VCLT - The Portfolio Playbook For A Policy Pivot

2024-01-11 07:00:00 ET

Summary

- The article discusses the current state of the economy and the potential for a recession due to the lagged effects of tight monetary policy.

- The Sahm Rule, which predicts the start of a recession based on the unemployment rate, suggests a recession may begin in the second quarter of next year.

- The question then becomes, when does the easing cycle start? The answer is that inflation numbers - core PCE and core ex-services PCE - will be the guide.

- If you are fearful of higher rates creating a mark-to-market loss in your portfolio, then I would devise a plan that allocates to the area on a systemic basis.

- Start taking advantage of longer duration opportunities in bonds now, as rate cuts are expected to begin in the second quarter.

(Since this article was originally written, rates have fallen and many of these ideas have "worked." That said, we think they can work much more.)

We have all become macro experts - not out of want, but out of necessity. The world is being driven by central banks and interest rates.

Last month was a bit of a game changer and we're starting to see a paradigm shift. In other words, I think we've entered a new stage in the cycle.

There is no doubt that we have slowed since the third quarter and the labor market is finally showing signs of materially slowing. We have been waiting for this for more than six months now.

But as I wrote in the November monthly letter, while it seems like we've been tightening for some time, we really have only had "tight monetary policy" for the last few months.

The lag time before that tight policy and the effects on the economy could be as much as 18 months, according to Apollo's Torsten Slok .

In other words, the transmission mechanism of monetary policy takes time, and the drag on growth from lagged Fed hikes over the coming year will be significant. That is why a recession is a more likely outcome than a soft landing, no matter what happens to inflation.

As such, Fed Chair Jay Powell noted in his remarks last month that they were likely to "proceed carefully" along with being in "wait and see" mode as the effects continue to penetrate the economy.

The repercussion is that the Fed is likely done with its hiking cycle, and on pause... for now.

The question then becomes, when does the easing cycle start?

The Inflation Story Is Over

Core PCE was +3.2% in November compared to a year earlier. While that may not seem like the inflation story is over and we have arrived at the Fed's 2.0% target, if you look deeper under the hood, you can see why it is.

Most of the reason for the 3.2% is the earlier comparison months from a year ago. Simply through the passage of time and the roll-off of those months (base effects), core PCE inflation (the primary measure for the Fed) should fall.

If you just look at the last six months and annualize it, Core PCE was just +1.9%, below the Fed's target.

If we use the Dallas Fed's trimmed mean inflation gauge, an alternative measure that is supposed to be more accurate, it came in at +1.5% for November, the lowest in three years.

Goldman Sachs recently published a note titled, "Could Inflation Fall Below Two Percent?":

With the November inflation reports and their accompanying revisions in hand, we now see below-2% core PCE inflation as a plausible outcome for 2024—based on a reasonable downside scenario for consumer goods and labor-reliant services prices.

For the Fed, we believe below-target core inflation would lead the Committee to consider consecutive 25bp cuts at every FOMC meeting until the funds rate approaches their estimate of neutral at that time, provided that the inflation decline does not appear temporary and that labor market rebalancing has not started to reverse.

But will we have a recession?

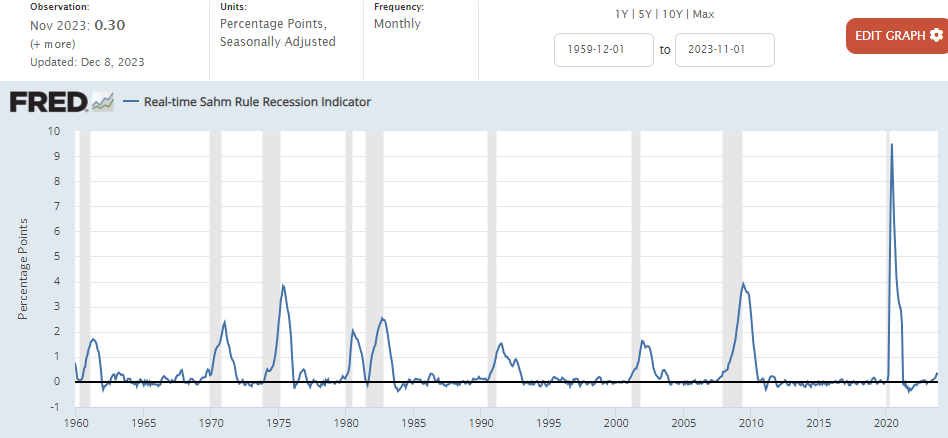

The Sahm Rule is getting a lot of play in the financial news media. This is something 99% of investors have probably never heard of. However, it is very easy to understand.

Sahm rules: the start of a recession is when the three-month moving average of the unemployment rate rises by a half-percentage point or more relative to its low during the previous 12 months.

Essentially, take the lowest reading of unemployment during the cycle and compare it to the 3-month moving average. If the three-month moving average is more than 0.5% above that low reading, then the rule is triggered.

