SPMD - The Recession Must Be Confirmed With A Weakening Labor Market

2023-04-05 12:07:17 ET

Summary

- The labor market is still strong, but showing some cracks.

- However, given the Fed's guidance, there could be 2M+ jobs lost by the end of 2023.

- The S&P 500 is facing a recessionary selloff, as earnings are downgraded.

The Wall Steet consensus is that the US economy is possibly already in a recession (Q2 2023). Except the labor market is still very tight, and it's difficult to acknowledge a recession as long as the labor market data is strong, especially for the service-based economy like the US. Thus, the key monthly labor report is exceedingly important.

Labor Report - Expectations for March 2023

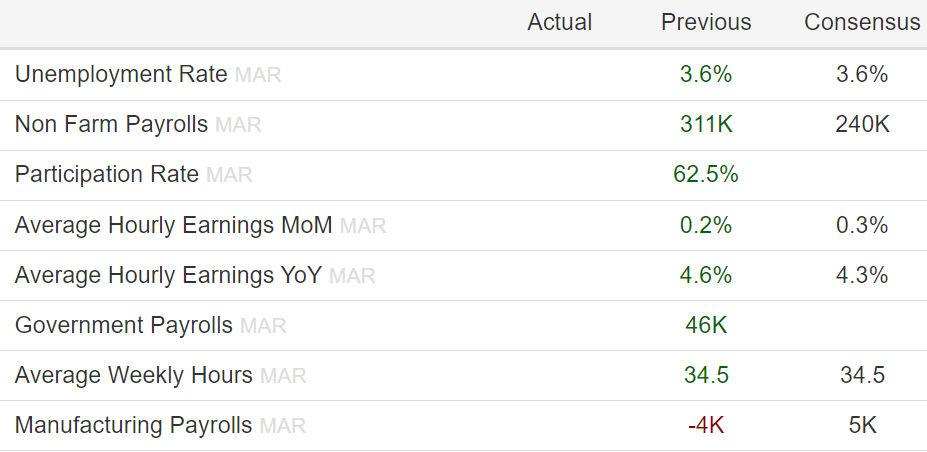

Here's the current state of the labor market, and the expectations for the Friday's labor report for March 2023:

{kind=link}

The unemployment rate is expected to stay at a ultralow level at 3.6%, which suggests that the expectations are that the labor market is still very tight. Consistently, wage growth is expected to increase on a month-over-month basis to 0.3%, over 0.2% in February, which is not the good news for the service part of inflation, even as the year-over-year the wage growth slows to 4.3% from 4.6%.

The expectations also are that the economy would produce 240K new jobs, which is below the 311K number from February, but still consistent with healthy economic growth. Manufacturing jobs are expected to increase by 5K, which would be a reversal form the 4K jobs lost in February - also a positive for the overall economy.

Thus, the expectations are that the labor data for March is still very strong, indicating a healthy economic growth - while Wall Street sees a recession. Something has to give. The recession is expected to start in Q2 2023, or starting with April 2023 labor data, so the March data would at least show some weakening.

Recent indications of the labor market slowdown

In fact, some of the recent labor data already has indicated cracks in the labor market:

- The ADP report showed below consensus 145K new jobs created in March, well below the 261K new jobs created in February and the consensus of 200K.

