O - The Most Common Misconception About REIT Investing In This Environment

2023-10-06 14:17:16 ET

Summary

- REITs face structural headwinds from higher costs of financing, which is a critical constituency in the process of how REITs create a value.

- If the interest rates remain elevated, many REITs will suffer and most likely continue to register a negative performance.

- Some REIT investors consider favourable supply and demand dynamics, as well as REIT's ability to increase rents via CPI-indexation or embedded escalators, as notable mitigants.

- I elaborate through Realty Income and Global Medical REIT that such an assumption in incorrect.

As many of my readers have probably noticed, lately, I have paid a very close attention to the REIT balance sheets and debt financing structures.

I think that restrictive interest rates for a long period of time is the biggest risk in the equity REIT universe. The so called "higher for longer" scenario and the current uncertainty around how long it will last have put a significant downward pressure on the REIT valuations.

Everyone who has invested a bit of his or her time into exploring how equity REITs work, understands that the chances of finding the next Nvidia or Apple by picking any REIT out there are extremely slim.

Instead, REIT-focused investors can play a more balanced and predictable game, which is underpinned by to a large extent a predictable business model and cash generation profile.

Some basics about how REITs create value

REITs per definition (regulation) have to devise a "buy and hold" strategy, where a notable portion of the collected cash flows (rents or leases) have to be regularly distributed to the shareholders.

The main ways how REITs can increase the cash flows are the following:

- Ask for higher rents / leases via rent escalators or positive spreads at new signings.

- Investing in new development projects that yield more than the cost of capital.

- Venture into M&A world, where the expected yield exceeds the cost of capital.

- Issue new equity to assume incremental leverage, and through a combination of these two sources conduct either investments outlined in point 2 or point 3 above.

- Other activities such as optimizing costs, refinancing debt at cheaper levels etc.

Besides increasing the rents / leases organically or conducting non-core activities such as positive debt refinancing, the key essence of REIT business is to capture a positive spread between asset (or investment) IRR and the cost of capital.

If the spread widens, REITs are deep in the money.

If the spread remains stable, REITs deliver stable and positive results.

If the spread decreases, REITs fall.

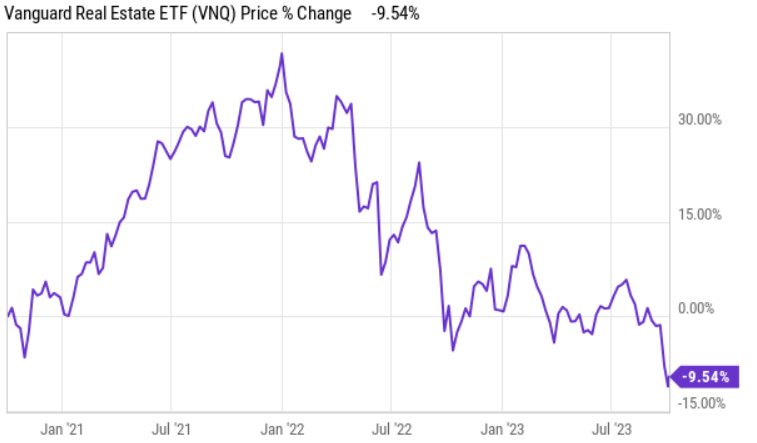

Since the early 2022, the overall cost of financing has gradually increased, sending the broader REIT index in a negative return territory.

{kind=link}

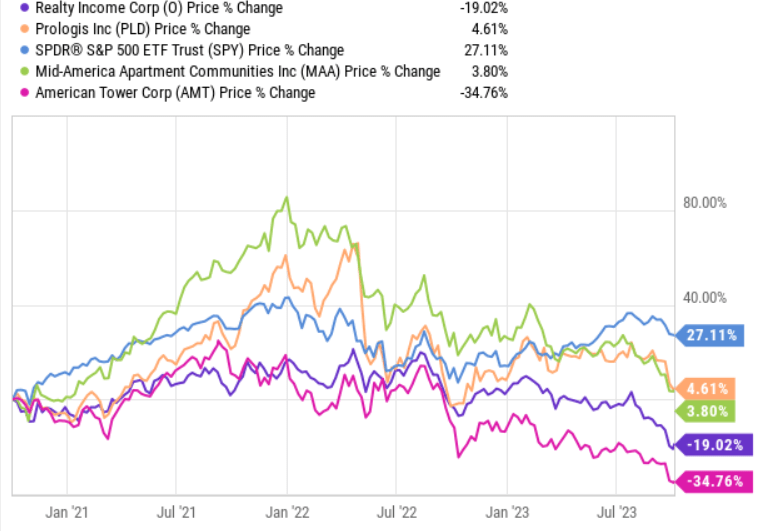

One might argue that this decline is mostly explained by the struggling office sector and if the office segment was excluded, the remaining REIT space would be in a nice position relative to the early 2022.

