QVMS - The S&P 500 Faces An Entirely New Set Of Problems

- The S&P 500 is falling sharply after the latest S&P Global PMI shows the services sector contracted in July.

- This is a leading indicator to a contraction in earnings.

- This is likely to push the S&P 500 PE Ratio to around 14.

Stocks don't always do what you want, when you want them to, but that's how it goes sometimes. The rally this past week for the S&P 500 is probably approaching its end ahead of next week's Fed meeting.

The economic data that may have killed this rally, which should have been a non-event, showed the US economy had slowed dramatically in July. S&P Global US Composite PMI was at 47.5 in July and well below the 52.7 that was expected. The manufacturing sector was stronger than expected at 52.3 vs. estimates for 52. But the big miss was on the services side, at 47, which missed estimates of 52.7.

{kind=link}

The miss is somewhat concerning and could signify what's coming in early August when the ISM services PMI is released. While the S&P global and ISM surveys don't align perfectly, the trend and themes are the same. Today's S&P Global report showed the US services sector is now in contraction, and while it doesn't have to mean recession, it suggests that earnings for the S&P 500 are likely to take a big hit.

An Earnings Hit

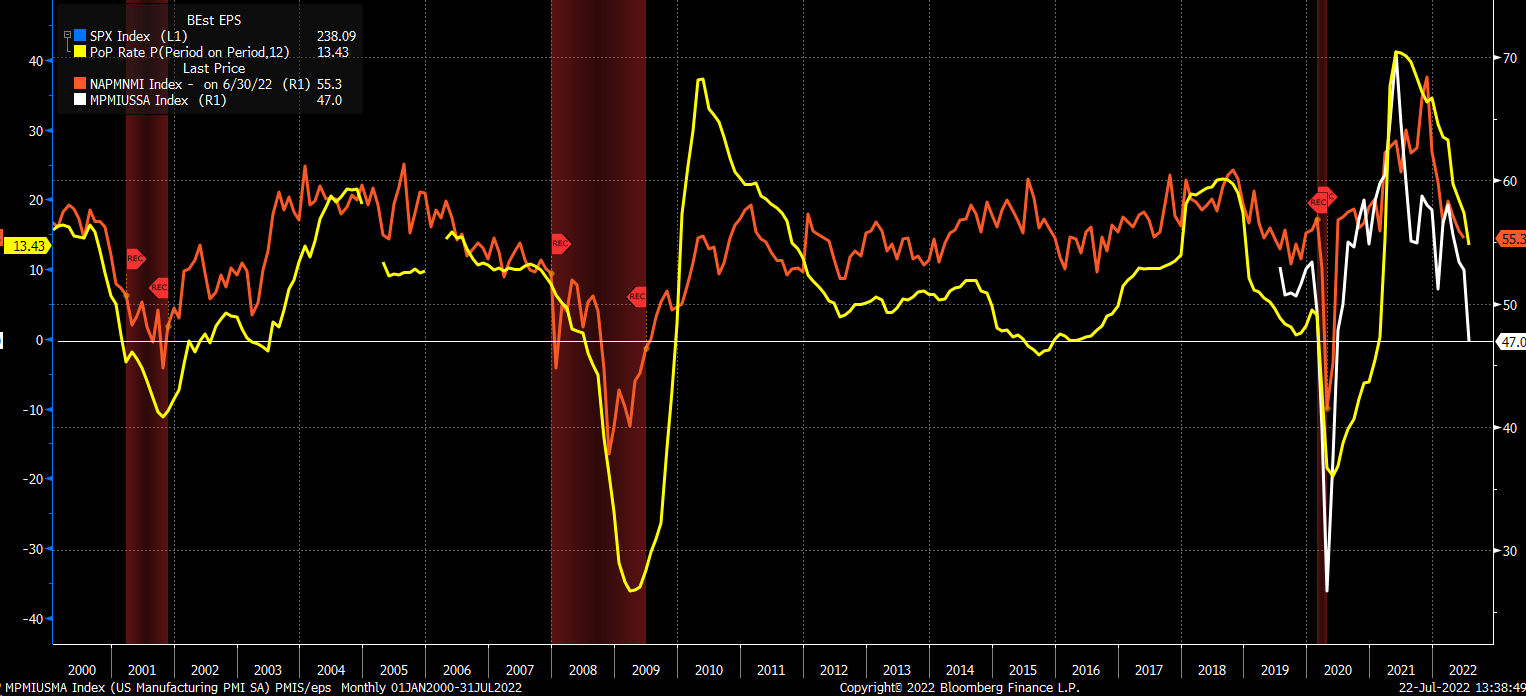

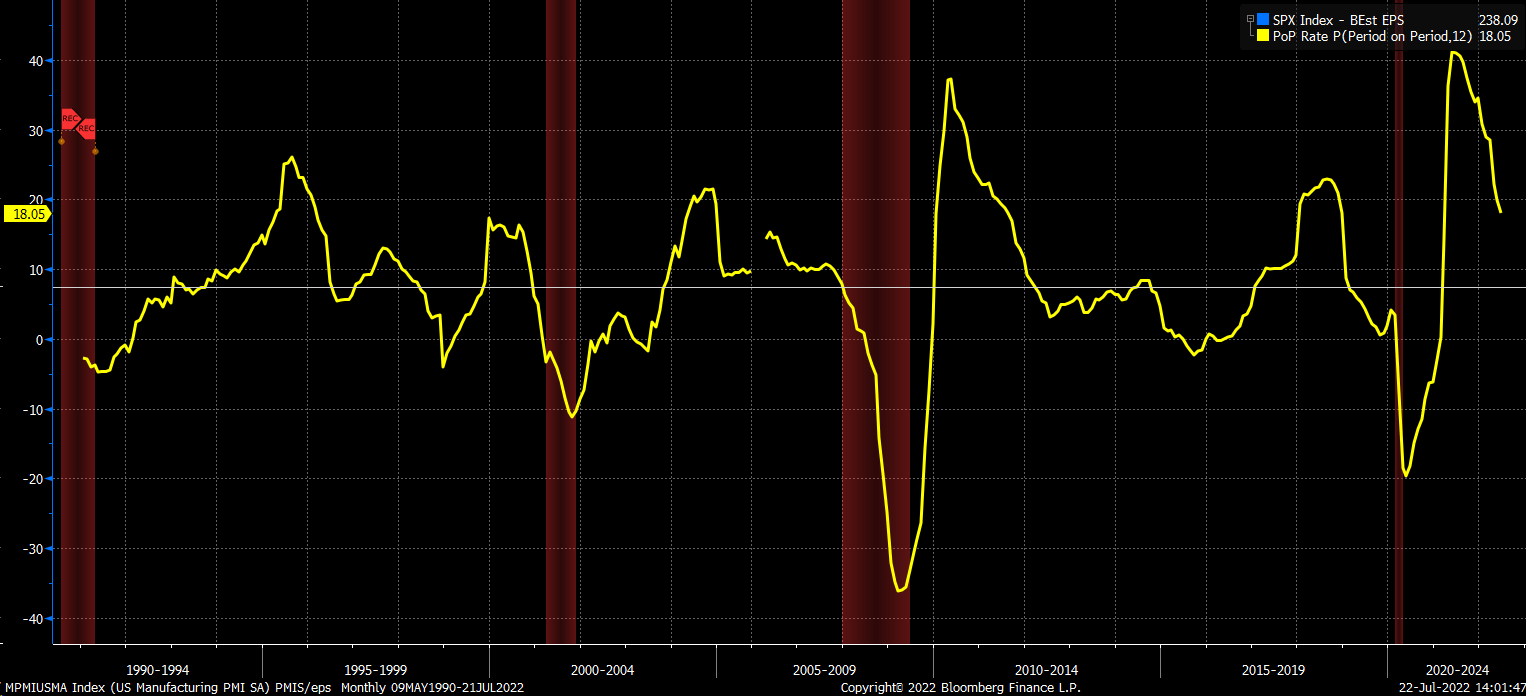

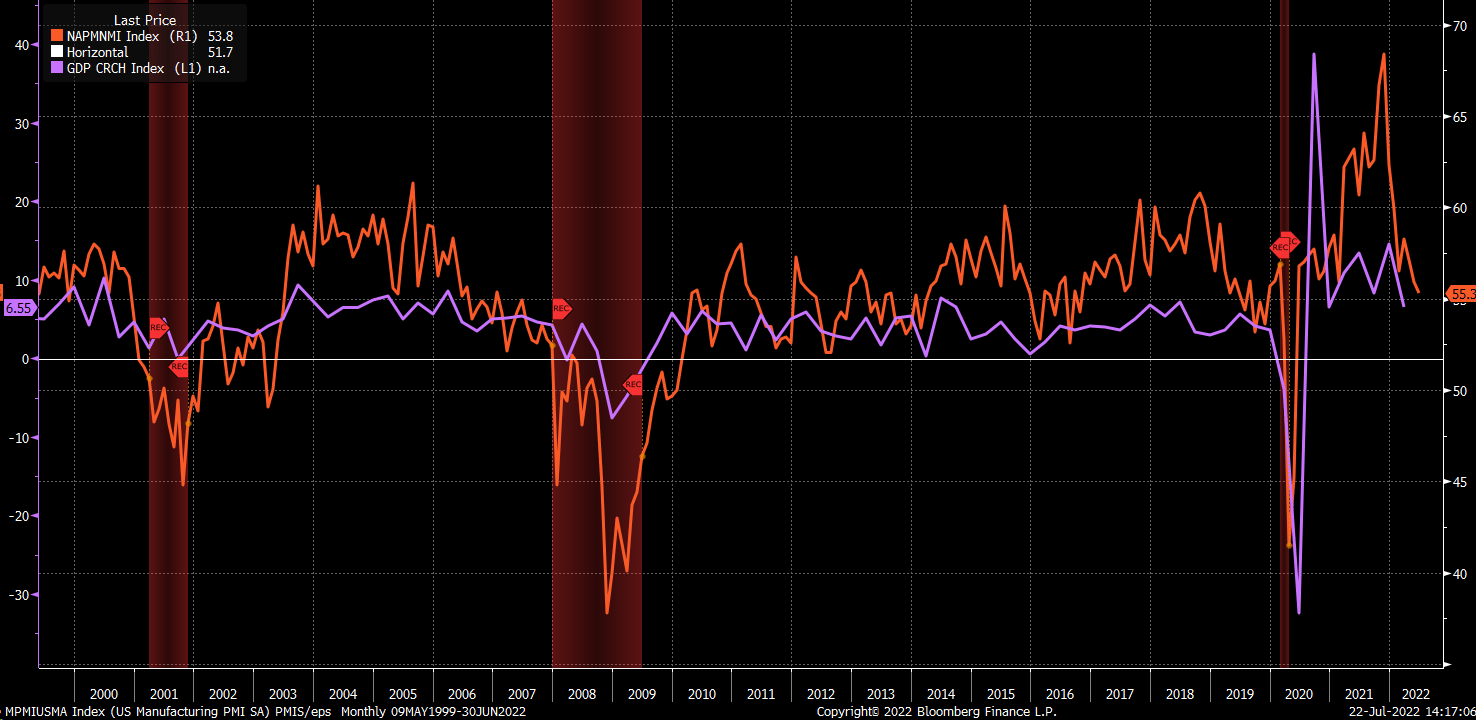

The 12-month blend forward earnings estimates for the S&P 500 growth rate tend to ebb and flow like that of an oscillator, and when overlayed with changes in the ISM Service index, it tells a scary tale. Because if today's report is a forecast for what the ISM services index will look like, then earnings for the S&P 500 over the next 12 months are likely to turn negative.

{kind=link}

While earnings estimates on a blended 12-month forward basis haven't started to fall yet, they have undoubtedly flat-lined and stopped rising. Over the next couple of months, we will likely find out if earnings will turn lower as the US economy continues to slow. If the services sector has moved into contraction and perhaps is even signaling a recession, as noted by today's data, those earnings estimates will start coming down soon.

