INVH - The Perfect Blend Of Growth And Income: Invitation Homes And Crown Castle

2023-03-24 12:39:47 ET

Summary

- In this article, we start with the pros and cons of investing in real estate (REITs), as I am not a fan of the historical performance of major REIT ETFs.

- I present two REITs that I like, starting with Invitation Homes, the nation's largest single-family housing REIT, which comes with a decent yield and growth potential.

- My second pick is Crown Castle, the cell-tower giant that comes with a high yield, high expected long-term dividend growth, and growth opportunities in 5G and the Internet of Things.

Introduction

If there's one thing I cannot stop mentioning, it's that I'm extremely picky when it comes to higher-yielding investments. As much as I like a stock that comes with a decent yield, I'm somewhat (read: very) afraid of buying a company that has close to no growth and a high likelihood of underperforming the market on a long-term basis. The high-yield space is sometimes a minefield as too many investors look for yields only. Hence, in this article, I want to share two REITs with you that I have added to my model portfolios this month.

The first one is Invitation Homes (INVH) , a company that is relatively new to the stock market. This giant buys houses in bulk and has a smooth business model that allows it to manage thousands of homes across the country.

Pick number two is the peer of the American Tower Corporation ( AMT ), which I discussed recently. Crown Castle (CCI) is a North America-focused cell tower REIT with a wide moat, a juicy yield, and plenty of future dividend growth.

While macroeconomic headwinds persist, I am looking to add both to my dividend growth portfolio at some point.

Now, let me explain why that is.

The Pros And Cons Of Investing In REITs

The graph below shows why I am so careful when it comes to real estate. Both the iShares US Real Estate ETF ( IYR ) and the Vanguard Real Estate ETF ( VNQ ) have underperformed the market by a wide margin since 2006. This is on a total return basis, meaning it includes dividends. These two REIT ETFs also underperformed the somewhat boring and slow Vanguard High Dividend Yield ETF ( VYM ).

With that said, there are some pros and cons when it comes to real estate investing.

Pros

- Diversification : REITs offer investors exposure to a diversified portfolio of real estate assets, reducing risk compared to owning individual properties.

- Income : REITs are required by law to distribute at least 90% of their taxable income to shareholders, providing a potentially attractive source of dividend income.

- Liquidity : REITs are traded on stock exchanges, making it easy for investors to buy and sell shares quickly.

- Professional Management : REITs are managed by experienced real estate professionals who oversee property operations, acquisitions, and dispositions.

In other words, most of the pros are based on getting well-diversified exposure to income tools. Hence, it's not really a surprise that these ETFs underperform the market, which is focused on growth.

Cons

- Interest rate sensitivity : As a leveraged asset class, REITs are sensitive to changes in interest rates. Rising interest rates can lead to higher borrowing costs, which can impact cash flows and profitability. Right now, we're in a situation where REITs suffer from high rates. This means we need to focus on REITs with healthy balance sheets (we always should do that).

- Market volatility : REITs are publicly traded securities and are subject to market volatility, which can impact stock prices and investor returns. This is also related to the above-mentioned interest rate sensitivity. REITs are way more volatile than the price of your home.

- Economic sensitivity : REITs are tied to the performance of the underlying real estate assets they own, which can be impacted by changes in the economy, industry trends, and competition. In other words, investors who avoid ETFs need to be on top of industry developments.

With all of this in mind, I believe that both Invitation Homes and Crown Castle offer unique characteristics that will allow them to beat their peers on a long-term basis while providing decent income.

High-Quality Residential Real Estate

With a market cap of almost $18 billion, the Invitation Homes REIT is one of the world's largest residential real estate owners. The company owns more than 80,000 homes in 16 markets across the United States.

