PMT - The Preferred Share Dilemma Chimera Created For Themselves

2023-09-22 17:29:38 ET

Summary

- Chimera Investment Corporation is considering whether to keep CIM-B as a fixed-rate dividend or allow it to float as originally intended.

- The company previously stated that the LIBOR rate payable on their preferred shares was already replaced with SOFR by operation of law.

- The company's financial statements stated unequivocally that series B, C, and D would float. These statements were filed with the SEC a month after SOFR replaced LIBOR.

- Shareholders who are concerned that the company may attempt to classify CIM-B as a fixed-rate share, despite their prior statements, may want to consider reaching out to the company.

Chimera Investment Corporation ( CIM ) is debating whether they should try to pull a fast one on some of their preferred shareholders.

They have four series of preferred shares:

Here's what happens with each share:

- CIM-A: Fixed-rate. Nothing new.

- CIM-B: Should use SOFR. Read this article.

- CIM-C: Uses SOFR.

- CIM-D: Uses SOFR.

I need to lay the framework for this article by starting a few weeks ago. I prepared an article discussing each share in our coverage universe where the floating rate was at risk. This was all based on my assessment of the terms in the prospectus for every preferred share we cover. It was a reaction to PennyMac Mortgage Trust ( PMT ) announcing that they believed fixed-to-floating can also mean fixed-to-not-floating.

In my article on August 30th, 2023, I wrote:

CIM-B should be able to land in the “all clear” pile, but they fell a tiny bit short. If we take “the spirit” of what they said, it would clearly be that they are going to use SOFR. However, the spirit of the contracts and the spirit of the law clearly hasn’t been enough. Consequently, I can’t give this an “all clear”. I e-mailed CIM on Monday morning (8/28/2023) and they haven’t replied yet (as of 8/30/2023 around noon Eastern).

