ENB:CC - The RPD Portfolio Across 2023: Still Winning

2024-01-08 06:30:00 ET

Summary

- This article shares how my retirement income has become increasingly secure over my four years of retirement to date.

- My strategy focuses on dividends and on investing in companies I understand well.

- The article also discusses how I seek to grow dividends and portfolio value with time.

My retirement has now lasted four years. It started five years before I had planned, thanks to health issues. (Youngsters: this could happen to you too!)

This article will share my progress with my investments. The important aspect is that my retirement income is becoming progressively more secure.

The unimportant aspect, still fun, is outperforming the S&P 500 over time. Considering my approach, such outperformance should happen when the S&P 500 has flat periods. If it happens when the index soars, then either I was lucky or good. You can decide about that.

Over the two years before retirement, I had developed a retirement income plan. It was steeped in the total return thinking that does make sense for many people. Plan to sell down your portfolio over time to support spending, relying on total returns to retain enough value that it outlives you.

Value investing - buy low, sell high - soon had more appeal. Then events immediately put me through the test.

It was certainly nerve-wracking to see my portfolio drop more than 50% over the next three months. But, even as a kid, I have never been one to panic.

My goal in 2020 was to make one good investment decision after another. Beyond the unavoidable paper losses related to the pandemic, I realized some losses while working my way out of various mistakes or poor decisions.

It feels as though those losses led to learning. Time may tell.

By the next summer, a friend helped me understand that I had come to see myself as an Investor . That is not a self-description to be taken lightly, but after reflection, I embraced it.

My investing paid off a bit in late 2020, with the arrival of the covid vaccine. Then in 2021, the portfolio gained 50%.

Considering what I invested in, this was amazing. Placing it in context was the job of my article at the end of that year.

My investing style also evolved a lot over those first two years, from widely diversified to quite concentrated. My article on portfolio evolution discussed the process of transition.

I recommend that article for its discussion of why an investor might want to take various approaches. One size definitely does not fit all investors.

After that, of course, the bull market ended, interest rates skyrocketed, and life got tough in the markets throughout 2022. I was proud of surviving with minimal losses, as described in A Year of Successful Defense .

The year 2023 has been challenging in my areas of focus, which are REITs and energy. They are both niche markets with aspects not so readily analyzed (especially by computers), providing opportunities for mispricing and outsized gains.

Despite the challenges of 2023, my net, after-tax gains reached new highs several times. The 2023 increase in portfolio value at year-end is 22%. The dividend yield on the entire value is 5.6%.

This article sets the context, shows some details, and later makes some comparisons.

Quantifying the Threats

Four years ago my challenge was to increase my assets enough that supporting my projected spending would be more likely to succeed long-term. By a year ago that goal was met and my focus had turned more strongly to what could go wrong with my plans.

One can invent any number of negative scenarios. My preference is to base the assessment of risks on actual past behavior as opposed to theoretical disaster scenarios.