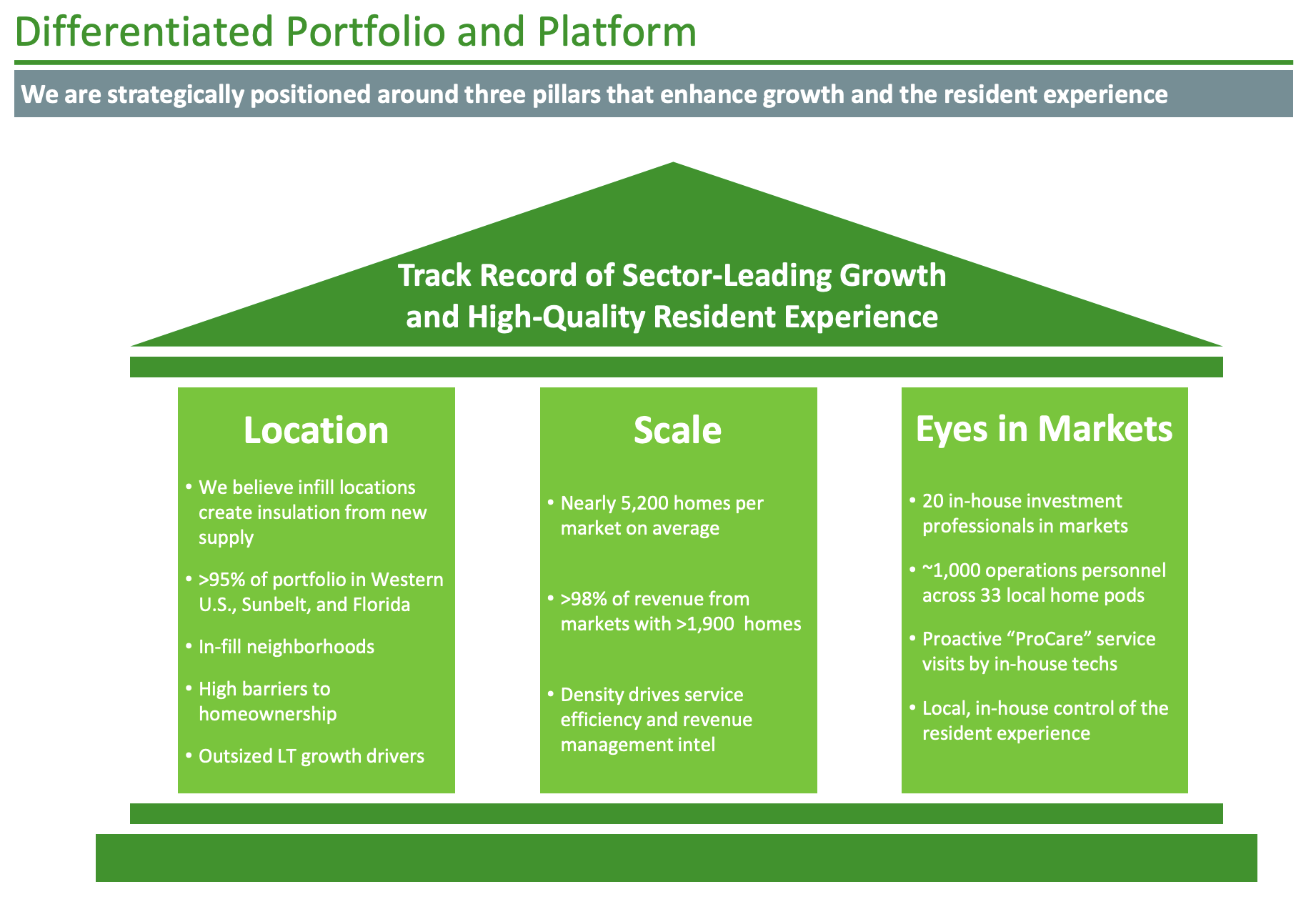

The company owns and manages homes in different regions of the United States, mainly in the Western part, Florida, and the Southeast. They choose these markets based on factors such as high demand for housing, high potential for rental growth, and significant barriers to entry. By being selective about where they invest, Invitation Homes believes they can capture the advantages of local density and economies of scale that are difficult for competitors to replicate.

Since it was established in 2012, Invitation Homes has developed an integrated operating platform that enables them to acquire, renovate, lease, maintain, and manage their homes efficiently. The homes they own average about 1,870 square feet, with three bedrooms and two bathrooms, which they believe appeals to residents who are more likely to stay for a longer time. They also invest in renovating their properties to reduce maintenance costs and attract tenants.

