MOS - The Mosaic Company: Good Growth Prospects With Limited Downside

2023-12-19 03:23:20 ET

Summary

- The Mosaic Company is a leading producer and marketer of phosphate and potash crop nutrients, accounting for a significant portion of global production.

- The company experienced extraordinary growth in revenue and profitability post-pandemic, driven by rising prices for phosphate and potash.

- The demand-supply dynamics in the agriculture market, including the Russia-Ukraine war and adverse weather conditions, are expected to support elevated grain and oilseed prices and drive demand for fertilizers.

- Company is trading near its book value and has limited downside risk, making it a good buy.

Business Overview

The Mosaic Company ( MOS ) is the world's leading producer and marketer of concentrated phosphate and potash crop nutrients. The company serves approximately 40 countries and accounts for 12% of estimated global annual phosphate production and approximately 14% of estimated global annual potash production.

The company operates in three segments, namely, the phosphate segment, the potash segment, and the Mosaic Fertilizantes segment.

Net sales and gross margins by segment for 2022. (10k FY22)

Recent Financials

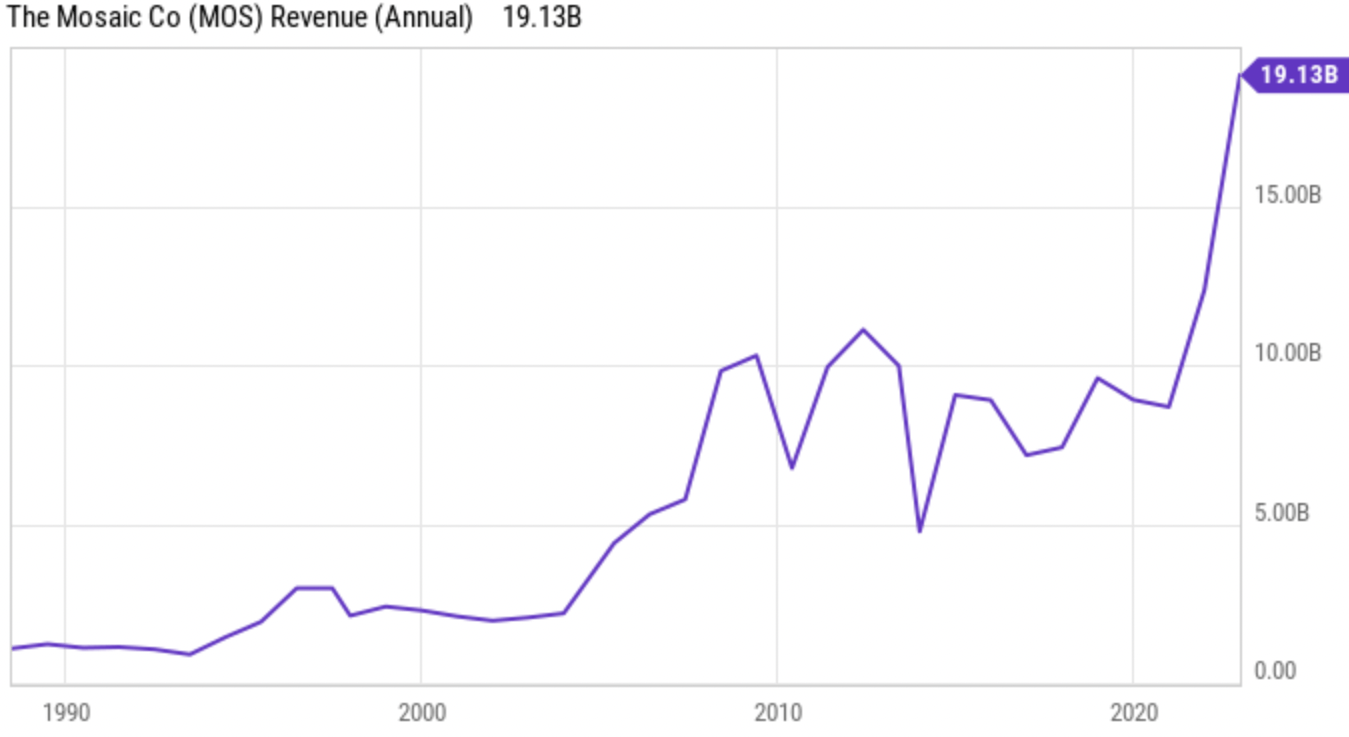

Before the pandemic, MOS had witnessed little to no growth in its topline and was delivering revenue in the range of $7 billion to $9 billion annually. Post-pandemic, the company witnessed extraordinary growth in its topline, reaching $19 billion in FY22, more than doubling the pre-pandemic levels. This phenomenal growth was largely driven by the sharp rise in average selling prices. The company started to benefit from rising phosphate and potash prices by early 2021 due to tightness in the global supply chain, which was further accentuated in FY22 by the Russia-Ukrainian war.

