SKY - The Pros And Cons Of Investing In Skyline Champion

2023-06-07 12:26:01 ET

Summary

- Skyline Champion Corporation is a leading player in the factory-built housing market and has useful qualities such as exemplary cash-generation and a strong balance sheet.

- However, the company faces a weak outlook, and forward valuations look pricey.

- The momentum is currently with the bears, and we also think SKY could do a better job with its capital allocation plans.

Introduction

Skyline Champion Corporation (SKY) is an Indiana-based producer of factory-built housing (homes manufactured in a factory). These factory-built homes (typically 400 to 4000 square feet) are constructed across 43 manufacturing facilities within North America (38 in the US and 5 in Canada).

{kind=link}

We think this is an intriguing story but we're also wary of an investment at this juncture. Here are some of the major pros and cons of investing in the SKY stock.

The Pros

The factory-built housing segment may not necessarily account for a large chunk of the overall housing market (for context, SKY's market share within the overall housing market is less than 3% ), but within this segment, SKY has ample stature. It is the second biggest player in the manufactured housing market (35 entities compete in this segment), and alongside the number 1 and number 2 entities, largely controls and dictates the dynamics within the market. For context, the combined market share of the top 3 players, is a whopping 80% , highlighting how difficult it is to crack and build scale in this segment.

We'd like to think that relatively low-cost of manufactured homes can give SKY an edge in the current housing environment where supply-side shortages exist, and buyers still have the appetite to buy homes but are priced out on account of a higher interest rate regime and general affordability issues. For context, MHI believes that the average price per square foot of factory-built homes costs half as much as site-built homes.

The construction of factory-based homes is generally more efficient than traditional homes, and the former is also not vulnerable to weather-related encumbrances that tend to disrupt the latter. Since these factory-based homes are constructed to withstand transportation, they are also generally sturdier.

We also like SKY's profile as a relentless cash compounder. Note that over the last 5 years, the cash flow from operations (OCF) has grown every single year, growing by 13x in aggregate.

Seeking Alpha

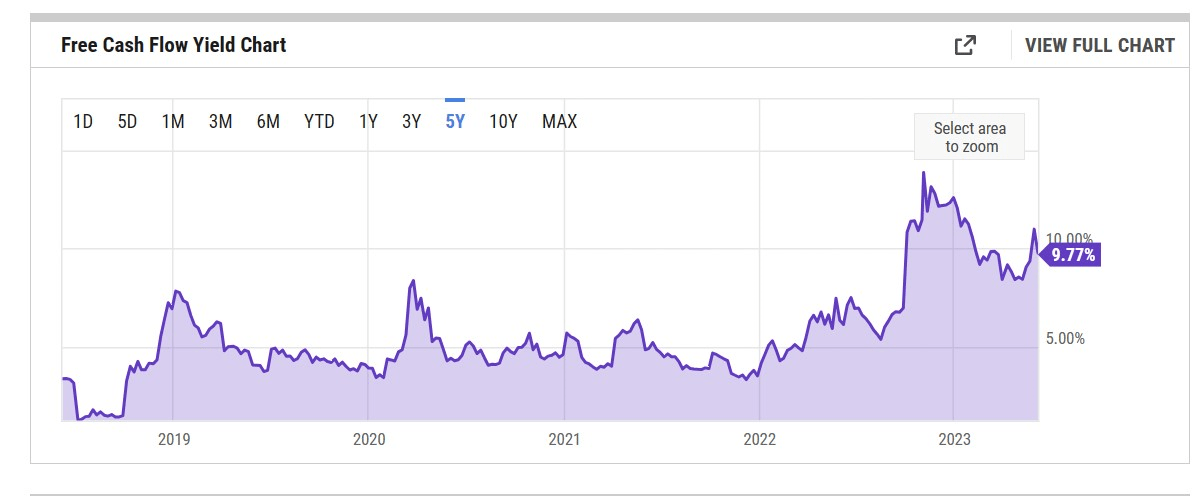

On account of the strong OCF generation, SKY's current free cash flow yield is close to double-digit levels and better than the 5-year average of 5.56%

{kind=link}

Even though SKY may likely face some net income challenges in the current year, we don't expect inventory to be a big drag on cash flow generation as management is not too keen to ramp up production aggressively and wants to build it linearly.