{kind=link}

Well, not exactly right. In the chart above, we can see some of the most popular REITs operating outside of the realm of office segment, and that have still delivered returns, which are significantly below the S&P 500.

All in all, the key message here is that REITs are extremely sensitive to the changes in the interest rate levels, as any movement in the cost of capital makes a huge impact on the underlying cash generation profile.

Plotting the potential danger of "higher for longer"

In most of my recent articles, I have incorporated a huge skew towards assessing the potential implications of higher cost of capital.

Why? Because I think that the "higher for longer" scenario and higher interest rates in general embody a significant potential to destroy huge chunks of FFO for many REITs out there.

The following are the main avenues through which this risk is most likely set to render a painful impact:

- When refinancing maturing portions of debt, which have previously been assumed at very favourable rates before early 2022.

- When existing interest rate hedges expire on the floating rate debt instruments (e.g., revolver facilities).

- When assuming incremental debt financing to finish the initiated projects or pre-stipulated activities via JV agreements.

Otherwise, at this stage, REITs are protected from additional headwinds that are associated with higher cost of capital as the effects from unhedged floating debt instruments have already been reflected in the latest financials.

In my view, refinancings at higher interest rates is the most critical issue.

Let me depict the embedded severity of this issue via one very common REIT: Realty Income Corporation ( O ).

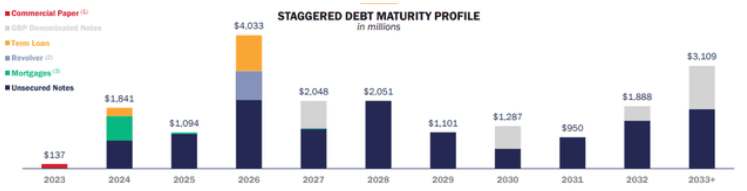

Currently, O has around $6.5 billion of debt (excluding the floating portion and the assumption of organic dept repayment) that has to be refinanced by 2026.

{kind=link}

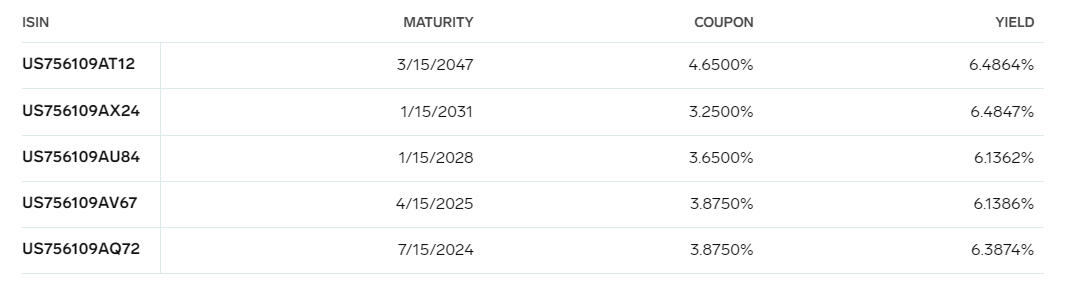

As of Q2, 2023, O had a weighted average cost of financing at 3.7%, which is considerably below the market level financing cost.

{kind=link}

Looking at the prevailing YTM of some of the O's outstanding bonds, we get an average cost of financing around 6.4% (~72% of an increase).

If we assign the prevailing cost of financing level to the maturing debt proceeds until 2026 (i.e., reprice according to the market level), O's FFO would decrease by ~ $175 million or by 6% taking TTM FFO as a basis. This, in turn, would send the FFO payout ratio higher to 80% level.

If we take a more extreme scenario and reprice all of the remaining $12 billion to the 6.4% interest rate level, the effects would be very severe, impairing O's long-term growth prospects. In other words, completely justifying the recent price decline.

Remember that via this example we see the potential consequences for a REIT, which has an upper investment grade credit rating, relatively well-laddered debt maturity profile, and a significant scale, which introduces flexibility in the financing processes. For many REITs the debt situation looks much worse.