{kind=link}

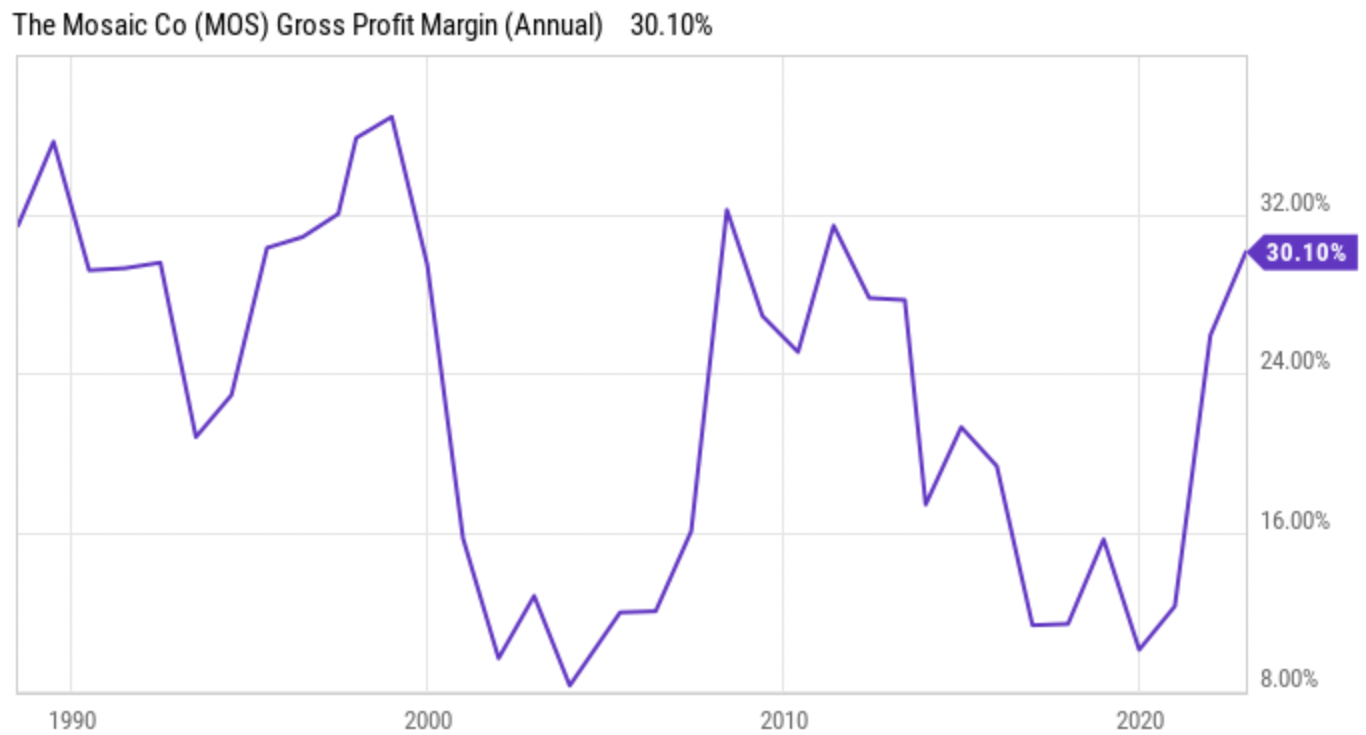

The higher ASP also benefited the company's margins and bottom line. MOS's gross profit margin rose from the 10% - 16% range (pre-pandemic) to close to 30% in FY22. The growth in topline as well as margins resulted in a significant increase in normalized diluted EPS, which rose from less than $1 (pre-pandemic) to $8.6 in FY22.

