UMPQ - The Retiree's Dividend Portfolio John's December Update: Outperformed The Major Indexes In 2022

Summary

- John's retirement accounts generated a total of $2,976.09 of dividend income for December 2022 vs. $2,306.98 of dividend income for December 2021.

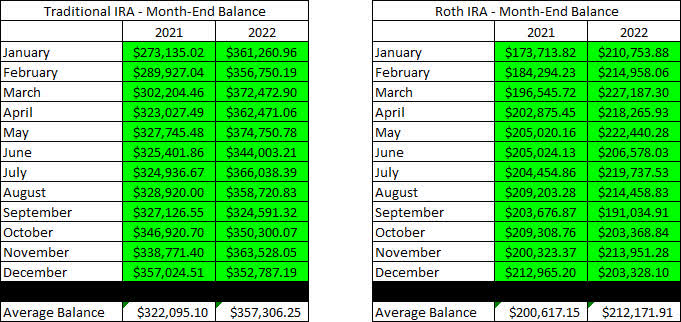

- John's Traditional IRA had a balance of $352.8K as of December 31, 2022, vs. $357K on December 31, 2021. The estimated annualized yield is 5.70%.

- John's Roth IRA had a balance of $203.3K as of December 31, 2022, vs. $213K on December 31, 2021. The estimated annualized yield is 4.48%.

- There were three companies that paid an increased dividend during the month of December.

Similar to the other December articles, I want to use this opportunity to review how the portfolio performed against the three major indexes for 2022. John's review will have similarities with the Taxable Account review (link at the end of the article) because we are going to add back the withdrawals that were made to better understand how the portfolio would have performed if no funds had been taken from the account.

Traditional IRA - The balance of the account on December 31, 2022, was $352,787.19 which compares to the balance at the end of December 31, 2021, of $357,024.51. The Traditional IRA had a total of $12K of withdrawals ($1,000 per month) which means that the ending balance would have been $364,787.19. This means that John's Traditional IRA saw positive growth in 2022 of 2.13% growth when we add back the withdrawals taken during the year.

Roth IRA - The balance of the account on December 31, 2022, was $203,328.10 which compares to the balance at the end of December 31, 2021, of $212,965.20. The Roth IRA had no withdrawals in 2022 so we will use the $203,328.10 for the calculation. This means that John's Roth IRA saw negative growth in 2022 of -4.53%.

The graph below shows how this compares to the performance of the three main indexes.

Once again, John and Jane's portfolio has withstood a harsh environment in 2022 and his Traditional IRA performed exceptionally well when we consider what the balance would look like with the distributions added back.

Background

For those who are interested in John and Jane's full background, please click the following link here for the last time I published their full story. The details below are updated for 2022.

- This is a real portfolio with actual shares being traded.

- I am not a financial advisor and merely provide guidance based on a relationship that goes back several years.

- John retired in January 2018 and now only collects Social Security income as his regular source of income.

- Jane officially retired at the beginning of 2021, and she is collecting Social Security as her only regular source of income.

- John and Jane have decided to start taking draws from the Taxable Account and John's Traditional IRA to the tune of $1,000/month each. These draws are currently covered in full by the dividends generated in each account.

- John and Jane have other investments outside of what I manage. These investments primarily consist of minimal-risk bonds and low-yield certificates.

- John and Jane have no debt and no monthly payments other than basic recurring bills such as water, power, property taxes, etc.

The reason why I started helping John and Jane with their retirement accounts is that I was infuriated by the fees they were being charged by their previous financial advisor. I do not charge John and Jane for anything that I do, and all I have asked of them is that they allow me to write about their portfolio anonymously in order to help spread knowledge and to make me a better investor in the process.

Generating a stable and growing dividend income is the primary focus of this portfolio, and capital appreciation is the least important characteristic. My primary goal was to give John and Jane as much certainty in their retirement as I possibly can because this has been a constant point of stress over the last decade.

Dividend Decreases

No stocks in John's Traditional or Roth IRA put/decreased dividends during the month of December.

Dividend And Distribution Increases

Three companies paid increased dividends/distributions or a special dividend during the month of December in the Traditional and Roth IRAs.

CCI and MAIN were covered in Jane's Retirement Account update, so I will only include information about the dividend increases. Those interested in reading the summary of these two companies can check the link included at the end of the article.

