PNTG - The Pennant Group: This Value-Based Care Play Is A Strong Buy

2023-04-21 13:39:33 ET

Summary

- The Pennant Group was spun out of Ensign Group in 2019.

- The company runs Home Health and Hospice agencies and Senior Living facilities.

- Pennant is profitable and drove $473m of revenues in 2022 - guidance for 2023 is for revenues of $503.5m-$518.5m and EBITDA of $38.4m-$42.6m.

- The company has substantial exposure to the fast-growing and very lucrative Medicare Advantage industry, and its business model is ideally suited to this industry.

- CVS Health recently paid $10.6bn to acquire a similar business in Oak Street Health and its 169 clinics. Pennant Group has 95 agencies and 49 Senior Living facilities but is only valued at $368m - that makes me believe this is a strong buy opportunity.

Investment Overview

"Value-based care" is an expression that anybody with even a passing interest in US healthcare stocks - or indeed a passing interest in their health insurance - is likely to be becoming increasingly familiar with.

What is value-based care? And why has it become so closely aligned with another health insurance trend that readers are doubtless hearing more and more about - Medicare Advantage?

Here are a couple of quotes I found while searching online that help to explain the twin concepts of value-based care, and Medicare Advantage, and their relationship. According to the Better Medicare Alliance :

Medicare Advantage is built on a value-based system in which Medicare Advantage health plans receive a per-member, per-month payment for each beneficiary's care, and are tasked with using those dollars most effectively - incentivizing high quality, high-value care for the 24.2 million enrollees who trust Medicare Advantage with their health care needs.

Now, here's a slightly more pragmatic explanation from Richard Eisenberg writing for Next Avenue , a blog focused on "unleashing the potential of older Americans."

A key tenet of value-based care is managing patients' healthcare well enough, based on specific quality measures, to keep them out of hospitals when possible and shorten their stays when hospitalization cannot be avoided. It's quite different from the traditional fee-for-service system in which health care providers are paid based on the amount of treatment they provide.

Both of the above explanations make valid points, although it may not surprise readers to learn that the Better Medicare Alliance is funded by UnitedHealth ( UNH ), Aetna - now part of CVS ( CVS ), and Humana ( HUM ) the three largest providers of Medicare Advantage plans, with respectively a ~28%, 18%, and 11% share of the market .

What does all this have to do with The Pennant Group ( PNTG ), the subject of this post? To simplify a complex state of affairs, the definition of Medicare Advantage supplied by the Better Medicare Alliance is accurate - health insurers are paid a flat per-member, per month fee to administer their plans, and essentially pocket the difference if they are able to administer care for less than the Centers for Medicare and Medicaid Services ("CMS") pays them.

All Medicare Advantage plans are star rated, and the best-rated plans also receive bonus payments, so theoretically, the better patients are taken care of, the more the Medicare Advantage plan providers stand to benefit.

And that is where a company like The Pennant Group comes in. It has a presence in 14 states and runs (according to a recent investor presentation ) 95 Home Health and Hospice Agencies, and 49 Senior Living Operations.

Most health insurance plans are still based on "fee for service" i.e. a patient visits a doctor, and the doctor then sends their bill to the health insurer to be reimbursed. But a doctor's time can be expensive, and they may bill for procedures that the health insurer may not deem strictly necessary.

In the new era of value-based care, a patient can visit a Pennant Group clinic instead, where they may be seen by a qualified nurse as opposed to a doctor, and that nurse may take a more holistic approach to managing the patient's health, making sure conditions are treated before they become too serious and require a hospital visit. The nurse's time is much cheaper to reimburse than a doctor's, and the health insurer no longer has to foot the bill for an unnecessary hospital visit.

As such, companies that provide value-based care services have become hot property. Oak Street Health ( OSH ), for example, which operates 169 clinics across the US doing similar work to the Pennant Group, was acquired in January this year by CVS, in a deal that valued Oak Street at $10.6bn, or $39 per share, nearly double its traded share price at the time.

Oak Street - as I discussed in a recent note - has never been profitable, making a net loss of $500m in 2022, and $400m in 2021 - but such is the appeal of the business model to the health insurance giants that CVS did not bat an eyelid, and has projected >$2bn in embedded EBITDA from Oak Street by 2026.