{kind=link}

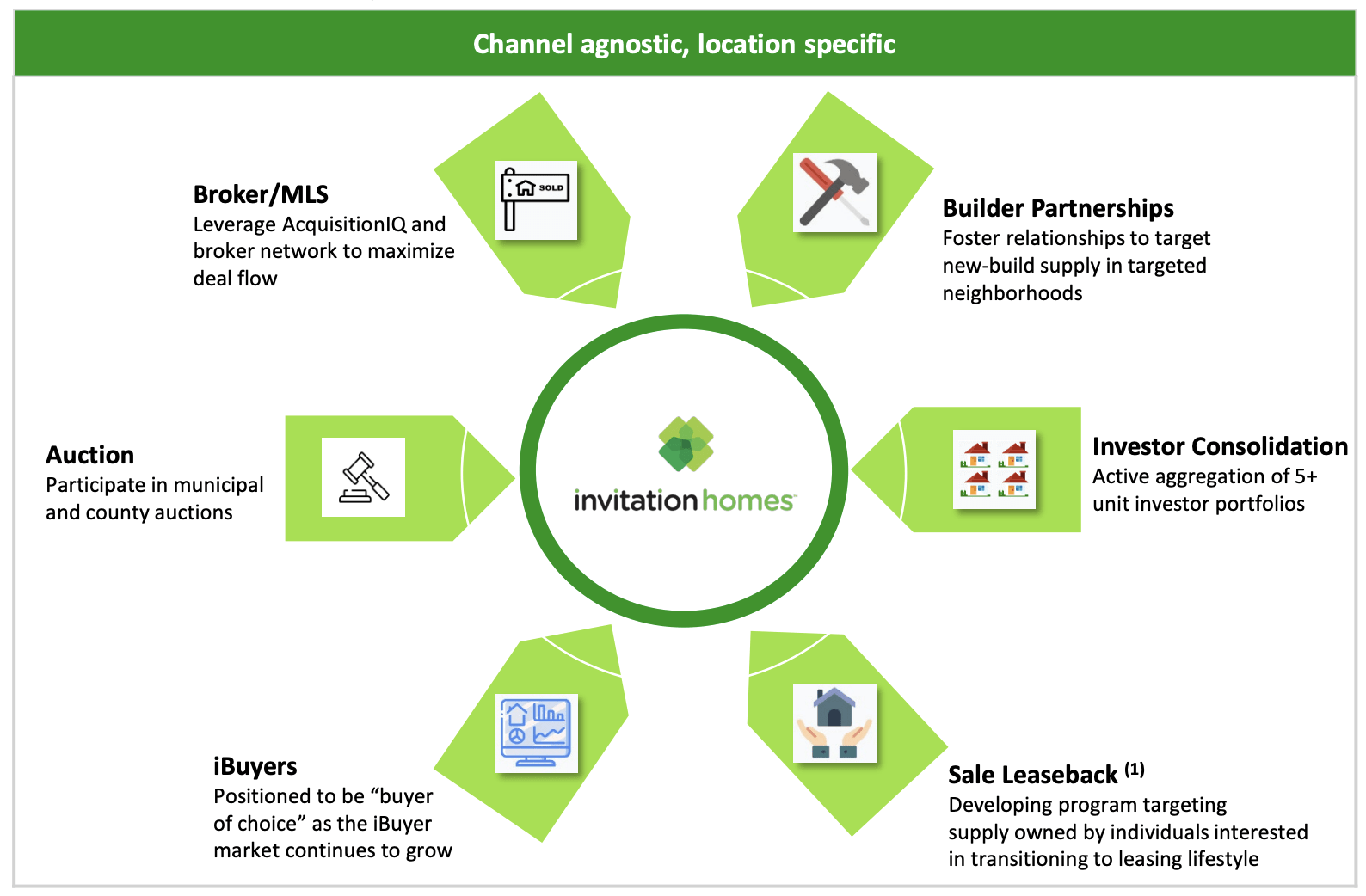

Moreover, the company has a dedicated in-house acquisition team with local expertise to identify desirable submarkets and neighborhoods for their single-family homes. They prioritize high-quality homes in high-growth, undersupplied markets that they believe will attract a stable tenant base and experience rental rate growth and capital appreciation. They also collaborate with local brokers and technology platforms to identify off-market opportunities. With a large portfolio and experience, they have a high degree of visibility into rental rates and expenses, enabling them to accurately forecast net yields. They also use feedback from past acquisitions to support future investment decisions.

This model also includes sale-leasebacks, which means homeowners sell their house to INVH (for whatever reason) and rent it back. This happens a lot in the industrial space, where companies access new capital by selling their property.

{kind=link}

For example, in Atlanta, the company owns close to 13,000 homes. The city is divided into five segments, each with less than 3,000 homes. These homes are managed by one vice president of operations, two directors of operations, five portfolio directors, and close to 80 maintenance technicians (among others).

These operations include ProCare, which is the company's maintenance program designed to satisfy tenants and minimize the number of trips maintenance workers make. After all, managing thousands of homes can be a nightmare from a cost perspective.

With that said, the company has a few things going in its favor.

- The housing market is underserved, which is further pressured by rising labor and material costs. On top of that, cities face increasing land scarcity and regulatory hurdles that increase entry barriers (less pressure from competition).

- These inflationary headwinds have significantly increased the replacement cost for single-family housing.

- Rising mortgage costs have made buying less affordable.

Moreover, the company operates in a segment that attracts higher-income clients. New residents have an average annual income of approximately $134,000 and an income-to-rent ratio of 5.2x. The nation's average is roughly 3.3x.

It also helps that INVH has a stellar balance sheet. As of December 31, 2022, the company had $1.3 billion in available liquidity through a combination of unrestricted cash and undrawn capacity on its revolving credit facility.

The company's net debt ratio was 5.7x, which is down from 6.2x at the end of 2021.

In light of the current high-rate environment, it is also important to note that the company has no maturities until 2026. 74% of the company's debt is secured, and 99.2% of the company's debt is either fixed-rate debt or secured by hedges.