{kind=link}

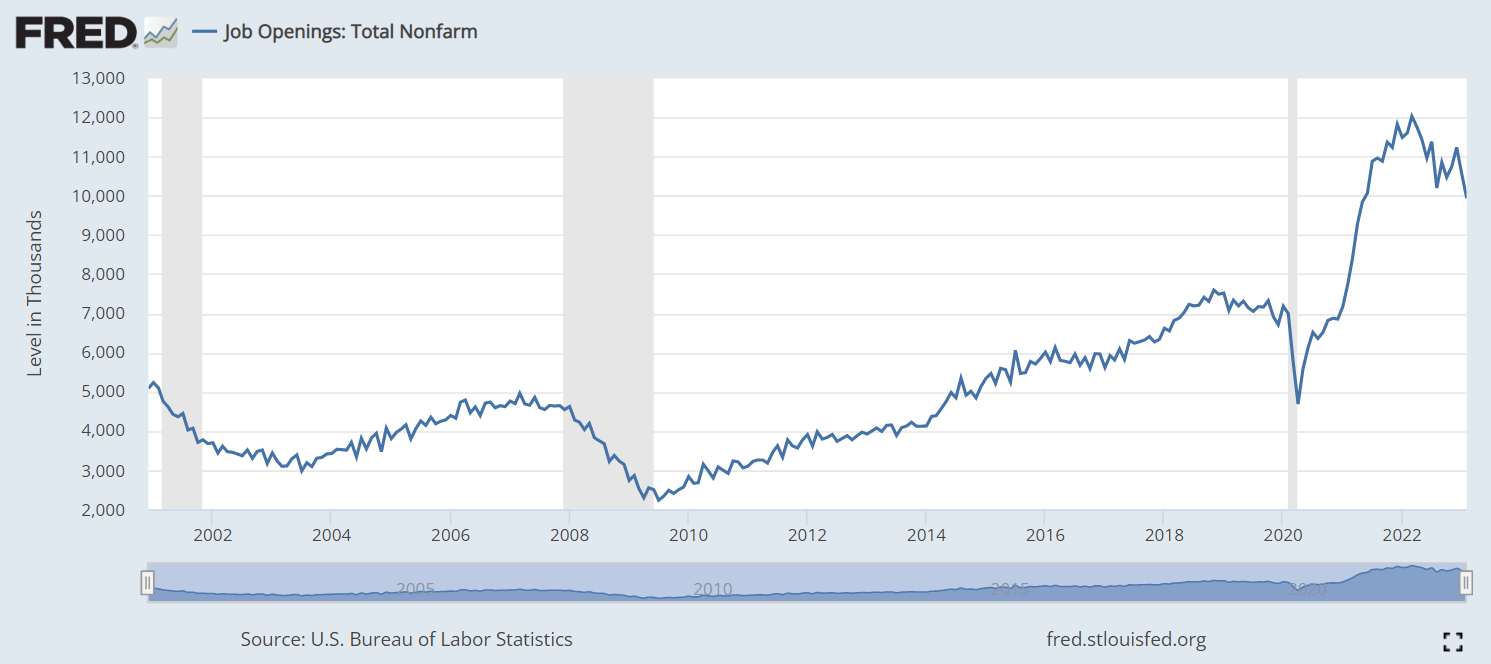

- The JOLTS report also indicated that job openings have started to fall from the post-pandemic spike, currently below the 10M level for the first time since the peak.