Crown Castle International - The dividend was increased from $1.47/share per quarter to $1.565/share per quarter. This represents an increase of 6.5% and a new full-year payout of $6.26/share compared with the previous $5.88/ share. This results in a current yield of 4.23% based on the current share price of $148.12.

Main Street Capital - The dividend was increased from $.220/share per month to $.225/share per month. This represents an increase of 2.3% and a new full-year payout of $2.70/share compared with the previous $2.64/ share. This results in a current yield of 6.90% based on the current share price of $39.15.

MAIN also paid a special supplemental dividend of $.10/share during the month of December.

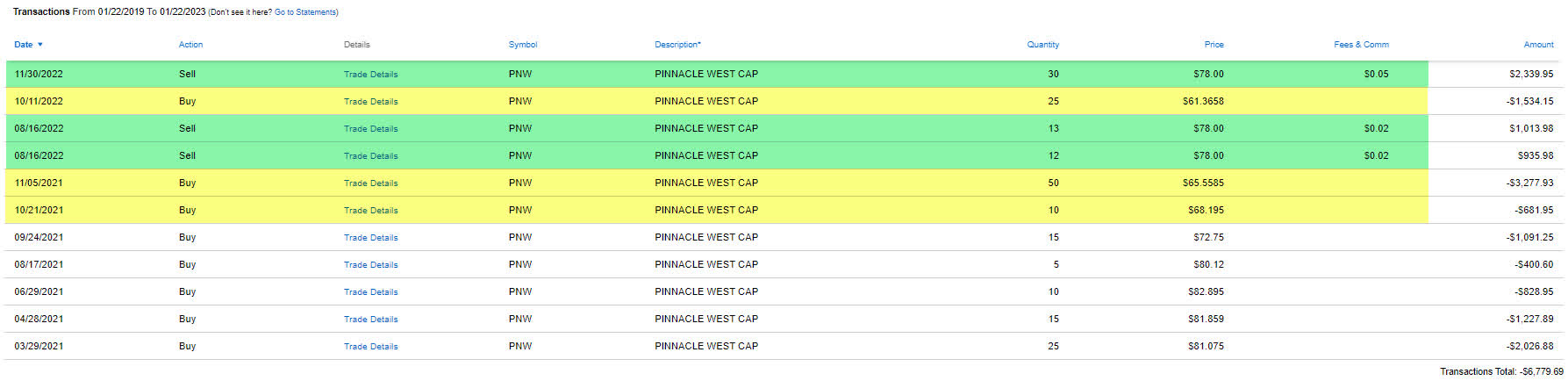

Pinnacle West - PNW's recent price volatility is largely related to the previous rate case that went into effect on December 1st, 2021. This decision meant that PNW is restricted when it comes to rate increases that would have helped offset inflationary pressure. This created a buying opportunity in December 2021 and October 2022. We won't be seeing PNW move back up to $100/share anytime soon but the dividend yield and upside are compelling when shares trade under $70/share.

We used these buying opportunities to add shares and then sell off the high-cost portion of the position. The image below shows all of the trades made with PNW and you can see that the position was originally built on higher-cost shares. The cost basis after recent purchases and sales is now $65.85/share which is a great long-term position to be in.

{kind=link}

The dividend was increased from $.85/share per quarter to $.865/share per quarter. This represents an increase of 1.8% and a new full-year payout of $3.46/share compared with the previous $3.40/ share. This results in a current yield of 4.59% based on the current share price of $75.36.

Retirement Account Positions

There are currently 38 different positions in John's Traditional IRA and 23 different positions in his Roth IRA. While this may seem like a lot, it is important to remember that many of these stocks cross over in both accounts and are also held in the Taxable Portfolio.

Below is a list of the trades that took place in the Traditional IRA during the month of December.

{kind=link}

Below is a list of the trades that took place in the Roth IRA during the month of December.

{kind=link}

For more details/insight into these trades and the rationale please see my trades summary articles (I will be working on that article next to cover December and January Trades).

