RBGLY - The Procter & Gamble: Do Not Chase This SWAN Over The Cliff

2023-09-21 14:00:00 ET

Summary

- With its offerings being important staples in most households globally, it is unsurprising PG has been able to command robust pricing power, with pricing being a top-line contributor since 2011.

- Perhaps this is why the management has offered an excellent FY2024 guidance, well exceeding its pre-pandemic and hyper-pandemic averages.

- PG's profitable growth is expected to continue at CAGRs of +4% and +8.1% through FY2026, as FCF generation remains robust, sustaining its 66 years of consecutive dividend growth.

- However, the strategy has had the unintended effect of lower overall volumes by -3% YoY as prices rose by +9% YoY, as the elevated interest rates tighten discretionary spending.

- Combined with its premium valuations and the stock's current resistance retest, we do not recommend anyone to chase this Sleep-Well-At-Night stock at this peak.

The PG Investment Thesis Remains Excellent, Thanks To Its Robust Pricing Power

The Procter & Gamble Company ( PG ) is a Household Product conglomerate indeed, with $361.71B in Market Capitalization at the time of writing.

Its product offerings require no introduction as well, with my own children using Pampers at some point in their lives, Oral-B/ Gillette/ Head & Shoulders gracing our bathrooms, and Pringles hidden in our pantries.

With its offerings being important staples in most households globally, it is unsurprising that PG has been able to command a robust pricing power, with the management similarly iterating that " pricing has been a positive contributor to its top line growth for something like 48 out of 51 of the last quarters."

Combined with the company's leading global market shares in multiple categories, we believe PG is a bellwether stock that may continue performing well no matter the macroeconomic outlook.

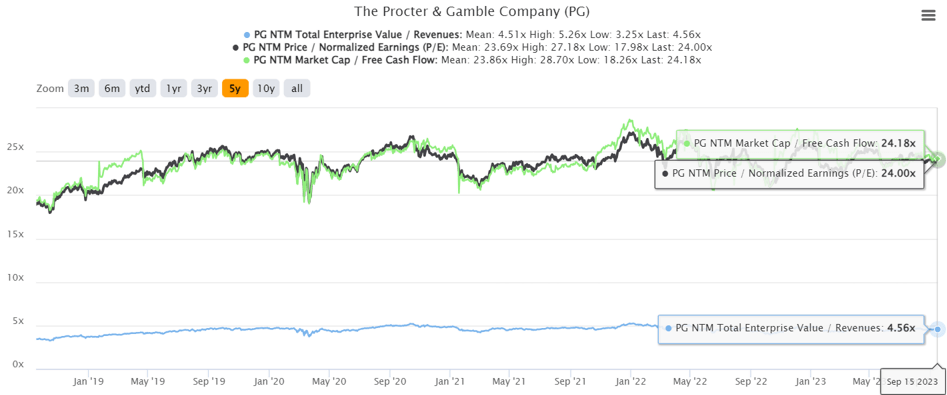

PG 5Y EV/Revenue, P/E, and Market Cap/ FCF Valuations

{kind=link}

Therefore, it is unsurprising that the PG stock trades at NTM EV/ Revenues of 4.56x, NTM P/E of 24x, and NTM Market Cap/ FCF of 24.18x, somewhat inline compared to its 1Y mean of 4.52x/ 23.93x/ 24.68x and expanded compared to its 3Y pre-pandemic mean of 3.80x/ 21.35x/ 21.25x, respectively.

Perhaps this is attributed to the management's guidance of FY2024 organic sales growth at +4.5% YoY and diluted net EPS growth at +7.5% YoY at the midpoint.

These numbers have painted an optimistic picture of PG's top and bottom line growth indeed, due to the comparison to its 3Y pre-pandemic CAGRs of +2.9%/ +9.3% and hyper-pandemic CAGRs of +4.9%/ +4.8%, respectively.

As a result of its profitable growth prospects, we can understand why Mr. Market has rewarded the stock with the premium valuations, since the consensus has also estimated the sustained expansion in its top and bottom line through FY2026 at CAGRs of +4% and +8.1%, respectively.