Now, if we consider The Pennant Group - a similar style business, but with a market cap of just $372m at the present time, that generated $473.2m of net revenues in 2022, and was also profitable, driving adjusted net revenue of $17.1m, my conclusion is that this company's stock is emitting very strong buy signals.

In the remainder of this post, I will provide an overview of Pennant Group's business and a little more context around the evolving value-based care landscape.

The Pennant Group Overview

In its 2022 10k submission, the Pennant Group describes its business as follows:

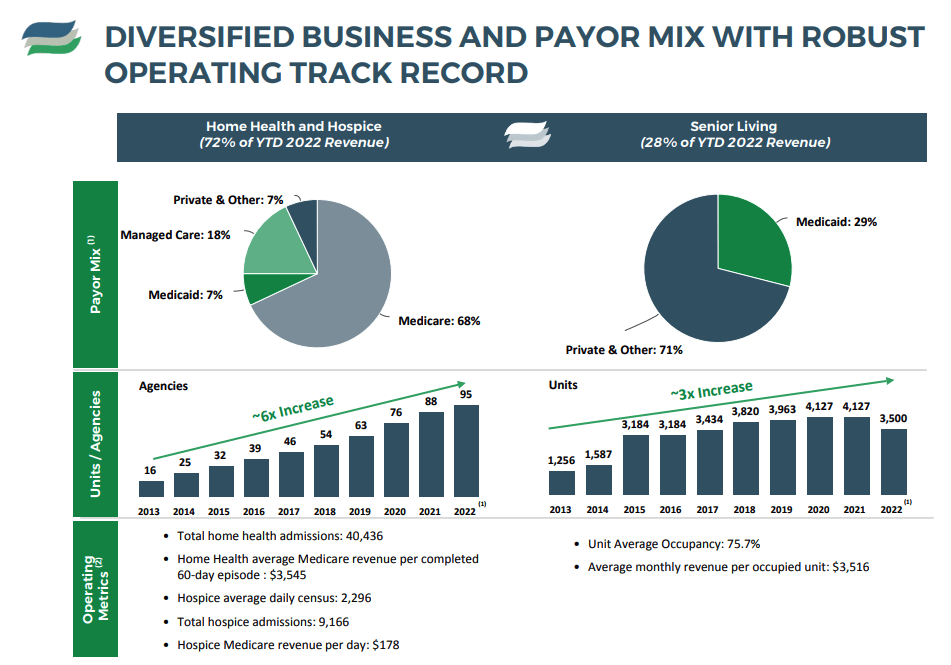

As of December 31, 2022, we operate multiple lines of business, including home health, hospice and senior living, throughout Arizona, California, Colorado, Idaho, Iowa, Montana, Nevada, Oklahoma, Oregon, Texas, Utah, Washington, Wisconsin and Wyoming. We provide home health and hospice services through 95 agencies, and senior living services at 49 communities with 3,500 total units in our assisted living, independent living and memory care business.

We derive revenue from a diversified blend of payors including Medicare and Medicaid programs, private pay patients and residents and managed care payors.

{kind=link}

As we can see above, Pennant has enjoyed impressive growth in its business since 2013. The company was spun out of The Ensign Group ( ENSG ) in 2019, and management explains in its annual report that:

The name "Ensign" is synonymous with a "flag" or a "standard," and refers to Ensign's goal of setting the standard by which all others in its industry are measured. The name "Pennant" draws on similar imagery and themes to represent our mission of becoming the "Ensign" to the home health, hospice and senior living industries.

Throughout its investor presentations and annual reports, Pennant repeatedly refers to its culture of high standards and peer accountability, advertising it as a significant strength of the business.