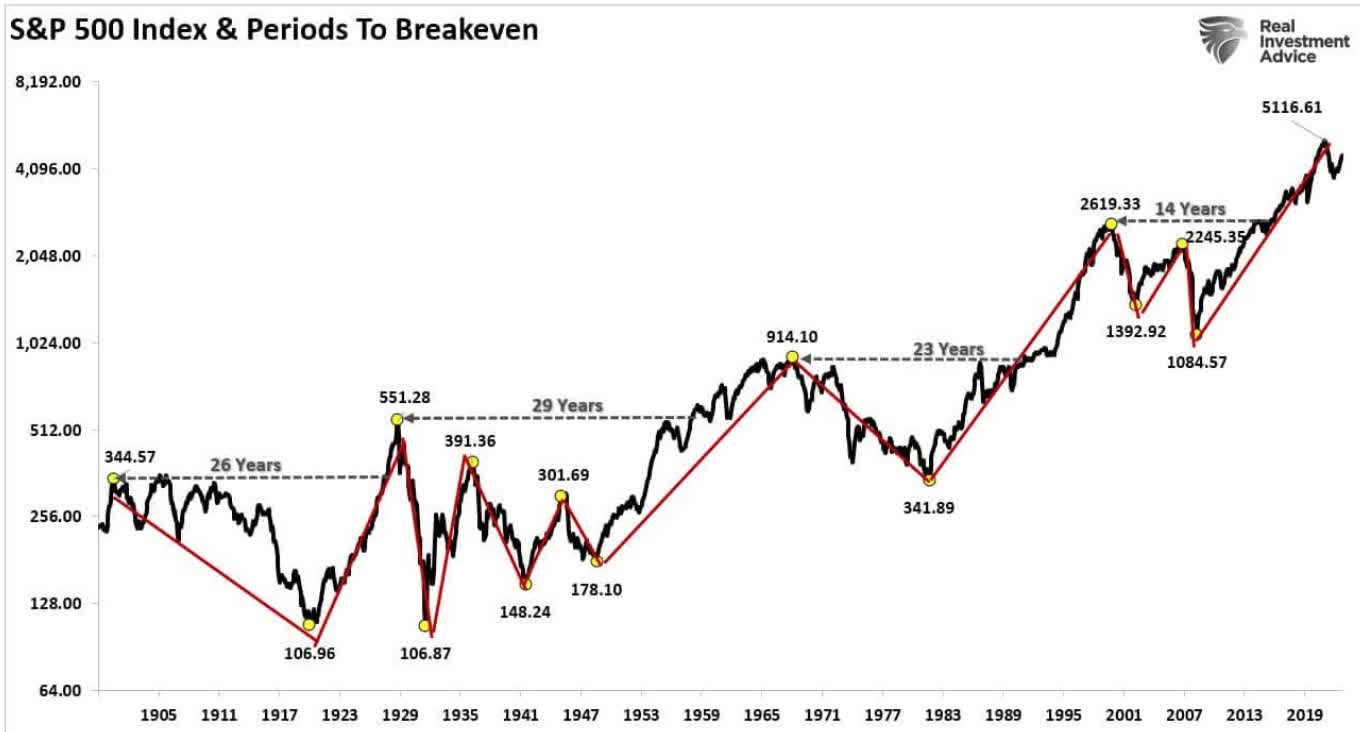

Let's look at a couple of scary plots. This one is from Lance Roberts:

{kind=link}

Suppose you retired in 1967, planning to draw 4% of your (all-stock) portfolio and increase the amount with inflation. If you stuck to that plan and had a typical dividend yield of 4%, then you ran out of money in 1981. Today dividend yields are lower so a strategy based on holding the S&P 500 would work less well.

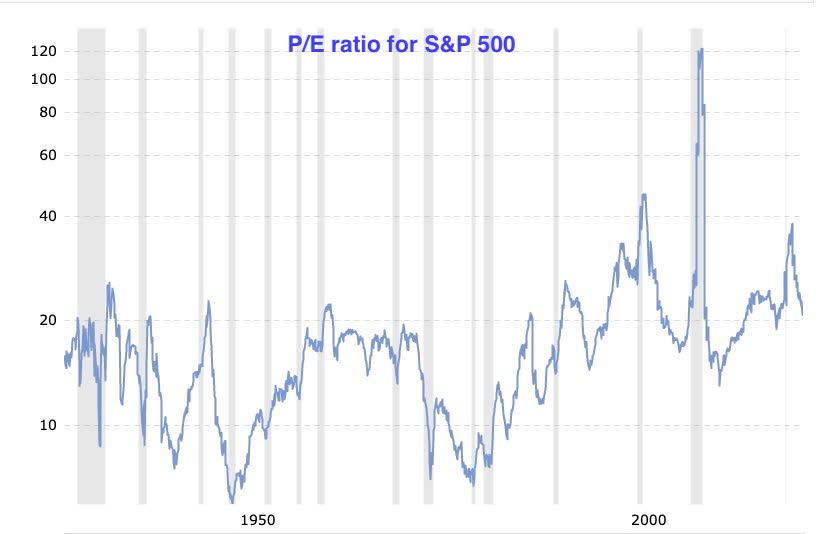

Another way to see the history is to look at P/E ratios. This is from Macrotrends:

{kind=link}

During this century the ratio has mostly been above 20x. But there were two periods since 1930 when it dropped well below 10x. So if you think earnings increases will always save your portfolio value then you are, well, wrong.

