TPVG - The More You Sell The More I Buy

2023-08-23 07:35:00 ET

Summary

- I use fundamental analysis to find opportunities when others are blindly selling.

- Your dream retirement will need to be paid for somehow, and this can be how.

- We look closer at two victims of recency bias.

Co-authored with Treading Softly

Do you remember what we had for lunch yesterday? How about dinner two weeks ago?

For most of us, we're terrible at remembering things.

It may be that these things are deemed unimportant in our mind and therefore not stored in the long-term memory banks or that we only have so much memory space to be able to store past information. This habit is not exclusive to the meals you've consumed.

When it comes to the market, investors are notoriously bad at having short-term memories. Often investors make decisions that are heavily colored by recency bias – looking only at the last few months, a few years, or even just throwing up a quick chart to look at the five- and 10-year history of a price movement without ever diagnosing any further causes. This can often lead to pricing dislocation. I know that there are many analysts out there who believe in an "efficient market," believing that the market appropriately prices every security over the long term. I'll let you know that I'm not a proponent of this viewpoint. I do not believe that the market is efficient because humans are not efficient. We're way too emotionally driven. We make emotional decisions and are quick to forget.

Today I want to look at two opportunities that people are investing in with short-term memories and failing to look at the fundamentals and therefore are avoiding two outstanding income opportunities.

Let's dive in!

Pick #1: EPR – Yield 7.6%

EPR Properties ( EPR ) is a REIT that focuses on owning "experiential" properties. EPR owns properties where people go to do things – movie theaters, water parks, ski resorts, golfing complexes, and even museums. In short, all the places people don't go when there is a global pandemic, and we're all supposed to be social distancing.

In the past, we've praised EPR management for its ability to navigate those difficult times. Most of EPRs tenants were unable to pay rent as their revenues crashed to virtually zero. EPR itself managed to maintain a strong balance sheet, exiting the pandemic with about the same amount of debt it had going into it. Additionally, EPR didn't issue equity, and it actually bought some shares back in 2020.

This isn't to say EPR didn't feel the impact. EPR's earnings crashed, and the dividend was suspended. EPR's Funds From Operation ('FFO') as Adjusted hit bottom in Q3 2020 at just ($0.16)/share, down from $1.46 the prior year. For all practical purposes, their business was shut down.

Since then, EPR has been gradually recovering, but it's still seeing some of the tail impacts of COVID. Specifically, while EPR managed to get through COVID without loading up on debt, the same cannot be said for some of EPR's tenants. Cineworld took out hundreds of millions in debt just to remain solvent through the crisis, and late last year, the debt burden proved too great, and it filed for bankruptcy. EPR's shares fell in price as Regal, a subsidiary of Cineworld, was one of EPR's largest tenants.

Fast forward to today, and Cineworld is exiting bankruptcy with substantially less debt. EPR worked out a deal, taking possession of some theaters and modifying the rental agreement for the properties that Regal still occupies. A rental agreement that works in a percentage rent, reducing the amount of rent due right now but providing upside for EPR as revenues recover.

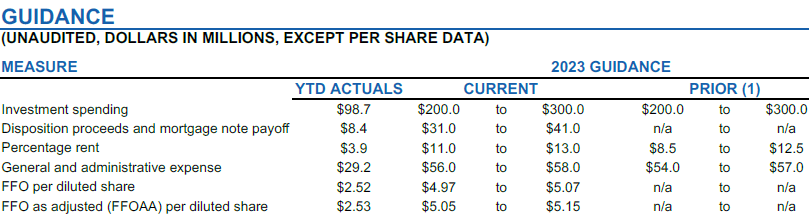

In Q2 2023, EPR reported FFO as adjusted of $1.28 and, with the Cineworld bankruptcy behind them, released earnings guidance. Source

{kind=link}

EPR Q2 2023 Supplement

The midpoint of $5.10 represents 9% growth year over year. It compares to EPR's 2019 FFOAA of $5.44. At current growth rates, we can expect that in 2024, EPR's FFOAA will exceed pre-COVID levels.

