EC - The Sell-Side Appears Too Negative On Ecopetrol

2024-01-05 14:05:47 ET

Summary

- EC is the most dominant oil producer in Colombia.

- Its CAPEX plan highlights continued capital discipline.

- The sell-side is too negative on EC and the company's business model is resilient to lower oil and gas prices.

When I began to take a look into Ecopetrol S.A. ( EC ), I was most surprised by the analyst consensus. Out of the twelve analysts I see covering the name, I only saw one analyst with a buy rating on the story. Ecopetrol is the largest and most dominant oil and gas company in Colombia and surprisingly, it's not a one-trick pony. Today, over 20% of its business is from activities that don't directly include hydrocarbons and by 2040, this number is set to double as EC slowly weans itself away from oil and gas. At the time of writing, the stock is trading below its historical valuation levels despite EC continuing to post strong operating and financial results.

Company Overview

In 2003, Colombia restructured its primary petroleum company, Empresa Colombiana de Petróleos, transforming it into Ecopetrol S.A. The government aimed to globalize and enhance its competitiveness in the oil industry. With Decree 1760, dated June 26, 2003, Ecopetrol became a wholly state-owned public corporation linked to the Ministry of Mines and Energy. This change freed the company from its previous role as the oil source administrator, delegating those responsibilities to the newly formed National Hydrocarbon Agency ((ANH)).

Since then, Ecopetrol has operated more autonomously, focusing on accelerating exploration efforts, achieving results with a business-oriented approach, and aiming to strengthen its position in the global oil market. Its international footprint extends to the Gulf of Mexico, with offices in Houston, Texas, and operations in offshore areas in Mexico (Veracruz, Tabasco, and Campeche) and Brazil (offshore, with offices in Rio de Janeiro). The government of Colombia still maintains an 88.49% ownership stake in Ecopetrol today.

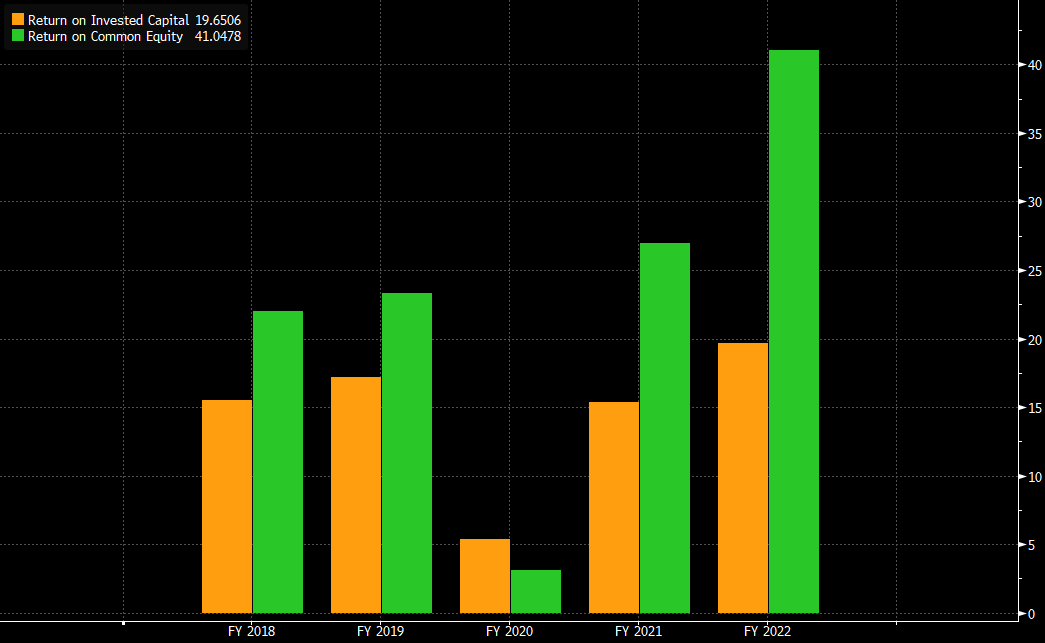

Capital efficiency has been the mantra

Over the past five years, the strength of EC's focus on capital efficiency has produced strong financial results. These are most obvious when looking at EC's return on equity ((ROE)) and return on invested capital ((ROIC)).

{kind=link}

The company has been averaging double-digit returns on invested capital and ROE in excess of 20% with the exception of 2020.

Looking into 2024 and beyond, the expectation should be of continued capital discipline. Recently, Ecopetrol revealed its upcoming investment plan with a reduced Capex of COP23-27 trillion for 2024, down from COP25-30 trillion in 2023. The forecasts for Upstream (725-730kbpd) and Refining output (420-430kbpd) remain unchanged. Paired with the company's Brent estimate of $75/bbl, this is expected to yield an average EBITDA margin of 38%. This projection is slightly lower compared to the 40% margin guidance for 2023 with Brent at $80/bbl. The plan aims for nearly unchanged production figures alongside slightly reduced CAPEX.