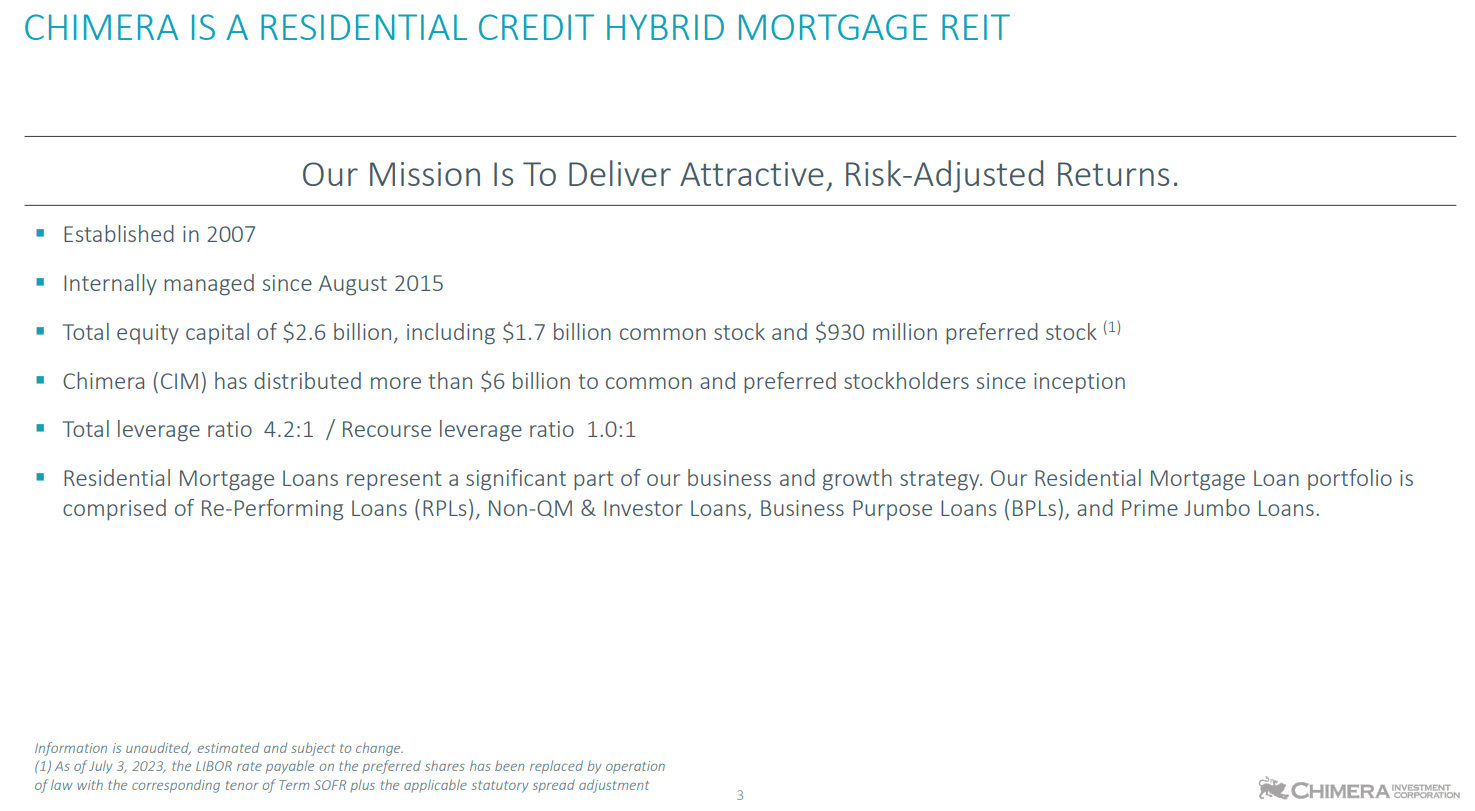

The first source is the CIM Q2 2023 Earnings Presentation :

CIM, underlining and notes by The REIT Forum

That’s pretty good. It’s almost complete. It should reference each series individually, but it’s close. This is about 90%.

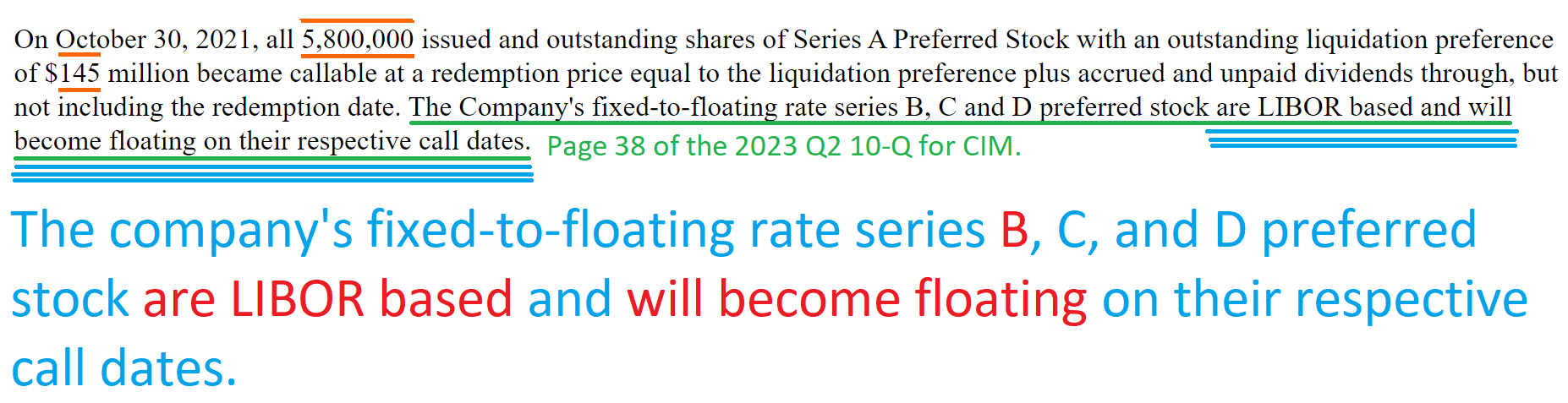

Using CIM’s Q2 2023 10-Q , we have further support:

CIM, underlining and additional notes by The REIT Forum

I think that brings it up to about 95%. Publishing that and then declaring that “will become floating” actually means “CIM-B will be fixed rate” would be indefensible.