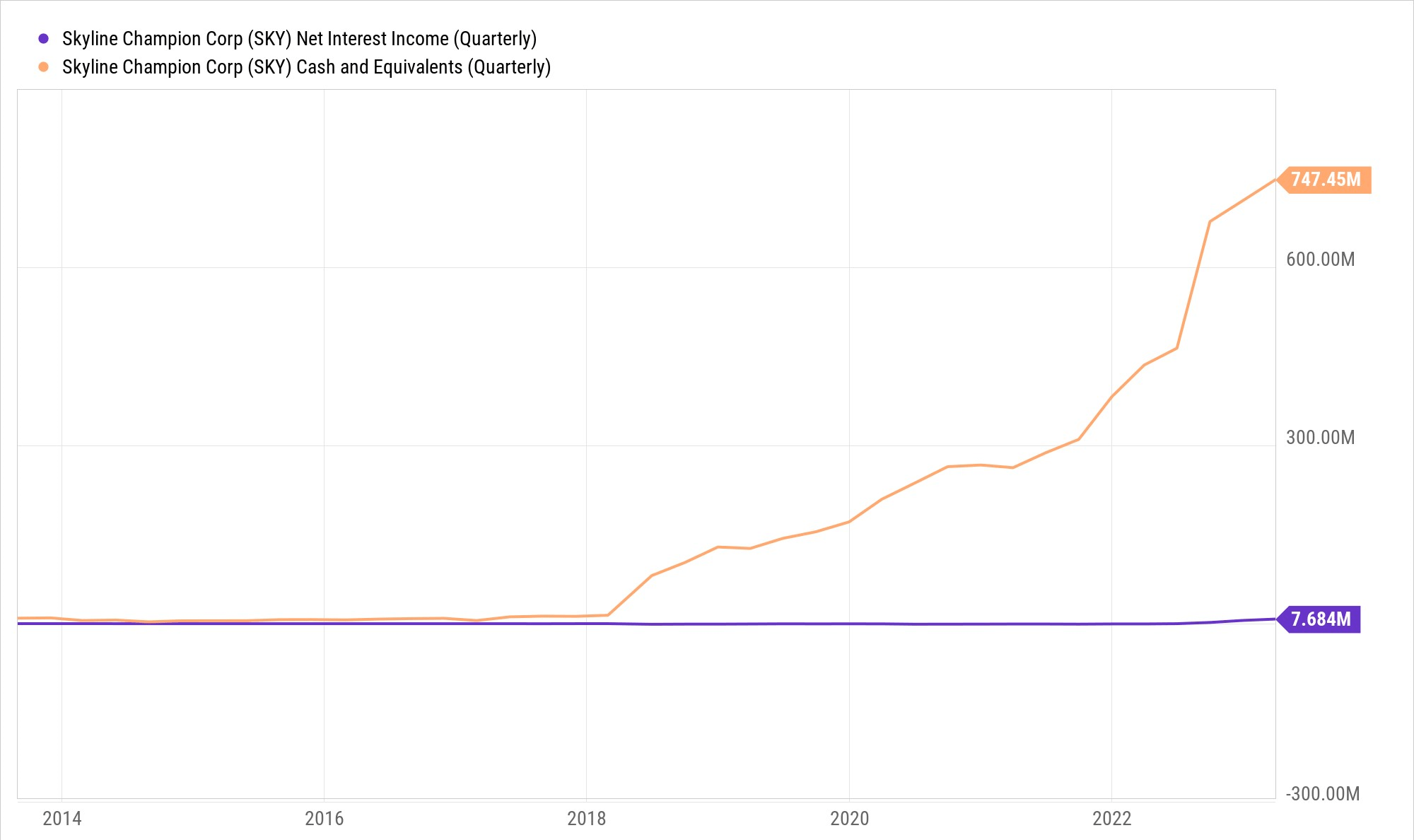

For a discretionary, growth play, SKY also offers some defensiveness on account of its sturdy balance sheet. You're basically looking at a business that has maintained a net cash position (where cash exceeds debt) over the last 7 years. Given the strong cash-generating abilities, cash on the books is currently at record highs of $748m, and accounts for the largest chunk of the asset base (48% of total assets). Whilst most other housing businesses will have to contend with heightened debt bills and interest expenses, SKY, on account of its superior net cash position has been generating net interest income in recent periods, thus abetting profit margins.

{kind=link}

The Cons

Despite all these merits, we don't believe SKY would make a wise investment at this juncture. Here's why

Firstly, the outlook isn't great. In the March quarter, which is Q4 for SKY (SKY's FY ends on April 1st), sales were down by 23% YoY, and if you thought that was bad enough, do consider that management guided to another mid-single-digit decline on a QoQ basis in the June quarter. This effectively translates to a sizeable YoY decline of 36% for the