LQD - The Overton Window

2023-07-13 17:34:12 ET

Summary

- The "Overton window" concept, which frames the range of policies a politician can recommend without appearing too extreme, is being used by politicians and central bankers to shift public opinion on policies.

- The US and European markets are seeing rising bankruptcies and credit spreads, indicating potential economic strains.

- The UK is facing economic difficulties, with rising inflation, mortgage defaults, and government debt, leading to comparisons with emerging market economies.

"We decide on something, leave it lying around, and wait and see what happens. If no one kicks up a fuss, because most people don't understand what has been decided, we continue step by step until there is no turning back." - Jean-Claude Juncker.

Watching with interest the ongoing "escalation" in the military equipment provided so far to Ukraine in the military conflict opposing Russia to Ukraine, also, while monitoring as well how central banking "financing" rules have been "bent" to accommodate government "financing needs" in recent years such as "Quantitative Easing", we found that it would be appropriate for us to use as a title analogy the "Overton window" also known as the window of discourse. The term is named after American policy analyst Joseph Overton, who stated that an idea's political viability depends mainly on whether it falls within this range, rather than on politicians' individual preferences. According to Overton, the window frames the range of policies that a politician can recommend without appearing too extreme to gain or keep public office given the climate of public opinion at that time. The "Overton Window" is an approach to identifying the ideas that define the spectrum of acceptability of governmental policies. It says politicians can act only within the acceptable range. Shifting the Overton window involves proponents of policies outside the window persuading the public to expand the window (this is where propaganda and mass media steps in). Politicians and central bankers are actually experts in the business of detecting where the window is, and then moving to be in accordance with it.

Political commentator Joshua Treviño has postulated that the six degrees of acceptance of public ideas are roughly:

- Unthinkable.

- Radical.

- Acceptable.

- Sensible.

- Popular.

- Public Policy.

In March 2022, President Biden defended his decision to veto the US-facilitated transfer of fighter jets to Ukraine to repel Russia's invasion, saying, "that's called World War III." In similar fashion, in 2011, Germany's head of state Christian Wulff criticized the ECB for its action of buying up the bonds of countries worst hit by the European debt crisis. He highlighted at the time that the European Union treaties forbid the ECB from buying debt directly from governments. "The Overton Window" is all about convincing the public that policies outside the window should be in, such that, an idea derided as "unthinkable" can become "inevitable". One could opine that both politicians and central bankers apply the "boiling frog" approach when it comes to shift the "Overton Window" but we ramble again.

In this conversation, we would like to look at the current market set-up which has seen rising real yields on the back of "strong" US data as well as the outperformance of "growth" (the magnificent seven in the S&P500) over "value" (the lag in Emerging Markets in general and the Energy sector in particular). We would like to reflect on what the second part of the year will entails from a "risk-reward" perspective and also look at worrying signs from the United Kingdom

Disturbance in the "Force"

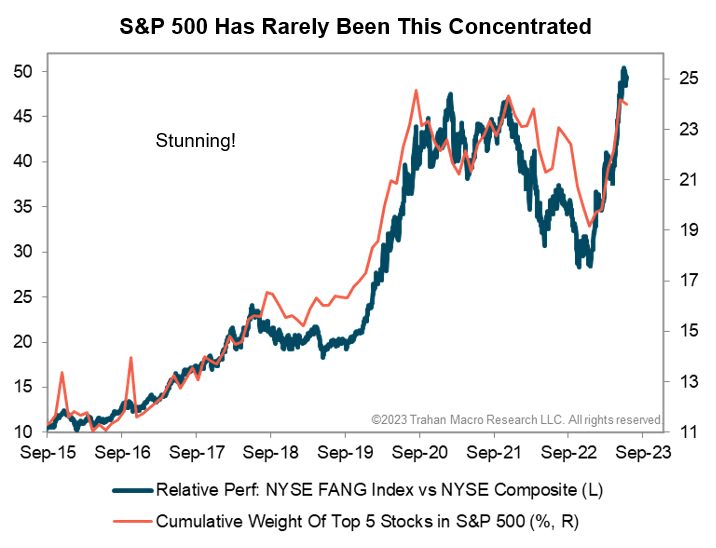

In our previous conversation we mentioned the significant weight of the largest five stocks as a percentage of Total S&P500 Market Cap. As well, we pointed out that in 2023 10 stocks made up 90% of the gain in the index based not on earnings but, on "multiple expansion".

As pointed out by François Trahan in our LinkedIn feed, the S&P500 has rarely been this concentrated:

S&P500 concentration (François Trahan Macro Research - LinkedIn)

{kind=link}

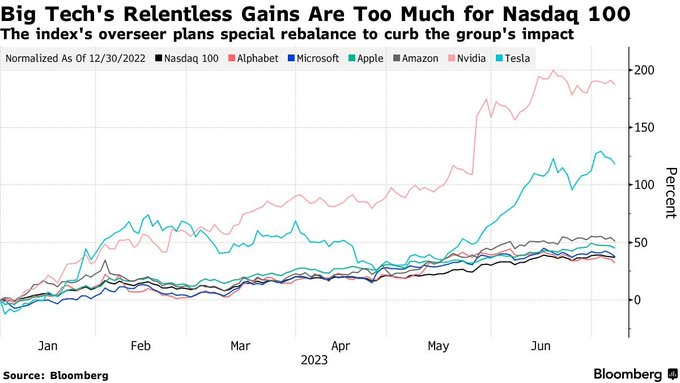

Given the above and recent points made in our musing, we are not surprised to learn that the Nasdaq has announced a "special rebalance" for the Nasdaq 100 to address the overconcentration and weight that the biggest tech companies have on the index. This is the first-ever "special rebalance" carried out by the overseer of the index:

{kind=link}

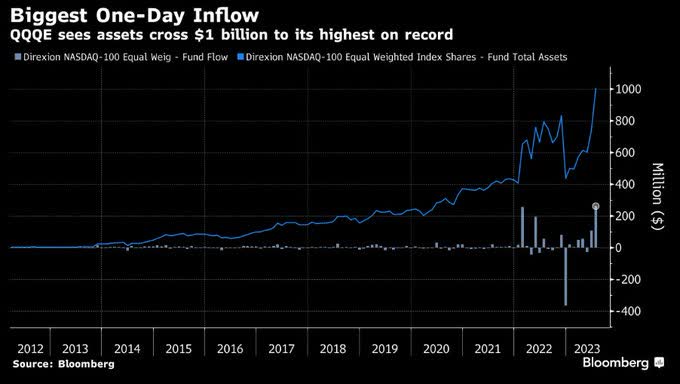

We could as well mention the "hype" in AI which has enabled the TECH sector to reach new dizzying levels. No wonder therefore that the upcoming "rebalancing" of the index has led to record inflows into ETF QQQE:

{kind=link}

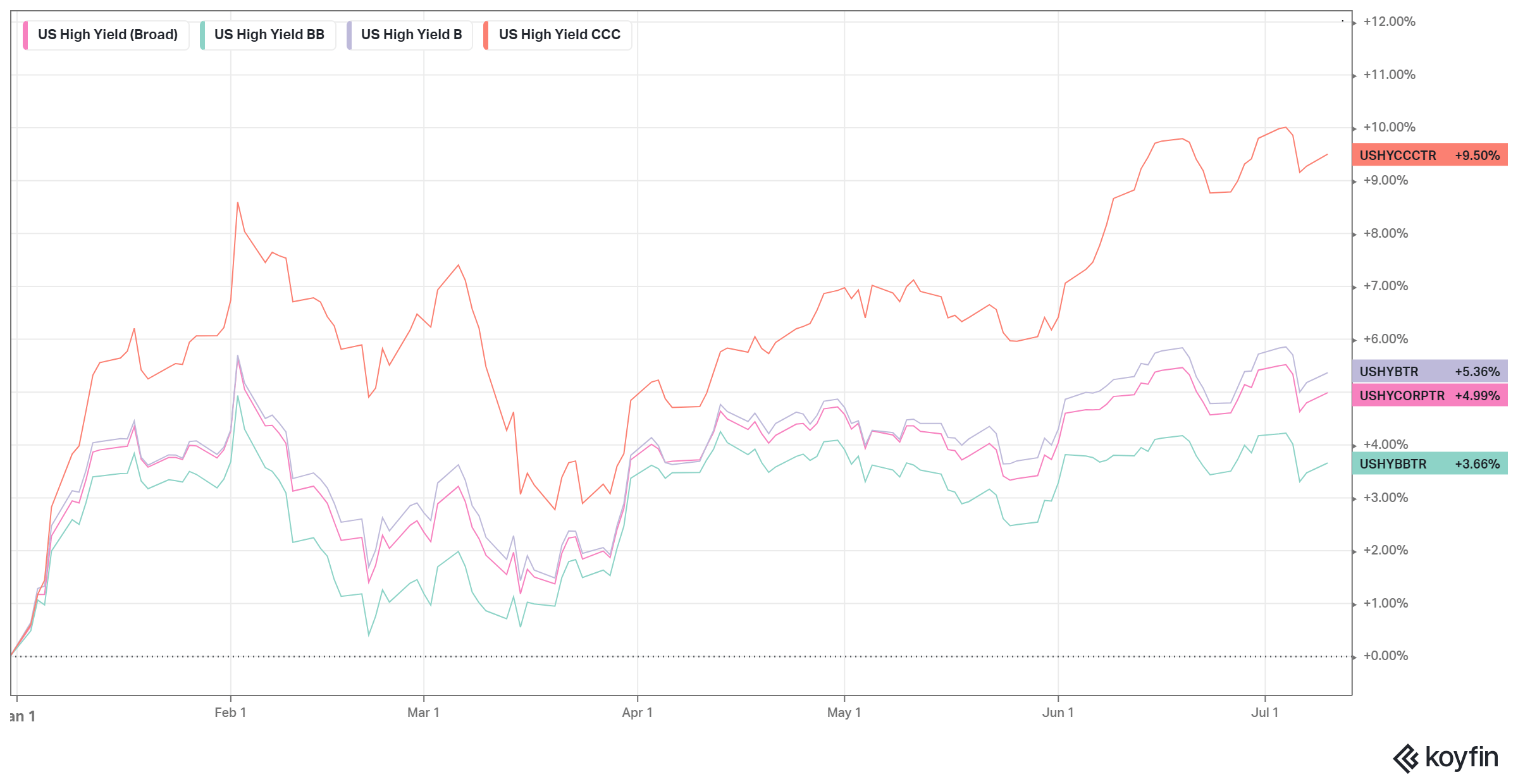

Whereas the ongoing trajectory of credit markets as per the below performance YTD from US High Yield in general and the CCCs bucket in particular has been pretty stellar so far, it seems to us that there are some changes taking places, with some small weakening as of late of the performance of the "Credit Canary" aka the CCC ratings bucket:

{kind=link}

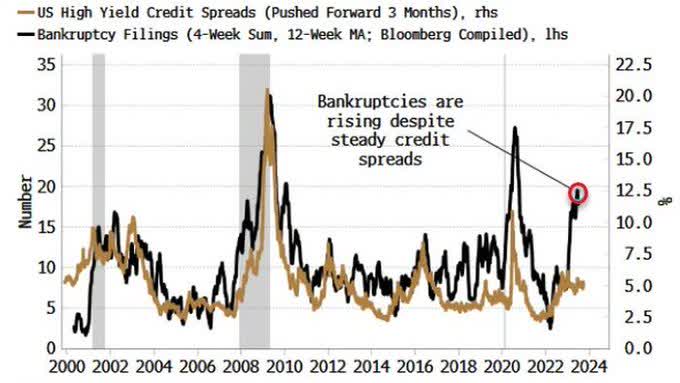

This we think warrants close monitoring in the second half of the year particularly in light of credit spreads not reflecting the real economy and rising bankruptcies as per the below chart:

{kind=link}

As pointed out recently by Bloomberg, rising bankruptcies points towards widening credit spreads at some point. We have discussed in previous conversations the deterioration coming from the Fed's most recent quarterly Senior Loan Officer Opinion Survey (SLOOs).

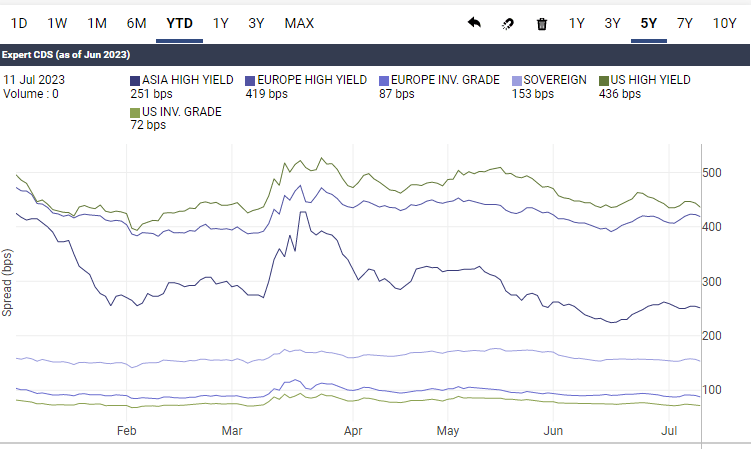

Sure, from a CDS credit spreads perspective, so far the market has been fairly muted as per Datagrapple.com YTD below chart:

Global CDS spreads level YTD (Macronomics - Datagrapple.com)

{kind=link}

Credit continues to behave in an orderly fashion but clearly it seems to us there is a growing disconnect between rising bankruptcies in conjunction of rising "real yield" and the current benign environment which portends to us for rising volatility towards the end of the second half most likely in conjunction with widening credit spreads:

{kind=link}

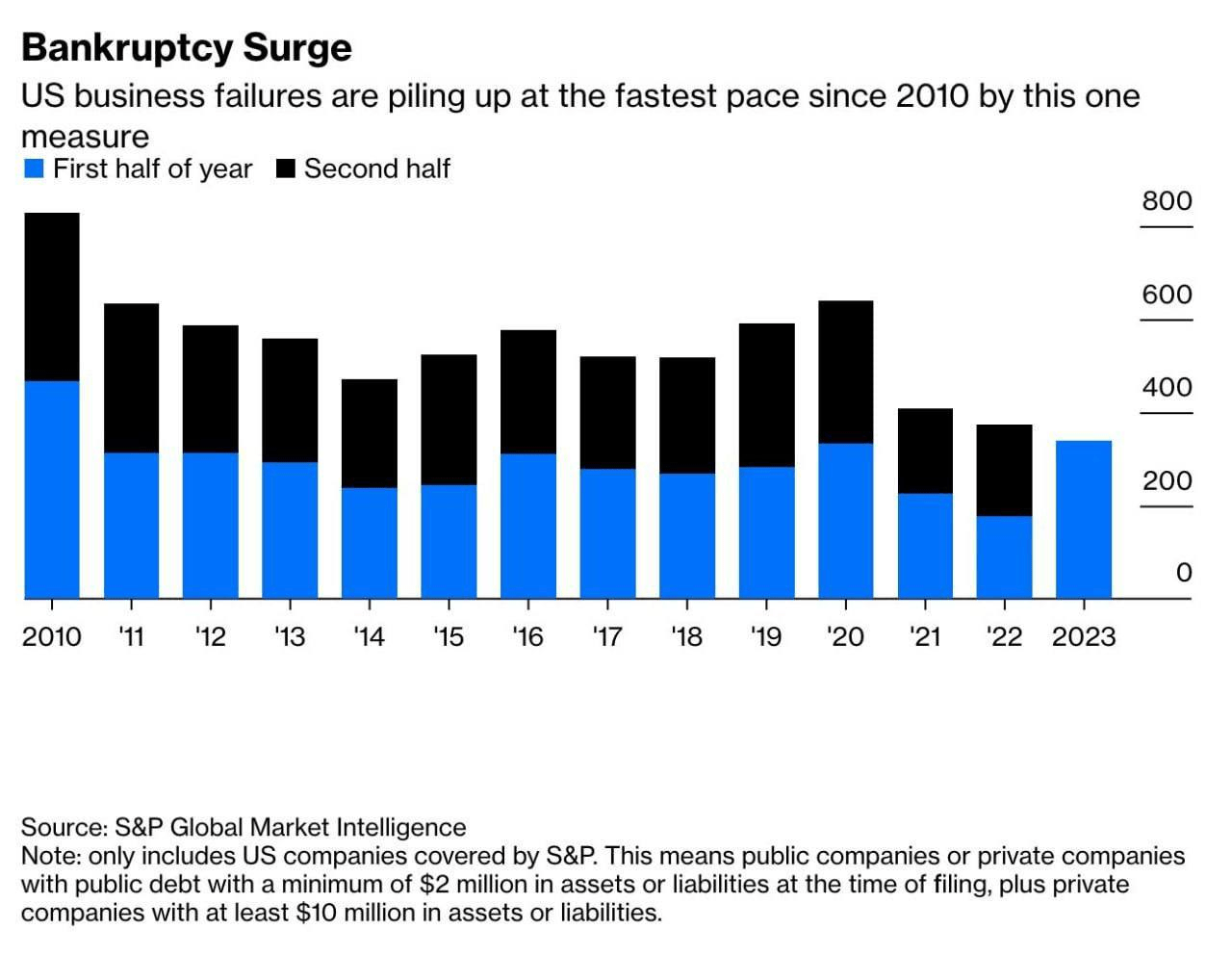

US bankruptcies in the first six months of 2023 were the highest since 2010. But rising bankruptcies are also happening in Europe, in the United Kingdom where corporate insolvencies are near a 14 year high and in Germany where they jumped almost 50% year on year in June to the highest level since 2016.

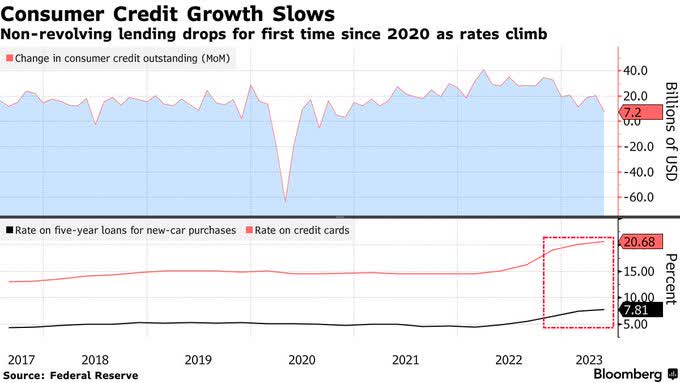

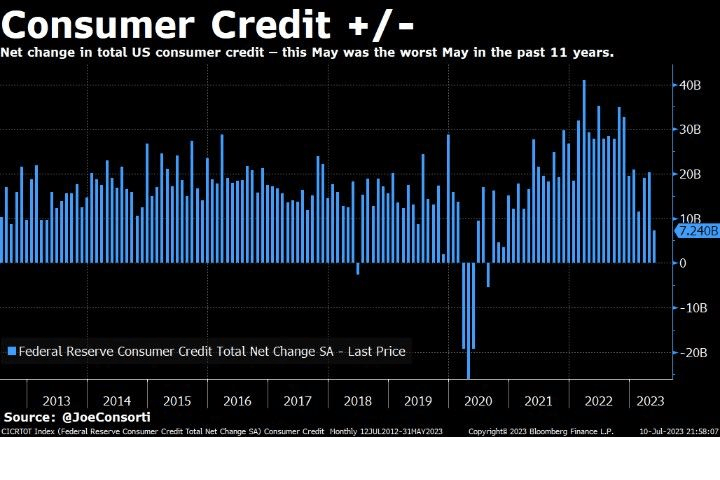

We are starting to see strains in the US economy particularly on the consumer front where consumer credit growth is already slowing:

{kind=link}

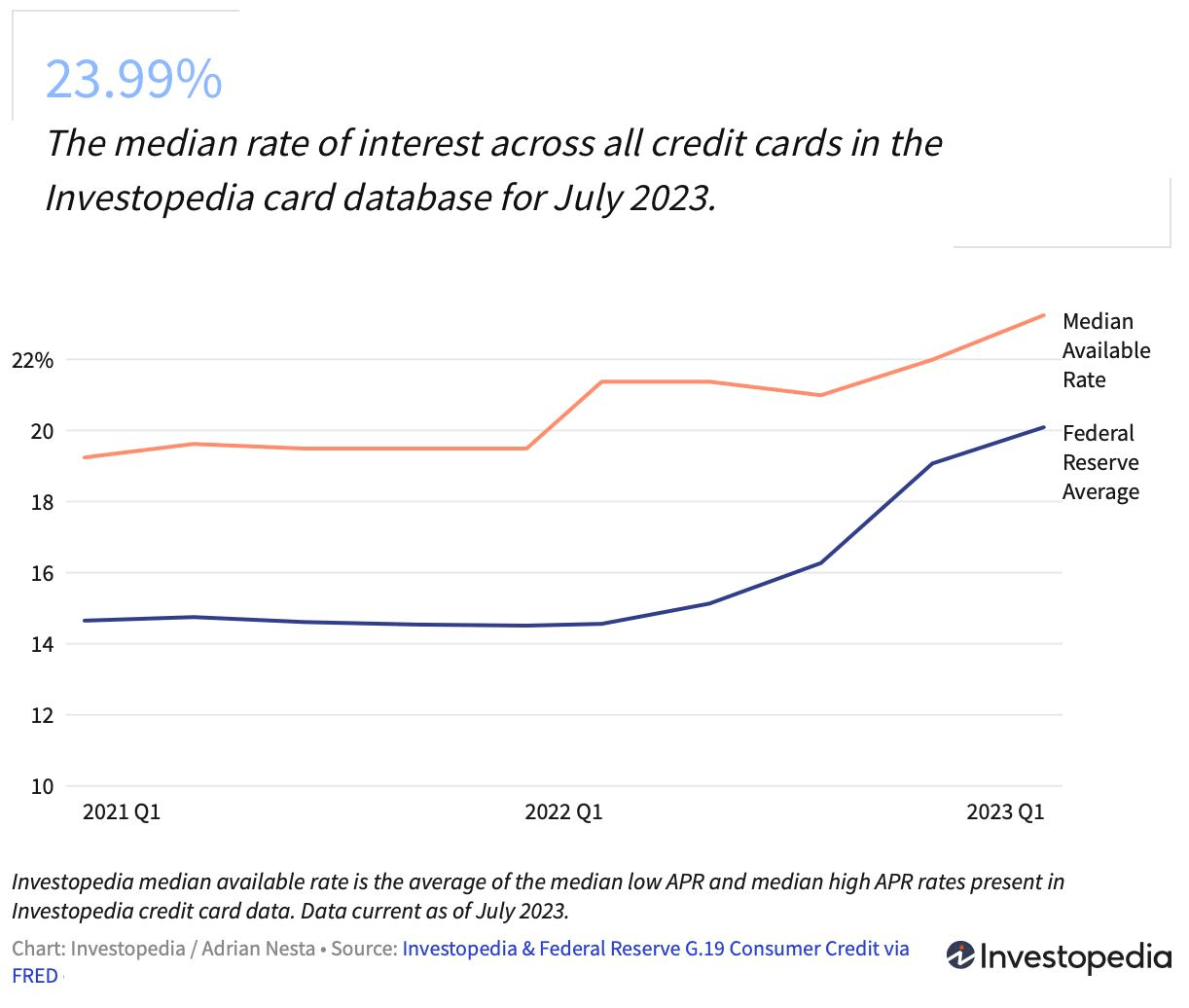

Credit card interest rates in the US have climbed to a record high of 23.99% in July, according to Investopedia:

{kind=link}

Given Federal student loan payments are set to restart in October, credit card balances pose a particularly big risk for some individuals and households. The average credit card debt is $5,733 per person, according to TransUnion. Notably, Americans have set a record for total credit card debt with $986 billion in Q42022 - which held constant in Q12023, speaking to the challenges of high inflation and surging interest rates. The US consumer is facing additional pressure to maintain consumption levels:

{kind=link}

The continuation of the Fed's rate policy is already having the desired effect of slowing down consumer credit and also US CPI is receding with the latest print coming at 3% YoY (3.1% expected).