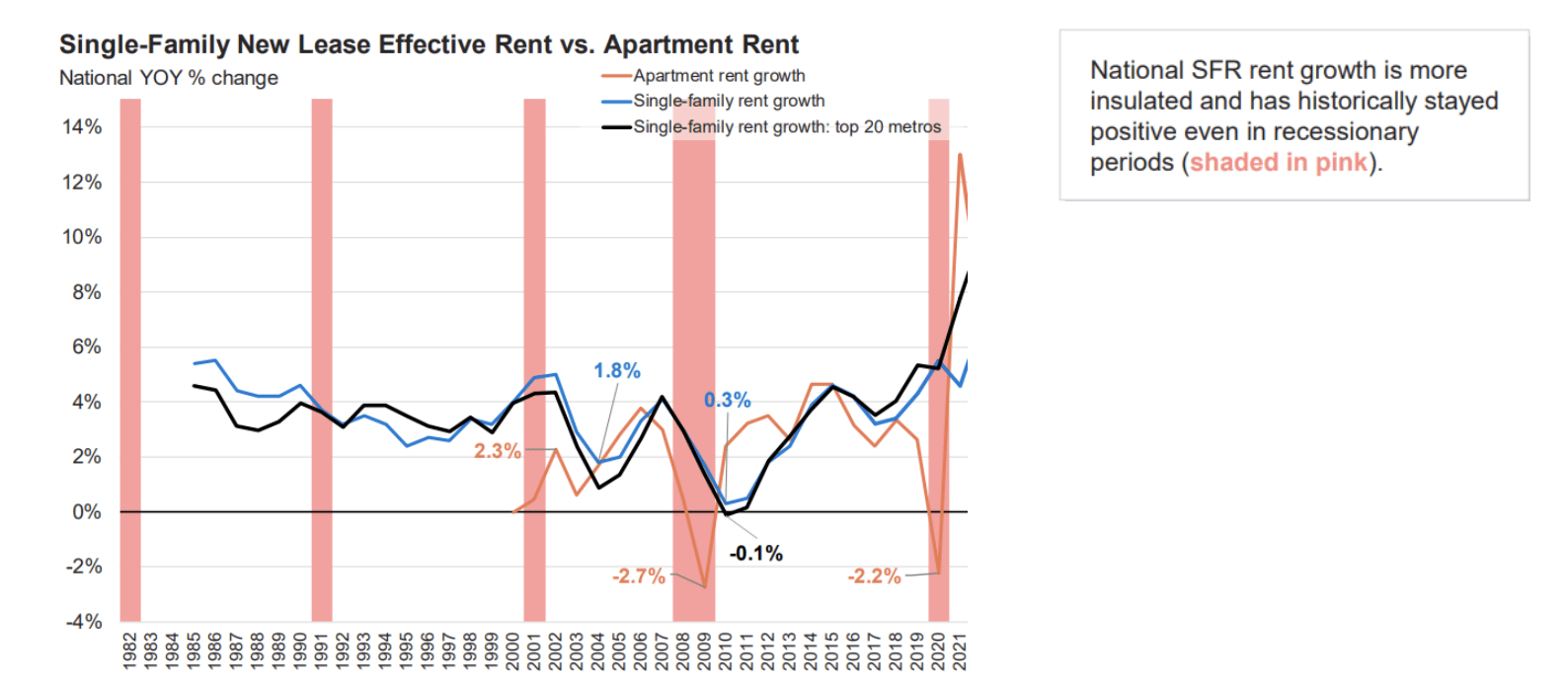

Moreover, not only are its clients financially strong, single-family rent growth never had a year with declining rents in more than 40 years of data collection.