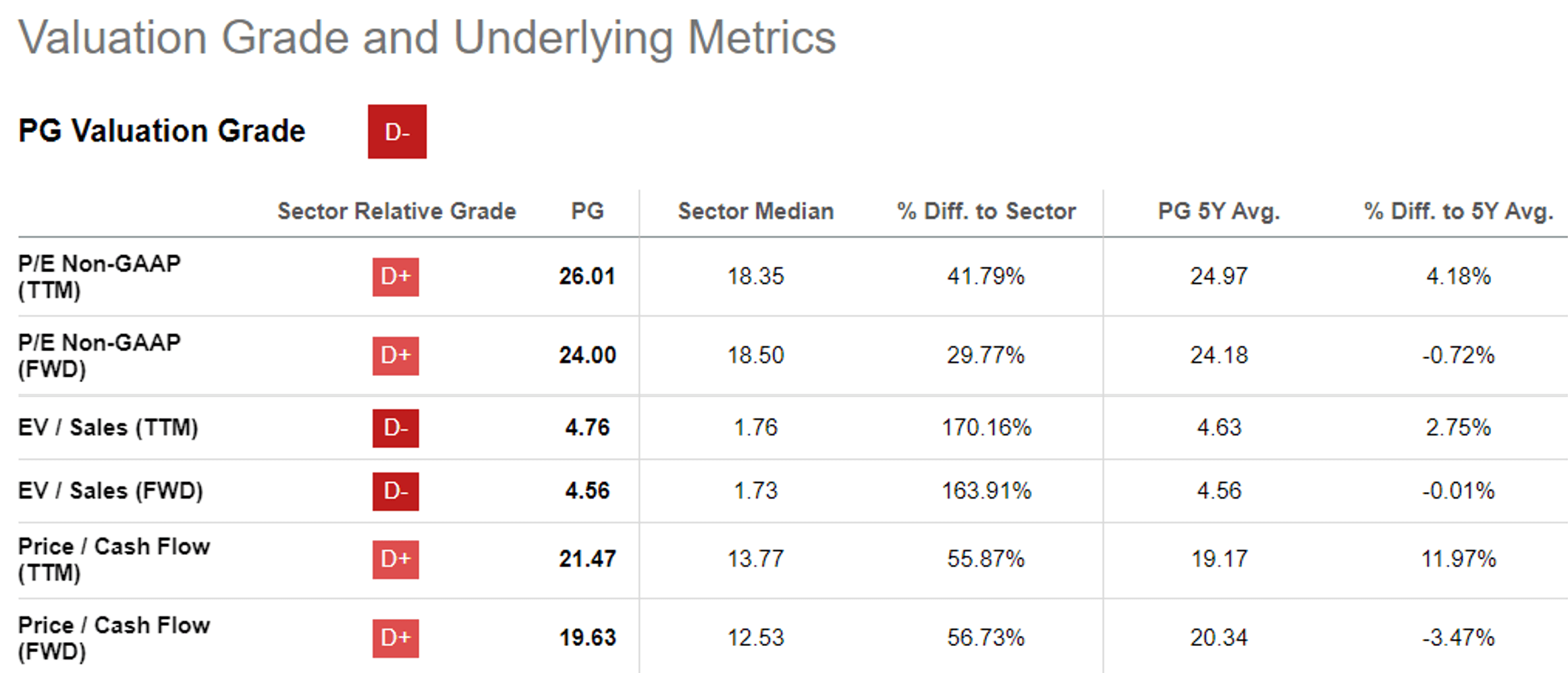

PG Stock Valuation Compared To Household Product Peers

{kind=link}

This also explains PG's seemingly expensive valuation grades, compared to the Household Products sector median FWD EV/ Sales of 1.73x, Adj P/E of 18.50x, and Price/ Cash Flow of 12.53x.

The same has been observed with its direct peers, including Colgate-Palmolive Company ( CL ) at an NTM adj P/E of 22x with a bottom line CAGR of +4.1% through CY2025, Kimberly-Clark Corporation ( KMB ) at 18.52x/ +4.8%, and Reckitt Benckiser (RBGPF) (RBGLY) at 17.60x/ +4.3%, respectively.

While PG may be trading near its all time peak valuations, the stock continues to offer a decent forward dividend yield of 2.45% as well, compared to its 4Y average of 2.41%, though slightly lagging behind the sector median of 2.67%.

Based on the consensus FY2026 adj EPS of $7.45 and its NTM P/E valuations of 24x, we are also looking at a long-term price target of $178.80, implying a decent upside potential of +16.5% from current levels.

As a testament to its dividend aristocrat status, the PG stock also offers 66 years of dividend growth and a 5Y Growth Rate of +5.68%, thanks to the robust Free Cash Flow generation of $14.01B in FY2023 ( +1.5% YoY ).

The management has also offered a promising shareholder return guidance of up to $15B in FY2024 (-8.2% YoY), comprising ~$9B in dividends (inline YoY) and ~$6B in share repurchases (-18.3% YoY), with the latter likely to further reduce its share count, with ~140M shares already retired over the past three years.