{kind=link}

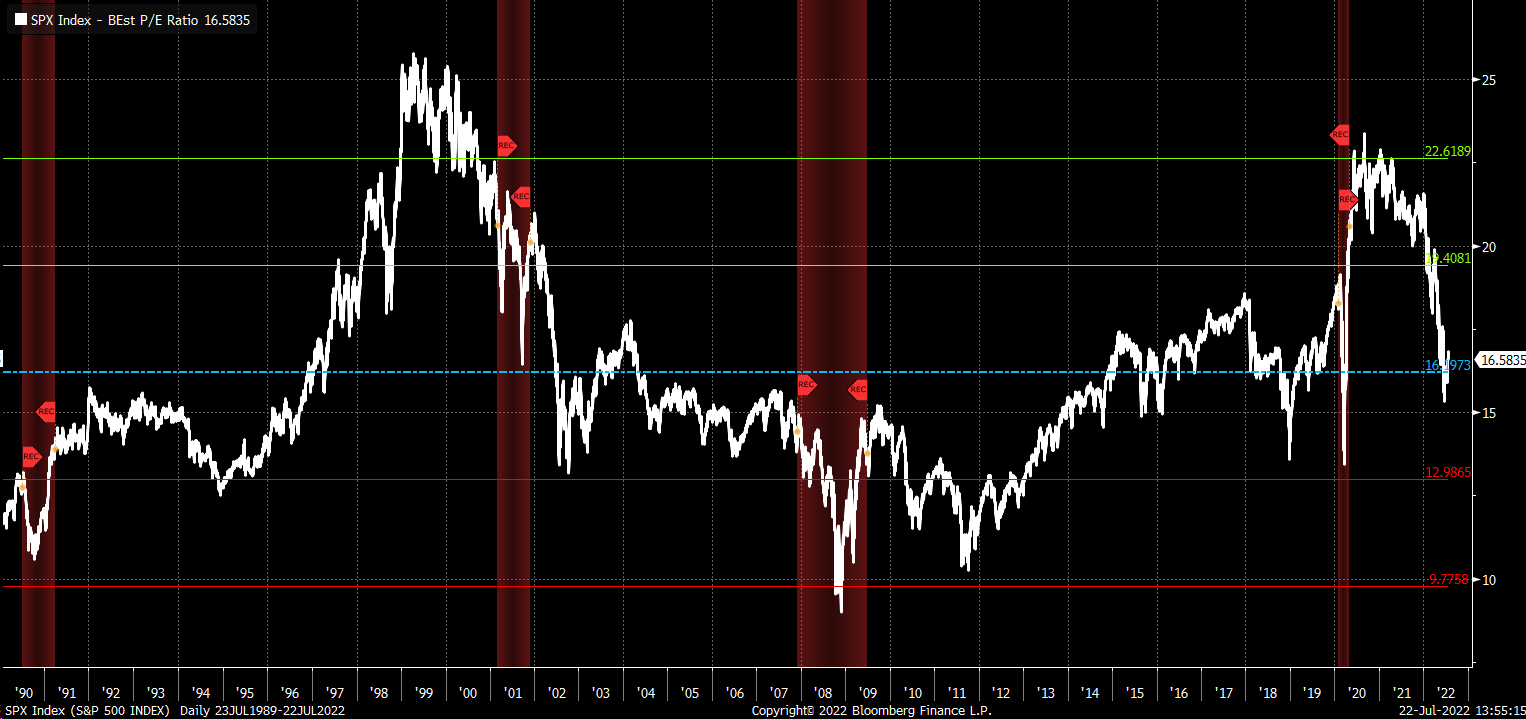

Declining earnings estimates should lead to further multiple compression. While the PE ratio has fallen for the S&P 500 in recent weeks, it has fallen back to average values and does not reflect the risk of earnings falling further. It would suggest that there's still further multiple compression for the market as it tries to discount future earnings.