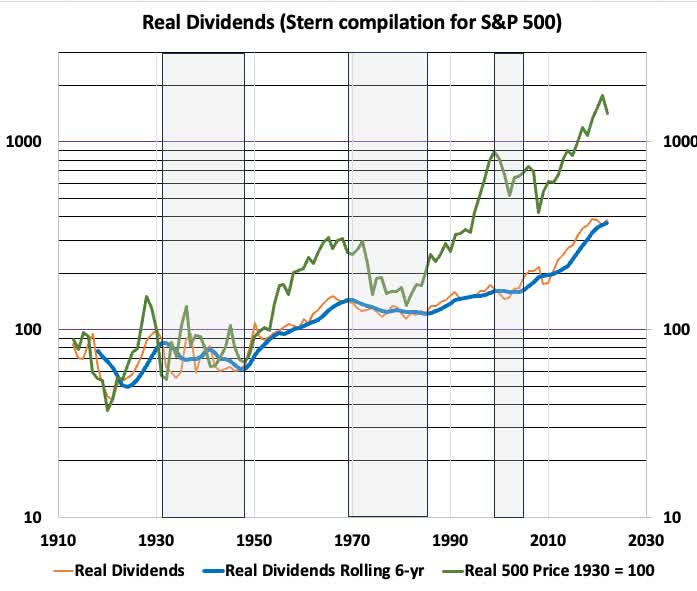

In my view the solution here is dividends. Take a look at this, based on my calculations using the compilations by Prof. Stern at NYU:

{kind=link}

The areas shaded gray show periods when the real value of the dividends from the S&P 500 decreased. Notice that they did not decrease much and decreased far less than the real index value. During those periods, a retirement strategy based on those dividends would have been far more successful than one based on total returns.

Now prior to about 1960 one could get good yields from the index overall. But between taxation, inflation, and the emergence of stock buybacks that is no longer possible.

You can see above that the S&P 500 was down more than 2x in real value during the 2000s.