{kind=link}

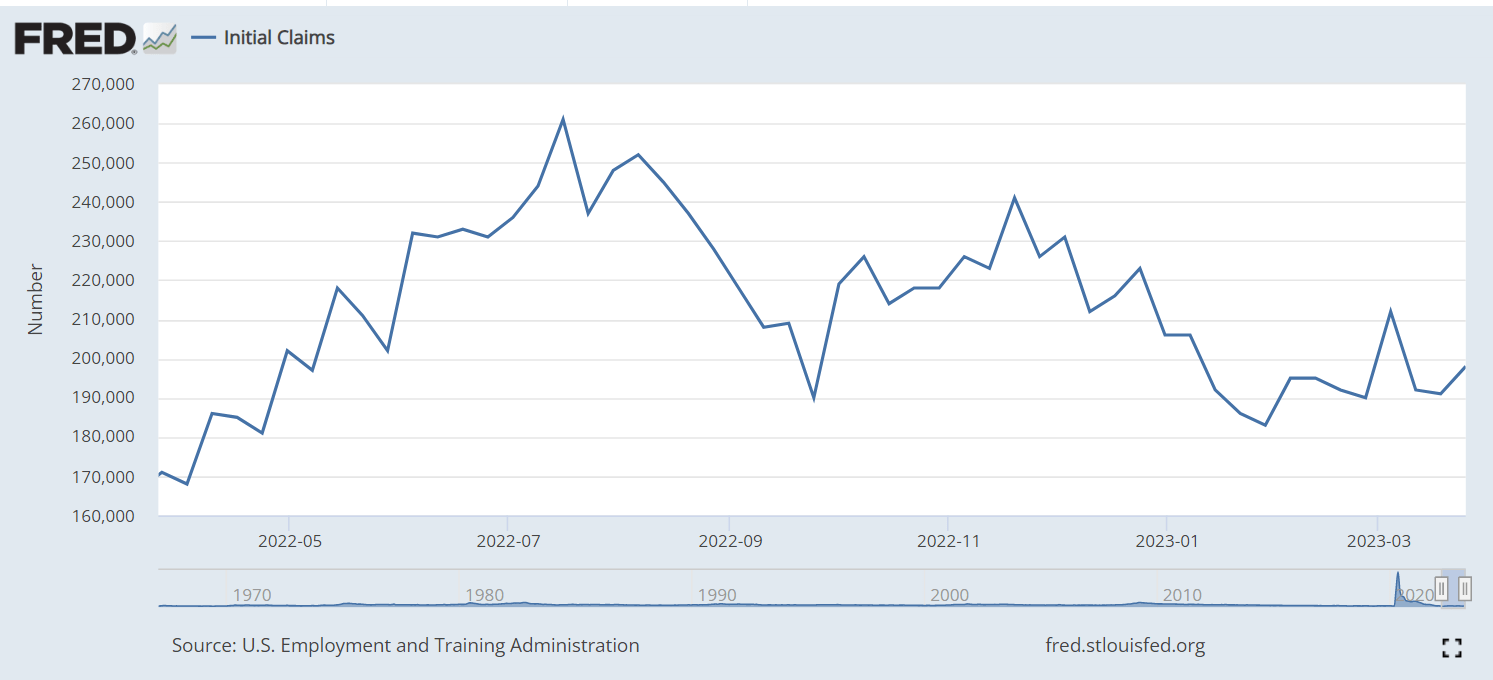

- However, the initial claims for unemployment data, which is the weekly indicator, and thus considered as the leading indicator for labor market strength, has been very strong, staying below the 200K level. Yet the weekly data on March 30 was above the consensus (198K vs 196K expected), which could indicate some weakening in the labor market.

{kind=link}

Note, these are only cracks in what is still a very strong labor market.

The Fed's expectations for 2023

The expected recession is (or would be) in fact the Fed-induced recession. The Fed has been trying to rein in the inflationary shock and hiked interest rates from near 0% to near 5% over the 12-month period.

The Fed is specifically targeting the labor market, and (in the post March 2023 FOMC meeting SOE projections) the Fed specifically guided that the unemployment rate will have to rise to 4.5% by the end of 2023, and more importantly stay at the 4.6% level in 2024 and 2025 to gradually bring the core PCE inflation down to the 2% level by the end of 2025.

The Fed

Expectation of 2M+ jobs lost in 2023?

In fact, the increase in the unemployment rate from 3.6% to 4.5% in 2023 would be recessionary.

Currently, the US civilian labor force counts around 166M people, with around 6M unemployed, which is approximately a 3.6% unemployment rate. The increase in the unemployment rate to 4.5% would require around 7.5M unemployed people, but given the growth in the civilian labor force, the number of unemployed people would have to increase to close to 8M by the end of 2023, which is at least 2M more people unemployed compared to now.

Thus, the payroll report would have to start showing around 200K jobs lost on average every month until the end of 2023, starting with April 2023, to produce the expected 2M jobs lost and the increase in the unemployment rate to 4.5%.

The March 2023 payroll report will likely not show any jobs lost. In fact, based on the predictions from the weekly initial claims numbers, the March 2023 payroll numbers will still show a strong labor market, but possibly confirm some weakening.

The key variable is the Fed's guidance for the Federal Funds rate in 2023. Specifically, the Fed guides that the Federal Funds rate will stay at 5.1%, even as the labor market weakens - the higher for longer policy. This is likely to cause the expected increase in the unemployment rate to 4.5%. The recession is possibly here, but don't expect the Fed to help until the inflation rate falls (or is on the track to fall) to 2%.

Effect on financial markets

The March labor report could have a significant effect on the financial markets if it confirms significant weakening, with the big miss below the consensus and below the 200K level, consistent with the ADP report.