December Income Tracker - 2021 Vs. 2022

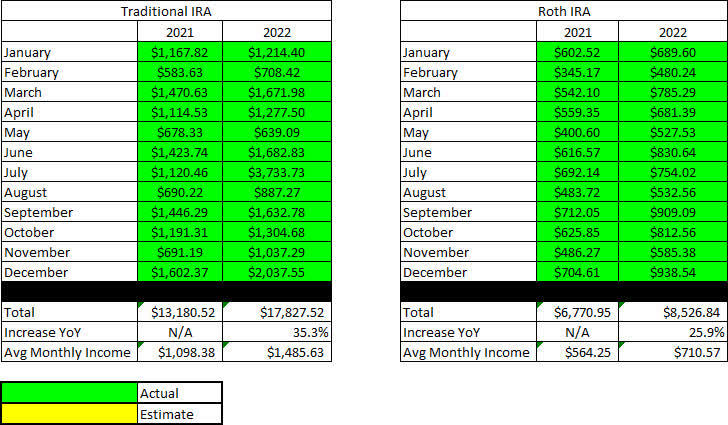

December's income for the Traditional IRA and Roth IRA were up considerably year-over-year.

- The average monthly income for the Traditional IRA in 2022 (compared to 2021) was up 35.3% YoY.

- The average monthly income for the Roth IRA in 2022 (compared to 2021) was up 25.9% YoY.

This means the Traditional IRA would generate an average monthly income of $1,485.63/month and the Roth IRA would generate an average income of $710.57/month. This compares with 2021 figures that were $1,098.38 and $564.25 per month, respectively. John's Retirement Accounts were able to generate a total of $6,402.89 more in dividend income than what was received in 2021.

It should be noted that a large amount of the increase in dividend income in the Traditional IRA can largely be attributed to the significant special dividend paid by Healthcare Realty ( HR ). For more information please reference the July update.

SNLH = Stocks No Longer Held - Dividends in this row represent the dividends collected on stocks that are no longer held in that portfolio. We still count the dividend income that comes from stocks no longer held in the portfolio even though it is non-recurring.

All images below come from Consistent Dividend Investor, LLC. (Abbreviated to CDI).

Traditional IRA - December - 2021 V 2022 Dividend Breakdown (CDI) Roth IRA - December - 2021 V 2022 Dividend Breakdown (CDI)

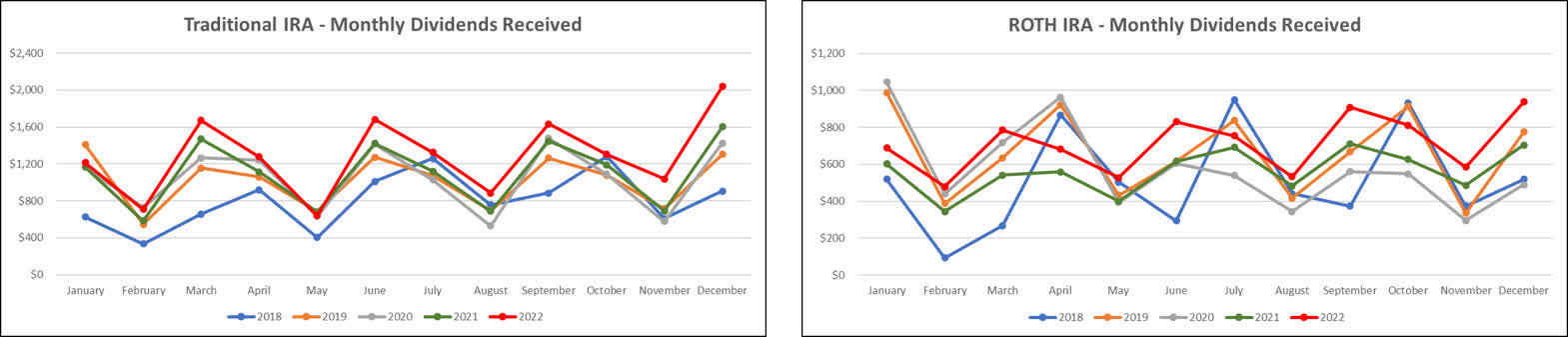

Here is a graphical illustration of the dividends received on a monthly basis for the Traditional and Roth IRAs.

Retirement Account - Monthly Dividends Received - December 2022 (CDI)

{kind=link}

Based on the current knowledge I have regarding dividend payments and share count, the following tables are a basic prediction of the income we expect the Traditional IRA and Roth IRA to generate in FY-2022 compared with the actual results from 2021.