{kind=link}

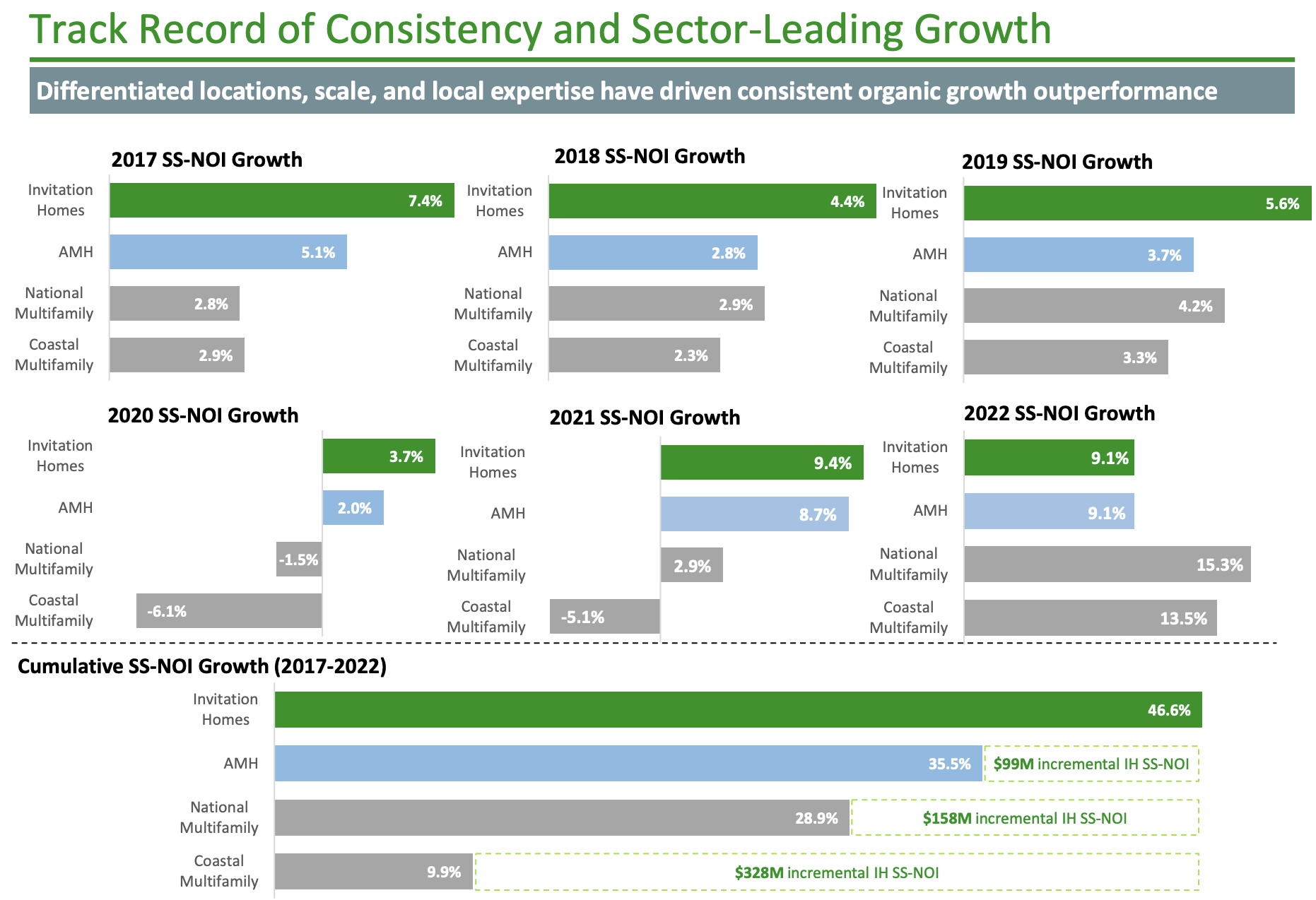

When combining these tailwinds, we get a high probability that INVH will outperform its industry peers as it did in the past five years.

{kind=link}

With that said, in 2022, the company did $1.67 in core funds from operations per share. That number was supported by 9.0% core revenue growth and 9.1% net operating income growth. The average occupancy rate slightly dropped from 98.2% in 2021 to 97.7%. The turnover rate dropped to 21.9%, while the bad debt ratio barely increased from 1.4% to 1.5%.

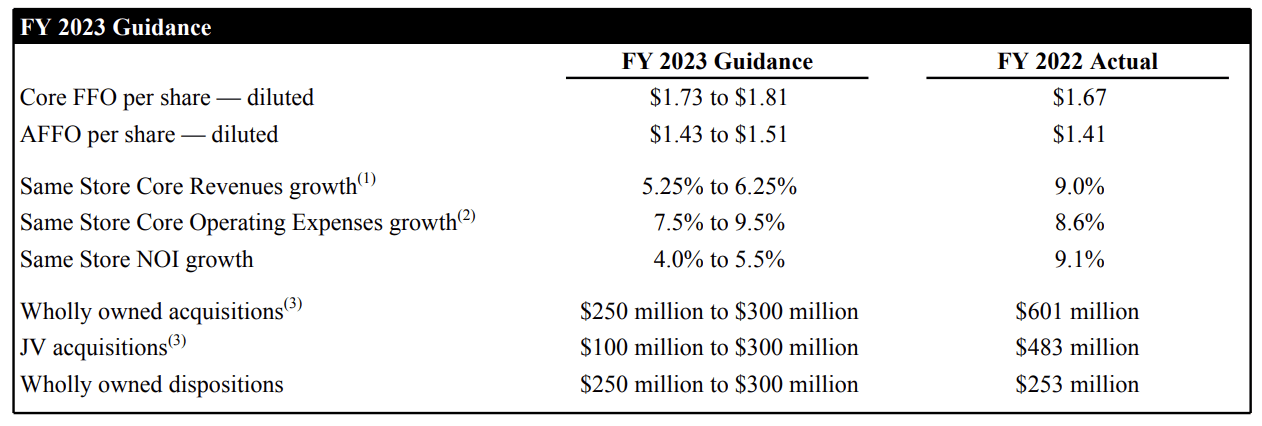

This year, the company expects at least $1.73 in core FFO, boosted by at least 4.0% same-store net operating income growth.

{kind=link}

This implies that INVH shares are trading at 16-16.7x 2023 core FFO. That valuation is fair.

Despite these numbers, INVH shares have been under pressure. Higher rates and the impact this is expected to have on the housing market keep investors away. Yet, INVH shares are still outperforming the REIT sector. I expect that to continue. Even better, once the housing market recovers, I expect outperformance to accelerate.

Moreover, the company currently pays a $0.26 per quarter dividend. This translates to a 3.6% dividend yield. On February 3, the dividend was hiked by 18.2%. Over the past three years, the average annual dividend growth was 19.4%. The FWD FFO payout ratio is 57%. The sector median is 65%. While I expect dividend growth to moderate, INHV is a neat long-term dividend growth REIT, which sets it apart from major REITs unable to grow their dividend.

So, with all of this in mind, if the real estate market takes another hit, I believe that INVH is a great stock to buy.

