AYX - The Name Of This Game Is Rotation (Back To Growth)

Summary

- The impact of interest rates on growth stocks.

- Earnings season and the market's early reaction to growth stock results.

- Conclusions.

Brian Dress, CFA - Director of Research, Investment Advisor

In this year's first newsletter, we asked "New Year, New Market?" In the first 6 weeks of 2023, it certainly does appear to be that way.

We noted throughout 2022 that the value-oriented sectors, especially energy but also healthcare, consumer staples, and some insurance companies, were the standout performers in a difficult market environment. Anyone giving even a cursory glance at markets last year will know that growth stocks faced a challenging environment, to say the least. We saw losses of 25% or more in the following sectors: real estate, information technology, consumer discretionary (retail), and communications services.

At Left Brain, we give a lot of credence to what we call the "January effect": that stocks which outperform well in the first month of the year tend to keep momentum throughout the year. We have been unable to build an ironclad case that this is true from the data as yet, but the experience certainly tells us that this phenomenon is a real one.

We posit that this January effect is even more pronounced in years following down markets, the likes of which we saw in 2022. Many of the best-performing stocks of the past 5-10 years reached a crescendo in selling in December of last year, as investors who bought these stocks at higher prices locked in their losses presumably as part of a tax loss harvesting strategy. The most obvious example of this pattern over the last few months was Tesla ( TSLA ) , whose stock lost nearly 37% in value just in December 2022. We have seen that stock come roaring back in the early weeks of 2023. We note also that the pattern appears in other high-profile large-cap tech stocks like Apple ( AAPL ), Salesforce.com ( CRM ), and Nvidia ( NVDA ). While we know there are still many aspects of the current economic environment that give investors pause, history tells us that stocks like this that outperform in the first month of the year tend to extend their gains in the subsequent 11 months. Time will tell.

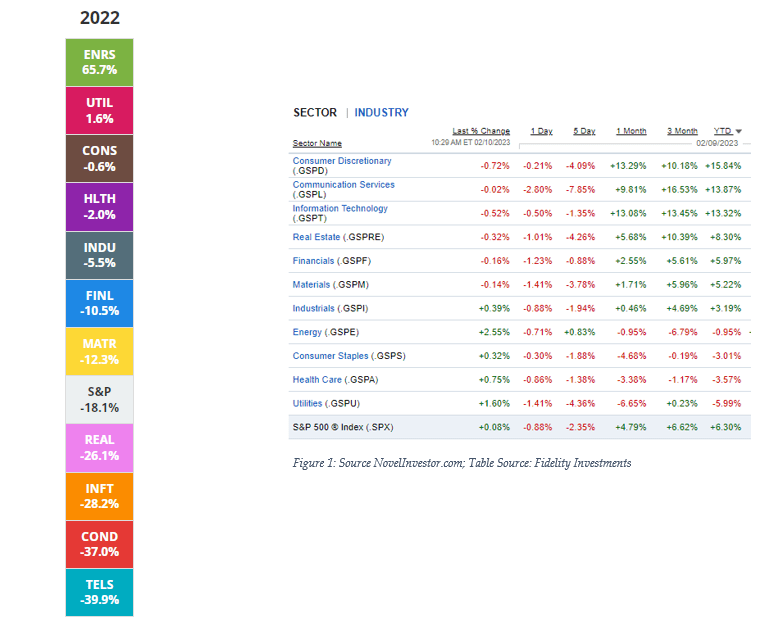

The reverse is also true, which is why we entitled this month's newsletter "Rotation is the Name of the Game". As we compare the sector return quilt from 2022 to that which we see in 2023 (so far), we also see that last year's winners are struggling to maintain their positions in 2023:

{kind=link}

As we interpret the two charts above, we see a clear pattern emerging. Those four beleaguered sectors we identified from 2022 are the four strongest performers here so far in 2023, while those stalwart sectors of health care, energy, and consumer staples, are having relative underperformance since the calendar turned. Of course, we will give you the caveat that this is just a few weeks of trading, but we do think our observation suggests to us that market participants are looking at things with fresh eyes in 2023. What are some of the reasons for this changing landscape? This is what we want to address for you in today's write-up.

With that all being said, let's get into it! We are excited to offer you our thoughts of the new dynamics for the market here in 2023.

Interest Rates and the Federal Reserve

If you follow us on other channels, you will know that last week we declared the end to our reading of the Fed tea leaves, as Federal Reserve Chairman Jerome Powell is starting to set a more optimistic tone. After last week's 0.25% rate hike and relatively dovish comments that came in his press conference, Powell said this week that the process of disinflation has begun in earnest. Investors are well aware that the Fed is willing to continue raising rates should inflation continue to be a problem, but they are looking at things with a much more positive point of view, as evidenced by the overall shift in markets.