PE Contraction

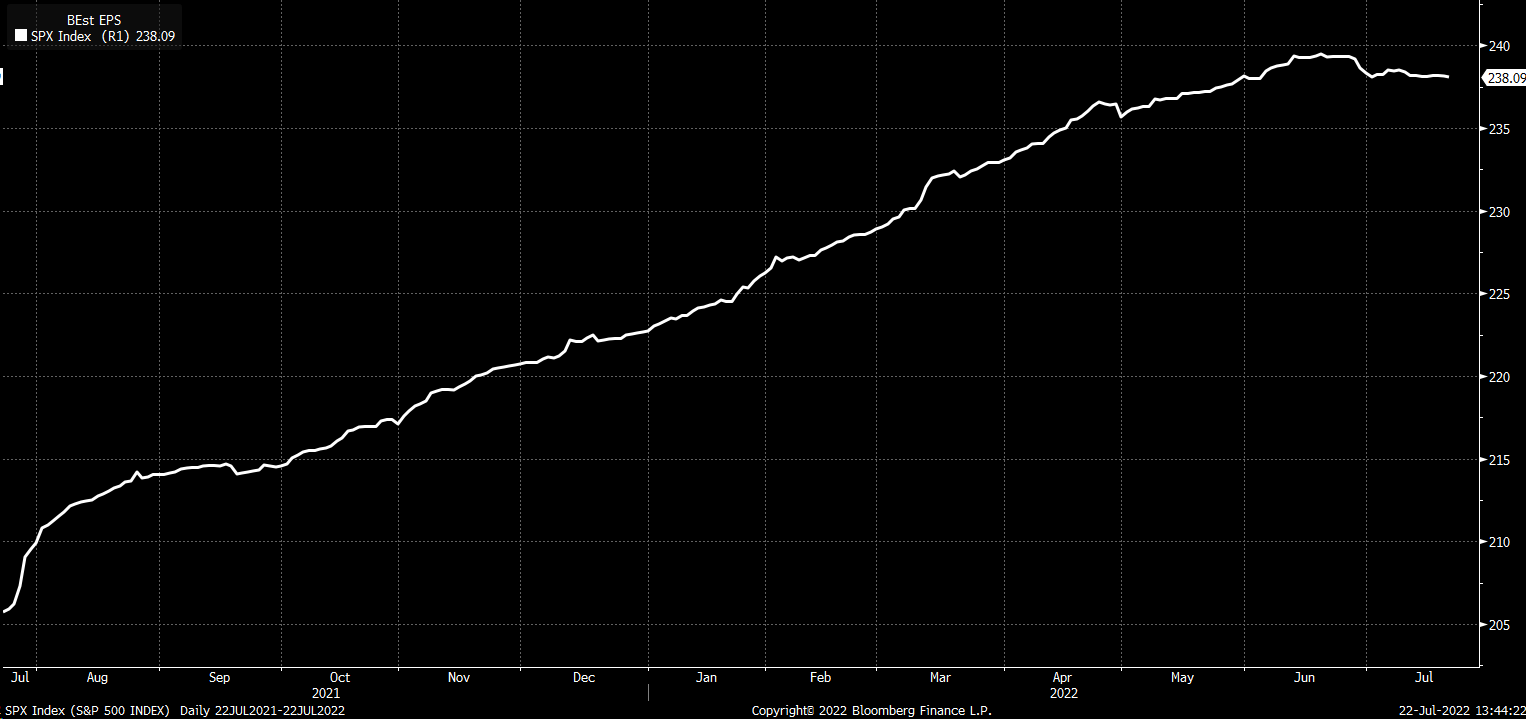

Based on history, that bottom PE range should be around 13 to 14, assuming this recession doesn't mimic 2008 and 2009, which I think is unlikely. But at 13 times earnings estimates of $238.09, the S&P 500 would be worth around 3,100, and 14 times estimates, the index would be around 3,300.