{kind=link}

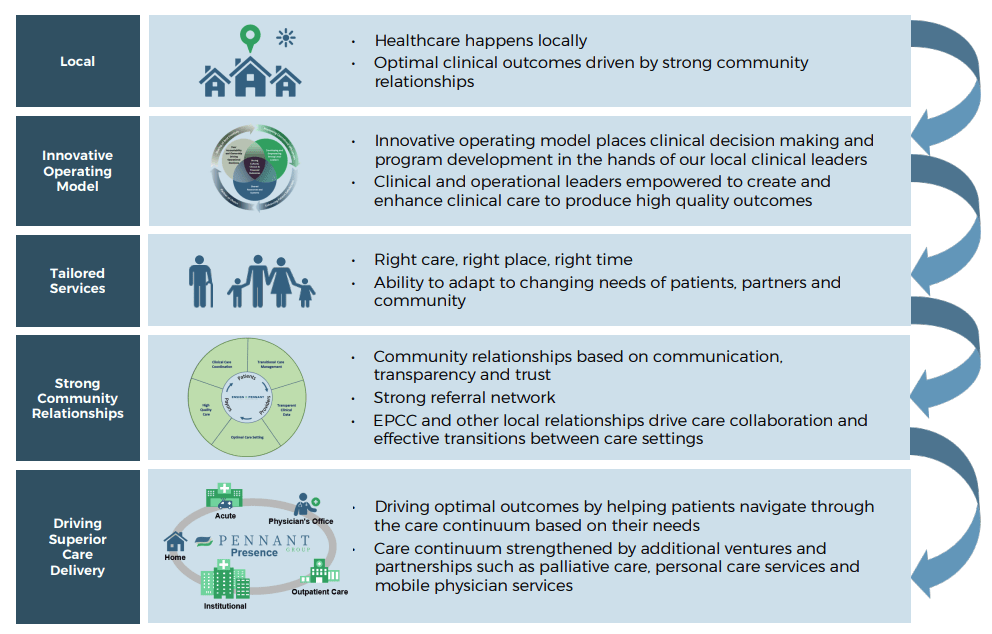

As shown above, Pennant also is focused on making sure it can be accessed locally, and that its staff and centers are in the right place at the right time. One of the criticisms that has been leveled at Medicare Advantage is that plan members may only visit certain physicians or health centers that are included in the plan - meaning access to essential care is often restricted.

Pennant's business model is clearly attempting to address this problem by making sure plan members can access services at the local level, and once again there is a strong emphasis on its staff being "leaders" who can "make key operational decisions that meet the individualized needs of their patients, residents and community partners." That may mean paying its staff a premium, but still significantly less than what a qualified physician might earn, as discussed in the Next Avenue blog:

On average, nursing assistants earn $35,180 a year, registered nurses earn $84,910, physician assistants earn $122,740, nurse practitioners earn $123,270 and family medicine physicians earn $209,020, according to Business Insider.

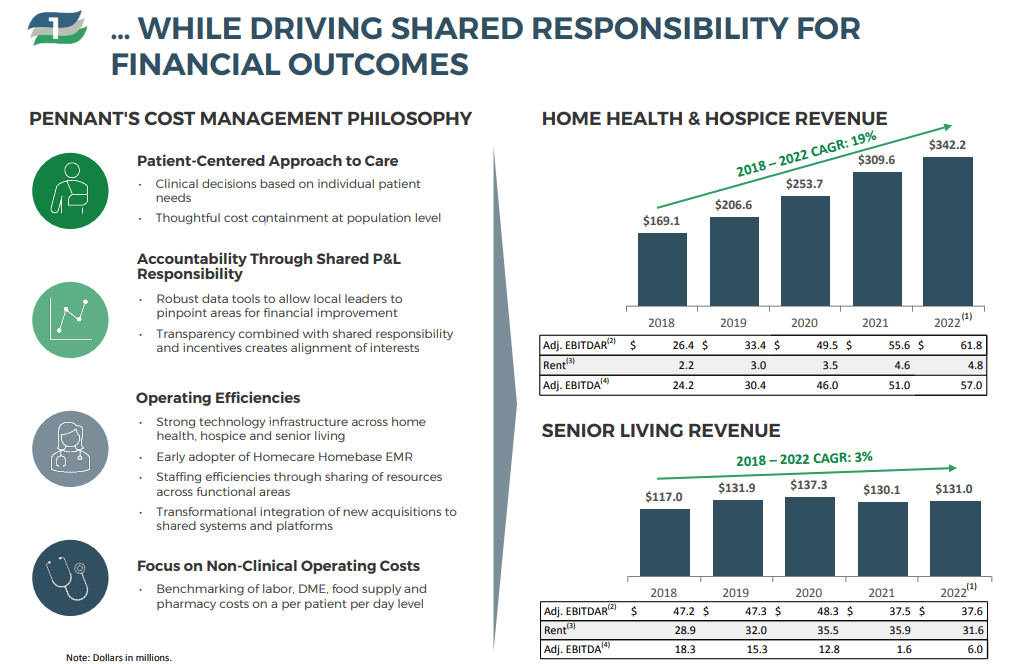

Of course, having more staff "on the ground" means being able to have more influence over health choices, and Pennant says it's focused on "shared responsibility for financial outcomes," a model that seems to be working and driving growth in the business, as shown below.

