MOS - The Mosaic Company's Current Valuation Is Attractive

2023-08-23 01:36:05 ET

Summary

- Increasing industrial demand would reduce phosphate fertilizer supply and support higher phosphate prices.

- Potash price is stabilized.

- Mosaic's valuation is reasonable compared to its historical levels.

Business Overview

The Mosaic Company ( MOS ) is one of the major producers of concentrated phosphate and potash crop nutrients.

MOS is organized into the following business segments:

The Phosphates business segment owns and operates mines and production facilities in Florida, which produce concentrated phosphate crop nutrients and phosphate-based animal feed ingredients, and processing plants in Louisiana, which produce concentrated phosphate crop nutrients for sale domestically and internationally.

The Potash business segment owns and operates potash mines and production facilities in Canada and the U.S. which produce potash-based crop nutrients, animal feed ingredients and industrial products.

The Mosaic Fertilizantes business segment includes five phosphate rock mines, four phosphate chemical plants and a potash mine in Brazil. The segment also includes a distribution business in South America, which consists of sales offices, crop nutrient blending and bagging facilities, port terminals and warehouses in Brazil and Paraguay.

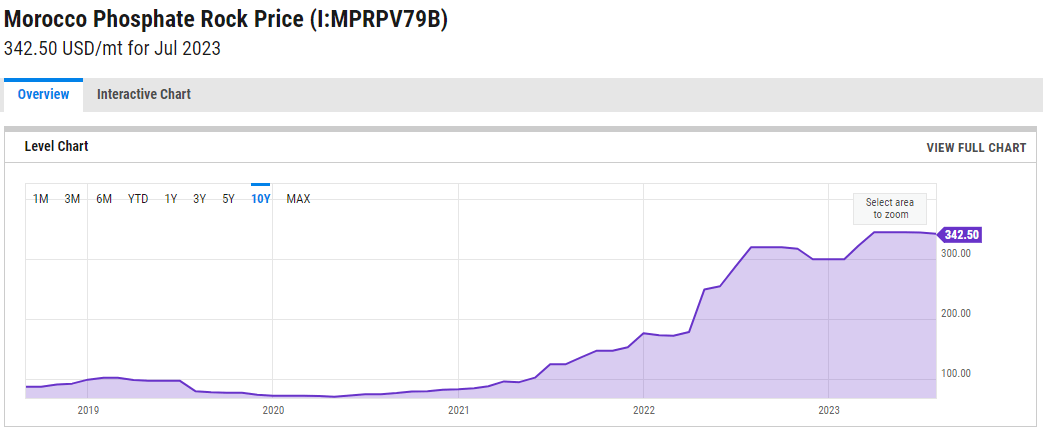

Phosphate Rock Supply is Limited in the Foreseeable Future

Q2 phosphate net sales declined to $1.3B from $1.8B a year earlier, as sales volumes rose to 1.9M metric tons from 1.7M metric tons but the average DAP selling price fell to $585/ton from $920/ton a year earlier.

According to MOS’s earning transcript, “Industrial demand, particularly in China's lithium iron phosphate production, is expected to grow dramatically over the next several years……This new market will continue to take phosphate volumes away from fertilizer production. We expect China's exports to be in the range of 7 million to 8 million tonnes this year or roughly 35% below 2021 export levels.”

Given the recent development (In China, Bidding Wars for Lithium Top Out at 1,300 Times the Starting Price, In China, Bidding Wars for Lithium Top Out at 1,300 Times the Starting Price ), industrial demand for phosphate will continue to rise, and China’s phosphate export will continue to decline in the future. The initial impacts had already affected the phosphate rock prices.

{kind=link}

This trend will be bullish for MOS’s Phosphates business segment and Fertilizantes business segment, boosting MOS’s revenue and profitability in the next few quarters.

