RPT - The Profound Misunderstanding Of The Landlord-Tenant Relationship

Summary

- Tenants are the primary source of revenue for REITs so they are important.

- But at the same time tenants are quite fungible.

- A better understanding of the tenant-landlord relationship provides insight into the battleground REITs.

Lately, quite a few REITs have entered the territory of what is known as “battleground stocks.” The kind of stock where everyone has an opinion, and those opinions appear to be heavily polarized. Some people love the stock, others hate it and there are few people in the middle.

At the moment, 3 of the most prominent battleground REITs are

- Medical Properties Trust (MPW)

- Welltower (WELL)

- Innovative Industrial Properties (IIPR)

I have already written about each of these individually (links MPW, WELL, and IIPR ), but what I’m realizing is that each of these has become a battleground stock for the same reason: A profound misunderstanding of the landlord to tenant relationship.

The market has been treating REITs as if they are tied at the hip to their tenants – rewarding REITs with reliable tenants and heavily punishing any REIT that has a tenant even hinting at going bankrupt.

In the following sections I want to clearly define the landlord-tenant relationship by exploring the terms on which they interact and then quantifying its value. I intend to shatter this false idea of landlord-tenant equivalency that has pervaded the market.

How landlords interact with tenants

REITs, for the most part, do not have material financial interest directly in their tenants. The REIT places the majority of its net worth in property, the land and buildings which are then inhabited by the tenants.

If something bad happens to the property, that is what destroys the value of a REIT.

- Location becomes worse

- Oversupply of competing real estate

- Property type is losing demand

- Flood, fire or other disaster that somehow is not covered by insurance

Yet in each of the battleground stocks listed above, the property has not been affected by such events. In each case, the market has dramatically oversold or overbought the stocks based on what has happened to the tenants.

So what really is the relationship between a landlord and its tenant?

Essentially, it is a contract in which the tenant gets to use the specified property or properties for a specified duration in exchange for a pre-negotiated stream of rent payments. Thus, the value of the tenant to the landlord rests in the value of this contract.

If a tenant of a biotech REIT cures cancer that is fantastic, but it provides almost no value to the REIT. Likewise, if a tenant’s earnings get cut in half that also has minimal impact on the REIT.

Tenant and REIT are separate entities and are only related by the terms of the contract.

The Value of a tenant to a REIT

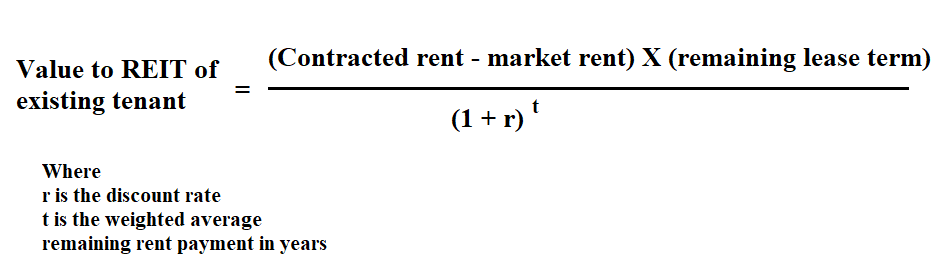

Contracts come with hard numbers and thus can be valued. In fact, the value of an in-place contract to a REIT can be mathematically defined.

{kind=link}

This might look like a lot of math, but it is just high school algebra so bear with me and please consider taking the time to truly understand this equation as it is the key to understanding these battleground stocks.

Let’s walk through it in English. The first term in the numerator is the contractual rent minus the market rent of similar properties. In REITs this is known as mark-to-market.

If the tenant is paying $20 per square foot but similar space normally rents for $18 per square foot, then the existing contract has positive value. That difference is then multiplied by the remaining term in the lease, let’s say 5 years.

Then to get the present value of the contract one would discount that numerator back to present using standard time value of money which is what the denominator is doing.

There are of course other things one could factor in to get a more precise value of a contract, but this is the quick estimation of what it is worth.

For most REIT sectors, market rents have moved up materially in the last few years due to inflation and other factors. This means market rents are generally higher than contracted rents of existing tenants. As such, many contracts have negative value. The landlord has to wait for the existing contract to expire before they can raise rents to the now higher market rate.

There seems to be quite a disconnect between the way the market views tenant bankruptcy and the way the REITs view it. Bed Bath & Beyond ( BBBY ) is a prevalent REIT tenant and as they continually announced news about their financial difficulties I watched as the retail REIT sector fell in tandem with BBBY.