{kind=link}

A decline in the PE ratio to 14 and an S&P 500 at 3,300 would imply an earnings decline of around 13%. This would assume that the PE ratio climbs back to the historical average of approximately 16. That type of decline in earnings would be not that dissimilar to the decline in earnings estimates during the 1990 and 2001 recession, which were between 5% and 10%.

{kind=link}

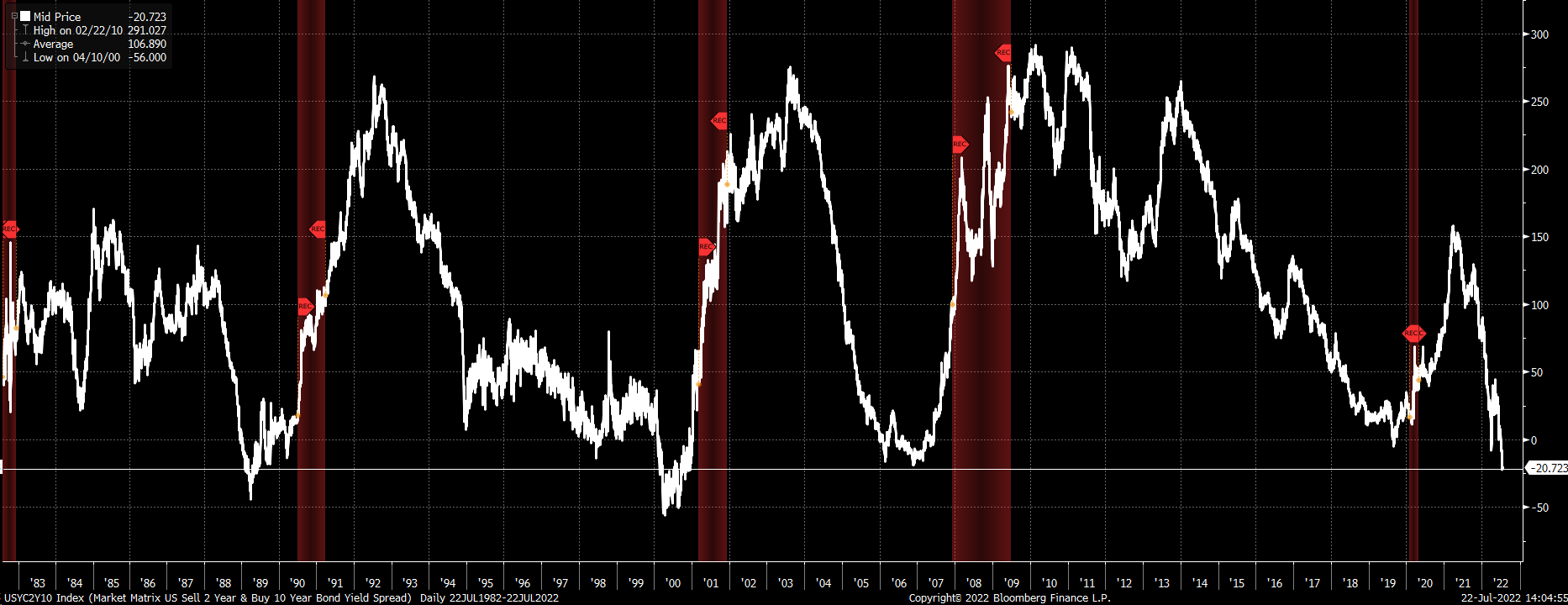

Inversion

The bond market is telling us that a recession is very close. The 10-year minus two-year yield has already reflected the risk of recession, trading around -20bps. That's roughly in line with how far the spread has fallen ahead of a downturn in previous instances.

{kind=link}

How Will The Recession Look

The only problem is that this recession may be different and take another form. Because the question is if nominal growth will fall enough to contract or if this will be a recession in technical terms when adjusted for the high inflation rate.

In a real or inflation-adjusted way, GDP was negative in the first quarter and is likely to be negative in the second quarter, given the high inflation rate. In nominal terms, growth should be strong in the second quarter. But this latest services data suggest that nominal growth may now be starting to slow in the third quarter.