Margins to remain strong despite lower oil prices

With an expected decrease in Brent to about $75/bbl (down from approximately $80/bbl in 2023), Ecopetrol's 2024 Financial Plan aims to sustain current return levels, targeting a slightly lower ROCE of around 9% compared to last year's 10%. The anticipated EBITDA margin is approximately 38%, a decline from 40% in 2023 but in line with the five-year average. Ecopetrol foresees transfers to the Nation exceeding COP38 trillion (compared to COP40 trillion in 2023) and investment levels ranging from COP23-27 trillion (compared to COP25.3-29.8 trillion previously).

Ecopetrol maintains its emphasis on Exploration and Production (E&P), allocating 62% of its investments to this sector. Within Oil and Gas E&P, 50% and 12% of the total plan are designated, respectively. The company's goal is to reach production levels between 725-730kbpd, a slight increase from 720-725kbpd in 2023. This includes drilling approximately 360 development wells, with 74% in Colombia and 26% in the Permian Basin, alongside an estimated 15 exploration wells, primarily situated in Northern Colombia and the Caribbean offshore region.

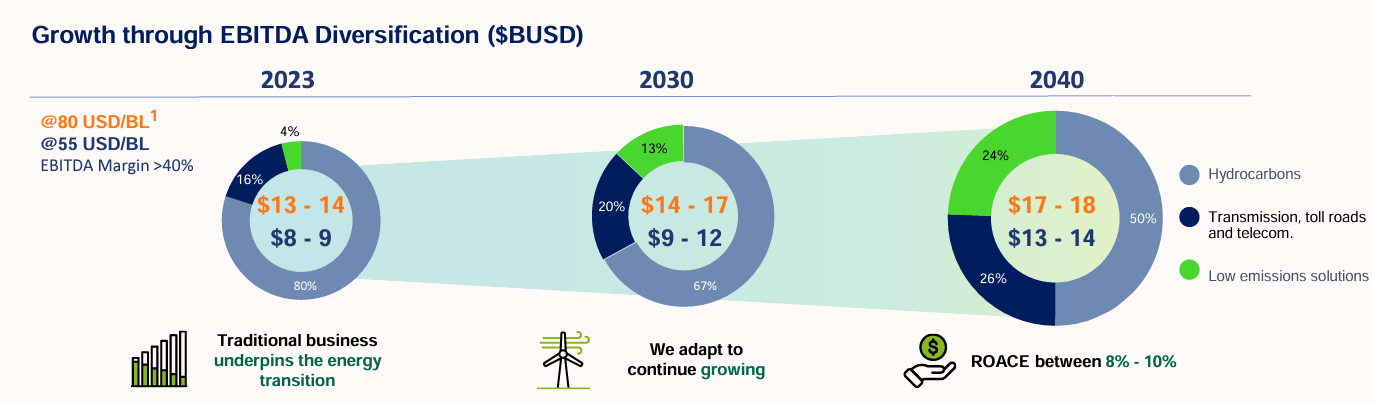

The overarching theme of the 2024 plan is the continued focus on maintaining the profitability of the business despite lower Brent prices while also focusing on its bread and butter business of hydrocarbons. There are continuing investments ongoing into its non O&G side of things which should result in EC doubling its exposure to non-extractive businesses by 2040.

{kind=link}

The company targets a payout to shareholders of ~75% of its profits through dividends and to that end, shareholders have received $2.81/share of regular and special dividends which is not too shabby considering the current share price of ~$12/share.

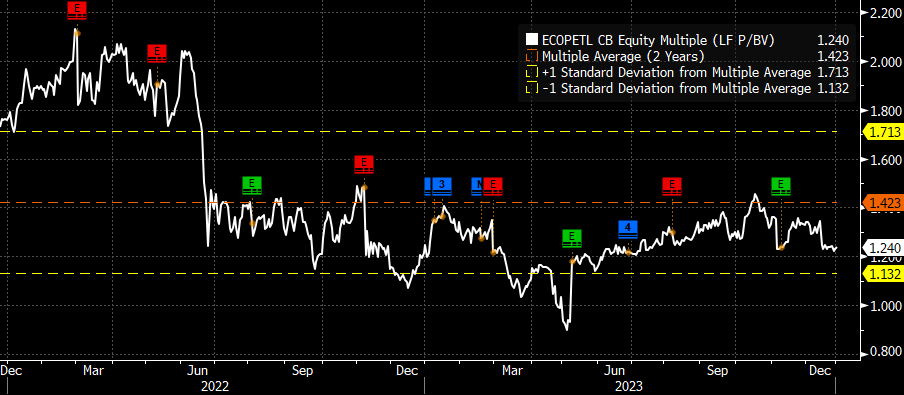

The valuations make a compelling case for EC

I get even more bullish on EC when looking at it from a valuation lens.

{kind=link}

Despite a strong performance in 2023, the company trades at a discount to its historical Price to Book. EC is currently trading at 1.24x versus a two-year average of 1.42x.