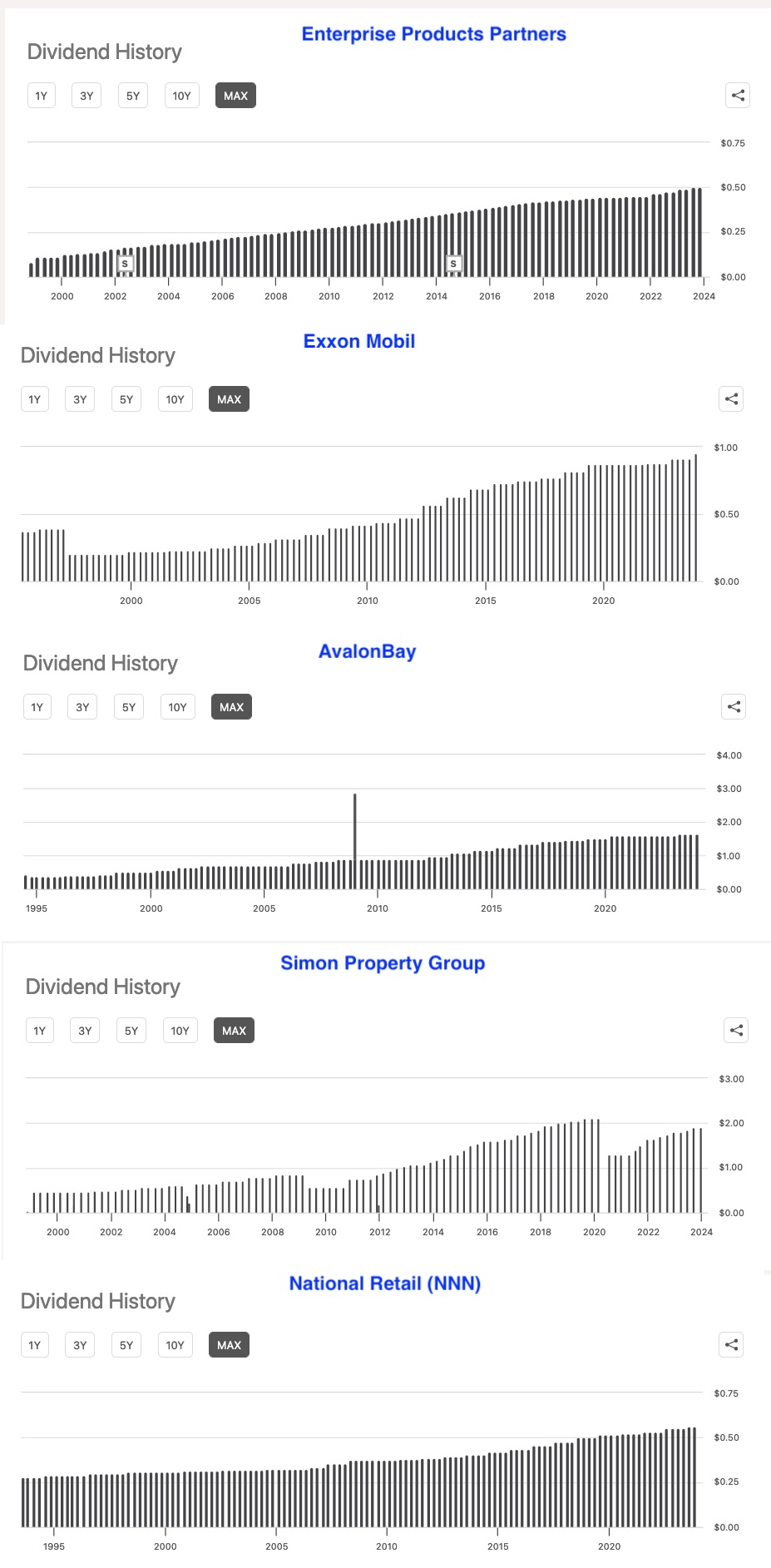

Today to get reasonable yields you have to look to dividends from companies holding hard assets and from companies that are required to pay out a large part of earnings. The next graphic shows the dividends this century from some such firms. They all held up and mostly increased across the 2000s, growing more than the price inflation of 25%.

{kind=link}

Thinking about these things led me to progressively increase my focus on dividends. This was described in a couple of articles . It also led me to realize that investing in growth positions makes little sense for me personally.

I discussed that here . Accepting a lower dividend in return for higher growth pays off in cumulative income mainly in the third decade of compounding and beyond. My timescale as an investor is much shorter than that.

What makes sense for me is to hold mostly income positions, within my "Income Bucket," along with some upside positions in my "Upside Bucket." The idea is that the upside positions are significantly undervalued by the market and have catalysts likely to prompt a revaluation within a year or two. I settled on personal target allocations of 80% income and 20% upside.

My preference in the Upside Bucket is for target upsides near 50% so that a 2% to 4% position grows the portfolio by 1% to 2%. If you can manage that even 5 times a year the impact becomes noticeable.

Even within the Income Bucket, though, I can work to grow portfolio value across cycles. The approach is to spread out the holdings during bull markets and concentrate them on the most undervalued stocks during bears.

Closed Positions

I closed positions for several reasons during 2023, detailed in the next few tables. In all cases, the REITs are in cells shaded green, the MegaCap Techs in cells shaded blue, energy positions are shaded gold, and what I think of as storage positions are in pink.

My decision to move out of growth positions led me to close 8 of them. Of course, closing out the MegaCap Techs turned out to cost me some gains later in the year, but second-guessing those things does no good. Overall those exits cost me 2% of my portfolio value.

RP Drake

I closed or trimmed some positions to take the gains. Two of these [KOS and CPPMF] had reached my price targets. In some other cases, I moved the money into another investment that better met my goals. And one company (Crestwood) got eaten by a bigger one. On net, these actions increased the portfolio value by 3%.

RP Drake

Unfortunately, my investing theses fell apart for Seritage Growth Properties (SRG) and for Clipper Realty (CLPR). The first, based on realized property sales, failed to live up to the initial value estimate. And on Clipper I had failed to do good enough forward modeling of the cash flows, which would have shown their abysmal liquidity situation.

RP Drake

Selling those two cost me 2%. I took no net loss on the two BDCs I used as places to store money while waiting for an opportunity. I had been using Ares Capital ( ARCC ) but switched to Oaktree Specialty Lending ( OCSL ) after deciding they would be better at defense.

So overall my closed positions were a net hit of 1% to portfolio value. I can live with that.

Next are my Energy and then REIT investments as of January 1, with some comments.