{kind=link}

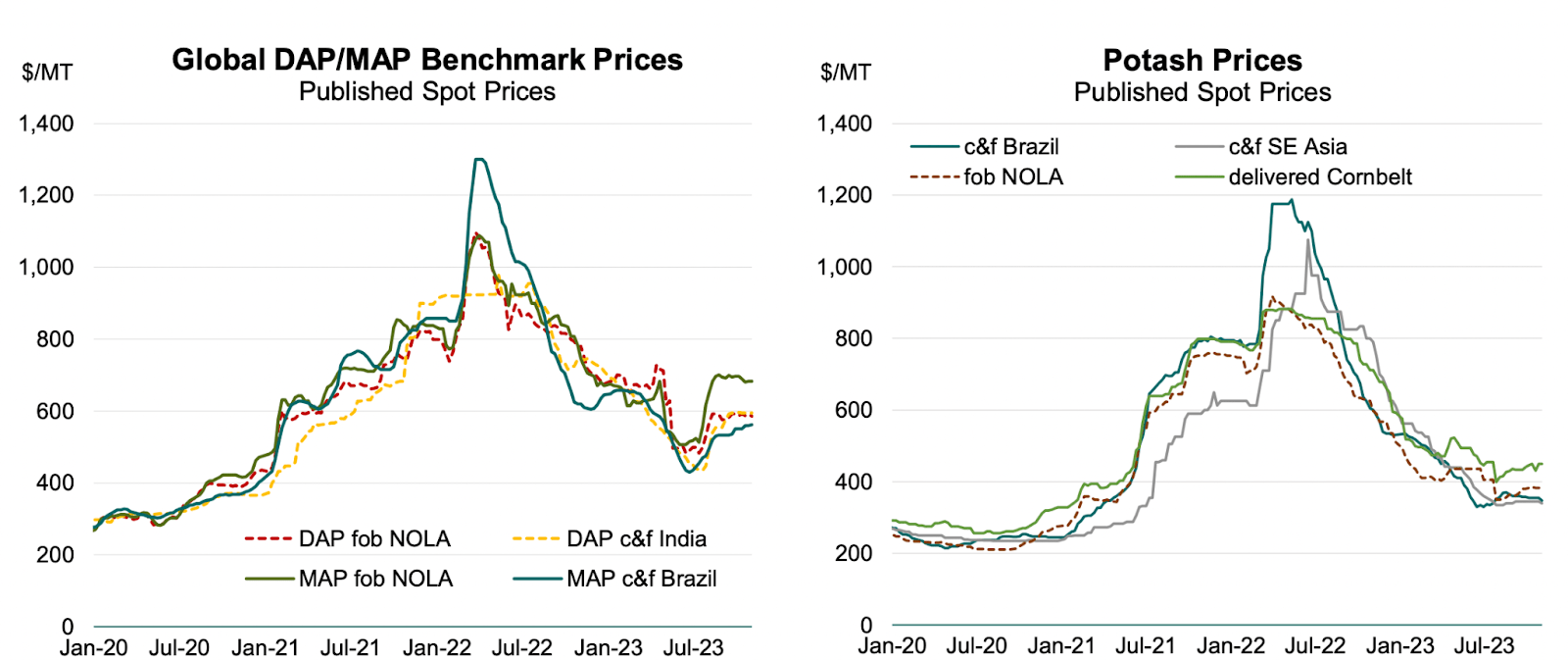

It is evident that a large part of the rise in all three key metrics—topline, margin, and bottom line—is primarily due to a significant rise in the prices of potash and phosphate. However, prices for these commodities peaked in the first half of FY22 and continued to correct, resulting in a weak performance in the first three-quarters of FY23.

Phosphate and Potash benchmark prices (Company presentation)

{kind=link}

Although global phosphate and potash prices have corrected considerably from their peak, they are still above pre-pandemic levels, and I believe they should continue to do so due to factors outlined in the next section.

Future outlook

Before understanding the fertilizer market, one should understand the agriculture market and demand-supply dynamics. Higher demand and constrained supply for agricultural produce lead to higher prices and incentivize growers to use fertilizers to increase yields.

