HCP - The Paradox Of HashiCorp: Impressive Growth Met With Overvaluation

2023-06-21 23:37:48 ET

Summary

- HashiCorp has a strong cash position and impressive top-line growth, but overvaluation and a longer timeline to profitability make it less attractive for immediate buying.

- The company faces risks from macroeconomic uncertainty, reliance on larger deals, and uneven cloud adoption across industries and geographies.

- The "Hold" recommendation is based on a cautious approach given the prevailing market and economic conditions.

Thesis

This article delves into the financial and operational landscape of HashiCorp (HCP) by laying out an analysis of its valuation metrics, financial performance, product innovation, market strategy, as well as potential risks and headwinds. Despite positive elements, my thesis argues for a "Hold" recommendation, advocating for a cautious approach given the prevailing market and economic conditions.

Company Overview

HashiCorp, Inc., a player in the realm of multi-cloud infrastructure automation, offers innovative solutions across the globe. A flagship offering is Terraform, a product that brings the concept of Infrastructure-as-Code to the fore, eliminating the traditionally manual and ticket-based approach.

Another feather in HashiCorp's cap is Vault, a product designed to manage secrets and protect data. It provides security teams the power to implement policies grounded in user identity and application specifics, thereby controlling access to sensitive information and credentials.

Consul, their application-centric networking automation product, has multiple benefits. It allows practitioners to control application traffic, security teams to safeguard and regulate inter-application access, and operations teams to automate the underlying network infrastructure.

Additionally, they offer Nomad, an orchestrator for scheduler and workload, which gives practitioners a user-friendly platform to manage the application lifecycle.

Founded in 2012, HashiCorp calls San Francisco, California its home.

Expectations

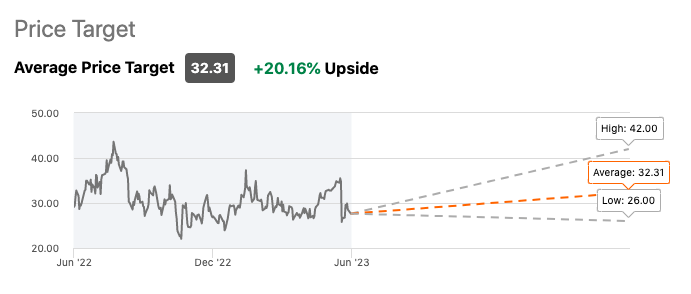

I was pleasantly surprised, considering that the company has only been around for about a decade, that it's followed by 18 Wall Street analysts who have an average "Buy" rating on the stock with a 20%+ upside potential.

{kind=link}

Performance

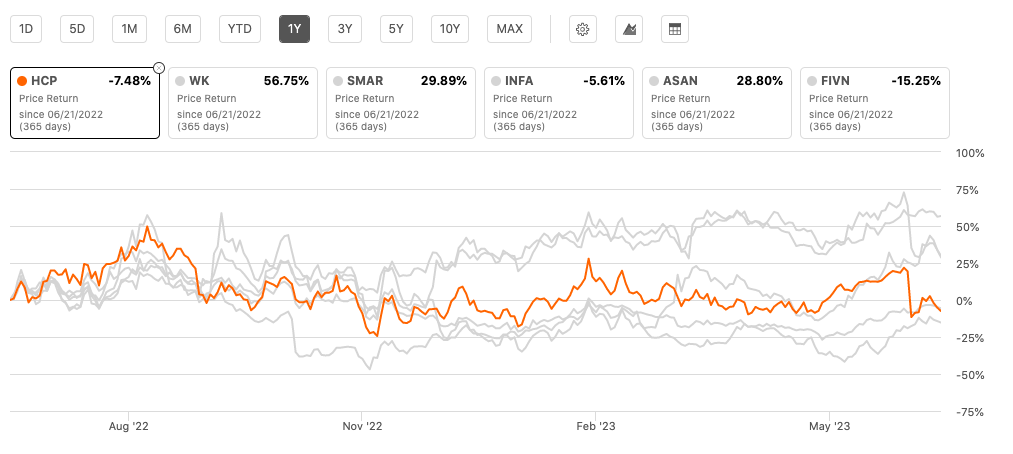

However, despite the optimistic "buy" sentiment, HCP's price return has lagged considerably relative to half of its peers.

