USMC - The Rising Risk Of Deflation

2023-04-05 12:51:31 ET

Summary

- Deflation, not inflation is the real risk to the US Economy.

- The negative correlation between stocks and bonds demonstrates the bullish backdrop for fixed income especially at times of market stress.

- In this environment fixed income securities are providing investors with potential capital preservation, competitive yields and opportunities for capital gains.

Monetary Policy and the Path of Rates

On March 22nd, The Fed decided to continue to raise rates a quarter of a point while changing guidance from “ongoing increases” to “some additional policy firming may be appropriate,” and reiterated their data dependency. Chairman Powell in the press conference also reiterated the safety of the banking system.

I believe we are likely to see one more rate hike before the Fed pauses and allows the lags in monetary policy, and the tightening of credit brought on by this stress in the banking system, to continue to tighten financial conditions to move inflation toward the 2% target with the freedom to raise rates further if it sees any acceleration in inflationary pressure. Time will tell if this will be enough to accomplish the Fed's goal or if further rate hikes will be necessary. The Bank of England also raised rates 0.25% as did the Norges Bank in Sweden citing the risks of inflation, so inflation continues to be a global concern.

Current expectations in the market are for significant rate cuts toward the end of this year. However, Blackrock has stated they do not see rate cuts this year.

“We don’t see rate cuts this year – that’s the old playbook when central banks would rush to rescue the economy as recession hit,” the strategists said. “We see a new, more nuanced phase of curbing inflation ahead: less fighting but still no rate cuts.”

Chairman Powell has unequivocally stated rate cuts are not in the cards based on the current data. However, the Chairman's own preferred gauge of recession risk, is flashing red.

“Frankly, there’s good research by staff in the Federal Reserve system that really says to look at the short — the first 18 months — of the yield curve. That’s really what has 100% of the explanatory power of the yield curve. It makes sense. Because if it’s inverted, that means the Fed’s going to cut, which means the economy is weak.” — Fed Chair Powell on March 21, 2022

Bloomberg

Stocks have been rallying after the Fed's meeting on the thought that a Fed pivot is around the corner. However, history tells us that the majority of the decline in bear markets comes AFTER the Fed pivots. Investors should be cautious before buying into this rally, as stocks remain highly overvalued at current levels, based on a range of valuation methods, and have only become more so, as the Nasdaq has rallied in recent weeks.

"... since the 1960s, the Fed has repeatedly hiked interest rates to combat inflation. Notably, the stock market continues to perform when the Fed is lifting interest rates. Each time, that increase in the stock market, as the Fed was hiking rates, led investors to believe that this time was different. However, the Fed paused or pivoted from monetary accommodation as an economic recession or crisis was realized."

@TommyThornton

New Risks From Rising Rates Materialize

Looking at the zeitgeist in the market today, investors seem to believe all is clear. The sun is out, spring is here, and so is a new bull market. I have seen a number of pieces on SA, and elsewhere in financial media, calling for a new bull market. I respectfully demur, there is no evidence at this point that all is clear. In fact, the stress in the banking system may have come down from a fever pitch of bank runs, and constant worries about who will fail next, but the overall risk in the market is very real. The Wall Street Journal recently posted an article, Where Financial Risk Lies in 12 Charts that demonstrates we are just beginning to feel the pain from the rapid rise in interest rates.