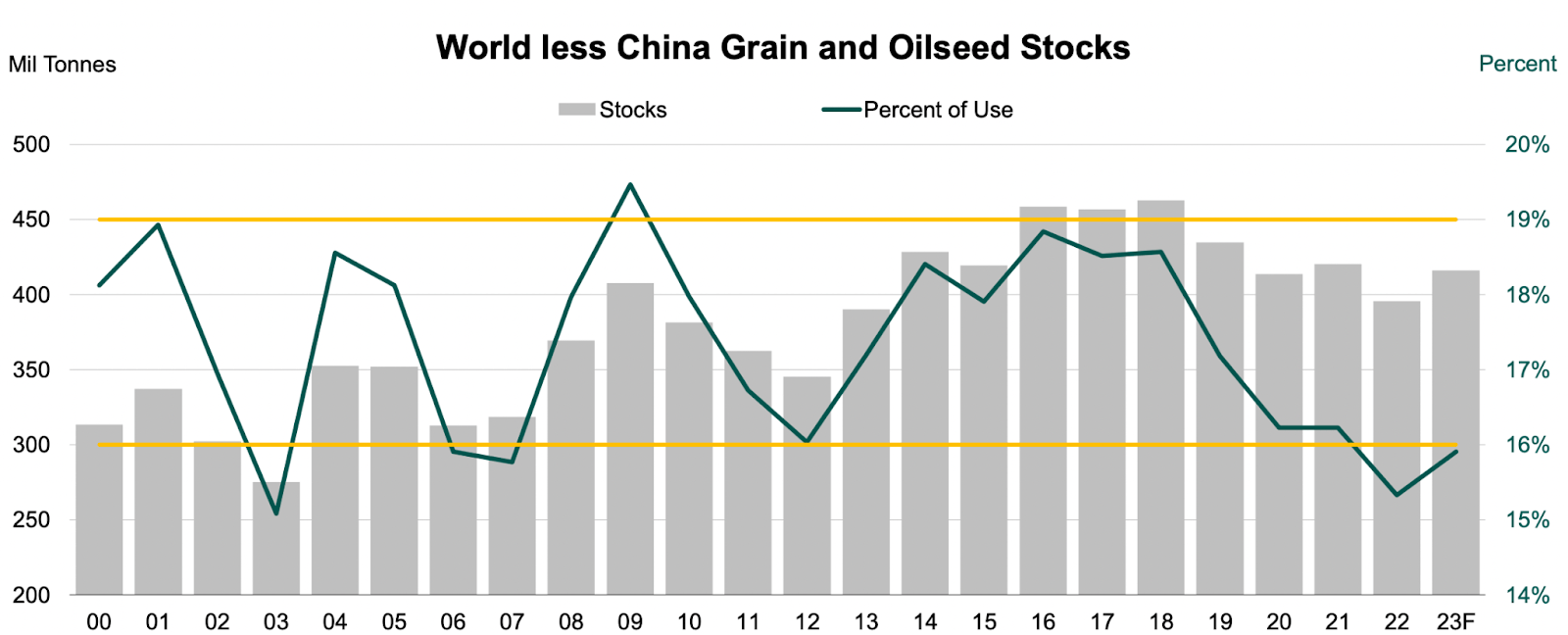

The broader agriculture market fundamentals remain constructive. Demand has remained robust with constrained supply around the world. The world excluding China grain and oilseed stock-to-use ratio is near a historic low of 16%. The last time these levels were seen was in 2012.

World less China Gain and Oilseed Stock (Company presentation)

{kind=link}

I believe the shortage should continue due to the factors mentioned below.

-

Russia-Ukraine war: Ukrainian grain and oilseed exports have declined by 32% from pre-pandemic levels. Efforts to move Ukrainian supply to the world market failed as the UN Black Sea grain deal collapsed, and it is unclear when the supply can be resumed.

-

Adverse weather conditions: Adverse weather conditions particularly in the recent past have become more common hurting crop yields around the world. Currently, the El-Nino weather event is hurting crop yields in southeast Asia and Australia which is expected to continue till spring next year .