whole year. As things stand, SKY's capacity utilization rates are sub-par at only 59% (down from 66% in the Dec quarter), on account of retail destocking, and the opening of a new facility in Pembroke, North Carolina.

Admittedly, the YoY sales de-growth should improve as we progress through the year, but even by the end of the year, the company is unlikely to post any growth. Consensus currently expects a -23% decline for the whole of FY24.

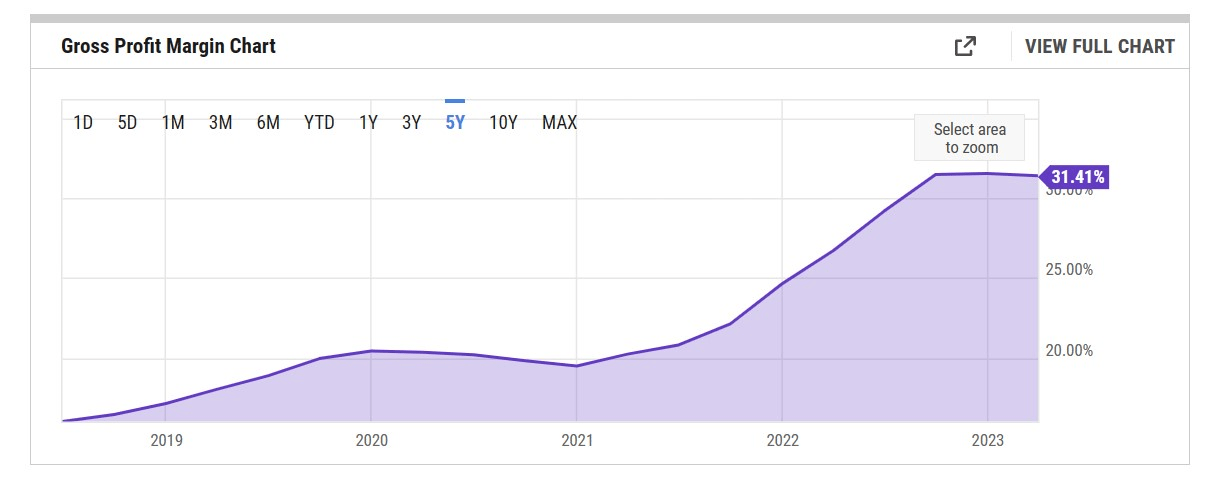

It isn't just top-line pressures; management has noted that its customers are currently largely opting for smaller homes with limited options which inevitably also come with lower ASPs (average selling prices). Consequently, expect gross margins - which have been quite stellar off late (see image below)- to take a hit, and drift closer to the FY22 levels of 26-27%.

{kind=link}

Meanwhile, after witnessing a 300% expansion in the EBITDA over 2 years, some sense of normalcy is to be expected, with consensus expecting EBITDA this year to drop off by -47% YoY. All these factors will also leave a mark on the FY24 EPS which is poised to come in at only $3.71, a considerable YoY drop of -49%.