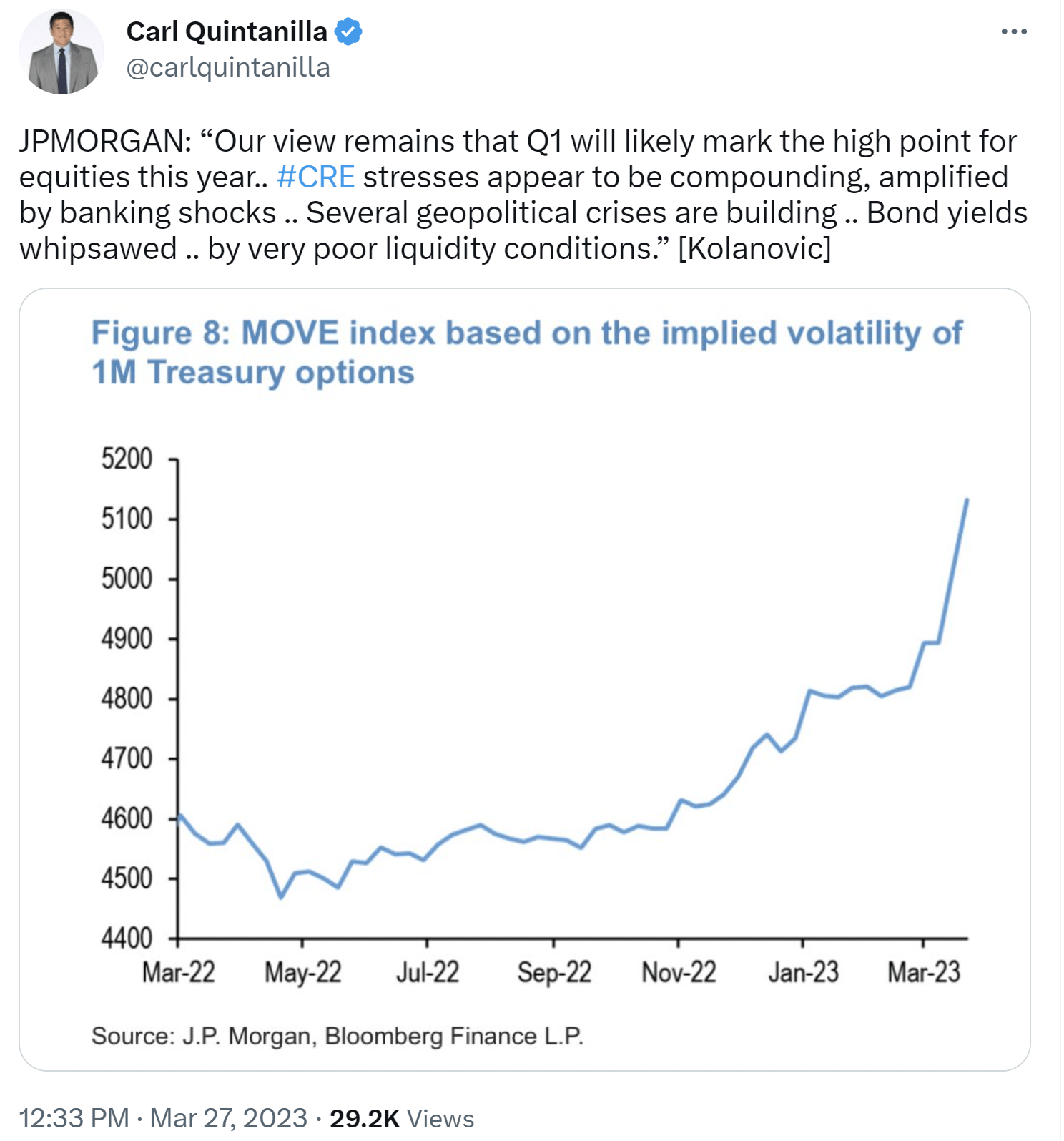

Risks Building in CRE

The risks in commercial real estate are also rising, as Dubravko Lakos-Bujas and the team at JPMorgan stated.

“Though office CRE has been in a multiyear decline, pressures are now intensifying from higher rates, hedging costs, declining property prices, business cycle slowdown, and secular demand disruption (e.g., office vacancy of 13% and total availability of 16% are at [global financial crisis] level)...The banking shocks should only amplify these pressures and could complicate the debt roll given that sizeable CMBS office loan maturities are coming due in 2023-2024...While options remain for borrowers/lenders to seek modifications (e.g., extend loan terms to avoid flood of distressed sales), a string of recent defaults should be interpreted more as an opening salvo as opposed to a one-off event...”

Marko Kolanovic, also of JPMorgan put out a note, reiterating his bearish stance on equities.

{kind=link}

I continue to be bearish over the next 12 months for risk assets, but in the short run, I could see the S&P 500 moving up towards 4,200 accompanied by a move higher in yield, lower in price for 30-year Treasuries. In my view, investors should take any move up in the S&P 500 to reduce risk assets, including high yield credit exposure, and add to their holdings of U.S. Treasury securities as rates backup, after a historic move.

Deflationary Risk Rising

"In other words, given that money supply growth is now even lower there is now certainly a risk of DEFLATION in the U.S. at some point in 2024-2025." -Lars Christensen, The Market Monetarist

Kelly Evans at CNBC put out a very insightful note drawing on the work of Lars Christensen, discussing the notion of deflation being the real risk here. The warning is that the Fed has done too much already and is in danger of missing their target to the downside, stating:

the market is warning that the Fed is about to miss its inflation target-- to the downside . The breakevens now imply that inflation will average a mere 2.1 % over the next five years, barely above the Fed’s 2% target. The series reached as high as 3.5% last March, when the Fed had only just begun to hike, but has steadily declined since. Even the upward creep we saw over the past few months has now been decidedly reversed.

Similarly, consumers’ expectations of inflation have kept dropping. Their year-ahead inflation expectations are quickly reversing the Covid surge, falling to 3.8% on Friday (they’re always a little higher than the actual inflation rate). Five-to-ten year expectations dropped as well, to 2.8%. Last Friday we also saw another decline in the index of leading indicators --for the 11th month in a row--and the 6.5% year-on-year drop we are in has never happened outside of recessions.