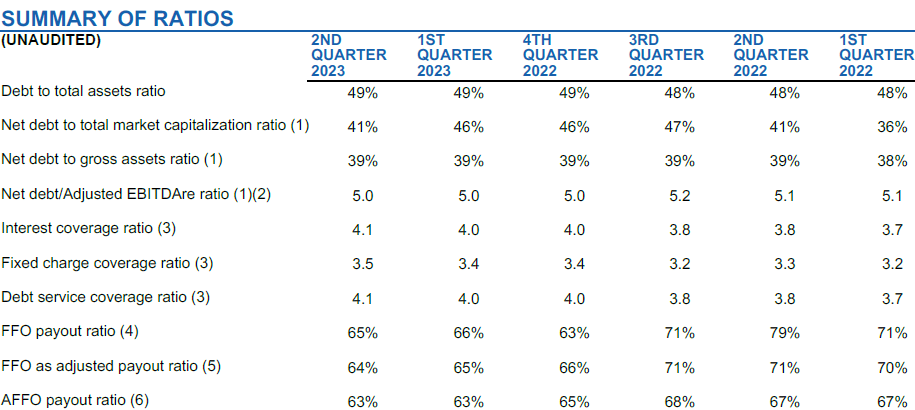

As income investors, our primary focus is on the prospects for the dividend to continue to recover. EPR's dividend is well covered by cash flow, with an FFOAA payout ratio of just 64%. In 2019, this metric was over 80%.

{kind=link}

EPR Q2 2023 Supplement

With the payout ratio declining so much, we are very optimistic about seeing a dividend hike late this year or early next year.

EPR's fundamentals are returning to pre-COVID levels, but the share price remains heavily discounted. This is ideal for income investors like us – a company that's performing well fundamentally but is trading at a very large discount.

Pick #2: TPVG – Yield 14.7%

Last quarter, TriplePoint Venture Growth ( TPVG ) saw its price tank due to its announcement that several portfolio companies were filing for bankruptcy. We suggested buying the dip, and sure enough, the price spent most of the quarter recovering.

This quarter, TPVG reported the same thing, from mostly the same companies, and the market is selling off the same way. We're happy to buy the dip again.

TPVG invests in companies that are backed by venture capital and are being prepared for an IPO. For obvious reasons, the current environment isn't favorable for an IPO. These are companies that typically are "growth" companies, and in good times, they will operate with negative cash flow pursuing a growth-at-all-costs strategy. The venture capitalists are happy to pony up more cash as needed because they understand that a high growth rate at IPO will attract investors and high multiples even if the company isn't profitable. When a company can't IPO in the foreseeable future, venture capitalists have to make a decision: Do they believe strongly enough in the company to keep subsidizing it? Or is it time to take their losses?

So throughout TPVG's portfolio, we are seeing a separation between the winners and the losers. The companies that venture capitalists are doubling down on, and those that they are abandoning. CEO Labe explained the environment like this:

"As venture investors remain -- gain confidence in valuations and valuation metrics, we believe it will enable companies to obtain values based on expectations for future year revenues and exceed their current private valuations. In the interim, many companies will remain on their path of bringing down operating burn to conserve cash and to extend their runways. As we've mentioned before in these calls, the environment for many venture growth stage companies has changed, from business plans of growth at all costs, transitioning into plans of conserved cash at all costs."