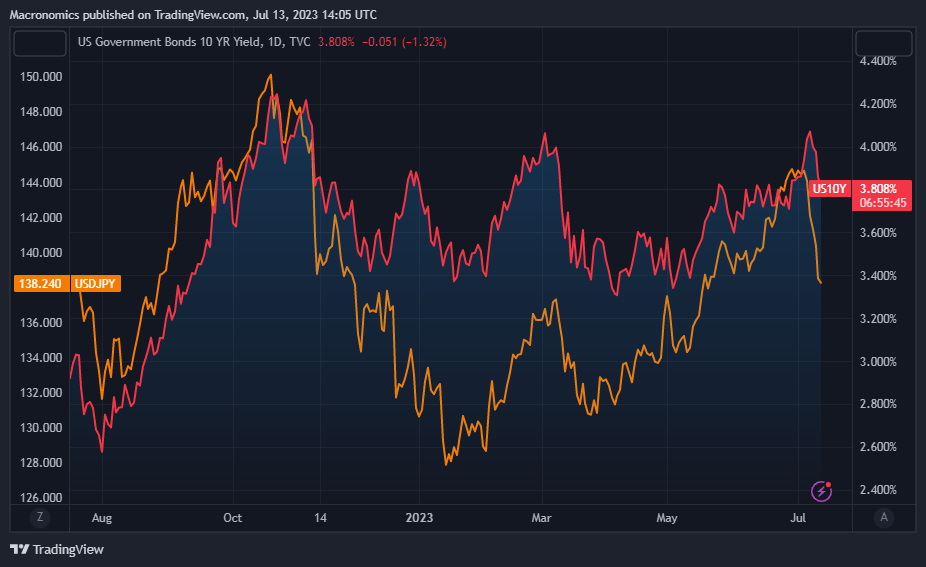

Both the US 10-year yield and the USD/JPY have moved in lockstep during the course of 2022 and continued to move in synch in 2023. On our twitter feed for those who follow us we pointed out the growing divergence on July 7 when we indicated that more Japanese yen was coming:

USTs 10 year yield vs USD/JPY 1 year chart (Macronomics - TradingView)

{kind=link}

Given the latest print of US CPI we believe we have seen for now the peak in real yields and more Japanese yen strengthening is on the card.

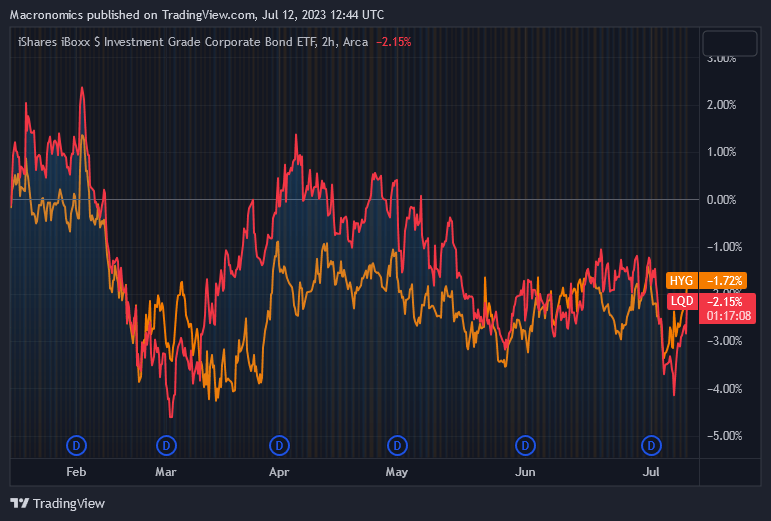

We also think that as such, ETF LQD (US Investment Grade) should potentially outperform again ETF HYG (US High Yield) in the second part of the year as per the 6-month performance chart below:

ETF LQD vs ETF HYG 6 months chart (Macronomics - TradingView)