Ok, that's enough Fed talk for one day.

What we are really speaking about here are interest rates. Rising interest rates are absolute kryptonite to growth stocks as we saw clearly in 2022:

TradingView

On the chart above, we plot the NASDAQ Composite Index (blue line) as a proxy for growth stocks writ large, against the movements of the 10-year US Treasury rate (orange line). As we read the chart from the left at the beginning of 2022 to now, we can see clearly that growth stocks fell precipitously last year, as treasury rates climbed steadily.

Let's take a look at this chart over the last 3 months (again NASDAQ is blue and 10-year treasury is orange):

TradingView

Here we can see in closer relief the inverse relationship between interest rates and growth stocks and the tide certainly appears to be turning, both in interest rates and in growth stocks.

Nothing ever happens in a straight line: we are likely to see fluctuations in rates throughout the year, as investors determine whether inflation really is on the wane. Growth stocks may be volatile, but we think the trend of rates is down after they peaked in late 2022 and we expect the arrow to be pointing up on growth shares as an asset class for the reasons we discuss in today's letter.

There is another important implication of the peak in interest rates and that is in the fixed income space. For the last 6 months, we have been harping on the opportunities we are seeing in fixed income. For years we were unable to purchase bonds and generate any sort of significant income. This was a huge challenge for investors in or near retirement, who needed to find a way for their portfolio to kick off ongoing income to cover living expenses from month to month and year to year.

Things changed dramatically last year and we have been encouraging investors to take advantage to lock in very attractive rates of return in fixed rate securities. The reason we have been adamant about locking in rates is that we don't expect opportunities to lock in 6-8% in quality corporate bonds to last very long. If you are in or near retirement, we think time is of the essence for you to get these securities into your portfolio and lock in passive streams of income for the next 5-15 years before rates fall and opportunities disappear.

Earnings and the Market's Reaction

As we resolve to move on from Federal Reserve tea-leaf-reading, we are moving back to our roots, which is bottom-up investing. At Left Brain, we love turning our gaze away from all the macroeconomic gyrations and getting back to what really matters, which are the fundamentals of individual businesses. Ultimately, the way we learn about the fundamentals of these businesses comes through the earnings reports and the conference calls where management gives us their thoughts on their companies' trajectories.

Let's again look back to 2022. In 2022, we were in a clear bear market, which meant in practice that both positive earnings reports and negative earnings reports were met with fierce selling (in general, of course, there are always exceptions).

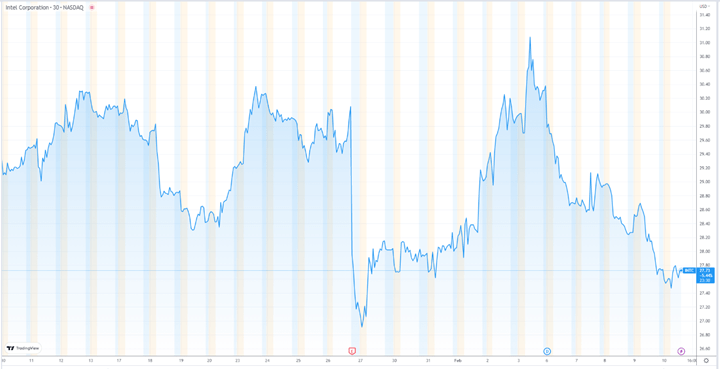

As we moved into the earnings season we are currently observing, our main aim has been to ascertain investors' reactions, both to good news and to bad news coming out of earnings reports. One of the first earnings reports this season came from Intel Corporation ( INTC ) , once a giant in the semiconductor industry, but a business that has been through hard times for the last decade. We read the press release from Intel and like many other investors, we thought it was yet another bomb of a quarter from the company. Revenues were down some 32% Year-over-Year, and the company missed estimates both for revenue and earnings by a significant amount. Believe it or not, however, as you can see from the 1-month chart of the stock below, the stock actually rallied after this dismal earnings report, denoted by the red letter 'E' on the bottom of the chart:

{kind=link}

This was our first data point that suggested to us that something might be changing in the markets, particularly as investors respond to earnings results out of the tech space. Our view is that expectations have fallen significantly, making it difficult for sellers to come in and punish these stocks too much beyond where they already sit. After years of stretched valuations, many tech stocks are trading now at more reasonable multiples, meaning they are no longer "priced for perfection". This should be in the favor of growth stocks in the coming years.