As you may have noticed from the quote, I e-mailed CIM. I eventually heard back from them, and I will include their reply in this article. However, I think these facts are easiest to process if we use a clear timeline. The reply from CIM comes at the end of the timeline.

Disclosure: To be clear, I am not a lawyer, judge, nor any other person who has studied law in a formal setting. I evaluate investments, not legal claims. This article only presents my opinion on the matter. Investors are encouraged to independently verify each matter that is important to them.

The Timeline

December 16th, 2022: The Federal Reserve indicates the final rule.

The final rule implementing the LIBOR Act is released.

March 23, 2022: The President signed the Adjustable Interest Rate (LIBOR) Act into law.

December 16, 2022: The Federal Reserve Board adopts the final rule .

June 30, 2023: US Dollar LIBOR ends . A synthetic version will exist until September 30, 2024.

August 3, 2023: CIM's Q2 2023 earnings presentation comes out.

{kind=link}

When we zoom in on the bottom left corner, it says:

CIM, underlining and coloring by author

{kind=link}

That statement appears pretty clear to me. CIM stated unequivocally that the shares had already transitioned to LIBOR.

Does that refer to CIM-B? Or was it only CIM-C and CIM-D?

Notice the number 1 in front of that line? That tells us which part of the slide goes with that footnote.

Specifically, we're talking about these words:

“Total equity capital of $2.6 billion, including $1.7 billion common stock and $930 million preferred stock (1).

Just to be sure that we're not making any dumb mistakes, we're going to verify that $930 million is a total that must include CIM-B. Upon checking the 10-Q, we find that the total liquidation value for each series is as follows:

-

Series A: $145 million.

-

Series B: $325 million.

-

Series C: $260 million.

-

Series D: $200 million.

I'll save you some time. According to my spreadsheet, those numbers total $930 million. Therefore, every series of preferred stock is included.

Consequently, we have confirmed that every preferred share was included in that footnote. Further, I am very confident that July 3, 2023, came about 1 month before August 3, 2023. Please correct me if I am wrong about that.

Because July 3, 2023 is the older date, that is not a forward-looking statement. We can even confirm that by the language "has been replaced." Therefore, everyone should agree that this statement was a matter of historical fact.

What does that mean for each share? If we make the leap of assuming words still have the same meaning in the English language, then we would believe:

- CIM-A: No impact because there is no LIBOR rate.

- CIM-B: LIBOR was replaced by SOFR by operation of law.

- CIM-C: LIBOR was replaced by SOFR by operation of law.

- CIM-D: LIBOR was replaced by SOFR by operation of law.

I am going to great lengths to emphasize that this is not a future event. Per the words on the slide, this event happened a month before the slide was released.

CIM explicitly told investors that SOFR had replaced LIBOR on their preferred shares.

However, we should verify that these fixed-to-floating shares that use LIBOR actually have a LIBOR rate. Besides the prospectus (which is old), we can use the 10-Q.

August 3, 2023 (again): CIM filed the 10-Q for Q2 2023.

We're getting the relevant part from page 38 (which was shown in the second screenshot):

CIM's 10-Q, underlining and commentary by author

{kind=link}

Again, I feel compelled to remind investors that this document was filed in August. August 3rd is:

- Over 7 months after the Federal Reserve announced the final rule.

- 1 month after the date CIM states SOFR replaced the LIBOR rate.

Before filing these documents, management knew about the LIBOR Act.

Why did management choose to publish those statements?

I have three theories:

- They believed CIM-B would float. Therefore, it would float based on SOFR. If this is the case, they intended to include it in the presentation and footnote stating LIBOR was replaced by SOFR plus the spread adjustment. Great, all they need to do is follow through on what they said they already did.

- They believed CIM-B would not float. That would be really bad. In that scenario, they would have published a statement they believed to be false. That is not something anyone should do, especially in a financial statement. However, the presentation would still apply because it referenced all of the preferred shares and indicated LIBOR was replaced by SOFR plus the spread adjustment. They should follow through on what they said they already did.

- The company meant to publish something different than what they actually published. Maybe the court would just overlook the very clear statements and pretend it said something other than what it obviously said?