The ultimate misconception - not understanding the rate of change effects

Finally, we come to the point, where I want to emphasize a very popular misconception in the context of REITs and the potential consequences of higher interest rates.

The challenge stems from the misunderstanding of the rate of change effects. More specifically, many REIT investors carry a concept that REITs are a natural hedge of the inflation due to the rents / leases that adjust to the inflation levels accordingly.

This coupled with the generally correct fact that many REITs exhibit favourable supply and demand dynamics - especially now when building new supply has become very expensive - leads to an opinion that the growing interest costs will be easily offset by a synchronized movement in the top line.

As a result, many REIT investors have become overly complacent and do not fully appreciate the potential consequences.

Now, my argument is that while all this is correct, it does not really move the needle in the context of surging interest expenses.

{kind=link}

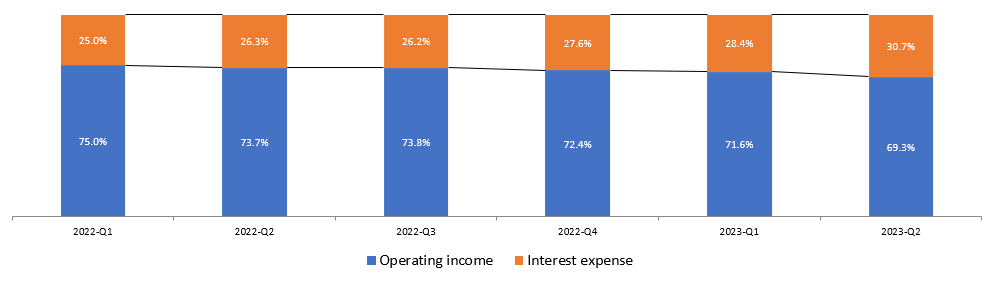

Since the early 2022, O has managed to deliver a superb growth in its top-line, registering a couple of very strong quarterly results. In total, from Q1, 2022 to Q2, 2023, O's operating income grew by ~34%. And for all of the reasons many REIT investors mention - e.g., embedded rent escalators, which kick in nicely during inflationary period and favourable supply and demand dynamics.

However, despite the solid growth numbers, the share of the interest expense component relative to the operating income has become larger. And now let me remind you that the current cost of debt sitting in O's books is still nowhere near the market level and that during most of these quarters the interest rates were actually much lower than we currently have given that the Fed was still in the aggressive hiking process.

{kind=link}

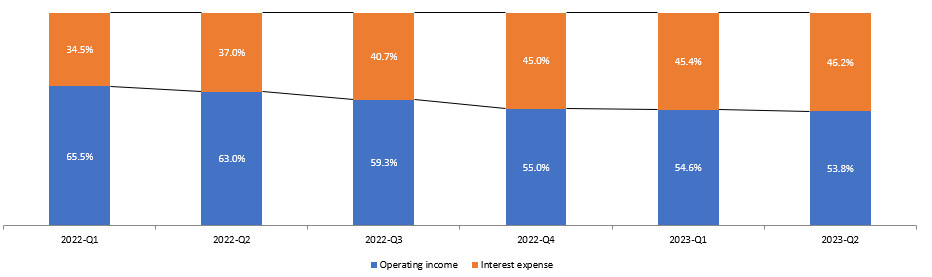

To contrast O, which is an A-rated REIT with a smaller REIT, which has not an IG balance sheet, I have taken the Global Medical REIT ( GMRE ) as an example.

As we can see, the higher interest costs have consumed a significant portion of GMRE's operating income, despite the fact that the Company has embedded rent escalators for almost all of its contracts. Moreover, GMRE operates on a net lease basis just as O, which protects the earnings from other inflationary costs.

Both in O and GMRE's case, the occupancy levels have remained robust (at their peaks) and there have been successful increases in the top-line. Yet, both companies have still significantly lower cost of financing recorded at their books currently, and first notable maturities are slowly but surely approach their deadlines.

Final words

I recommend REIT investors to revisit the theoretically correct yet practically insignificant thesis that rent / lease indexation to inflation or rent increases in general serve as meaningful mitigates to the "higher for longer" scenario for REITs. Mathematically and based on the actual results, organic growth in rents or leases is not sufficient to protect many REITs from a gradual convergence to higher cost of capital and the resulting consequences.

For further details see:

The Most Common Misconception About REIT Investing In This Environment