{kind=link}

Below is an expanded table that shows the full dividend history since inception for both the Traditional IRA and Roth IRA.

Retirement Projections - December 2022 - Full Dividend History (CDI)

{kind=link}

I have included line graphs that better represent the trends associated with John's monthly dividend income generated by his retirement accounts. The images below represent the Traditional IRA and Roth IRA, respectively.

Retirement Account - Monthly Dividends - December 2022 (CDI)

{kind=link}

Here is a table to show how the account balances stack up year over year (I previously used a graph but believe the table is more informative).

Retirement Account - Month End Balances - December 2022 (CDI)

{kind=link}

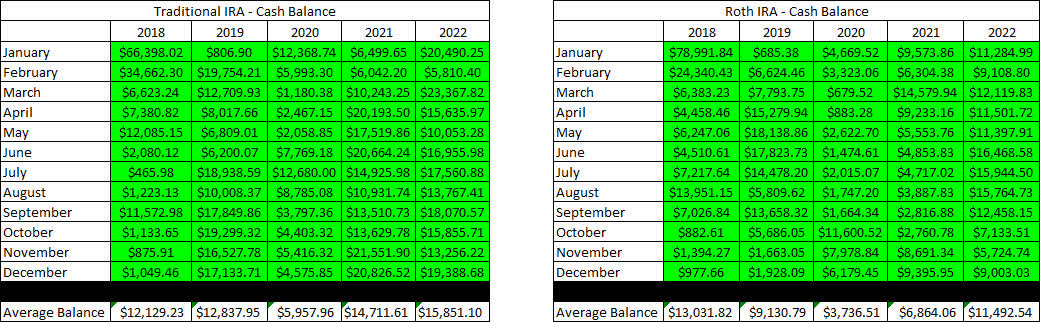

The next images are the new tables that indicate how much cash John had in his Traditional and Roth IRA Account at the end of the month, as indicated on his Charles Schwab statements.

{kind=link}

The following two tables provide a history of the unrealized gain/loss at the end of each month in the Traditional and Roth IRAs, going back to the beginning of January 2018.

Retirement Accounts - December 2022 - Unrealized Gain-Loss (CDI)

{kind=link}

John has finally begun taking disbursements from his Traditional IRA, and he has opted to receive $1,000/month. Based on the dividend income generated he could take up to $1,400/month from the Traditional IRA before his withdrawals would start to negatively impact his principal. Our goal for John is to maintain withdrawals below the dividend income generated for as long as possible.

Traditional IRA Withdrawals - December 2022 (CDI)

I like to show readers the actual unrealized gain/loss associated with each position in the portfolio because it is important to consider that, in order to become a proper dividend investor, it is necessary to learn how to live with volatility. The market value and cost basis below are accurate as of the market close on January 20, 2023.

Here is the unrealized gain/loss associated with John's Traditional and Roth IRAs.

Traditional IRA - December 2022 - Gain-Loss (CDI) Roth IRA - December 2022 - Gain-Loss (CDI)

It should be noted that Essex Property Trust ( ESS ) and Prologis ( PLD ) reflect an annual yield of 0% because these were recently established positions and no dividends were received in 2022.