Pennant philosophy drives revenue growth (Pennant Presentation)

{kind=link}

Admittedly, the Senior Living side of Pennant's business model is not growing as well as the Home Health and Hospice revenue side, but management insists there's a substantial opportunity here - as company President and Chief Operating Officer John Gochnour explained to analysts on the Q422 earnings call :

While we took a significant step forward in 2022, enormous organic growth opportunity exists in our senior living portfolio. We remained focused on translating revenue improvement, the bottom line financial performance through rigorous cost management and cluster accountability, growing occupancy through improved sales practices and support, and accurately capturing and receiving appropriate reimbursement for the care we provide.

As our local teams succeed in these objectives, we will create stronger operating results in the senior living space and look forward to it joining our home health and hospice segment as a growth engine for Pennant's success.

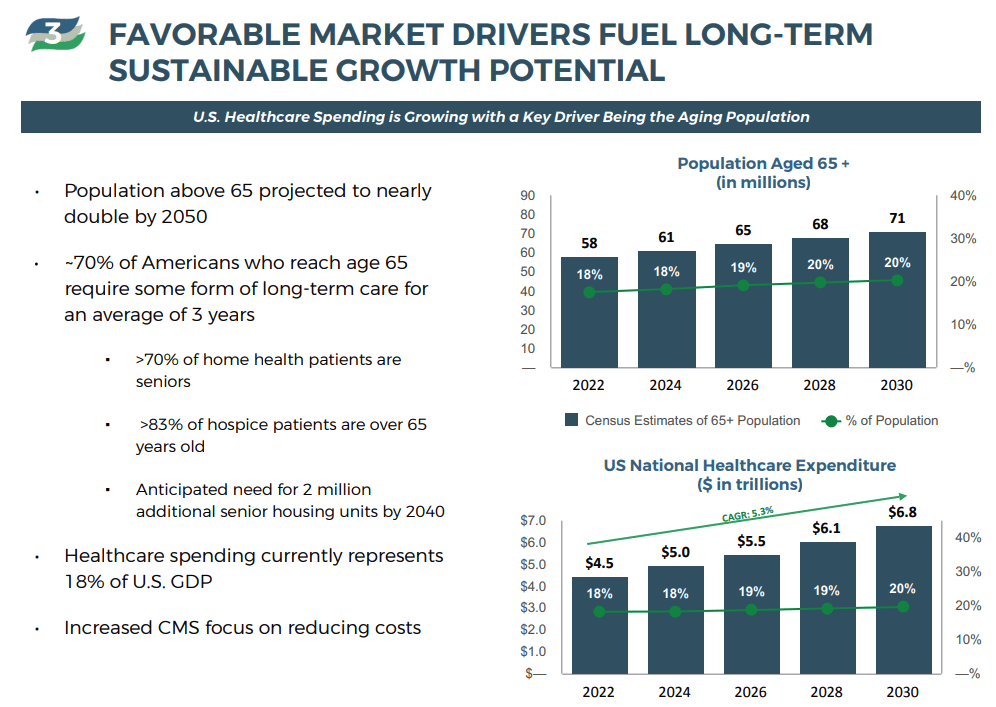

That sentiment is backed up by Pennant's market research, as below.

{kind=link}

In summary, I believe Pennant is correct to point to its ability to scale rapidly, and that in itself is consistent with moves made by healthcare giants such as CVS to acquire Oak Street, for example, and the strong growth of Medicare Advantage - according to Kaiser Family Foundation:

In 2022, more than 28 million people are enrolled in a Medicare Advantage plan, accounting for nearly half or 48 percent of the eligible Medicare population, and $427 billion (or 55%) of total federal Medicare spending (net of premiums). The average Medicare beneficiary in 2022 has access to 39 Medicare Advantage plans, the largest number of options available in more than a decade.