{kind=link}

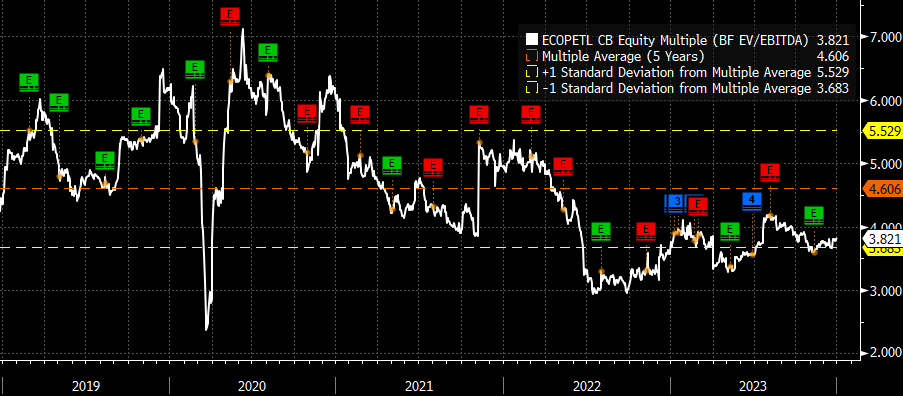

Similarly, EC is currently trading at a lower end of its valuations on a EV/EBITDA basis. EC currently trades at the lower end of its five-year EV/EBITDA range.

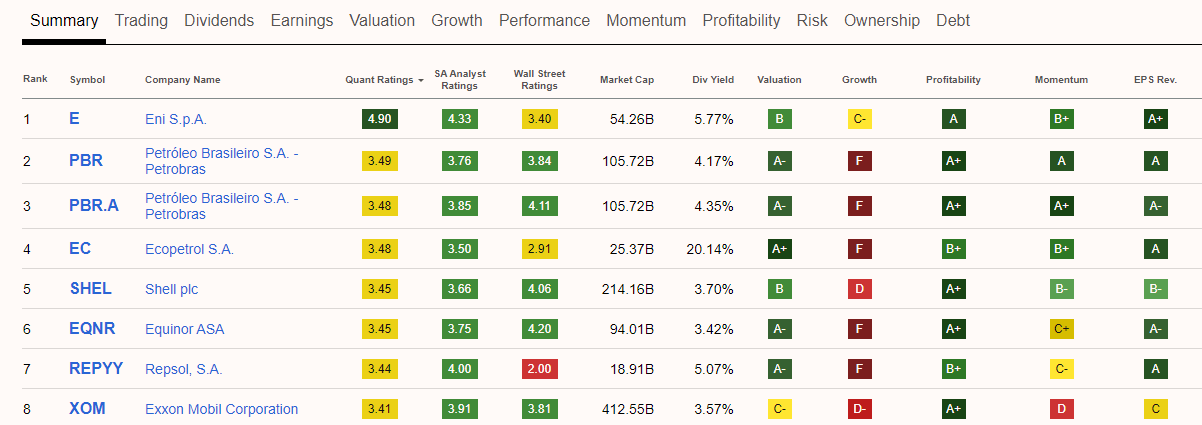

A key reason for the negative analyst mood towards EC is their growth profile, or rather the lack thereof. This is already priced into the stock in my opinion. When viewing the name through the Seeking Alpha quant rankings, it screens quite well, ranking 4th out of the 16 names in the large cap integrated oil and gas universe.

{kind=link}

It must be noted that EC ranks ahead of behemoths like Shell and Exxon, partially due to its valuation and partially due to earnings being revised upwards.This goes to my initial point about the analyst community being too sour towards this name. The negativity towards this name has made it easy for the company to surprise to the upside of late.

What can go right?

There is room for this valuation to look even more cheaper should we get higher commodity prices. As stated earlier, EC is forecasting a Brent price of $75/bbl versus $80/bbl in 2023. There is good leverage to rising oil prices in EC's business model.

An optimistic scenario could arise from:

- Improved lifting costs or lower breakevens, leading to enhanced margins.

- Increased volumes or oil prices surpassing expectations.

- A more robust economic rebound in Colombia, resulting in higher refinery utilization rates.

Any of these scenarios would boost EBITDA upward and make the stock even cheaper versus its current valuation.

What can go wrong?

Inversely, however, we could see EBITDA come under pressure should Brent trade lower than currently forecasted. Another aspect of risk worth mentioning is in the Permian where EC operates. Should production fail to meet expectations, it will negatively impact the company's profitability.

The 88.49% stake in EC held by the Government of Colombia is a cause for concern for some shareholders. There is always a possibility, that one day a socialist government comes into power and seeks to reassert control over the entire company by leveraging their existing position in the stock.

Sometimes it's good to be a contrarian

I believe that the sell-side is too negative on EC. The company's business model is resilient to lower oil and gas prices and its position in the Colombian economy is dominant. With only 1 out of 12 sell-side analyst rating this a buy, I think the contrarian trade here is for investors to look at more optimistic scenarios in this name. With valuations near trough and a shareholder friendly model, EC could be a profitable investment for investors especially if we get higher Brent prices and valuations reassert themselves to historical levels.

For further details see:

The Sell-Side Appears Too Negative On Ecopetrol