The PG Stock Is A Hold For Now, Thanks To The Growing Risk Of Volume Declines

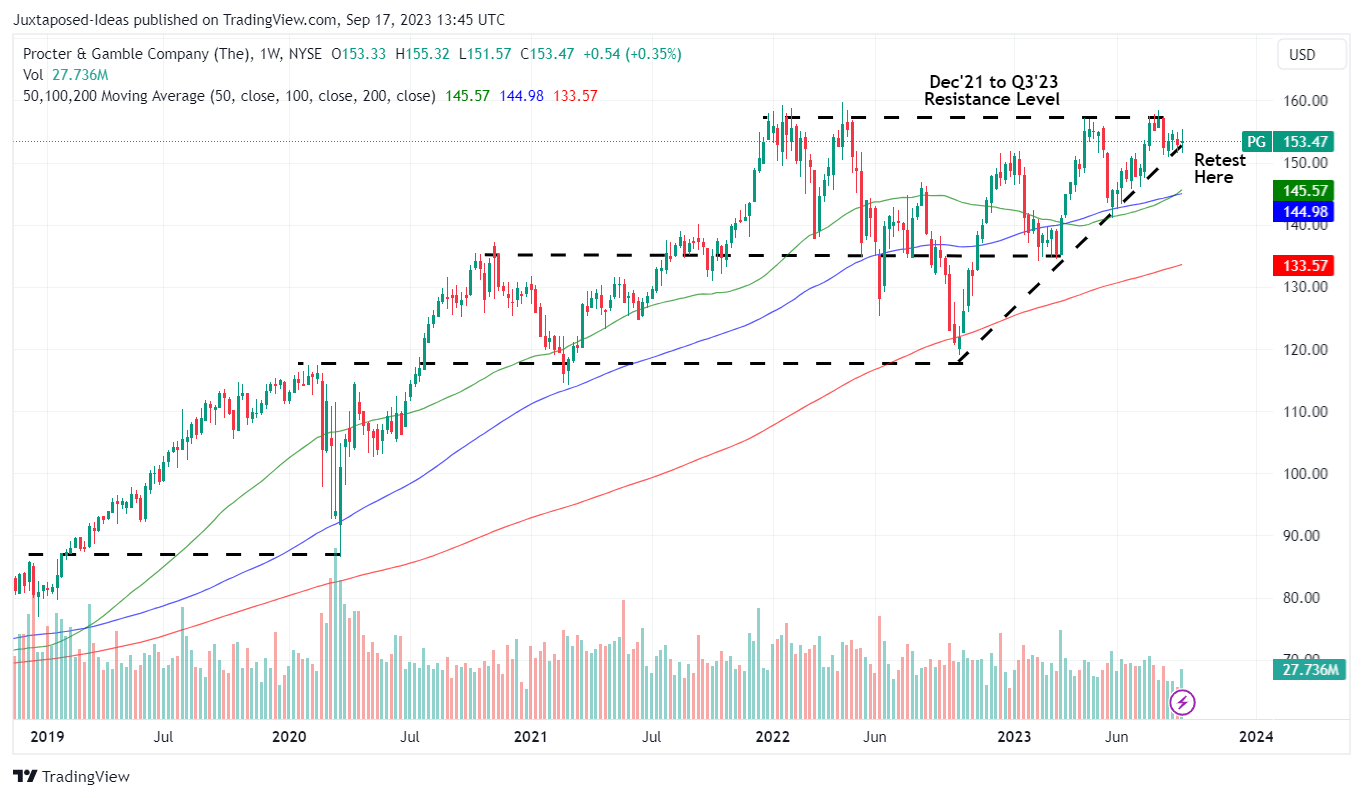

PG 5Y Stock Price

{kind=link}

As a result of its dual pronged returns through stock price appreciation (as observed in the chart above) and decent dividend income, we believe the PG stock is a long-term hold for discerning investors indeed.

However, with the stock currently trading at its peak, with higher tops and higher bottoms since October 2022, its forward trajectory appears to be uncertain in the near term, with it remaining to be seen if an eventual break out may occur.

Thanks to the ongoing inflation, the PG management has also opted to preserve gross margins at 49.1% (+0.9 points QoQ/ +3.5 YoY), near to its pre-pandemic averages of ~49.5%, resulting in higher overall prices by +7% on a QoQ basis in FQ4'23.

However, this also has the unintended effect of lower overall volumes by -1% QoQ, as the elevated interest rates tighten discretionary spending.

Investors must also note that the decline in its overall volume in the latest quarter is built up from the -3% QoQ reported in FQ3'23 and -6% QoQ in FQ2'23, with FY2023 already recording a decline in overall volumes by -3% YoY as overall prices rose by +9% YoY.

Particularly, PG's Fabric & Home Care segment's volume has been impacted by -2% QoQ/ -2% YoY for the latest quarter, with FY2023 recording a lower overall volume by -4% YoY.

This is an important metric indeed, since the segment comprises 34.5% (+0.2 points YoY) of its top line and 32.7% (+3.1 points YoY) of the bottom lines in FY2023.

Therefore, while the US job market remains robust in August 2023, allowing PG to maintain its elevated pricing, it remains to be seen when the Fed may pivot, eventually contributing to the growth in its sales volume.

As a result of its mixed near-term prospects and its premium valuations, we do not recommend anyone to chase this Sleep-Well-At-Night stock at this peak. New investors may want to wait for a moderate retracement before initiating their positions for a lower dollar cost average.

On the other hand, existing investors may want to continue their existing DRIP programs, allowing them to regularly accumulate additional shares on a quarterly basis.

We will be waiting for a potential entry point near the PG stock's intermediate support levels of $135s as well, adding it to our portfolio of income and growth stocks. We'll see how it goes.

For further details see:

The Procter & Gamble: Do Not Chase This SWAN Over The Cliff