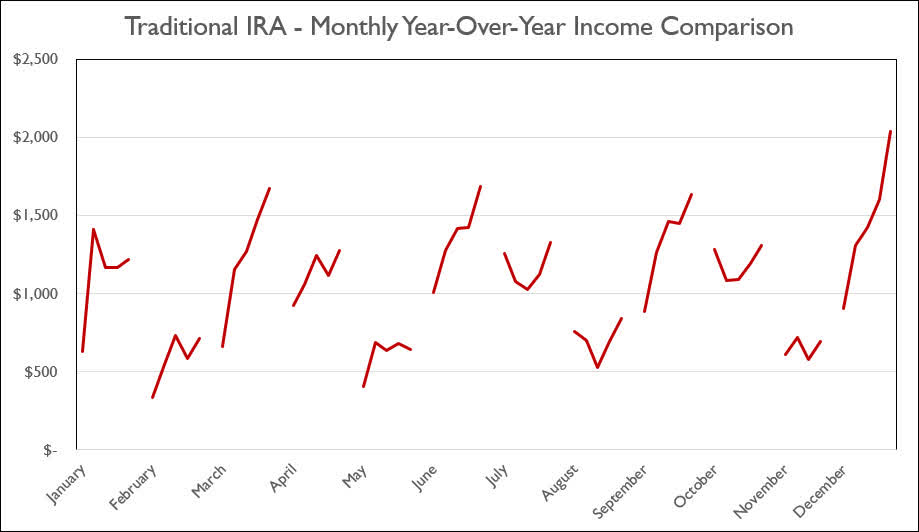

The last two graphs show how dividend income has increased, stayed the same, or decreased in each respective month on an annualized basis. Now that we are in our fifth year of tracking, the trend for each respective month of the year has begun to show interesting trends for when income increases year-over-year.

Traditional IRA - December 2022 - Annual Month Comparison (CDI)

{kind=link}

{kind=link}

Conclusion

John's portfolio performed even better than Jane's portfolio during this time and much of this was the result of having less exposure to the tech sector which performed the worst during this time. John has a significant amount of cash available and we will likely look to deploy it into Certificates because there isn't a lot that we would be confident deploying cash into at this point in time.

Certificates are also an excellent alternative for the retirement portfolio because interest is taxed at the income level so Traditional and Roth IRAs are a great place to collect that income. We have a certificate in the Taxable Account so it's good to be aware of the consequences of how the income is taxed and what tax bracket applies.

December Articles

I have included the links for John and Jane's Taxable Account and Jane's Retirement Account articles for the month of December below.

The Retirees' Dividend Portfolio: John And Jane's December Taxable Account Update

The Retiree's Dividend Portfolio, Jane's December Update: Index-Beating Year-End Results

Article Format: Let me know what you think about the format (what you like or dislike) by commenting. I appreciate all forms of criticism and would love to hear what I can do to make the articles more useful for you!

In John's Traditional and Roth IRAs, he is currently long the following mentioned in this article: AFC Gamma ( AFCG ), Aflac ( AFL ), Apple Hospitality REIT ( APLE ), Avista ( AVA ), BP plc ( BP ), Brixmor Property Group ( BRX ), Crown Castle ( CCI ), Canadian Utilities ( OTCPK:CDUAF ), Chatham Lodging Trust ( CLDT ), Chevron ( CVX ), CSX ( CSX ), Dominion Energy ( D ), Deere ( DE ), Digital Realty Preferred Series J ( DLR.PJ ), Duke Energy ( DUK ), Eaton Vance Floating-Rate Advantage Fund ( EAFAX ), EPR Properties ( EPR ), EPR Properties Preferred Series G ( EPR.PG ), Healthcare Trust of America ( HTIA ), Iron Mountain ( IRM ), Kinder Morgan ( KMI ), Kite Realty Group ( KRG ), Lowe's ( LOW ), Main Street Capital ( MAIN ), Masco ( MAS ), Altria ( MO ), New Residential Investment Corp. Preferred Series B (NRZ.PB), Realty Income ( O ), Oshkosh ( OSK ), Occidental Petroleum Corp. ( OXY ), Bank OZK ( OZK ), Bank OZK Preferred Series A ( OZKAP ), PacWest Bancorp ( PACW ), PepsiCo ( PEP ), iShares Preferred and Income Securities ETF ( PFF ), VanEck Vectors Preferred Securities ex Financials ETF ( PFXF ), Pinnacle West ( PNW ), PIMCO Income Fund Class A ( PONAX ), Nuveen Nasdaq 100 Dynamic Overwrite Fund ( QQQX ), Global X Funds Nasdaq 100 Covered Call ETF ( QYLD ), STAG Industrial ( STAG ), Sun Communities ( SUI ), Southwest Gas ( SWX ), AT&T ( T ), Toronto-Dominion Bank ( TD ), Truist Financial ( TFC ), T. Rowe Price ( TROW ), Cohen & Steers Infrastructure Fund ( UTF ), Valero ( VLO ), Umpqua Holdings ( UMPQ ), Ventas ( VTR ), WestRock ( WRK ), Warner Bros. Discovery ( WBD ), and W. P. Carey ( WPC ).

For further details see:

The Retiree's Dividend Portfolio, John's December Update: Outperformed The Major Indexes In 2022