{kind=link}

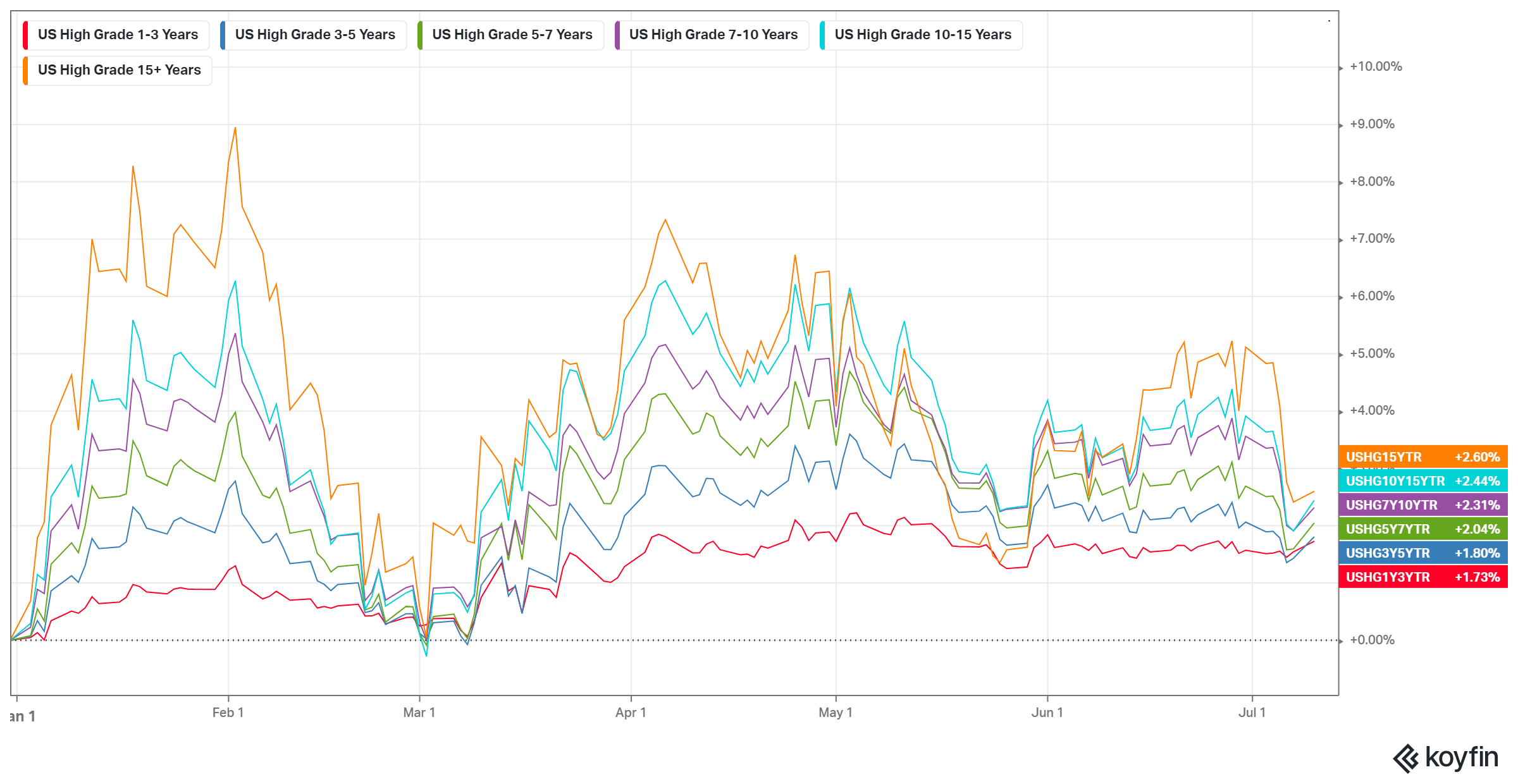

US Investment grade which has been lagging "high beta" such as US High Yield since the beginning of the year should as well benefit from receding "real yields" for the time being:

US Investment Grade YTD return by maturity bucket (Macronomics - KOYFIN)

{kind=link}

Obviously receding "real yield" continues to be a boon for TECH and growth stocks. The issue of course is that we see it more as a continuous support from multiple expansion than through earnings.

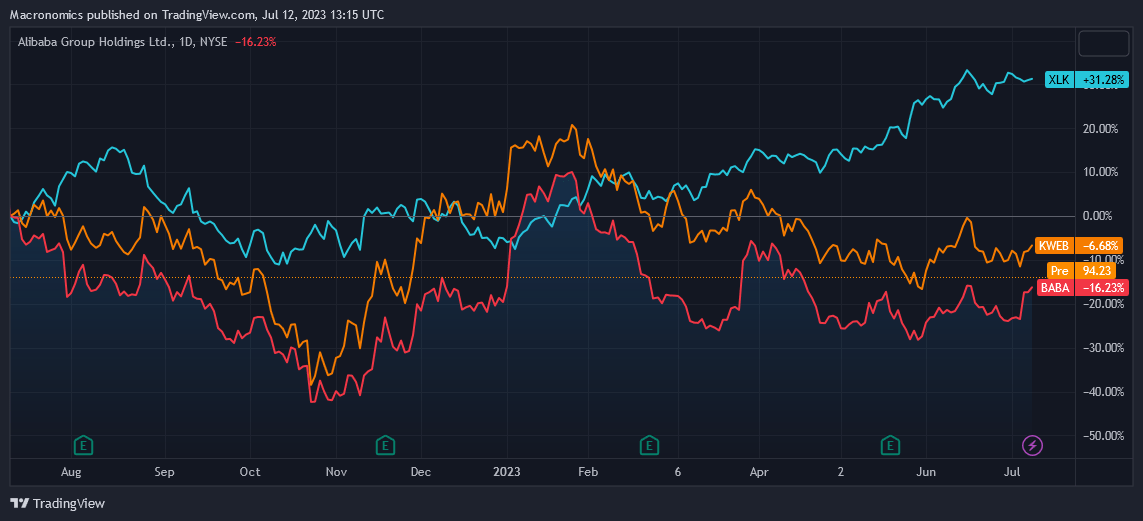

We discussed in our previous conversation the attractiveness of Alibaba (BABA). Since our last conversation, the stock's performance has been fairly muted but we continue to believe things are finally moving in the right direction for the stock given that China's premier has met with major internet companies and is vowing more support for the sector. This is ending a two-year crackdown on the industry (ETF XLK vs ETF KWEB vs BABA, one year chart):

ETF XLK vs ETF KWEB vs , one year chart (Macronomics - TradingView)

{kind=link}

China is joining the global rush to generative artificial intelligence, boasting close to 80 AI models from firms like Baidu and Alibaba and startups have attracted around $14 billion of funding over the last six months. On a relative basis, we continue to think Chinese tech stocks could bounce relative to its us counterparts following the end of the relentless crackdown we have seen in the space from Chinese authorities.

Funk in the UK

Since the jitters of last year relating to the near risk of the United Kingdom pension system blowing up thanks to rising "yields" in the long end, we have put the United Kingdom on our radar given it seems to us more and more that the UK is more and more trading "debt" wise like an Emerging Market country and its growing economic woes are piling up in conjunction with entrenched inflationary pressure. The Bank of England is indeed in a much less favorable position than the US Fed for instance. We discussed in our conversation " Tacitus Trap " the Bank of Japan moved which at the time triggered the British gilts blow up as a reminder.