My Energy Investments

My goal these days is to generally write one deep article per year about each of my holdings, with a few exceptions. These articles are my investment reports to myself, shared with readers. More articles may be needed if events lead me to want to re-examine some holdings in less than a year.

The exceptions may be some midstream energy firms, especially big integrated ones. There seems little point in trying to explain those in only a couple thousand words.

But sometimes the really dumb things other authors or commenters say do motivate me to write something. It never ceases to amaze me how little understanding many authors demonstrate of the things they invest in.

My portfolio includes six midstream energy firms. My requirements for such firms include an investment-grade balance sheet, diverse revenue sources, limited recontracting risk, potential for growth, and strong dividend returns. A few comments about these holdings:

- To get a good overview of Enterprise Products Partners ( EPD ), just thoughtfully read one of their outstanding investor presentations.

- There might be a little more use to doing an article on MPLX ( MPLX ), and perhaps that will happen. But the main point would be that most authors completely misrepresent the relative roles of oil and gas at that company.

- I might do articles on Enbridge ( ENB ) and TC Energy ( TRP ). If so, they would focus on aspects that concern or encourage me.

- An article on Western Midstream ( WES ) is likely at some point, as it would be good to understand them more deeply.

I do expect to write on my two upstream energy investments, as happened this year . These are Tourmaline (TRMLF) and Canadian Natural ( CNQ ). They both have strong balance sheets, very deep resources, low-end cost of production, and strong shareholder returns emphasizing dividends.

On top of those aspects, my involvement with Michael Boyd and members of his Investing Group benefits me in three ways. There are the data and coverage that Michael produces. And there are lots of continuing critical interactions about the energy space among knowledgeable investors.