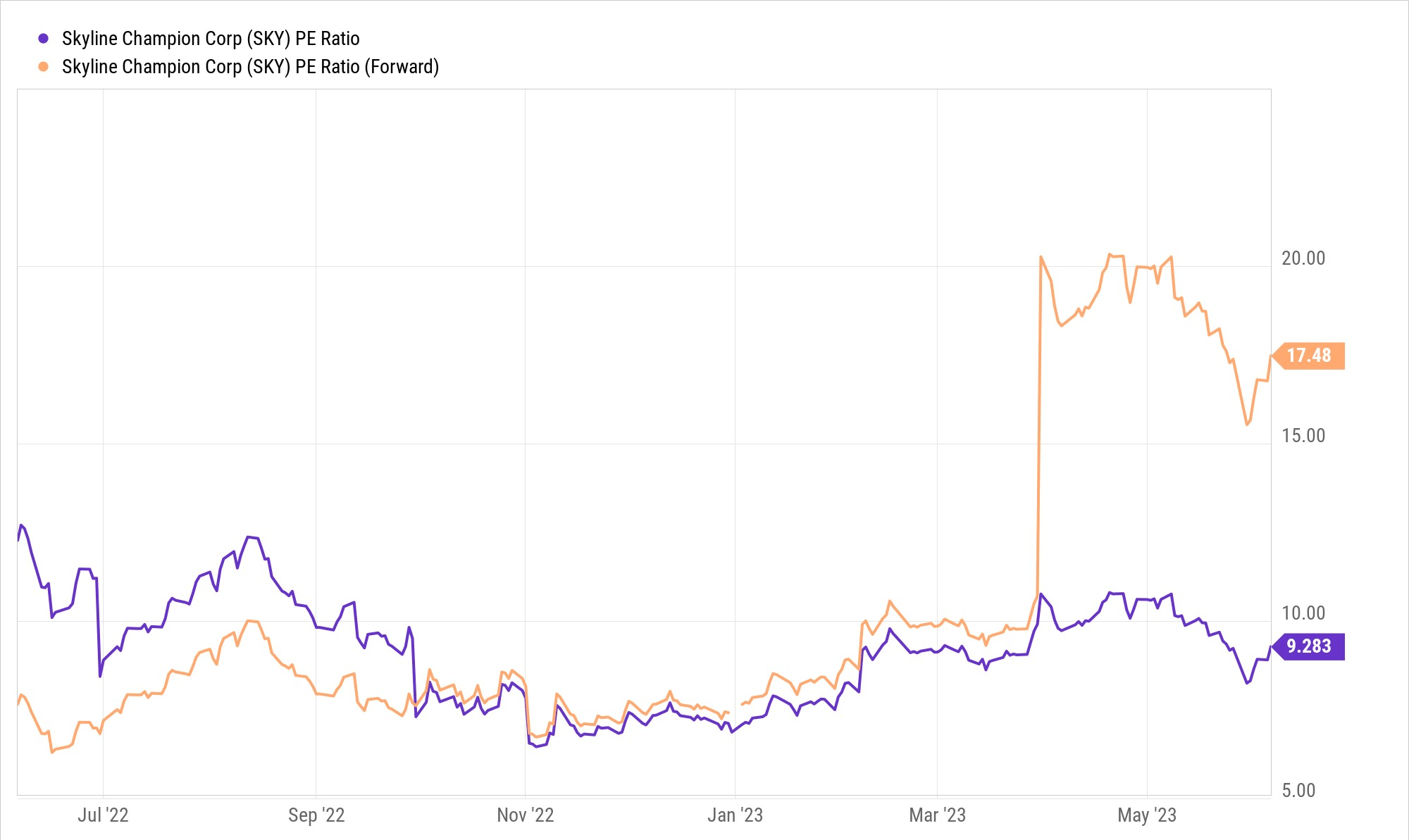

Typically with most companies, you'd expect the forward P/E to be lower than the trailing P/E but such is the expected drop off in SKY's EPS, that you see its forward P/E go through the roof at 17.4x, almost 2x as much as the trailing P/E. Relative to the stock's own 5-year forward P/E average (the rolling average over the last 5 years), SKY currently trades at a 78% premium.