-

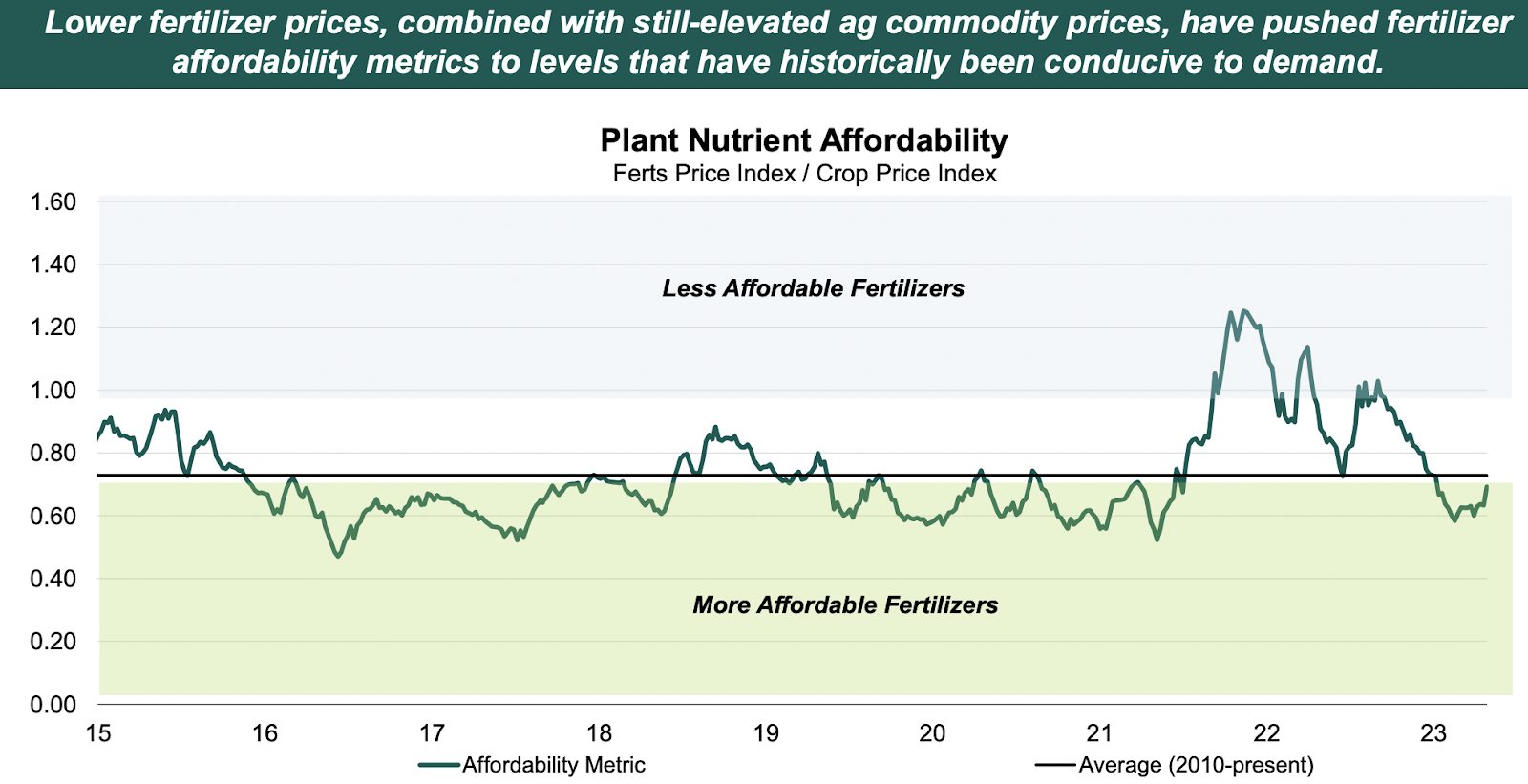

Under-fertilization: Since early 2021 plant nutrient affordability indexed (fertilizer price index/crop price index) has increased substantially. This means that the growers were paying more for fertilizers as compared to what they were earning from their produce. This affordability issue resulted in lower use of fertilizers in the last two years resulting in lower yields.

{kind=link}

These dynamics should serve as good fundamentals for elevated grain and oilseed prices for the foreseeable future. The elevated grain and oilseed prices should incentivize growers to use fertilizers that are more affordable than they were in the last two years.

The green shoots on the demand side are already visible. As of 3Q23 North American MOS’s phosphate and potash shipment rose to the highest level in the last 5 years.

On the phosphate and potash supply side, the dynamics look good too for MOS. Russia and Belarus were the world's top potash exporters after Canada before the Russia-Ukraine war. After the imposition of the sanction on both Russia and Belarus, their potash export suffered significantly leading to a 45% and 61% decrease in exports respectively. These lower export levels are expected to improve in the future as both countries will find new ways to export to other countries. However, any significant improvement is not likely as the war is still going on and the Western countries are not likely to waive sanctions.