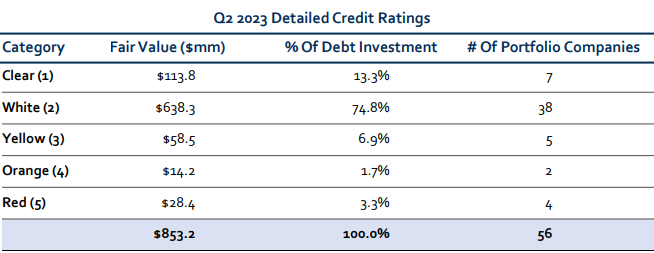

We can see the polarization starting to have an impact on TPVG's internal credit ratings. "Clear" means that the company is outperforming TPVG's expectations. "White" means it is meeting expectations, and below that are the companies that are "on watch" or when you get to Red is where you will find companies that TPVG believes a full recovery is unlikely. Source

{kind=link}

TPVG Q2 2023 Presentation

Last quarter, 15.9% of TPVG's portfolio companies were Yellow or below. This quarter, that has reduced to 11.9%. On average, TPVG's credit quality actually improved over the quarter, however, the $28.4 million in "Red" is new. TPVG also saw a significant increase in "Clear" from $80.5 million in Q1 to $113.8 million in Q2. This is what we mean by the portfolio separating into "winners" and "losers." The companies that are getting support from VCs are doing well and many are exceeding expectations. Those that are not, are deteriorating and becoming more uncertain.

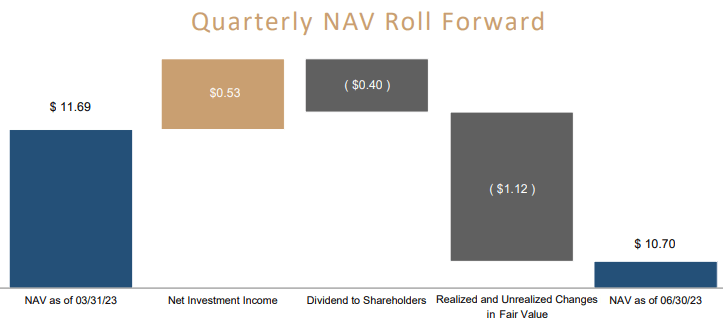

In Q2, TPVGs book value was negatively impacted by $1.12 in unrealized losses, primarily from the companies that were moved into the "Red" category.

{kind=link}

TPVG Q2 2023 Presentation

However, note that TPVG's Net Investment Income significantly exceeded the dividend, which was a $0.13 positive impact on book value. Thanks to high interest rates, the cash flow impact of companies that have stopped paying is offset by higher interest payments from the companies that are doing well.

In fact, TPVG's NII in the first half of 2023 has nearly matched what TPVG did for the whole year in 2019.

TPVG Q2 2023 Presentation

At worst, TPVG will end the year with its second-highest NII ever, and there is a very good chance that 2023 will be TPVGs best year ever from a cash flow standpoint.

It isn't a coincidence that TPVG is seeing the weaker companies in its portfolio experience issues now. The combination of high interest rates, the failure of Silicon Valley Bank shaking up the VC community and a poor IPO environment have created the pressure that tests these companies and the resolve of VCs to support them.