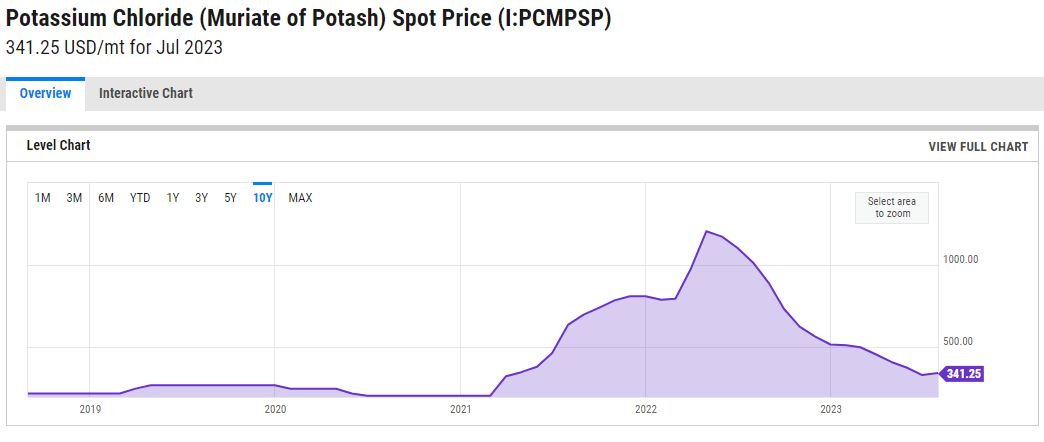

Potash Demand and Supply are Balanced for Now

Q2 potash net sales dropped to $849M from $1.6B in last year's Q2, as sales volume slipped to 2.2M metric tons from 2.3M tons reflecting idled production at the Colonsay mine in Saskatchewan, and the average MOP selling price fell by half to $326/ton from $678/ton.

Due to the Ukraine war, the sanction had reduced Russia’s and Belarus’s export and limited the worldwide supply. On the demand side, farmers are facing the increasing liquidity pressure from the high interest rate. Agricultural credit conditions are tightening in the US ( Tenth District Ag Credit Conditions Moderate ). The lack of liquidity for farmers in Brazil had already caused farmers to defer their purchase of fertilizers ( Brazil's Momentum as a Global Agricultural Supplier Faces Headwinds ) even though the central back in Brazil just lowered their interest rate (still above 13%?).

This somehow balanced picture stabilized the potash prices for now.