For phosphate, China had emerged as a leading supplier in the last decade supplying ~30% of the seaborne market. But now China is shifting its production of phosphate from agricultural use to industrial use such as in the production of lithium iron phosphate. As a result, MOS’s management expects the Chinese export of phosphate to be 7-8 million tonnes in 2024 which is ~3-4 million tonnes less than in 2021.

Overall, I believe the demand and supply dynamics for phosphate and potash to be quite favorable for MOS which should help the company to maintain or possibly increase margins and absolute profits in the coming future.

Valuation and Conclusion

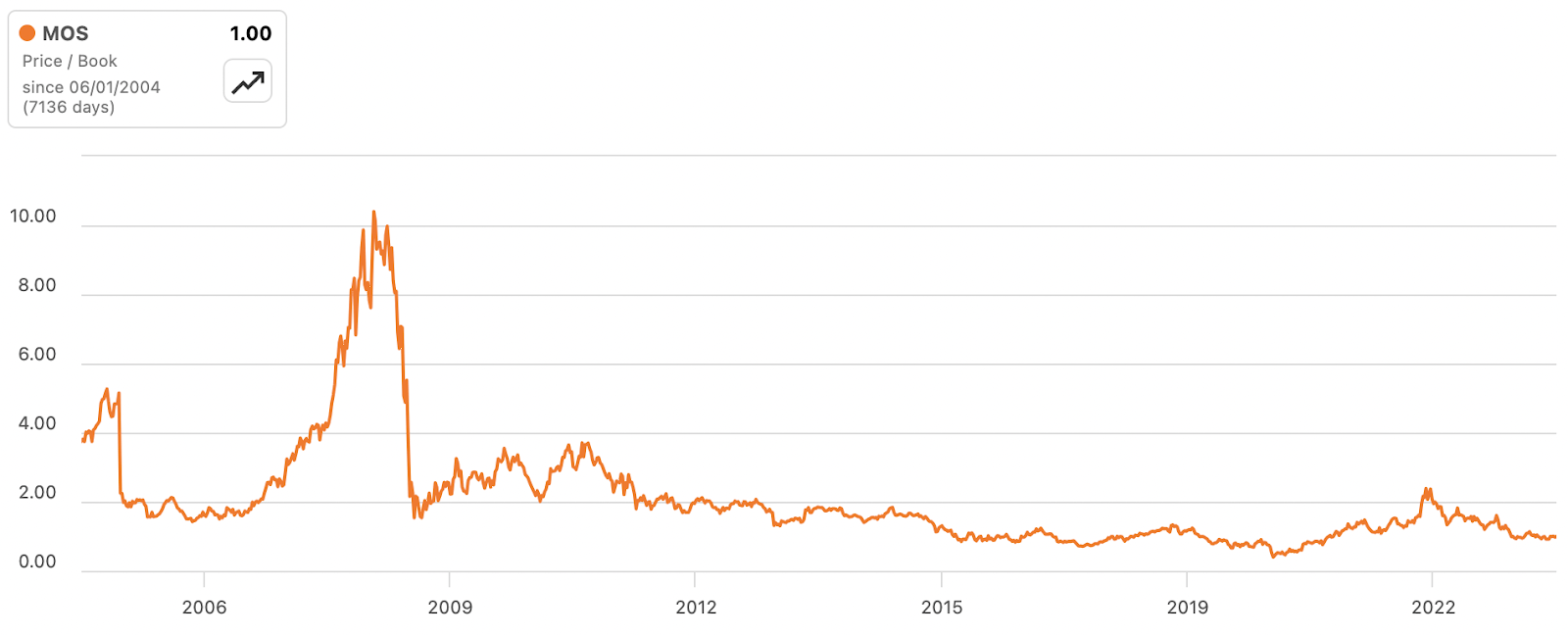

I am using the price/book ratio to evaluate MOS’s stock. The current price/book ratio stands at 1x which means that the company’s market value of all the outstanding stocks is equal to all assets minus liabilities. For the majority of MOS’s history, it had traded above its book value. However, there were periods between 2016 and 2020 when the company traded slightly below its book value and way below its book value in the pandemic crash.