The Power Of Cell Phone Towers

Crown Castle is the peer of a stock I discussed earlier this month: American Tower.

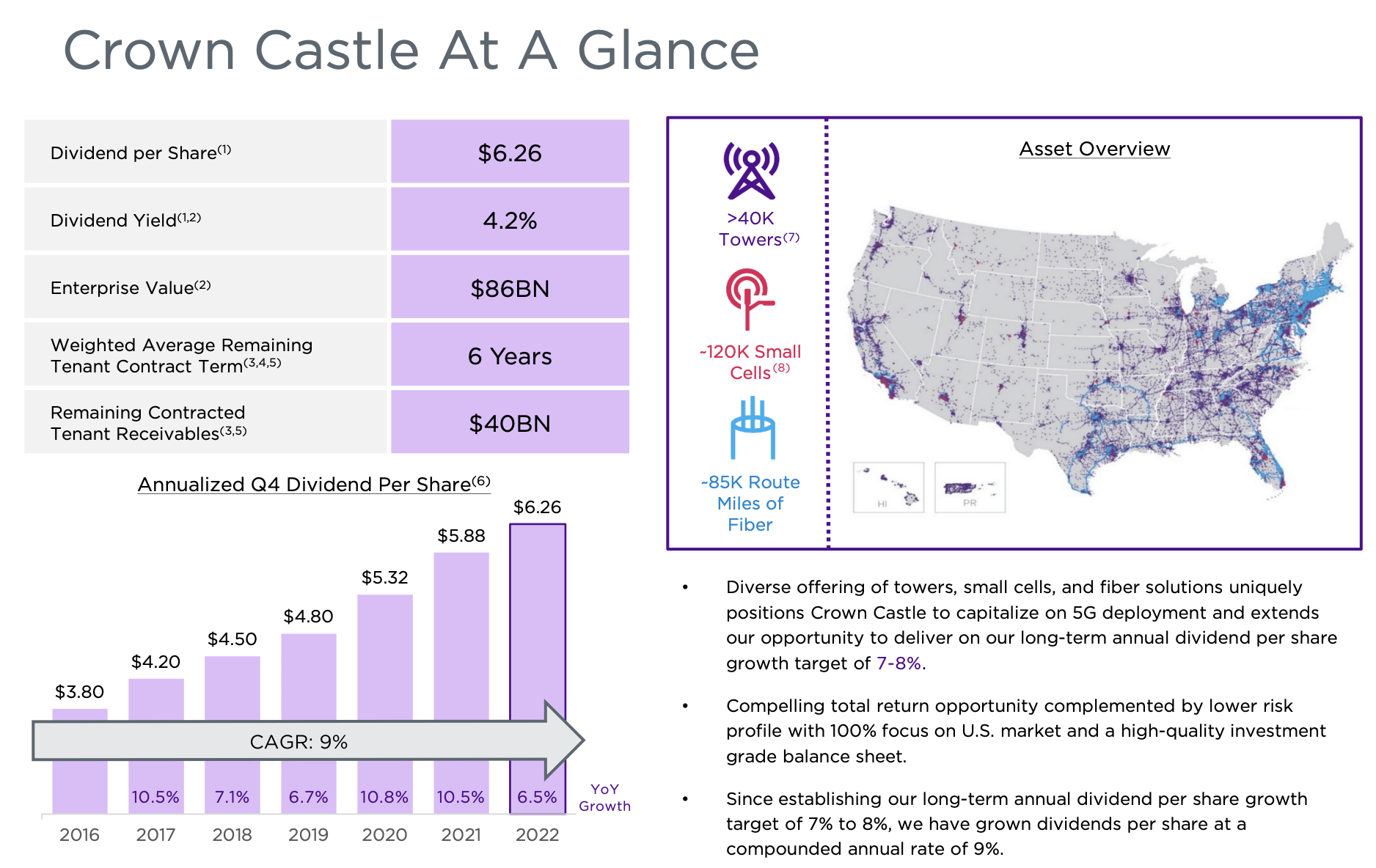

With a market cap of $54 billion, CCI is one of the largest REITs in the United States.

Crown Castle is a company that owns, operates, and leases shared communications infrastructure throughout the United States. This infrastructure includes over 40,000 towers and other structures, approximately 120,000 small cells, and approximately 85,000 route miles of fiber. The company's main business is providing access to this infrastructure to tenants through long-term contracts, including lease, license, sublease, and service agreements.