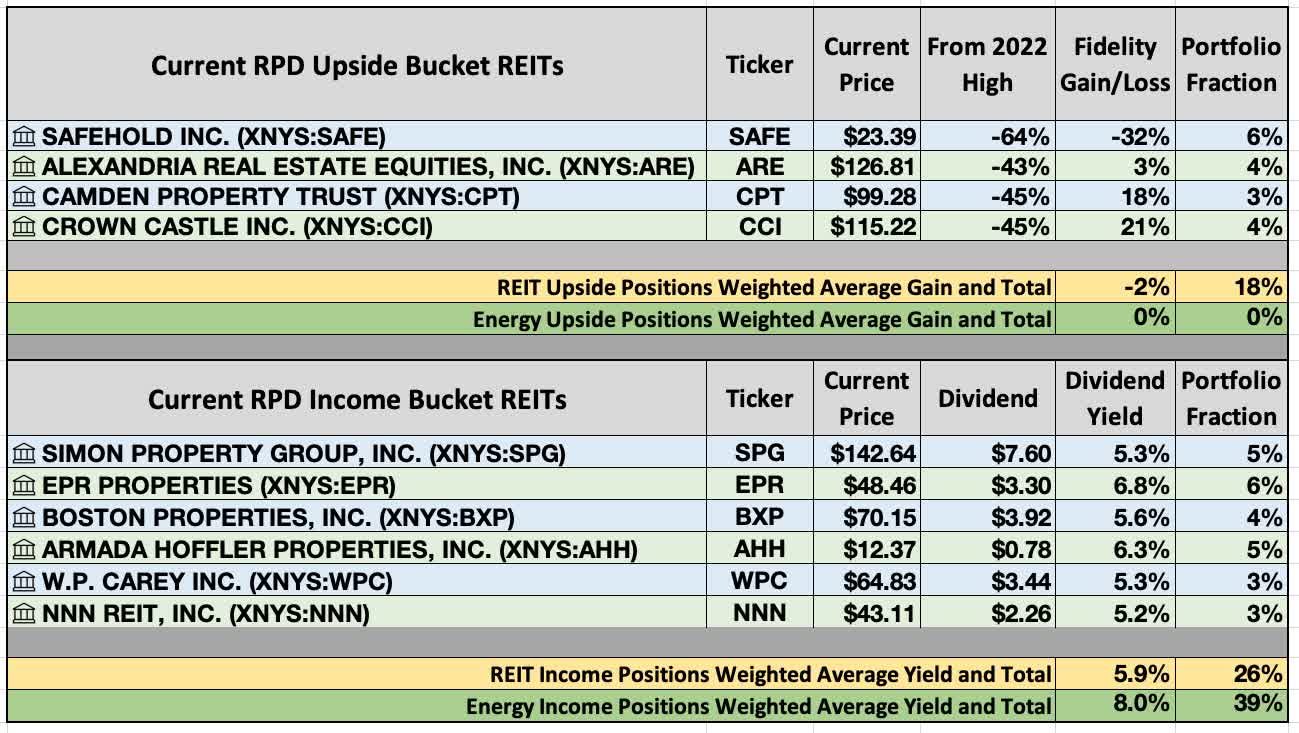

My current bottom line on energy positions is that they are all for income. They make up 39% of my portfolio. My projected dividend yield from those holdings for 2024 is 8%.

Beyond that, Michael's analysis or his chat room occasionally identifies stellar opportunities for upside. At the moment I have no upside positions in energy, but with the next big downward move in oil prices, some will pop up.

REIT Investments

My own analysis has driven my REIT investments for some years now. They also benefit from interactions with Jussi Askola and with the authors and members of his Investing Group.

My requirements for REIT investments emphasize safety. My expectations include: good balance sheets, clear and complete disclosures, a focus on real estate, and a business model supporting growth under all market valuations.

As of year-end, here are my current REIT holdings. The table shows information related to gain and loss for the upside positions and related to dividends for the income positions.

{kind=link}

The Upside Bucket only recently got back near my target fraction, having shrunk when some energy investments reached their price targets. But the final phase of the interest-rate blowout pushed both Camden Property ( CPT ) and Crown Castle ( CCI ) down to levels that met my requirements so I hold them now.

This paid off so far; overall my newer positions have nearly overcome my paper losses in Safehold ( SAFE ). And with those all having at least 2.3x upside to their 2022 highs, my view is that another 30% to 50% from here is a conservative expectation.

The Income Bucket expanded from four to six REITs across 2023. In addition, Spirit Realty Capital ( SRC ) agreed to be bought out and I sold it.

Opportunities arose to split some positions without loss of quality or income. As valuations increase, my hope is to do more of that and to move some funds into "Storage" income positions. I have a little money there now.

Also not shown in the table is my decision last week to replace Boston Properties ( BXP ) with VICI Properties ( VICI ), each of which I wrote about last year. I realized a short-term gain of 30% in my Roth, almost completely replaced the income and ended up with income that should grow much more strongly.

Other Investments

The portfolio includes some illiquid investments, mostly via three private equity opportunities. I carry these at my book value.

It also includes a variable amount of the "storage" investments described above. Mostly I have used BDCs and tobacco companies for these.

Comparisons

My focus on investing has never been alpha. What I care about is securing retirement income and, ideally, a legacy.

With my approach, I expect my portfolio to underperform the S&P 500 during its hot periods. More importantly, though, I expect strong outperformance when the S&P 500 falls.

So far this has gone well. Here is a comparison of annual and cumulative total returns for the past 4 years for the RPD Portfolio, the S&P 500 ( SPY ), and the equal-weight S&P 500 ( RSP ).

RP Drake

Events in 2020 hit my areas of emphasis hard, which also let me end up in positions whose upside was realized in 2021. Plus I lost money while "finding my feet."

Since then, though, the RPD Portfolio has beaten the two indices in five of six possible comparisons. It fell a few percent short of the gain of SPY for 2023.

The cumulative return of 63% over four years solidly beats that of the SPY and trounces that of the RSP. Well, this is what value investing is supposed to do. Perhaps I am good at it. Or perhaps just serially lucky so far.