Option 3 sounds really dumb, but it wouldn't be the first time a company showed up to court with that argument.

September 14, 2023: CIM replied to us (and several other investors) by saying:

Dear Investor,

After June 30, 2023, all LIBOR tenors relevant to the Company ceased to be published or became no longer representative. Under the federal Adjustable Interest Rate (LIBOR) Act (the "Act") and the related regulations promulgated thereunder, three-month CME Term SOFR will automatically replace three-month LIBOR as the reference rate for calculations of the dividend rate payable on each of the Company’s 7.75% Series C Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock (the “Series C Preferred Stock”) and 8% Series D Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock (the “Series D Preferred Stock”) for dividend periods from and after September 30, 2025, in the case of the Series C Preferred Stock, or March 30, 2024, in the case of the Series D Preferred Stock. The replacement rate, and therefore the calculation of the dividend rate payable, for the Series C Preferred Stock and the Series D Preferred Stock will also include the applicable tenor spread adjustment of 0.26161% per annum, as specified in the Act. With respect to the Company’s 8% Series B Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock (the “Series B Preferred Stock”), the Company is currently evaluating the impact of the cessation of LIBOR and the application of the Act and the applicable dividend rate payable on the Series B Preferred Stock after March 30, 2024.

Thank you for your interest in Chimera,

In my opinion, that means CIM hasn't made a decision yet. They still want more time for lawyers to look at it or to see what happens with other fixed-to-floating-but-not-really preferred shares.

Updated Projections

I lowered price targets based on the negative development. However, I still own some shares purchased before the e-mail and I picked up a few more since then. I still think they are a bargain, as I think CIM should be honoring their statements.

While PMT is trying to get out of the actual terms laid out in their contract (my opinion), CIM would need to escape the contract and escape their public commentary to investors.

What Can You Do?

Investors should let CIM know how they feel. There are two routes they can use here. Posting them will most likely result in CIM never replying to my e-mails again, but such is life. I believe drawing attention to this is beneficial for shareholders and for CIM, because it can help protect CIM from making a mistake.

- You can go to the contact page to contact investor relations .