{kind=link}

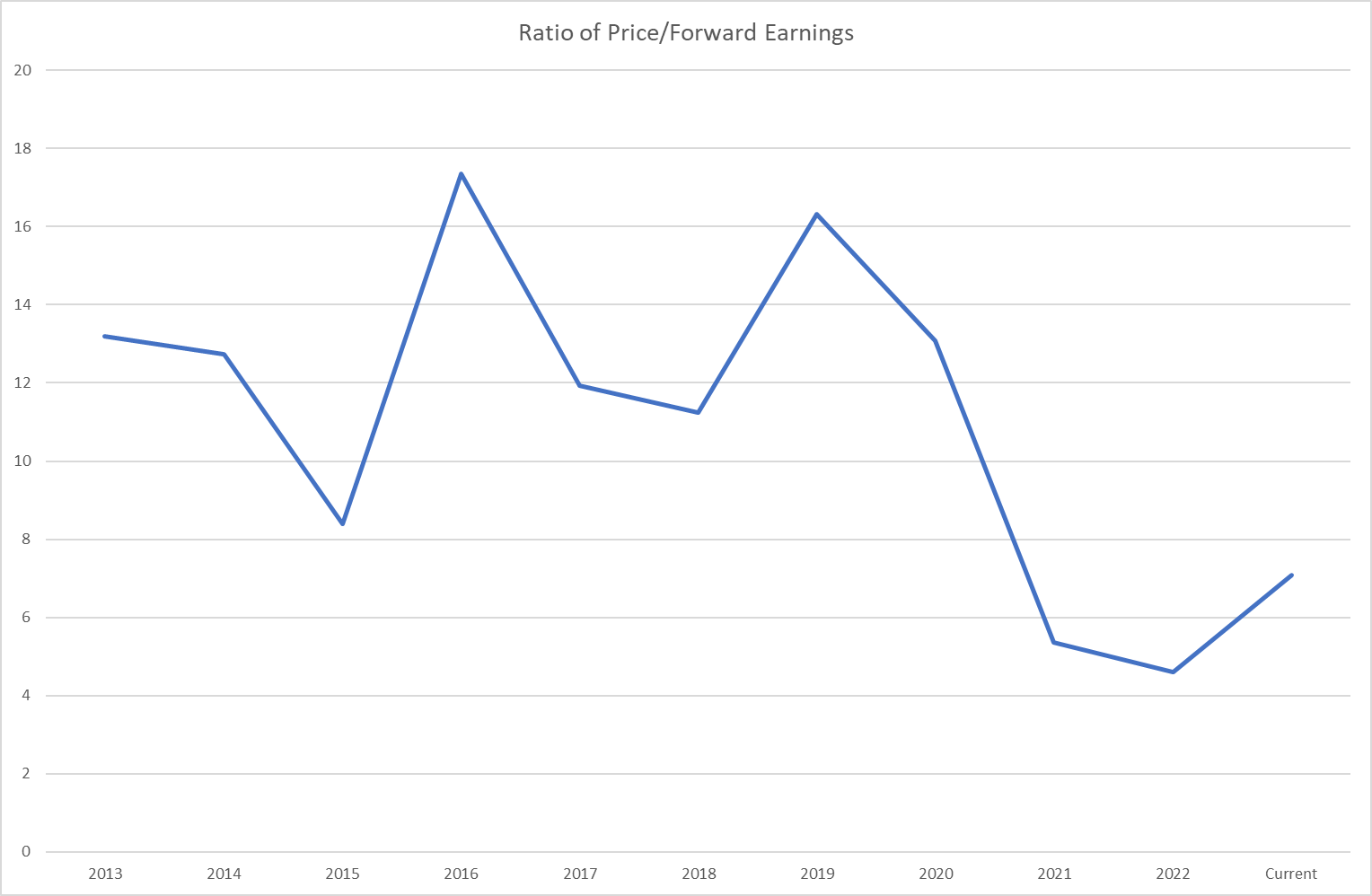

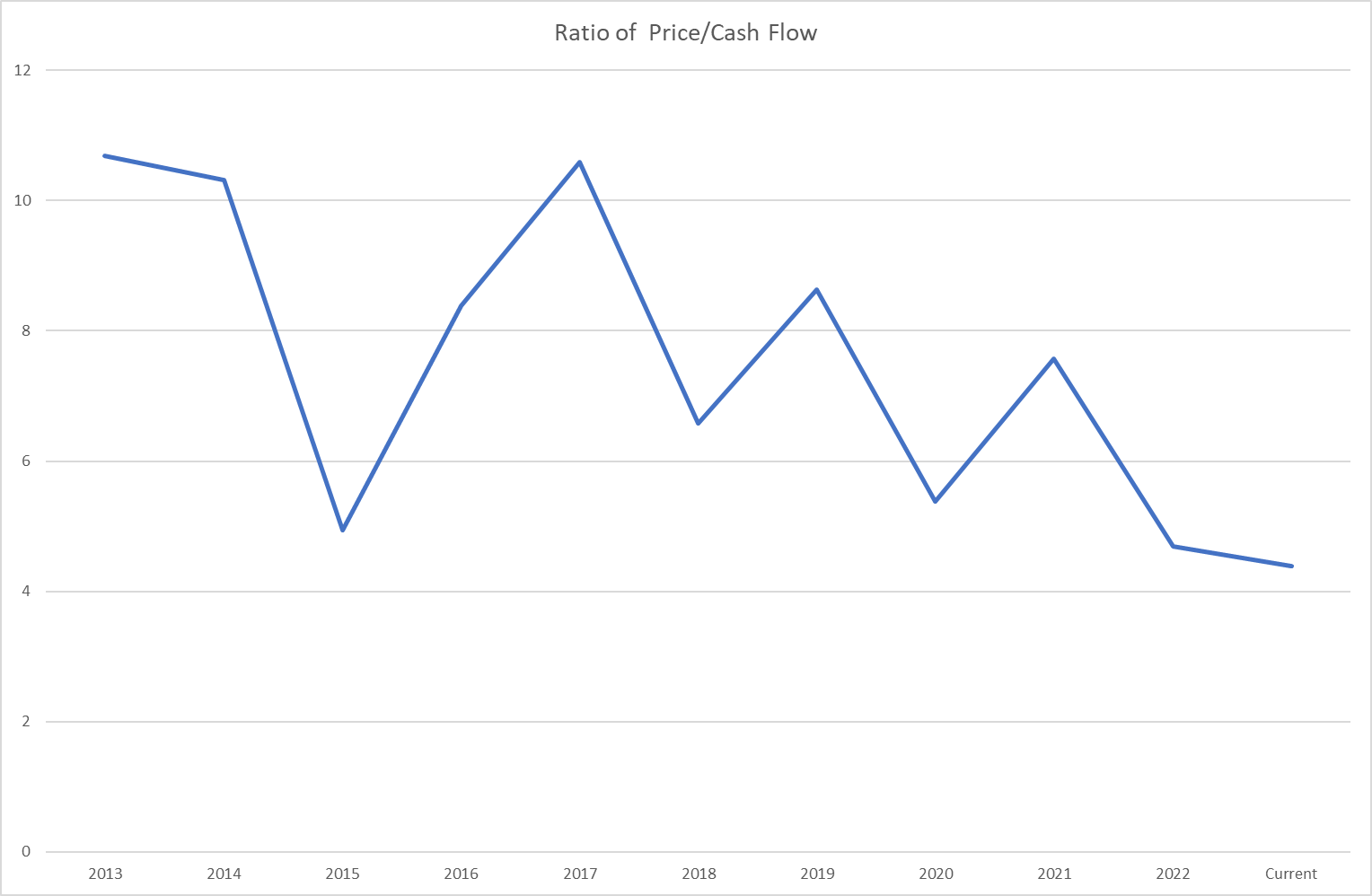

Valuation is Reasonable.

| Unit: |

| FY2020 |

| FY2021 |

| FY2022 |

| FY2022 Q1 |

| FY2022 Q2 |

| FY2023 Q1 |

| FY2023 Q2 |

| Revenue |

| 8,682 |

| 12,357 |

| 19,125 |

| 3,922 |

| 5,373 |

| 3,604 |

| 3,394 |

| Gross Profit |

| 1,065 |

| 3,200 |

| 5,756 |

| 1,439 |

| 1,846 |

| 670 |

| 571 |

| Gross Margin |

| 12.3% |

| 25.9% |

| 30.1% |

| 36.7% |

| 34.4% |

| 18.6% |

| 16.8% |

| Net income (loss) |

| 666 |

| 1,631 |

| 3,583 |

| 1,182 |

| 1,036 |

| 435 |

| 369 |

| Net Income Margin |

| 7.7% |

| 13.2% |

| 18.7% |

| 30.1% |

| 19.3% |

| 12.1% |

| 10.9% |

MOS’s Q2 net income fell to $369M, or $1.11/share, from $1.04B, or $2.85/share, in the year-earlier quarter, adjusted EBITDA dropped to $744M from $2B in the same period last year, and free cash flow plunged to $197M from $794M a year ago. Its gross margin and net income margin are both lower than the peak during the pandemic period.