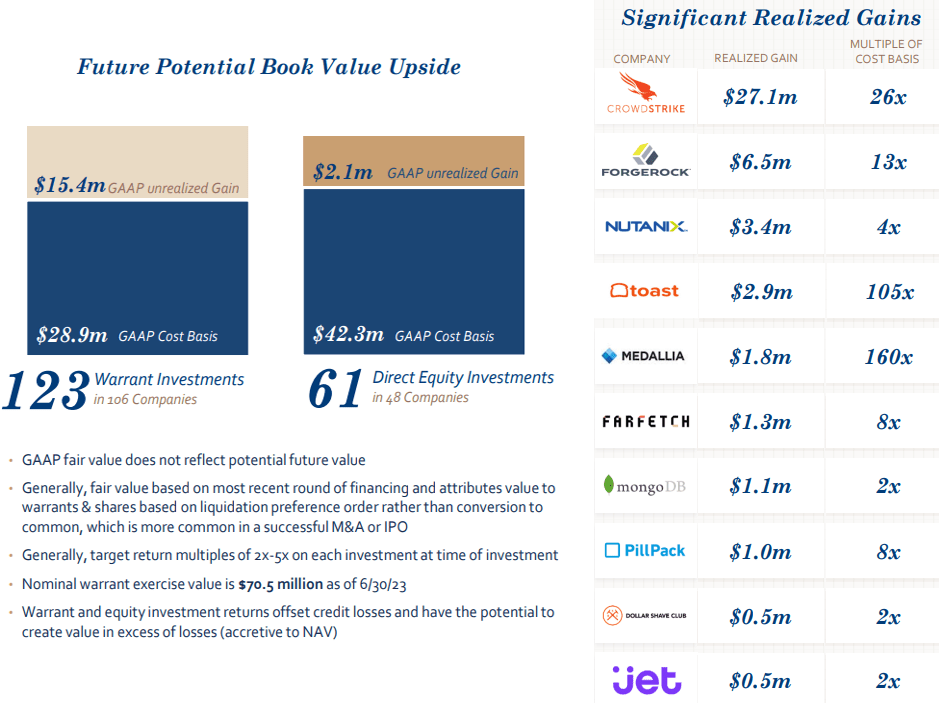

As a result, we can expect that the tide is out, and the companies that aren't going to find support have been exposed. TPVG will seek recovery in or out of court from the companies that failed, and the rest of the portfolio will move on. Book value will be recovered over time through a combination of excess earnings and as the IPO market warms up TPVG still has a lot of potentially large gains embedded in its equity portfolio. Last quarter, TPVG recognized a $2.9 million gain on Toast, a 105x return on its equity investment.

{kind=link}

TPVG Q2 2023 Presentation

Management identified a few of the companies they expect could have significant equity upside as Revolut, WorldRemit, Monzo, Upgrade, Signify, Cohesity, and Passport Labs.

It's a difficult environment for VC companies, but we're seeing a separation of the "winners" and the "losers." The losers are getting the most publicity today, making the headlines by filing bankruptcy and forcing TPVG to mark down the fair value of the investments. Yet on the upside, GAAP accounting rules don't allow for TPVG to mark up its equity holdings to their likely fair value. So in book value, you see the immediate impact of the negative, but not the potential upside of the companies that are doing better than expected and therefore likely to IPO with very impressive returns in the future.

TPVG's business model is getting the 10x, 20x, or even 100x+ gains on equity positions that offset the credit losses inherent in lending in the VC segment. The home runs help offset the strike-outs. TPVG's cash flow is well in excess of its dividend, meaning we can sit back and collect our dividends while we wait for the IPO market to improve and for TPVG to start recognizing the home runs that will be driven by the $113.8 million of investments in the top category, to offset the losses of the $28.4 million of investments in the Red category.

Conclusion

With EPR and TVPG, we're seeing that investors are investing or selling with short-term memory issues. Both of these companies are operating strongly and have been forecasting their steps, meaning that there should be no surprise whatsoever about what is occurring with their portfolios. Yet investors continue to act as if there was new information given that deserves a strong reaction.

At the end of the day, I cannot help investors who are not willing to help themselves. I can write articles to try and educate, inform, and empower investors to make the best decisions possible, and I love doing so. My desire for your retirement is to have the best possible retirement, whatever that looks like for you. I can imagine that almost everyone's dream retirement is going to cost them something, and that cost needs to be paid for in dollars. Those dollars can come from the market through outstanding income investing opportunities.

That's why I work diligently to create professional income investors out of new retirees and novice investors. I try to educate and guide them. One big battle we all often face is a recency bias. Don't let the fear of the recent override logic and judgment when looking at the market. That way, you can have a portfolio full of outstanding income investments, which pay you handsomely for simply being an owner, allowing you to unlock true passive income. This way, you can spend your days doing things that you enjoy instead of having to worry and fret.

That's the beauty of my Income Method. That's the beauty of income investing.

For further details see:

The More You Sell, The More I Buy