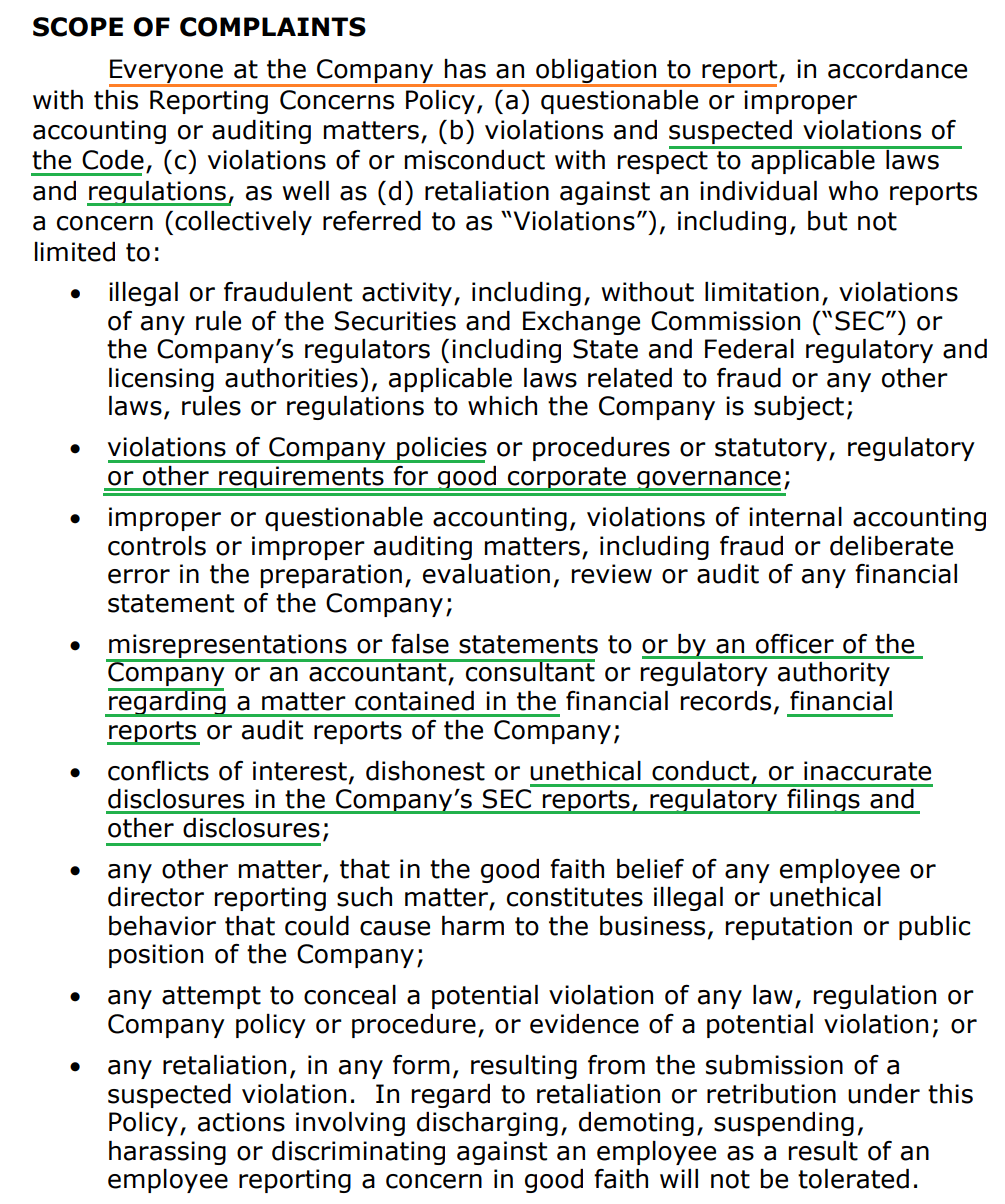

- You can go to the governance page to report a concern .

Of course, you should only report a concern if you reasonably believe there is a concern . To understand "concerns," you can use the button: "View Reporting Concerns Policy."

The first sentence states:

Chimera Investment Corporation (the “Company”) is committed to fair, accurate and transparent accounting of its financial matters and expects all employees of the Company and its subsidiaries to act in accordance with the highest ethical standards in the performance of their duties and obligations.

You'll have to evaluate whether you reasonably believe this matter could lead to a potential violation of those standards .

- Is it fair, accurate, and transparent accounting of its financial matters?

- Is it acting in accordance with the highest ethical standards ?

My opinion on that isn't relevant. It is your reasonable belief that is important.

People who can make complaints include multiple groups. One group is known as "shareholders".

For a bit more detail, I found the part on the scope of complaints and underlined some parts:

{kind=link}

Shareholders don't work at the company, so they don't have the obligation. However, these are examples of items that fall within the scope of matters to report.

What you do with this information is entirely up to you. I'm simply sharing my understanding of the current situation.

Conclusion

If CIM announces they intend to keep CIM-B at a fixed-rate dividend, I believe it would lead to a bear scenario. However, CIM-B is presently at $19.79. That is only $.28 above CIM-A. If CIM-B at a fixed-rate dividend, it would be fixed at $.50 per share per quarter, which is the same as CIM-A. Therefore, CIM-B should be valued at no less than CIM-A.

If CIM affirms that CIM-B will float in accordance with their prior comments, I believe it would lead to a bull scenario. CIM-D trades at $20.86, which is nearly $1.00 higher.

Investors who want to avoid the risk with CIM-B can use CIM-D instead. It has a lower floating spread and a higher share price, which I attribute to the uncertainty around CIM-B.

The Floating Rate Period for CIM-B and CIM-D is scheduled to begin March 30, 2024. Absent a significant economic downturn or a decrease in rates, I would expect shares to benefit as they approach the floating date. For CIM-B, this depends on an announcement that shares will actually float, as the company previously stated.

Regarding PMT's decision, I'll have further information coming on that as well. However, that article is not ready yet.

I hope you enjoyed the article and have a great weekend. Let me know what you think in the comments.

For further details see:

The Preferred Share Dilemma Chimera Created For Themselves