{kind=link}

{kind=link}

{kind=link}

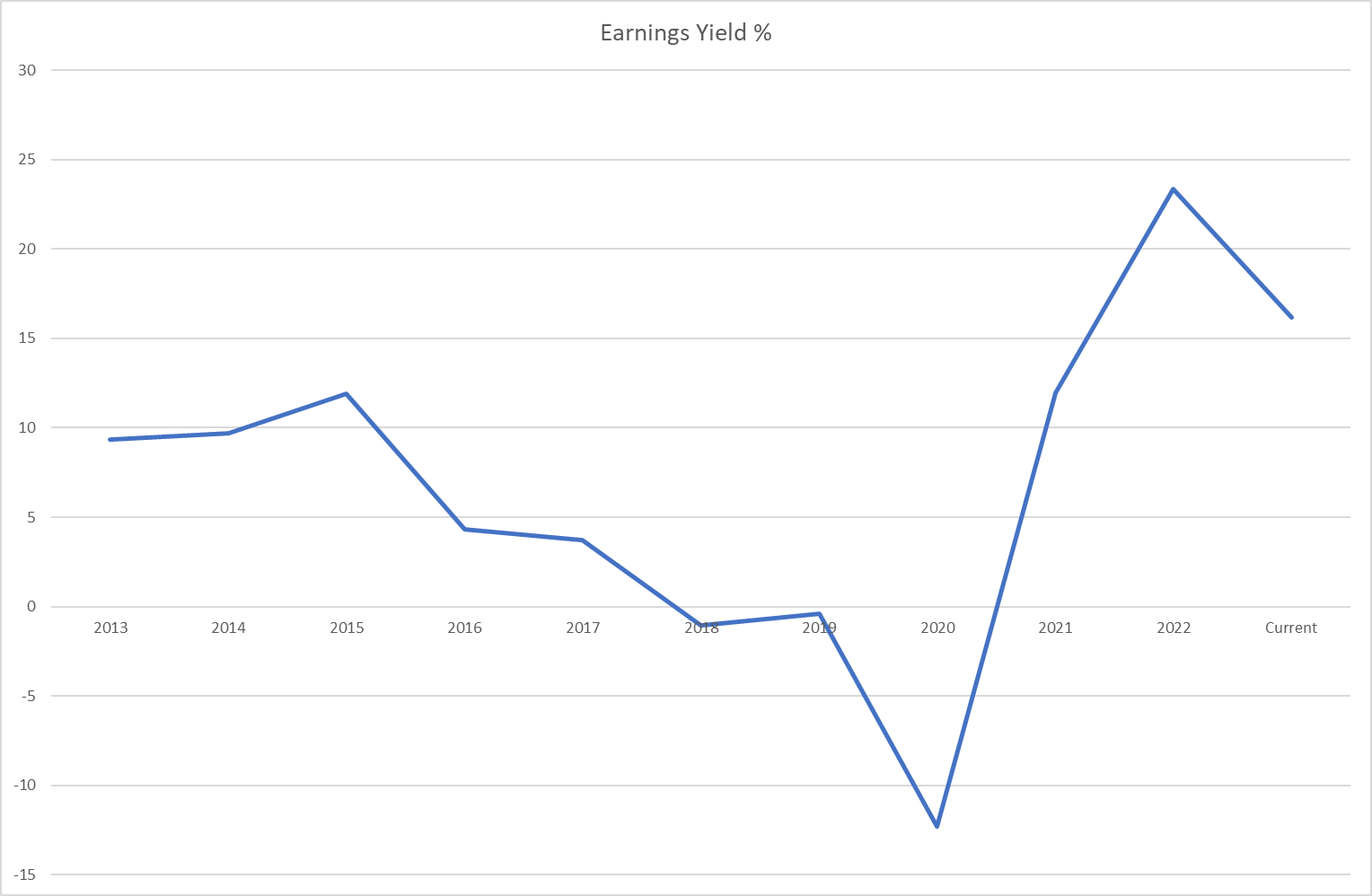

Currently, the price/forward earnings ratio is still closer to the lower end of the historical range. The ratio of price/cash flow is actually at the lowest point after 2013. The current earnings yield is also just below its 2022 level, the second highest level since 2013.

Conclusion

The company had forecasted that Q3 potash sales volumes of 2.1M-2.3M metric tons with MOP prices of $250-$300/ton, phosphate sales volumes of 1.7M-1.9M metric tons with DAP prices of $475-$525/ton. I believe that its forecasts on phosphate price is too conservative in the long run. Given the reasonable valuation and potential supply limitation of phosphate, MOS is attractive at current price level.

For further details see:

The Mosaic Company's Current Valuation Is Attractive