It has accurately shown the start date of all recessions. While it has a high degree of accuracy, it is a heuristic, not a forecasting, tool. All it can tell us with any measure of reliability is that the NBER, the part of the government that records when recessions started and ended (typically with at least 6 months hindsight), is likely to note that a recession has begun.

We are currently at 0.30% above. The cool thing about it is its part of the FRED (Federal Reserve) charting database:

{kind=link}

In order for it to trigger, we would need to hit 4.3% in December (quite a move), or more likely an average of 4.1% for December and January. More likely, the rule will be triggered in the second quarter of next year, implying a recession sometime later in the second or third quarter of 2024.

The use of the Sahm rule is to better understand what the Fed will do, not what the markets will do.

All this to say that as of now, the Fed is likely to start cutting in March (there is no April meeting) or May - it really doesn't make a difference. The market is expecting five or six rate cuts of 25bps each next year. That's a lot of cutting.

So does that mean wait until then to buy bonds or extend the duration on your current portfolio?

ABSOLUTELY NOT .

When that day comes, rates will likely already have reacted and you will have missed some of the upside. Since the November CPI announcement, the 10-yr yield (US10Y) has fallen more than 110 bps from its high of just above 5.0%.

In order to capture the price appreciation of lower rates, we would want to continue to build in new positions, recycling some short-term positions (cash, MINT, CDs, etc.) into longer-term positions. I would be getting a bit more aggressive in adding longer-duration individual bonds today than I have been over the last six months.

Timing the top is still a fool's errand given that most of the return on a bond holding is from the yield. This is why we started earlier as rates were rising, taking short-term, unrealized losses. This is because we can never time the top and it takes time to build an individual bond portfolio. If you wait until rates start falling, you may miss the boat.

Currently, approximately 57% of my portfolio is individual bonds. These were accumulated over the course of the last year-plus. Some have unrealized losses as rates continued to move higher after my purchase. That's ok. My goal is to hold to maturity (some go out to 2050 when I'll likely not be alive. And that's ok).

Take Advantage of Longer Duration Opportunities Now

While each brokerage is different, many will do a fixed income analysis to assess your individual weighted average coupon, years to maturity, yield on cost, yield to maturity, and even modified duration.

There are few ways to do this. The easiest way would be to add higher-duration funds - ETFs or mutual funds. You can then slowly liquidate that/those positions as you add longer-term individual bonds.

A few options:

- Vanguard Extended Duration ( EDV )

- PIMCO Extended Duration ( PEDIX )( PEDPX )

- Vanguard Long-Term Bond ( BLV )

- Vanguard Long-Term Corp ( VCLT )

- iShares 10+ Year Corp Bond ETF ( IGLB )

- SPDR Portfolio LT Corp ( SPLB )

- Fidelity Investment Grade Bond ( FIGB )

- iShares iBoxx IG Corp Bond

- Fidelity Corp Bond ( FCOR )

- iShares iBonds Dec 2032 Term Corp ( IBTM ).

I prefer to use FIGB, IGLB, and SPLB along with the Bulletshares 2033 Corp Bond ETF ( BSCX ) .

If you are fearful of higher rates creating a mark-to-market loss in your portfolio then I would devise a plan that allocates to the area on a systemic basis - perhaps a bit each Friday or every other week or even monthly.

That helps to take the emotion out of it and make it more formulaic.

I recommended one such duration fund recently and received a comment from a member who stated that the 3-year trailing return was -4.5%. I said yes, but I only care about future returns, not backward-looking returns. I didn't own the fund for the last three years.

Investors need to look forward, not backward. Future returns for most core bond funds will be in the middle single digits (at least!) for the next 5 years or more. That is an attractive return profile and something we haven't been able to say for more than 16 years.

Higher duration is unlikely to result in the same pain that was experienced over the last two years. Whereas the S&P 500 (SP500) is back to its all-time highs, the bond market still has a way to go. So if you feel like you've missed out, you shouldn't.

YCharts

Concluding Thoughts

Hiding out in cash and other very high-quality short-term bonds and paper (like money markets) may seem safe but it comes with hidden risks. The largest of which is reinvestment risk.

If you can lock in a yield of 5-7% for the next ten years (or more), you will have insulated a lot of principal from ever needing to be withdrawn during retirement to support your lifestyle.

Locking in these yields for at least 5 years (we would prefer 10-20 years) can make a world of difference in retirement planning and outcomes. I have run Monte Carlo analysis that shows improvement in the longevity of retirement by as much as 10-15 years by locking in these yields for a decade or more. The ability to extend retirement by 10 years (in other words do not draw down assets for an extra decade) will be a powerful tool.

Even if you're not in or near retirement, the compounding of ~6% consistent income over a decade or two as a base (foundation) for your portfolio will be hugely beneficial.

For further details see:

The Portfolio Playbook For A Policy Pivot