Beyond just the stock price reactions from earnings, we are beginning to learn a lot about what is happening in the business models of many of the former "highflyers" in tech. One of the major stories we have been following out of Silicon Valley in the past couple of months has been the significant layoffs of employees at many of the largest operators in tech. These include Alphabet ( GOOG ) ( GOOGL ), Salesforce.com, Amazon.com ( AMZN ), among many others. Prior to 2022, the focus of most growth tech businesses was to grow top-line revenue at almost any cost, and the conception of margins, profits, etc. very much took a back seat. This led to bloated headcounts and excessive spending at many of the giants in tech. After investors signaled in 2022 that profits now were the most important data point in their processes, as evidenced by the dramatic rotation out of pre-profit growth stocks into value stocks with predictable cash flows, it seems to us that tech CEOs have gotten religion on margins.

None has demonstrated this more than Meta Platforms ( META ) , formerly known as Facebook. We saw META shares fall nearly 80% from the peak in September 2021 to the trough in October of last year. The company had become bloated from a cost perspective, with the company spending huge amounts of money on Research & Development, particularly with respect to its Metaverse presence, a moonshot bet that does not yet produce significant revenue. Investors had been clamoring for years to see rationalized spending out of the social media giant, which runs popular platforms including Facebook, Instagram, and WhatsApp, all of which are hugely generative from the free cash flow perspective.

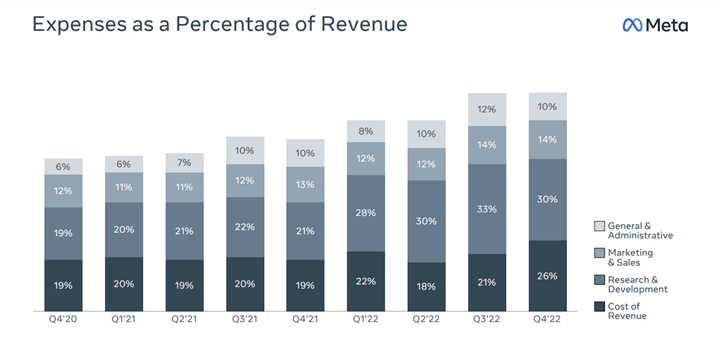

Finally, in Q4, we saw lower spending on R&D. As you can see from the slide in the META investor presentation below, Q4 was the first quarter in recent memory where R&D as a percentage of revenue actually declined, signaling that CEO Mark Zuckerberg is listening to investor concerns on profitability.

{kind=link}

We have avoided META as an investment for some time now, mainly due to awful stock price performance, which was driven by the bloat in expenses. From the earnings call transcript , Zuckerberg said the following sentences that were music to our ears:

"As part of this, we are going to be more proactive about cutting projects that aren't performing or may no longer be as crucial. But my main focus is on increasing the efficiency of how we execute our top priorities. So I think that there is going to be some more that we can do to improve our productivity, speed, and cost structure. And by working on this over a sustained period, I think we will both build a stronger technology company and become more profitable."

META was not the only business thus far that has impressed in terms of cost containment. We heard from telehealth leader Teladoc ( TDOC ), who reported a significant improvement in operating margins. Tesla has been showing signs that profitability is more on management's mind. Other tech companies striking a similar tone in their earnings calls include Gartner ( IT ), Enphase Energy ( ENPH ), Fortinet ( FTNT ), Alteryx ( AYX ), and ServiceNow ( NOW ). Most of these companies reported some improvement in profitability, whether it be in bottom line profit, operating margins, free cash flow, or other metrics of profitability.

Investors have been through it in the last year and they are looking for some indication that company management teams take their desire for profits and cash flow more seriously. The significant layoffs in Silicon Valley, along with what we have learned so far in the Q4 earnings season, have been a strong indicator that this shift in focus from revenue growth to profit growth is taking place in the tech and growth spaces. This is making us more bullish on growth in general and in particular, old growth stalwarts like META and Netflix ( NFLX ).

Takeaways

We came into this year still skeptical about growth investing, though that has historically been a major part of our investment philosophy. As we have moved into 2023, a number of factors have changed, which have made us much more enthusiastic about growth shares, many of which are trading at reduced valuations from where they were in the go-go days of 2021.

We believe we have seen a peak in interest rates, at least for the current cycle, as we have observed treasury and mortgage rates backing down over the last three months. Despite the fact that the Federal Reserve is still hiking rates (albeit more slowly) and that the perception throughout the country is that interest rates are on the rise, this is not borne out in the movement of market-driven interest rates like treasuries. Combining the fact that interest rates are in retreat with positive fundamental business developments, we think the major market story of 2023 (so far) is the re-emergence of growth and tech as investible themes.

Let's not forget the attractive opportunities that remain in fixed income securities as interest rates still hold at elevated levels relative to the last decade. As interest rates retreat, we think investors should move with a sense of urgency to lock in passive streams of income in the 6-8% range for the next 5-15 years. If rates continue to come down, the opportunities will not last much longer!

And I almost forgot in anticipation of this weekend's Super Bowl:

GO CHIEFS!!!

For further details see:

The Name Of This Game Is Rotation (Back To Growth)