{kind=link}

Valuation

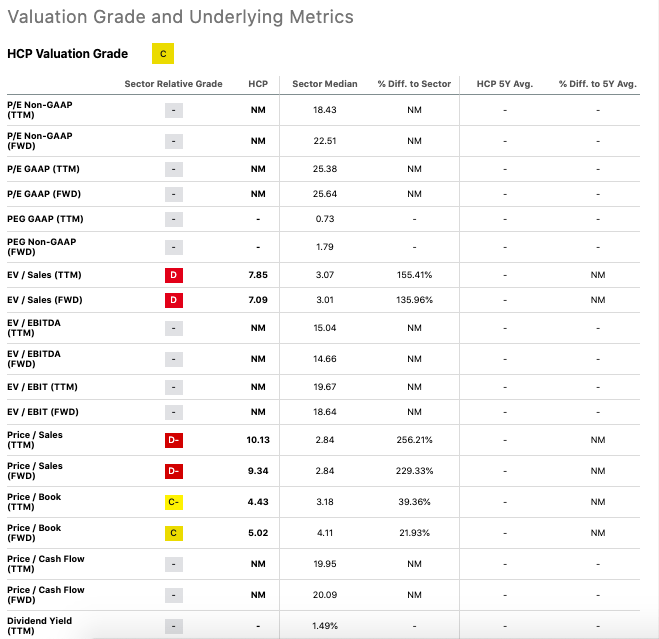

The most prominent issue for HashiCorp comes from its EV/Sales and P/S ratios (see table below), both of which are noticeably high on a TTM and forward-looking basis. This indicates the company’s valuation is significantly higher than the sector median, hence potentially overvalued. A "D and D-" rating in EV/Sales (TTM, FWD) and P/S (TTM, FWD) respectively underscores the firm’s expensive price tag relative to its sales.

{kind=link}

Furthermore, an elevated P/B ratio (TTM and FWD) relative to the sector median further accentuates this issue, revealing that the market has a high regard for the company’s assets. And, as you can see from the table, the fact that the majority of P/E, PEG, EV/EBITDA, EV/EBIT, and Price/Cash Flow metrics are not covered or not meaningful makes it hard to accurately measure the company’s growth and profitability against industry standards. While not entirely damning, this dearth of data restricts our full understanding of the company's financial health, hence increasing investment risks.

{kind=link}

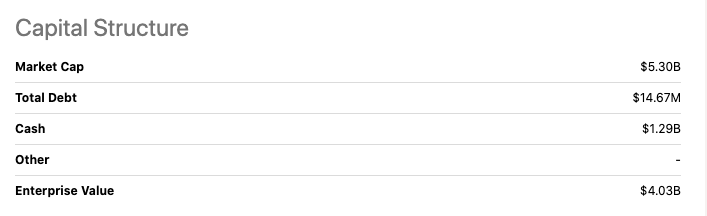

Regarding the capital structure, HashiCorp sports a robust balance sheet with minimal debt ($14.67M) against a cash reserve of $1.29B. A cash-heavy and low-debt posture insulates HashiCorp from financial distress in the short term. Its market cap of $5.30B against an enterprise value of $4.03B further confirms this strong cash position.

And finally, it’s worth noting that the company does not provide dividends. This is typical for growth-oriented firms in the tech sector, but it means investors looking for regular income may want to pass on this opportunity.

Q1 2024 Bullish Earnings Takeaways

To start with, HashiCorp's impressive top-line growth signals a healthy and expanding market appetite for its offerings. The robust 37% year-over-year growth not only beats the company's own guidance, but also illustrates a significant demand trajectory that's tough to ignore. Furthermore, the firm reported positive free cash flow for the first time, a clear testament to its improving operational efficiency and potentially a major inflection point in its financial journey.

But growth isn't merely confined to the bottom line. HashiCorp has also made significant strides in expanding its customer base, adding 32 clients with an annual recurring revenue [ARR] north of $100,000, and onboarding 26 new logos from the esteemed Global 2000 list. These milestones not only reinforce the firm's market penetration prowess but also bode well for the strengthening of its customer relationships.

Diving deeper into HashiCorp's revenue composition, one can't overlook the notable contribution of its Cloud Platform offerings, constituting 12% of the firm's subscription revenue. With cloud adoption showing no signs of deceleration, this segment poses an exciting growth opportunity for the company. Steady adoption trends further hint at a sustained revenue stream that could fuel HashiCorp's profitability engine in the long run.