{kind=link}

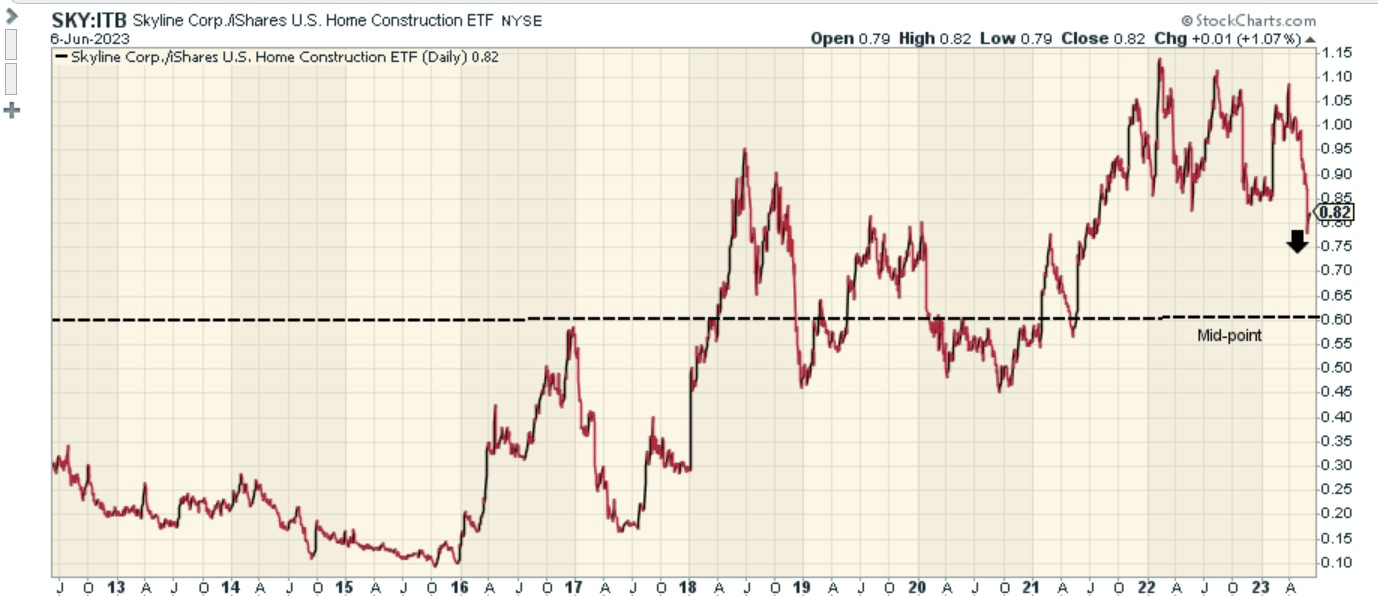

Then, relative to other US home construction stocks, SKY does not appear to be the most promising option for rotation; the image below shows you that the relative strength ratio of SKY over the US Home Construction ETF is still around 37% higher than the mid-point of the long-term range