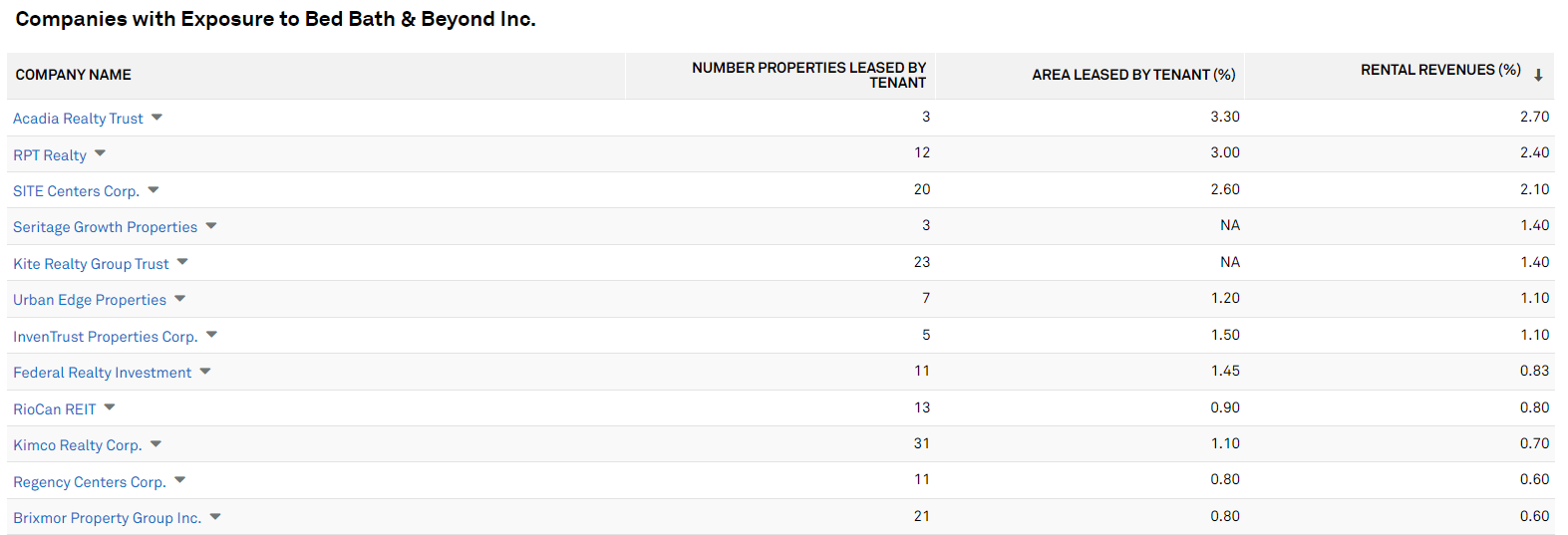

Below is the REIT exposure to BBBY as a tenant.

{kind=link}

I think the market is looking at a table like this and thinking that if and when BBBY goes bankrupt, Acadia ( AKR ) will lose 2.7% of its revenue, RPT Realty ( RPT ) will lose 2.4% of its revenue and SITE Centers ( SITC ) will lose 2.1% of its revenue.