I highly recommend all investors read this, as the argument is an alternative to many of the arguments we are hearing today about how the Fed needs to remain focused on inflation. Personally, I believe both can be true. Deflation is the longer-term risk; I have written about this for some time. However, the near-term risks of inflation are also real. The Fed needs to be sure inflation is moving towards target before it can make any meaningful change in monetary policy. Currently, inflationary expectations are declining, giving evidence to the contention that inflation was in fact transitory. Time will tell if the trend continues, or if further tightening is necessary.

Apollo

The Ominous Warning in the Collapse of M2

For the fifth time in 153-years an economic indicator is flashing red. I am speaking about the drastic fall in the M2 money supply. We know from Fishers Equation of Exchange, that GDP=M*V, with M being the money supply and V being velocity on M2. The drastic fall in M2 is a harbinger of things to come, namely, falling GDP. But what is really noteworthy is the dramatic fall in M2 from a historical context. The last time the Fed was raising rates and M2 fell at this rate was during the depression of 1921. What followed was double-digit unemployment and a steep economic contraction.

M2 (www.nasdaq.com/articles/for-only-the-5th-time-in-153-years-this-leading-economic-indicator-is-sending-a-terrifying)

If history is any guide, we are looking at a serious drawdown on the horizon. I believe the waterfall stage of this bear market could see the S&P 500 fall to my target of 3,000-3,200, representing a 20-25% decline from current levels, which when added to the previous year's decline of 25% should be a run of the mill 50% correction, which has been sorely needed to restore the equity risk premium.

I have written at length about the fact that this market is unlikely to see a single cathartic move lower that signals the end of the bear. Bear markets so often move in waves. In fact, in the 2000-2002 bear market, there were 16 double digit bear market rallies on the way to new lows. We are likely to continue to grind lower throughout 2023, even as some see the Fed cutting rates in the fourth quarter. I do not believe we are likely to see rate cuts this year, as a result of the Fed's ongoing war with inflation.

{kind=link}

JPMorgan's CEO Jaimie Dimon, in his annual letter to shareholders commented on the economy, and the possible outcomes from the inverted yield curve, and the immense stress we have seen on the banking system.

Today’s inverted yield curve implies that we are going into a recession. As someone once said, an inverted yield curve like this is “eight for eight” in predicting a recession in the next 12 months. However, it may not be true this time because of the enormous effect of QT. As previously stated, longer-term rates are not necessarily controlled by central banks, and it is possible that the inversion we see today is still driven by prior QE and not the dramatic change in supply and demand that is going to take place in the future... Higher interest rates will obviously have an important impact, not just for banks but for some of those who borrow on a floating rate or those who have to refinance in a higher rate environment. If this tide goes out, you should assume that it will expose additional weaknesses in the economy."

It is clear that while Mr. Dimon goes on to discuss the opportunities for his company, he also sees storms on the horizon. Bears have long been perplexed as to how markets can continue on a seemingly irrational path higher, even as the world around them continues to experience significant earthquakes.

He gives rise to the idea that the Fed may have changed the structure of the macroeconomy in their reaction function and the tools employed to deal with crises. This is an interesting point that deserves further exploration. The yield curve has been inverted for some time however, no recession has materialized. Are we wrong to be bearish, and is the effect of the Feds extraordinary monetary policy changing macroeconomics as we know it? I will explore this in my next piece, Are we Wrong to be Bearish ?

Conclusion

Any decline in yields is not a sign that the FED is about to bring a punch bowl... but rather a sign that recession probability has increased... we believe stocks are set to weaken for the remainder of the year and one should be [underweight] from here.” -Marko Kolanovic, JP Morgan

Deflation continues to be the real risk to the economy long term. The question remains whether the Fed has done enough to deal with the near-term inflationary pressures or whether further accommodation is necessary. The Fed has done a poor job of forecasting and is likely to tighten too far leading to undesirable outcomes.

Bob Michele, Chief Investment Officer, and Head of Global Fixed Income at JPMorgan stated in his March commentary:

"Recession remains our base case and was kept unchanged at 60% . The central banks are in all-out inflation-fighting mode. Rates will go as high as necessary and ultimately trigger the painful adjustment we all hoped would be avoided... After a year of torture from negative convexity (notably, duration extension), the absence of bank buying and the removal of Fed support, the market looks washed out. A government bond with yield should be the ideal investment headed into a contraction." (Emphasis mine)

It is clear in times of market stress; the negative correlation of US Government bonds has been a profitable choice for investors. As I stated in my last piece , we are increasingly headed toward a Minsky Moment. This is not the time for investors to take on additional equity risk. Instead, I favor government bonds across the curve, particularly long duration. I believe investors should use any backup in rates to add to these positions.

There will come a time again for investors to deploy capital towards risk assets, but the current risk/reward is skewed to the downside, and with high yields in high quality paper, it seems a gift to lock in these rates. I see the entire curve flattening and echo the prediction of JPMorgan's Bob Michele who said the entire curve is going down to 3% minimum. The bond bull market continues.

For further details see:

The Rising Risk Of Deflation