{kind=link}

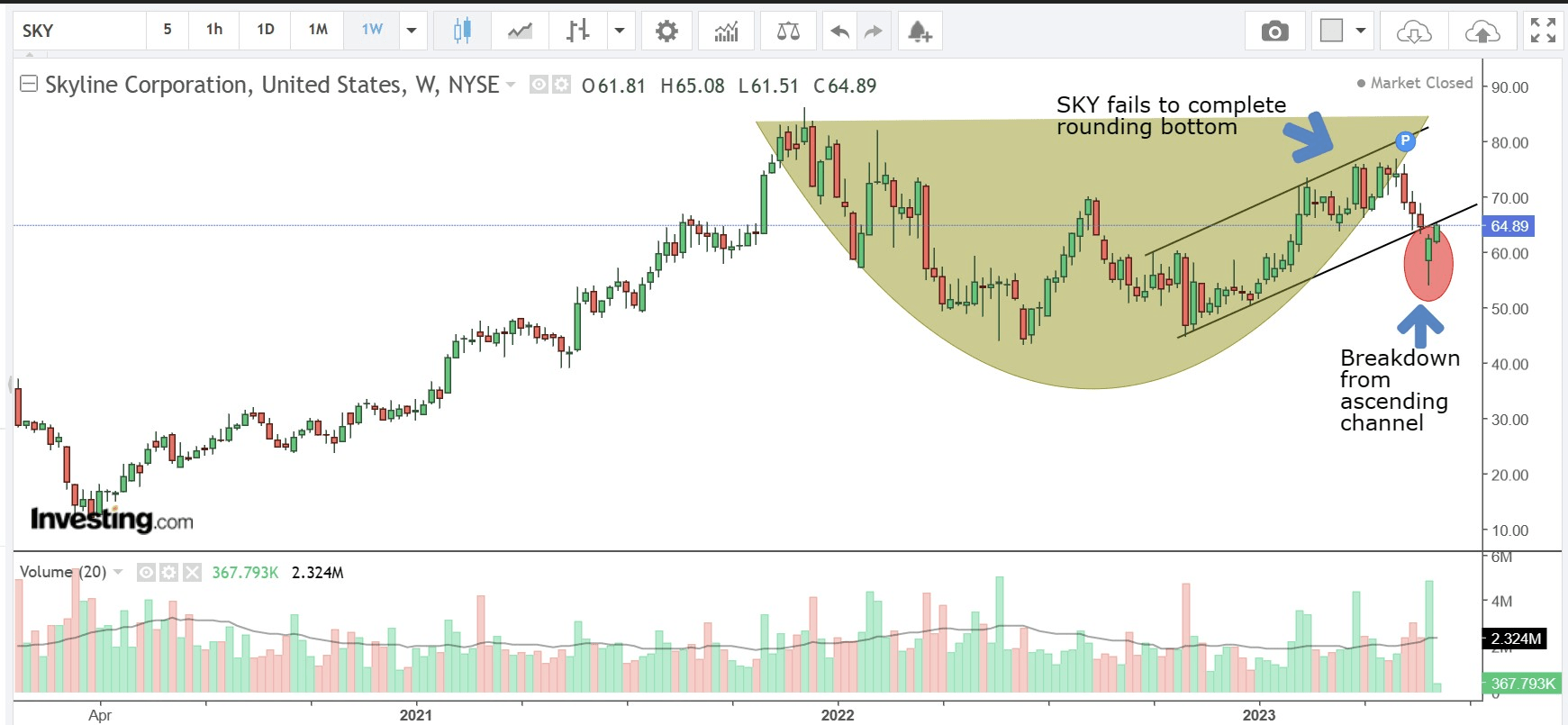

On SKY's own standalone chart, there appears to be a real tug-of-war between the bulls and the bears, with the latter gaining an edge in recent periods. Since the turn of this year until May, it looked like the bulls would have their way as the stock was on the cusp of forming a rounding top (at the $86 levels), even as it continued to trend up in the shape of an ascending channel. However, it failed to witness any traction around the $75-$77 range and that's when you saw the bears go for the jugular, sending the stock crashing out of its ascending channel.

{kind=link}

Finally, we also feel that SKY is not doing an effective enough job with its capital allocation strategies. With such enormous cash balances, and strong OCF generation, there was the opportunity to go ahead with a special dividend or kickstart a buyback program after the last fiscal, but that does not seem to be on the agenda; we feel this lack of capital distributions dampens the investment case of SKY.

For further details see:

The Pros And Cons Of Investing In Skyline Champion