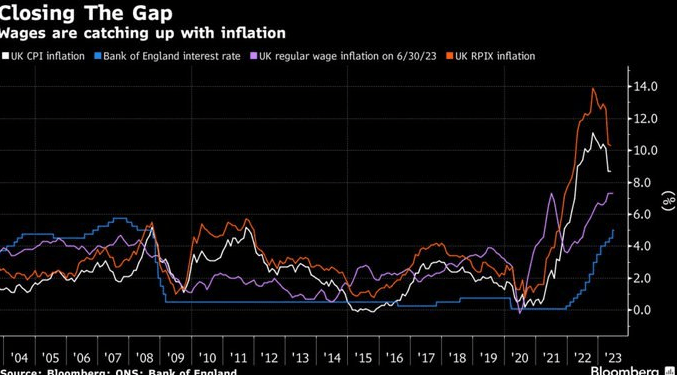

The Bank of England is in the difficult situation of seeing wages catching up with inflation:

{kind=link}

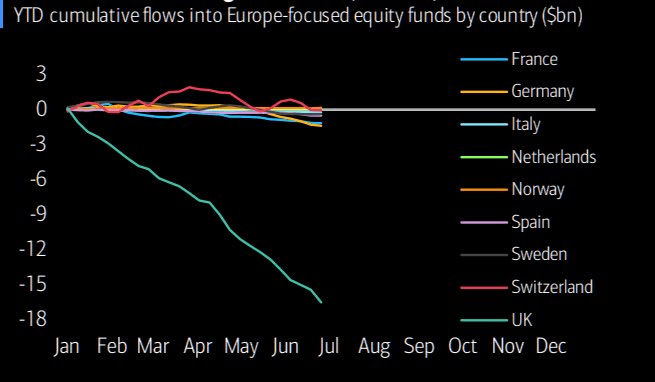

If YTD cumulative flows into Europe can be seen as further indication on investors' concerns on the United Kingdom:

{kind=link}

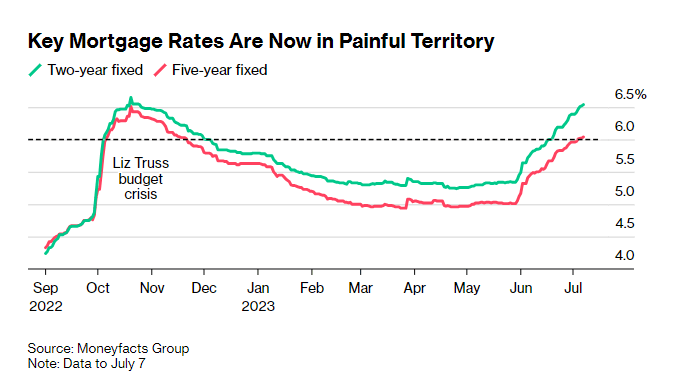

The continuation of rising key mortgage rates is adding to the ongoing inflationary woes impacting UK consumers:

{kind=link}

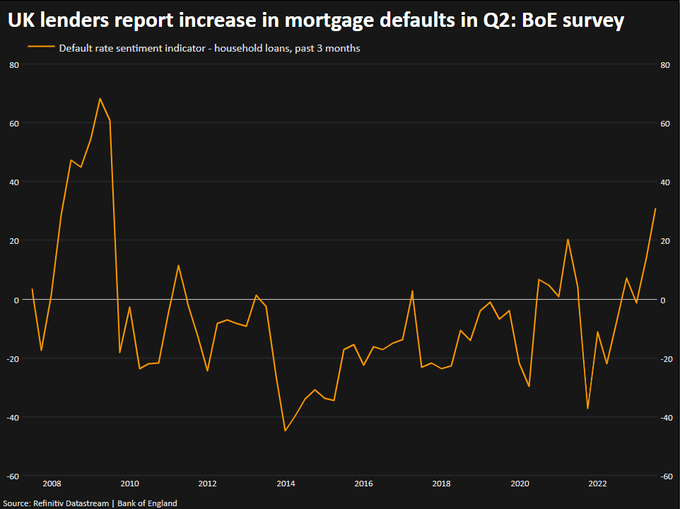

As well, UK lenders report a noticeable increase in mortgage defaults in Q2 and the highest reading since 2009, although still some way off financial crisis levels. So, all in all, the situation from an economic perspective in the United Kingdom is deteriorating:

{kind=link}

Looking at the UK conundrum, how many hikes will the "bond vigilantes" ask without any fiscal adjustment? We wonder given UK government bond borrowing is at its highest since the mid-1940s, and the stock of government debt is at its highest level since the early 1960s. On top of that the cost of debt servicing is at its highest since the late 1980s. State pension spending faces a GBP 23 billion increase by 2027-2028 and utilities such as Thames Water (GBP 14 billion in debt) are in the need of a state bailout:

Thames Water debt to equity (Bloomberg - Twitter)

It looks to us that the United Kingdom is facing an Emerging Market disease, namely an "Internal debt bubble" as explained in a recent video by our friend Geoffrey Fouvry's.

If some DMs (Developed Markets) trade like new EMs (Emerging Markets), then to paraphrase Josep Borrell the European Union High Representative of the Union for Foreign Affairs and Security Policy, the "garden" is quickly turning into a "jungle". No bueno…

"To know what you know and what you do not know, that is true knowledge." - Confucius.

For further details see:

The Overton Window