{kind=link}

Easy Street

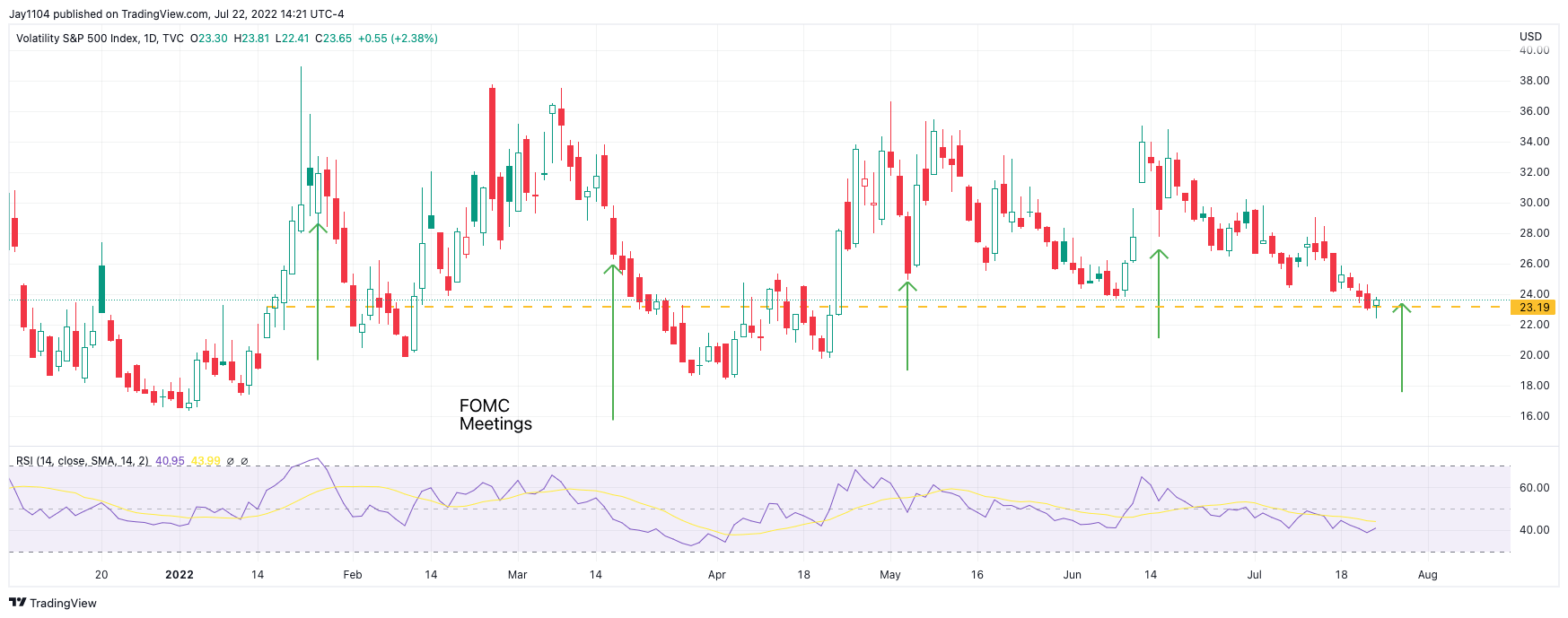

Of course, this will be front and center next week at the FOMC meeting and press conference. The language the Fed uses will be significant because if the Fed stays resolute and sticks to its tune, you can't have a strong economy with runaway inflation. Meanwhile, signals it's willing to sacrifice growth to kill off the dangers of high inflation, one would think the stocks market would not like that.

This week's market has not reflected any fear going into the FOMC meeting. Currently, the VIX is only at 23. If it stays there, it would be the lowest level the VIX has entered at a Fed meeting all year.

{kind=link}

The market appears to have taken comfort in the idea that inflation has peaked and growth is slowing, and therefore a Fed pivot is near. The market seems to be missing that the Fed also has made it clear that some pain may be endured along the way.

For further details see:

The S&P 500 Faces An Entirely New Set Of Problems