Furthermore, Pennant points out that the Home Health, Hospice and Senior Living industries are fragmented - the top 10 largest operators in each segment apparently account for just 27%, 19%, and 35% of the market, respectively.

In summary, Pennant appears to tick most of the boxes a healthcare provider affiliated to the health insurance industry needs to tick, and there's more besides - its clinics enjoy a star rating average of 4.3 out of five vs. a national average of 3, the company plans to grow by acquisition as well as organically - the company added three home health agencies, four hospice agencies, and one senior living community to its operations last year - the company is already profitable, and long-term debt stands at just $63m.

Some Risks To Consider

The Medicare Advantage industry has grown so quickly - after all, it's rumored 10k "baby boomers" turn 65 every day - and become so lucrative that it has caught the attention of the CMS, who are attempting to claw back some of the funds it has pumped into this nascent industry and is reluctant to raise its plan payments as much as the healthcare insurers would like.

I discussed this matter in more detail in a recent post on UnitedHealth, whose share price has suffered based on the perception that CMS is squeezing rates, although the final proposal from CMS for 2024 suggested a 3.3% rise in payments, as opposed to the >2.5% cut that health insurers had feared.

Medicare Advantage has attracted criticism - as has the concept of value-based care - for allowing health insurers to "game the system," i.e. using nurses as opposed to qualified doctors, making strenuous attempts to keep patients out of hospitals when that may be a better option, and misrepresenting the costs of servicing plan members in order to earn a higher fee.

Health insurers have powerful lobbies but given Pennant's exposure to this industry, its growth could be seriously affected by a backlash against Medicare Advantage - although equally, it may be viewed by health insurers as a way to solve many of the negative reputational issues being encountered.

The Senior Living segment of Pennant's business in its current state appears to be experiencing shrinking growth in terms of number of units - although it drives a far lower percentage of overall revenues, 27% is still a significant amount and this also strikes me as a more cash-intensive business than Home Health and Hospices, with the level of care required higher.

Pennant does not seem to be a cash-rich business - cash reported as of the end of 2022 was just $2.1m, and total current assets on 73.8m. That suggests to me that the company may look to make dilutive fundraisings to fund M&A and growing SG&A costs, which will stymie share price growth

The share price performance since Pennant was spun out also has been unusual - shares reached a peak of ~$64 in January 2021 - valuing the business at around $1.9bn based on current share count - but had rapidly declined in value to <$10 by early 2023 - a decline of >85%. Some post spin-out volatility is to be expected, but declines over such a long period are more of a concern. These declines appear to be related to a failure to grow at the pace the market demanded.

Conclusion - Not Without Risk, But Pennant Group Stock Looks Highly Attractive At Current Price And The Growth Opportunities Extremely Strong

The value-based care model is a new dynamic within the health insurance and healthcare business that presently has very strong momentum, although there's still a very long way to go - Goldman Sachs believes this is an industry that could be worth >$1 trillion one day, and it's already attracting billions of dollars of private and now public investment.

Based on my research Pennant Group does look to be ideally positioned within this space. Unlike many of its rivals, it has been spun out of an already successful listed company - the Ensign Group, and it's profitable, and it seems to have inherited Ensign's relentless focus on the quality of staff who can be leaders and establish valuable connections at the local level.

This last point particularly impresses me given many of the new wave of Value Based Healthcare startups have attempted to focus on technology, arguing that they can use data to eliminate inefficiencies. In my experience health plan members are unimpressed with tech and prefer personalized care to be delivered by real people, be they nurses, or doctors, and as such I believe Pennant Groups' model can be a winning one.

Most of all, I like Pennant's current valuation, which is >28x lower than the figure Oak Street was purchased for, and nearly 6x lower than the market cap valuation of another rival, Apollo Medical Holdings ( AMEH ).

In summary, based on all of the above, I believe Mr. Market has been punishing Pennant far too heavily for a failure to grow - an issue the company looks highly likely to address successfully in the coming years, and my thinking is that shares in Pennant Group look a steal at the current valuation.

For further details see:

The Pennant Group: This Value-Based Care Play Is A Strong Buy