{kind=link}

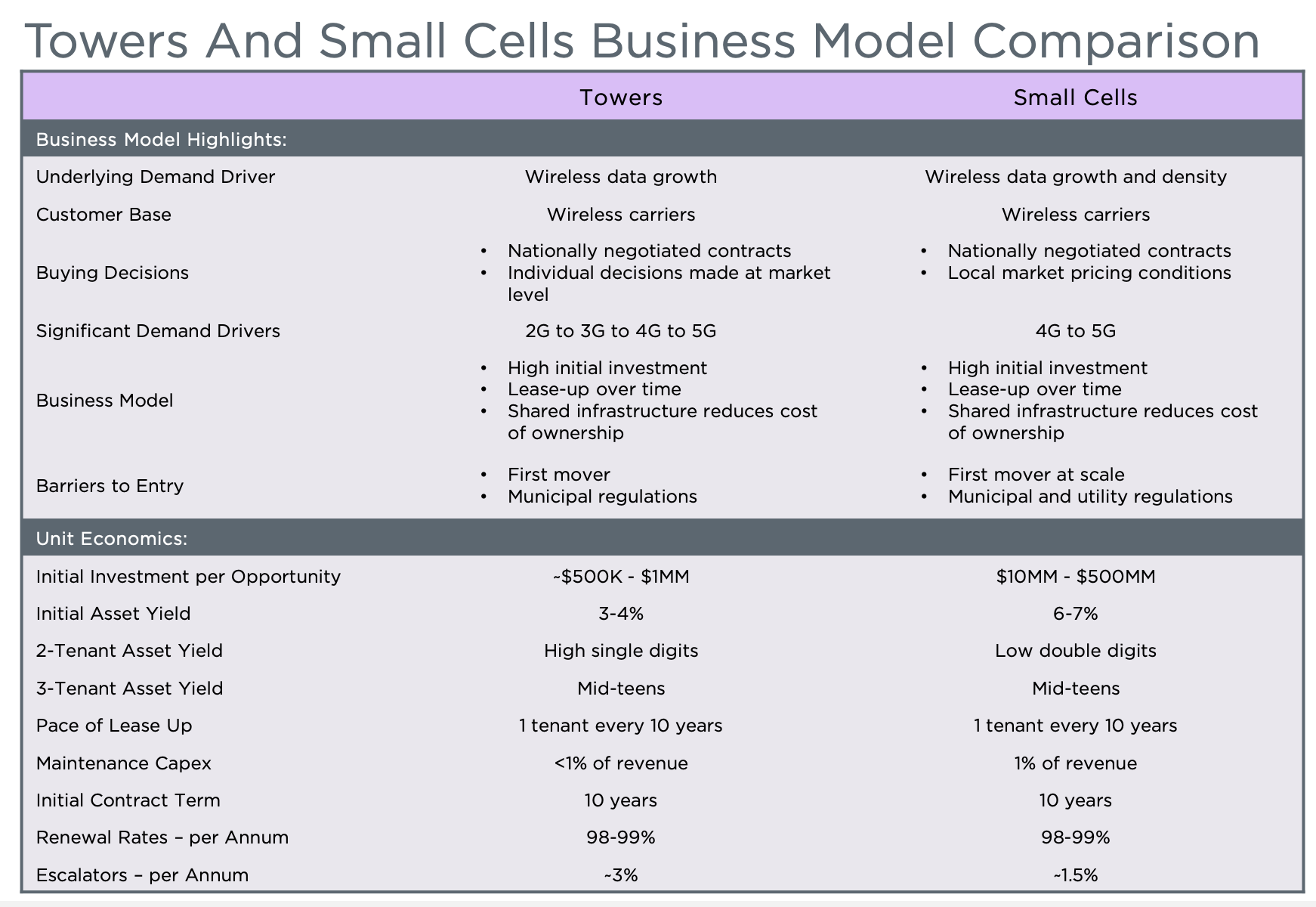

This business model can easily be leveraged, as one tower can host multiple tenants. Meaning, while costs are relatively high to host just one tenant per tower, adding new tenants comes with little additional costs.

Unlike its peer American Tower, Crown Castle's towers are located throughout the United States, with approximately 56% and 71% of them located in the 50 and 100 largest US basic trading areas, respectively. Crown Castle's largest tenants are T-Mobile ( TMUS ), AT&T ( T ), and Verizon Wireless ( VZ ), which collectively accounted for approximately three-fourths of the company's 2022 consolidated site rental revenues. While being dependent on just three customers is a red flag in almost every industry, we cannot make the case that CCI is in danger. After all, its customers are highly dependent on its network and unable to switch to a competitor without losing service quality. While CCI is highly dependent on the three telecom giants, the telecom giants are also dependent on CCI.

Crown Castle

The major benefit of CCI is that it is a perfect mix of offering a high yield and long-term growth.

The company currently pays a $1.565 dividend per share per quarter. This translates to a 5.0% yield. Over the past five years, the average annual dividend growth was 8.7%. The most recent hike was announced in October 2022, when CCI hiked its dividend by 6.5%. The FFO payout ratio is 78%, which is above the sector median.

On a long-term basis, management expects to maintain between 7% and 8% annual dividend growth, which is a huge deal given its 5.0% yield.

Dividend growth is expected to rely on several pillars.

- Embedded growth tied to contracted escalators .

Our wireless tenant contracts have initial terms of five to 15 years with contractual escalators and multiple renewal periods of five to 10 years each, exercisable at the option of the tenant.

- Data growth and required network investments.

