit revenue growth, but it's evident from recent trends that this growth rate is decelerating. For instance, in 2021, the company was clocking in quarterly revenue growth exceeding 60%, a figure which has now fallen below 30%, as illustrated in the accompanying graph.

{kind=link}

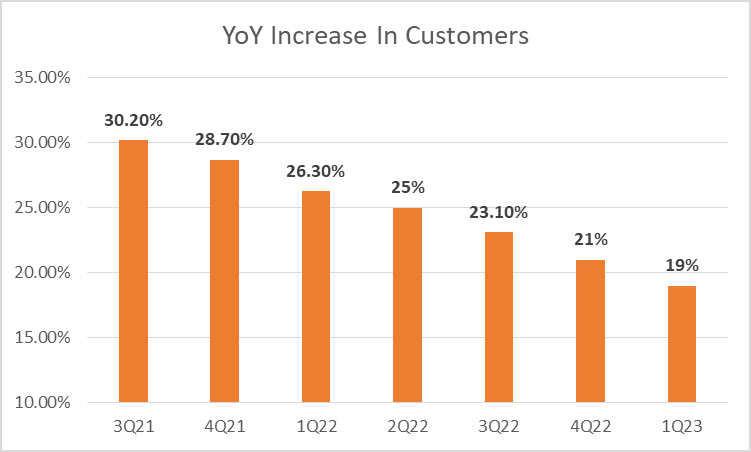

In terms of customer acquisitions, there's a similar trend. Don't get me wrong; Docebo is successfully onboarding new customers, which is a testament to the market's demand for their products. In Q1 2023, they welcomed 112 net new customers, including names like Vimeo and Freedom Mortgage. They've also made strides in the European market, attracting major corporations and striking deals with top-tier companies, including a leading transportation and logistics services provider operating across 160 countries.

So, the performance seems solid on the surface, but is it sufficient to curb the downward trend or at least stabilize it? Unfortunately, in my opinion, it doesn't appear so. In 2021, Docebo reported a nearly 30% year-over-year increase in its customer base. Fast forward to the present, and we see a sharp drop, with the company announcing only a 19% increase in customers in Q1-2023.

{kind=link}

The management attributes the slowdown to macroeconomic vulnerabilities, including recent issues within the banking sector, affecting their "small and mid-sized customers." This challenging environment is causing anxiety among the company's clients, thereby impacting their spending habits. This predicament is not unique to Docebo, as numerous other SaaS companies are grappling with similar issues.

For instance, I recently wrote about Five9 ( FIVN ) - another SaaS company with a superior product and a robust customer base - which, akin to Docebo, is experiencing pressure on its revenue growth. Five9 recently reported a 20% increase in revenues for Q1-2023, following a similar growth trajectory in Q4-2022. Although this growth is commendable, it represents the company's slowest growth rate in over three years.

Moreover, Docebo's management appears to have increased its focus on delivering profitable growth, as opposed to aggressive growth, which has further influenced the company's expansion rate. In an effort to protect its bottom-line, the company has implemented cost-cutting measures, including trimming expenses in the sales and marketing department. The company is reducing its workforce by 5%, with the sales and marketing and G&A sectors being primarily affected. This could have had a detrimental impact on growth. Conversely, this strategy has enhanced the company's profitability, although the progress has been gradual.

Docebo is now consistently yielding profits, marking the previous quarter as its second consecutive one in the black. While this trend is undoubtedly a step in the right direction, the profit margins, coupled with the rate of top-line growth, might not meet Wall Street's expectations.

To gauge Docebo's performance, we can apply the 'Rule of 40', a benchmark often used in the SaaS sector. This rule suggests that the sum of a company's revenue growth rate and profit margin should ideally be 40 or above. Regrettably, Docebo has consistently fallen slightly short, with this metric wavering between 35 and 38 over the past four quarters.

{kind=link}

From the table above, the crux of the issue becomes clear. Although Docebo continues to grow its revenues, this growth isn't accelerating at the desired pace. Concurrently, while the company is posting profits, the margins remain thin.

Uncertainty Ahead

At this juncture, it's uncertain whether Docebo has hit a turning point, and if a recovery is imminent. There's a cloud of ambiguity, but in my opinion, given the economic climate, the company may face downside risks. To put it plainly, Docebo might face further hurdles before things start looking up.

The economic slowdown is already leaving its mark on Docebo's financials. US economic growth has decelerated due to the Federal Reserve's aggressive interest rate hikes - ten increases in just over a year to a range of 5% to 5.25%, the highest in nearly 16 years. This drop in economic activity and rise in borrowing costs will likely dent corporate earnings. Simply put, many of Docebo’s clients could face profit pressures. And this trend may already be underway.

In the last quarter of 2022, the S&P-500 witnessed an earnings decline, and another drop seems likely. With 92% of S&P-500 companies reporting, blended earnings have fallen by 2.5%, according to FactSet. As profits shrink, companies will seek to trim costs, and Docebo could feel the brunt of this.

There's no denying that Docebo offers valuable services enhancing employee productivity and retention, and its learning programs are indispensable for many organizations in today's constantly evolving skills market. However, those firms seeking to immediately safeguard margins and reduce costs in the face of a slowing economy may not be eager to become Docebo clients, or they may postpone their purchase decisions. As a result, Docebo's customer acquisition could falter, meaning all the key metrics discussed above – revenue growth, customer acquisition, and Rule of 40 – may decline in the coming quarters.

I anticipate Docebo's revenue growth will continue to diminish in the upcoming quarters. While I believe the company will maintain profitability, its low EBITDA margins could result in continued underperformance according to the Rule of 40 metric. This could negatively impact the company’s shares.

Final Thoughts: A Cautious Approach

In short, Docebo is a company with a fantastic product, but it finds itself in a tough spot, grappling with slowing growth and tepid profitability improvements. For Docebo, things may get worse before they get better. Consequently, in my opinion, potential investors may want to exercise caution and stay on the sidelines for now.

For further details see:

The Momentum Shift: Docebo Is Losing Its Pace