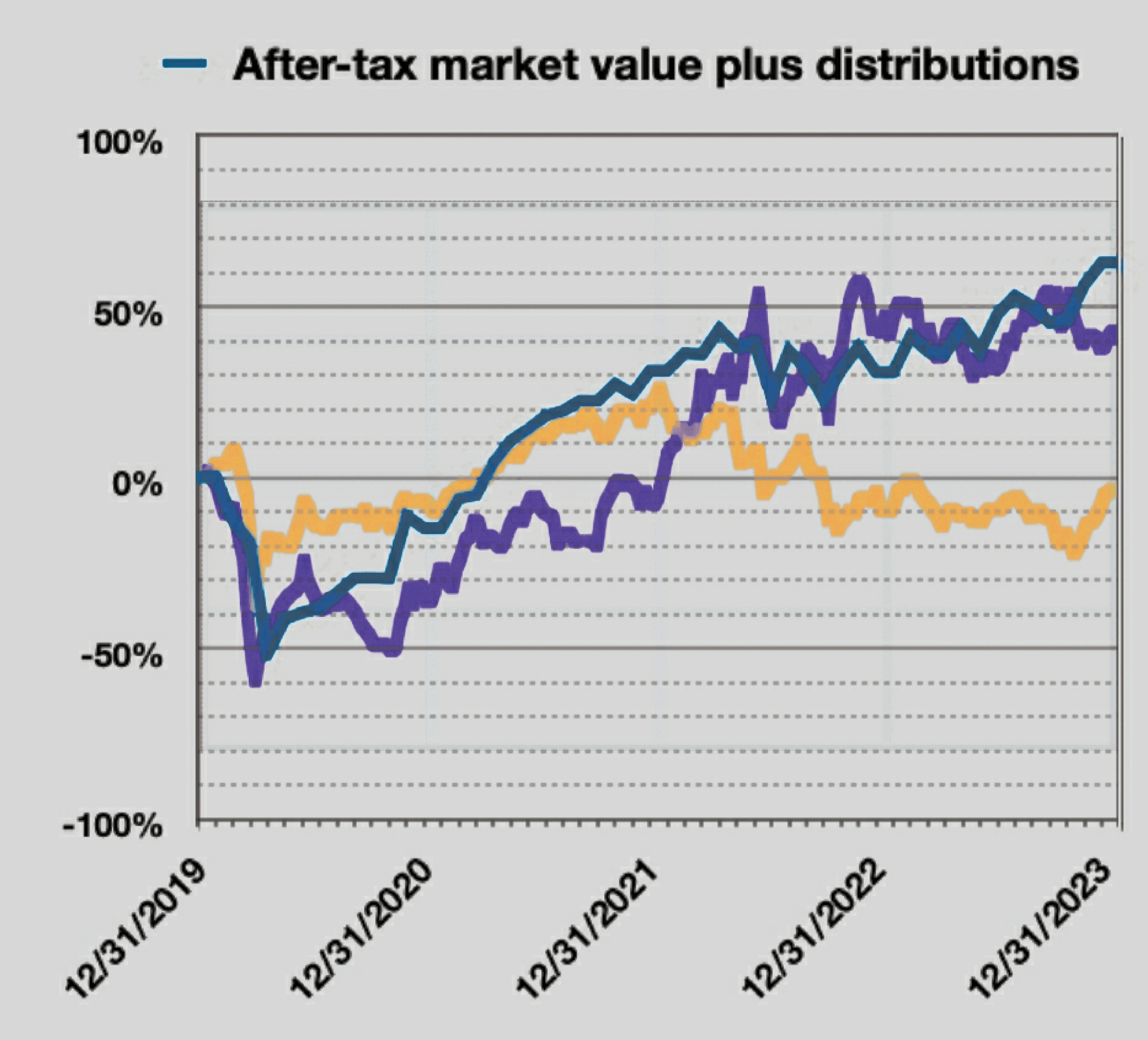

A more direct comparison is to compare the trajectory of my gains with those of the (cap-weighted) REIT markets and energy markets. We see that here. Dark blue is the RPD Portfolio, purple is the Energy Select Sector ETF ( XLE ), and orange is the Vanguard Real Estate ETF ( VNQ ).

{kind=link}

You can see the pandemic crash in 2020 and the gradual recovery. In 2021 I emphasized REITs, which really powered the upward move. But by late 2021 and through half of 2022 it was energy that was the big mover.

Not long ago the XLE gain since 2019 was above that of my portfolio. But the year-end surge in REITs powered my portfolio to higher net, 4-year gains.

My view today is that REITs are likely to lead the charge through much of 2024. We will see.

Let me emphasize this. If I wasted my thinking time on the nonsense that so many investors spend time and energy on, my portfolio would not be where it is. Focus on the important stuff, folks.

Despite all the advances in my thinking and the evolution of my approach, one basic goal remains: to make good investment decisions, one at a time.

For further details see:

The RPD Portfolio Across 2023: Still Winning