{kind=link}

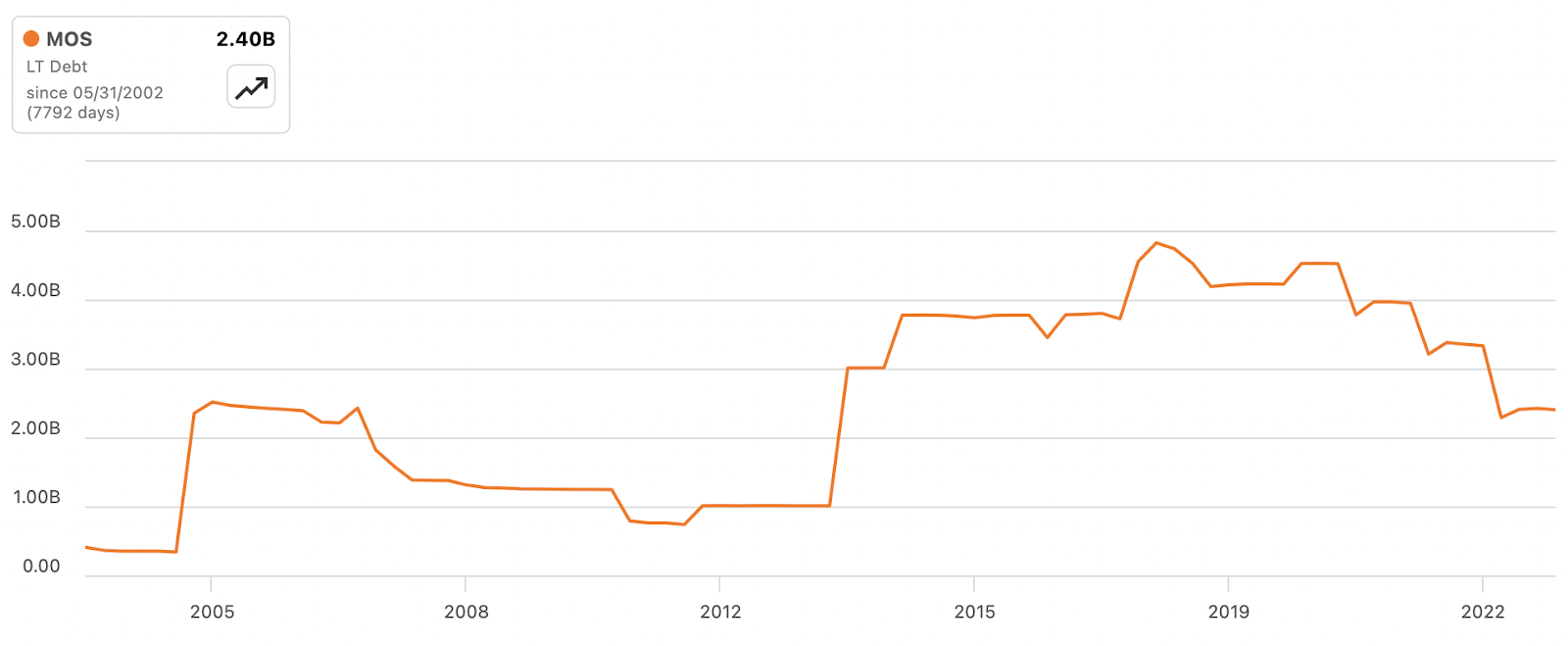

Although the company has occasionally gone below 1x price to book value in its history primarily during the pandemic and 4 years prior to the pandemic. During these times the company has significantly higher levels of debt as compared to now which explains the occasional drop of market cap below book value.

{kind=link}

The company’s balance sheet is in better shape now than it was earlier. I don't believe that the company has much of a downside from here.

While the downside is limited, I believe the demand and supply conditions of potash and phosphate are good and the company should benefit from it in the future resulting in strong price appreciation. Hence, I am bullish on the stock.

Risk

MOS’s recent financial performance had solely been driven by favorable market supply-demand dynamics. The investment thesis revolves around the conditions to remain intact or improve in the future with limited downside risk. However, if the supply-demand dynamics change dramatically against MOS the company could report losses temporarily resulting in a negative change in the book value and the stock can also trade below its book value.

For further details see:

The Mosaic Company: Good Growth Prospects With Limited Downside