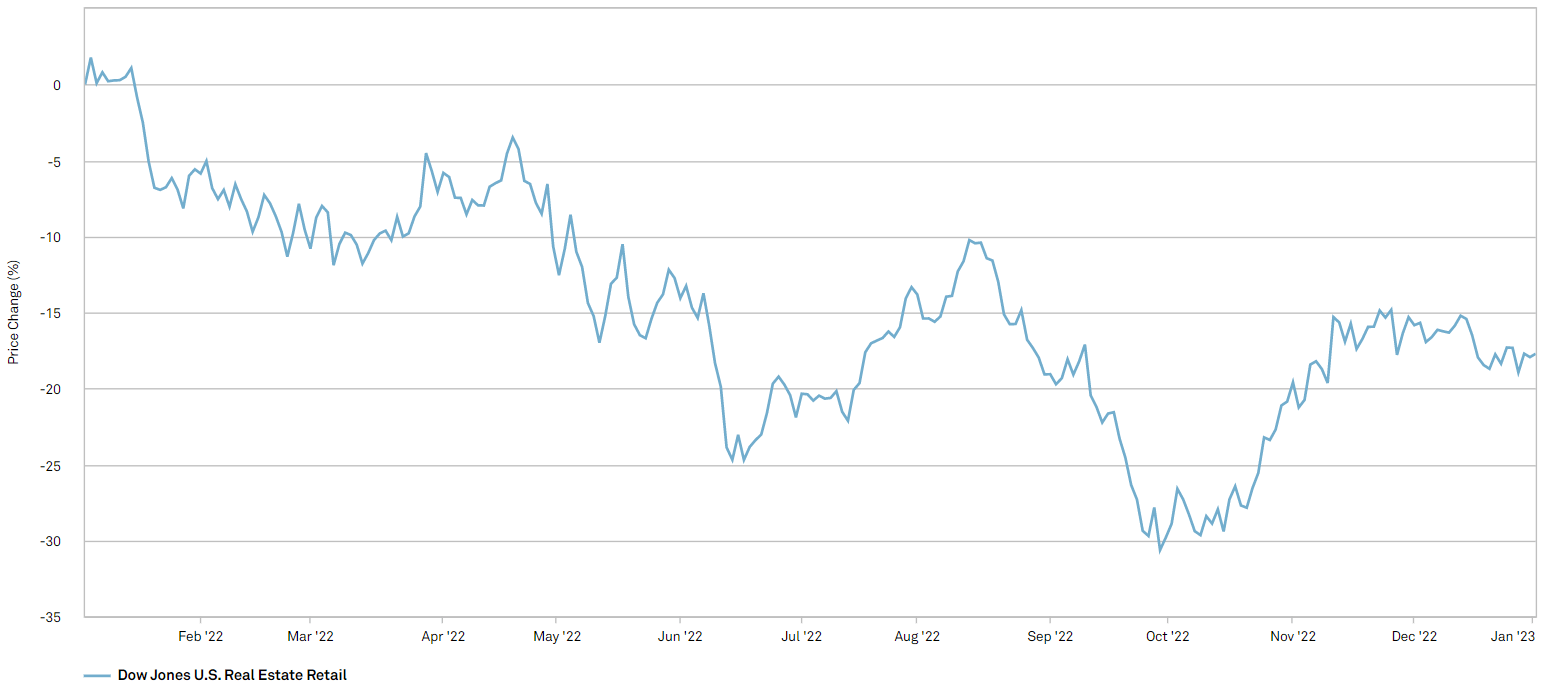

There are other similar retail operators that are struggling and I think the market is doing a similar calculation on the REIT revenues for those tenants. The net result is a retail REIT sector chart that looks like this.

{kind=link}

In talking to the REIT managers one hears a very different story. It is not fear that BBBY or other retailers will default on their leases, but more hoping they default soon so that they can be replaced.

This all boils down to the tenant-landlord relationship. The tenant is only as valuable to the REIT as the delta between their rent and what the property could otherwise generate in rent. In cases like BBBY or other struggling retail tenants they are generally paying somewhere around $13 to $20 a foot in spaces that now rent for closer to $15 to $25 a foot.

There might be a minor hiccup to cashflows in the window of finding a new tenant, but overall that is arguably a positive event for the REIT. Thus, in looking at battleground stocks I would advise focusing more on the properties and less on the tenants.

The value of the property

It is the property that determines the market rent. If a property is well maintained and well located it is going to command a high market rent upon re-leasing. This is the key to figuring out whether the tenant has a negative or positive value to the REIT.

It answers the question of whether the REIT is benefited or harmed by a tenant vacating its space. With this in mind, I would like to apply the tenant value equation to each of the battleground stocks.

Medical Properties Trust

There has been such a tremendous amount of news and analysis on the relationship between MPW and Steward that MPW is traded as if their fates are linked. When Steward misses a filing deadline, MPW sells off 5% and when Steward successfully extended its loan with their bank MPW soared.

All of this trading activity is predicated on the notion that Steward is somehow hugely important to MPW. I see Steward as just another tenant. Its value to MPW is defined by the same equation that governs other tenant lease contracts.

{kind=link}

As far as I can tell, Steward is paying approximately market rent. Hospitals are in high demand so the properties can be re-leased at similar rates to new tenants if Steward fails (no idea on the likelihood of that).

So if contracted rent is roughly equal to market rent then the value of Steward to MPW is close to zero.

This, of course, is an oversimplification as it refers to the long run value. Re-leasing does cause a hiccup in revenues and since Steward is a large tenant it would be a significant hiccup. Given MPW’s size I think they can handle it just fine.

Perhaps one could disagree with me on that point, but this is a reasonable framework from which to analyze the situation.

Trading MPW as a proxy for Steward is not the right way to go about things. I have no idea what fate will come to Steward and as an MPW investor I don’t particularly care.

Welltower

WELL has been sold off after a bear attack suggesting a major tenant of Welltower (ProMedica/Integra) is likely insolvent or potentially fraudulent.

In this article the idea I am really trying to establish is that tenant is not equal to landlord. They are separate entities only related via the rental contract.

In the worst case scenario in which Integra is just a house of cards as insinuated in the attack, it simply doesn’t affect Welltower that much. WELL owns the properties and would continue to own the properties and can re-lease them.

I don’t think WELL is a great value right now, but it should be traded on the fundamental outlook for senior housing and skilled nursing properties, not on the intricacies of an individual tenant.

Innovative Industrial Properties

This case is particularly interesting because, unlike the others, it involves a substantial overvaluation due to the market not fully understanding the landlord-tenant relationship.

So far, I have been hammering home the idea that a tenant bankruptcy is not necessarily a big deal for the REIT.

In IIPR’s case it absolutely is.

The reason goes back to that same equation. IIPR was signing leases that were approximately 3X market rent for similar properties. This means that upon signing a new tenant, IIPR would likely lose about 2/3 of its rent on the related properties.

Therefore, the existing tenants are incredibly valuable to IIPR. It needs those tenant to stay healthy so IIPR can keep collecting the far above market rent.

The takeaway

Sticky tenant situations make for great stories. They are entertaining, aggravating, and intriguing, but at the end of the day, REITs are about real estate. It is the real estate fundamentals that matter and I would strongly encourage approaching these battleground stocks with a focus on real estate basic fundamentals. Tenant bankruptcies have happened for decades but the real estate lives on.

Factors that matter

- Above or below market rent

- Location of property

- Fungibility of property

- Demand for property type relative to supply

- Frictional costs of re-tenanting

For further details see:

The Profound Misunderstanding Of The Landlord-Tenant Relationship