Between 2010 and 2020, cell towers went from 150K sites to 417K sites. Mobile data usage grew by 108x from 0.4 to 42.2 trillion MBs. Especially in light of 5G and the Internet of Things (full connectivity), we can expect demand growth to remain robust.

Looking at the bigger picture beyond this year and why I am so excited about our growth opportunity, we are still in the early innings with 5G as the industry is only a couple of years into what we expect will be a decade-long growth opportunity. Our customers are seeing significantly higher levels of monthly data consumption as consumers upgrade to 5G, providing the need for significant network investment for years to come to keep pace with this persistent growth in mobile data demand.

- The company's ability to capture network densification with its portfolio of towers, small cells, and fiber.

- Its track record proves that the company is indeed capable of excelling in its area of expertise.

Please note that the lower part of the overview below highlights the company's ability to leverage existing infrastructure, which I briefly highlighted earlier in this article.

{kind=link}

With regard to its balance sheet, the company has made tremendous progress. Crown Castle finished 2022 with leverage in line with its target of approximately 5x net debt to adjusted EBITDA, and its discretionary CapEx outlook for the full year 2023 is unchanged with gross CapEx of $1.4 billion to $1.5 billion. The company expects to be able to finance its discretionary capital with debt while maintaining its investment-grade credit profile, based on its current backlog of small cells that includes a significant mix of co-location nodes.

In January, Crown Castle issued $1 billion in senior unsecured notes with a 5% coupon to term out borrowings under its revolving credit facility, increasing its available liquidity to approximately $5.5 billion. As a result of this transaction, the company now has more than 85% fixed-rate debt, a weighted average maturity of over eight years, and limited maturities through 2024.

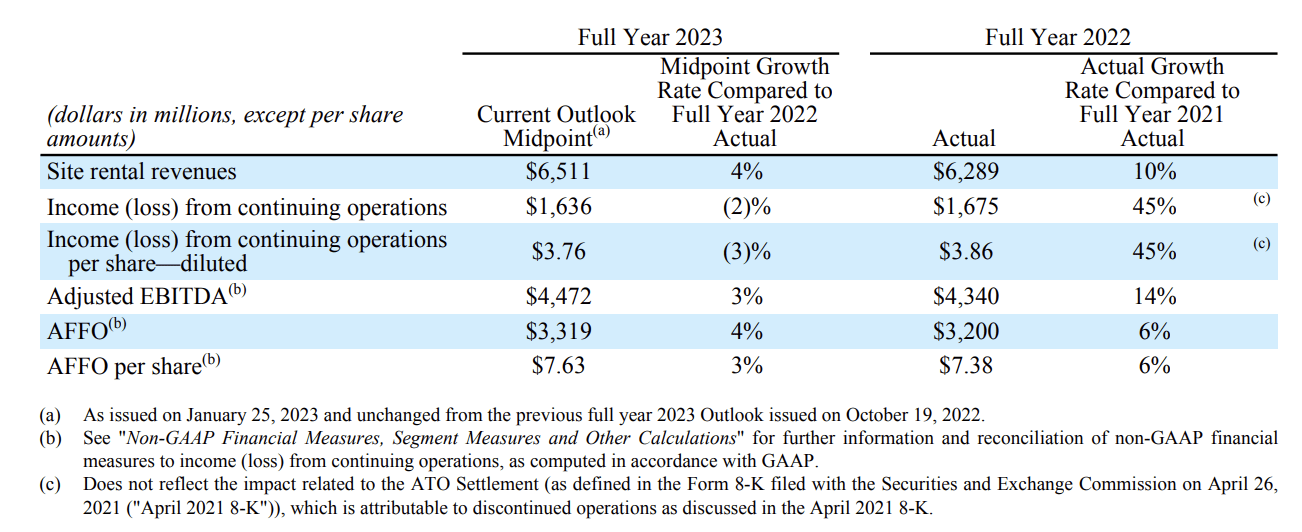

With that said, on a full-year basis, the company expects to grow adjusted FFO by 4% to at least $3.3 billion. AFFO per share is expected to rise by 3% to $7.63, which is the midpoint of its current guidance range.

{kind=link}

This implies a valuation of 16.3x, which I believe is fair.

Over the past ten years, CCI has outperformed its sector peers. I expect that to continue.

With that said, here's my takeaway.

Takeaway

In this article, we started by discussing the pros and cons of investing in REITs. In light of my fears to buy underperforming REITs with little to no growth, I presented two REITs I recently put in model portfolios and on my watchlist. Invitation Homes is a giant in the residential real estate space, with growth opportunities due to restricted supply and its healthy balance sheet. Crown Castle is a cell tower REIT with a massive footprint and growth opportunities in 5G and related secular trends. CCI is the perfect mix between a high yield and high (expected) long-term dividend growth.

While the market is currently tricky, I believe that both stocks will outperform their peers on a long-term basis.

Needless to say, based on current market challenges, I will maintain a neutral rating for the time being. If we encounter more stock market weakness, I'm tempted to add at least one of these stocks to my dividend growth portfolio.

For further details see:

The Perfect Blend Of Growth And Income: Invitation Homes And Crown Castle