Pivoting towards product innovation, HashiCorp's introduction of Boundary has piqued significant client interest. Evidently, HashiCorp's relentless drive towards innovation is not only helping address pressing customer needs but also ensuring its offerings remain at the forefront of the ever-evolving cybersecurity landscape .

Another aspect worth noting is HashiCorp's customer adoption strategy. The company's savvy approach of transitioning clients from open-source products to commercial offerings is a smart play that could foster long-term customer loyalty and ensure a steady stream of recurring revenue. And in terms of cost management and future cash flow, HashiCorp's strategic decision to reduce costs is anticipated to positively impact free cash flow margins from Q3 of this year. A projection of sustainably positive annual free cash flows in the ensuing years illustrates a financial outlook that's both promising and appealing to potential investors.

And finally, HashiCorp's guidance for the next quarter and full year further reiterates its confidence in its ongoing business strategy. Predictions of continued growth in revenues amplify this assurance, providing a positive outlook for the future. To that end, CFO Navam Welihinda noted on the latest conference call:

To summarize our guidance, for the second quarter of FY'24, we expect total revenue in the range of $137 million to $139 million and a non-GAAP operating loss in the range of $46 million to $43 million.

For the full year '24, we expect total revenue in the range of $564 million and $570 million and expect FY'24 non-GAAP operating loss in the range of $113 million and $108 million.

Risk & Headwinds

Firstly, the looming macroeconomic uncertainty casts a long shadow over HashiCorp's prospective sales and profitability. Client budgetary restrictions triggered by these uncertainties could pose significant hurdles for the company's revenue growth. Illustrating this point, CEO Dave McJannet reflected:

During Q1, Armon [co-founder & CTO] and I spent much of our time speaking with customers. A key theme from these discussions, regardless of customer size, is the uncertainty that they are feeling about the economy and what it means for their own businesses. As we have mentioned in the last few earnings calls, we saw this budget uncertainty start in October of last year as higher interest rates began to impact our customers thinking about their FY'23 budget cycles.

This economic uncertainty is driving organizations to optimize their software spend. Procurement teams are scrutinizing many larger software purchases and stretching deal cycles. As deepening inspection of budgets is happening across all of our customer segments, but most notably in our largest customer deals

Secondly, HashiCorp's reliance on larger deals for a considerable portion of its business model could turn into a double-edged sword. On one hand, these larger contracts can substantially boost revenues, but on the other hand, budgetary scrutiny on large expansion deals in the current economic context might exert considerable pressure on HashiCorp's growth rate. The fallout from this pressure could potentially rattle the firm's financial foundations.

In response to these economic challenges, HashiCorp has made the difficult decision to trim its workforce by 8% . While this move can be viewed as a necessary strategy for cost control, it risks dampening employee morale and potentially impeding the pace of product development and innovation in the near term.

When we shift our lens to the varying pace of cloud adoption across industries and geographies, it's clear that this unevenness could potentially inject volatility into HashiCorp's revenue growth. While the overarching trend towards cloud computing remains undeniably favorable, the fluctuations in the adoption pace can yield irregular revenue growth and may make forecasting a challenging endeavor.

Moreover, HashiCorp's dependence on a select group of high-value customers does expose the company to specific vulnerabilities. A small group of these customers wield substantial influence over HashiCorp's financial health, meaning that their budget decisions could significantly impact the company's revenues. The recent adjustment in spending by one of HashiCorp's largest clients in the retail sector offers a case in point, underscoring how changes in spending patterns of key clients can pose significant risks to the firm's financial performance.

Lastly, HashiCorp's target to reach non-GAAP EBIT profitability by the second half of FY 2025 might raise eyebrows among investors eager for quicker returns. Delayed profitability, while not uncommon for fast-growing tech companies, could test the patience of some stakeholders.

Final Takeaway

Given these points, my recommendation would be a "Hold". The company's positive cash flow, impressive top-line growth, and expanding customer base are encouraging. However, the current overvaluation, the longer timeline to profitability, and the uncertain economic conditions make it less attractive for immediate buying.

For further details see:

The Paradox Of HashiCorp: Impressive Growth Met With Overvaluation