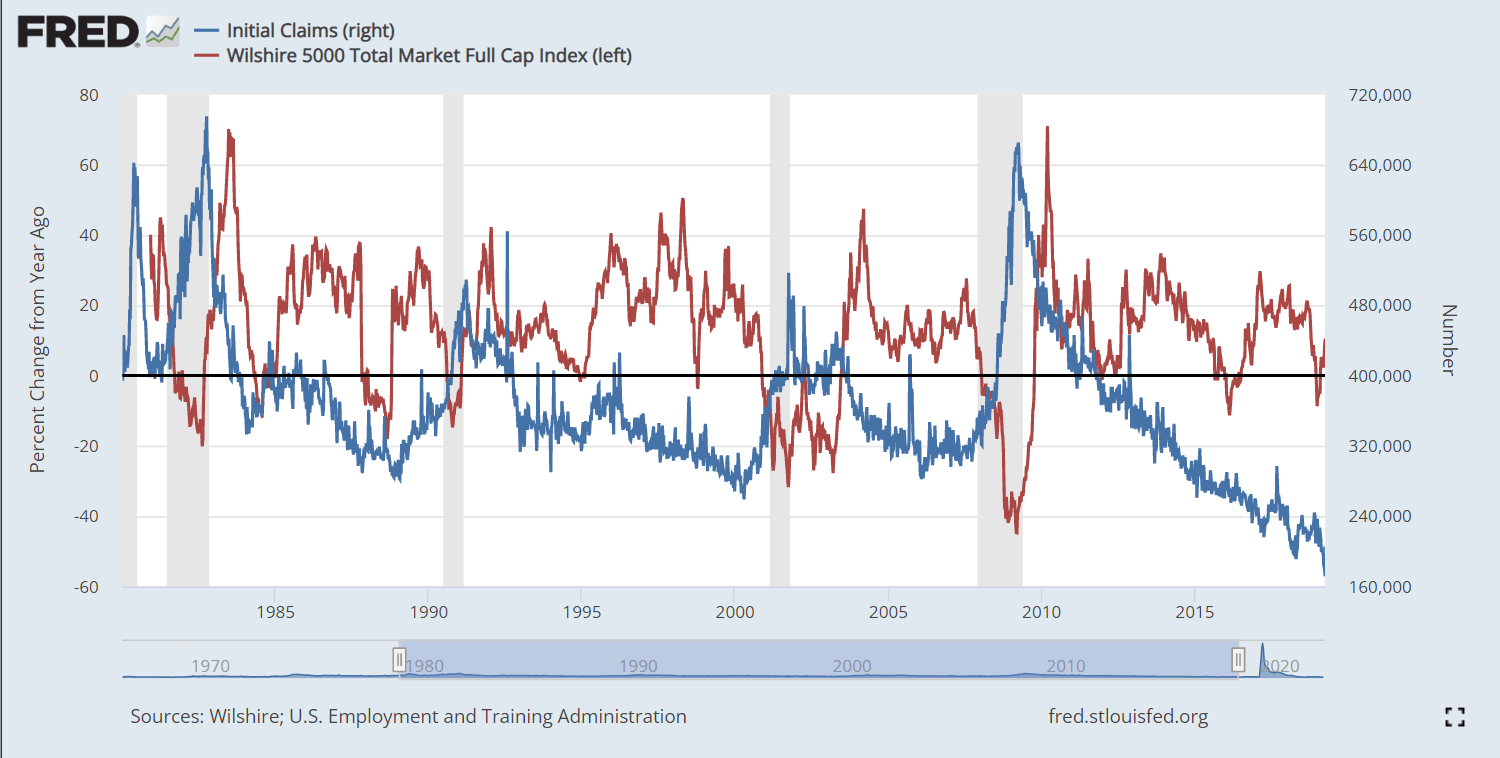

However, the key indicator going forward will be the weekly claims for unemployment. The research shows that weekly claims for unemployment data strongly predicts the monthly payroll report, especially in a weakening labor market.

The chart below shows the percent change in stock market (in this case proxied with Wilshire 5000 index) from the year before, in relation to the weekly claims for unemployment:

{kind=link}

If you look at the 2008 case, the rise in the initial claims (blue) was perfectly negatively correlated with the falling stock market measure (red). The same relationship holds in 2000, 1991, and 1980.

Thus, the key trigger for the recessionary selloff in S&P 500 ( SP500 ) will likely be the sharp increase in the unemployment claims.

The Fed's tight monetary policy, reflected in a deeply inverted 10Y-3mo yield curve, already has caused the banking crisis in March 2023, which will likely result in an immediate tighter lending standard, and likely start showing up in the initial claims for April.

The S&P 500 is still overvalued with the forward PE ratio near 18. The recession will force the bottom-up analysts to significantly downgrade the earnings for 2023. Thus, S&P 500 has a significant downside from here given the expected selloff in reaction to the lower earnings projections and further contracting PE valuation metric.

For further details see:

The Recession Must Be Confirmed With A Weakening Labor Market