NPCPF - The Sherwin-Williams Company: Solid Dividend Portfolio Pick With No Upside

2023-05-29 01:49:34 ET

Summary

- Sherwin-Williams Company has strong profitability, a rock-solid dividend, and a fair balance sheet.

- SHW has a solid competitive advantage in recession-resilient businesses and is rapidly expanding its production line and exploring new market opportunities.

- I will give SHW a "hold" rating entering the second half of 2023.

I repainted my flat for the first time in five years. The work is tough in the summertime in Asia (over 30 degrees!), but hard work turned into huge satisfaction and a comfy living environment for my family.

The Sherwin-Williams Company ( SHW ) was founded in 1866, which develops, manufactures, distributes and sells paint and coating products to businesses and retail customers. Statista estimated that the America-focused company owns nearly 30% of the painting and coating market share in North America.

Over the last decade, the company provided over 250% return (excluding dividends) for its investors, outperforming S&P 500 (SPY) by over 100%. However, the recent sluggish housing market has led SHW to a 5% decline YTD.

In this article, I studied SHW's fundamentals from both qualitative and quantitative approaches and found the company as a solid long-term choice but too expensive now.

Quantitative Analysis

1) Strong Profitability

Revenue per share and earnings per share of SHW grew 8.3% CAGR and 18.7% CAGR from 2018 to 2022, respectively.

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Earnings per Share |

| $3.89 |

| $5.50 |

| $7.36 |

| $6.98 |

| $7.72 |

| Revenue per Share |

| $61.53 |

| $63.86 |

| $66.58 |

| $74.67 |

| $84.60 |

(Data from Seeking Alpha, Compiled by Author)

Margins significantly improved during the pandemic tailwinds but returned to pre-pandemic levels in the previous financial year.

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Gross Margin |

| 42.31% |

| 44.89% |

| 47.29% |

| 42.83% |

| 42.1% |

| Operating Margin |

| 10.78% |

| 13.55% |

| 15.54% |

| 13.36% |

| 13.55% |

(Data from Gurufocus, Compiled by Author)

As summarized using Seeking Alpha's Comparison function , SHW's margins are the best of the class, but its growth is slower than its Japanese competitor, Nippon Paint ( NPCPF ). The other two companies, PPG Industries ( PPG ) and Sk Kaken ( SKKAF ) showed weaker performance overall.

It is worth mentioning that SHW and NPCPF do not face direct competition as their major geographic revenue streams differ.

Data from Seeking Alpha, Compiled by Author

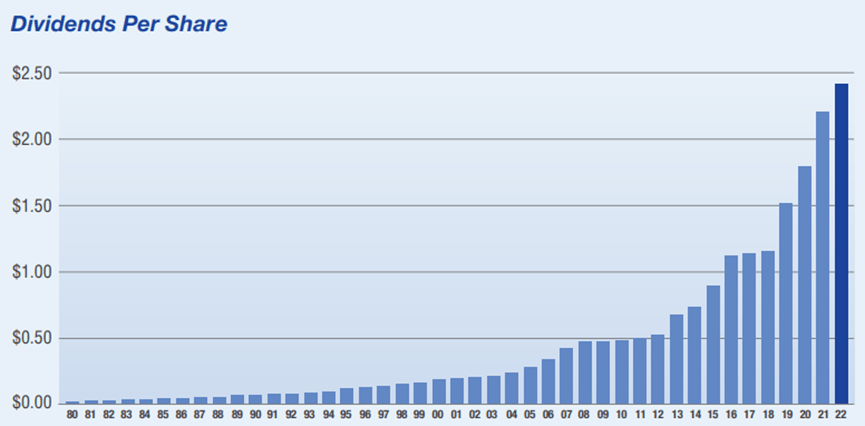

2) Rock Solid Dividend

As a highly anticipated recession is approaching, investors worry if their passive income is at risk. A handful of REITs have already cut their dividend payment . SHW is a solid choice for dividend seekers. SHW is not the most popular choice for dividend investors as the company only has a slightly over 1% dividend yield now.

However, the company has increased its dividend payment for 44 consecutive years (since its first dividend payment in 1980!).

{kind=link}

It also has an impressive 15.05% 10-year CAGR dividend growth rate but only at the expense of 26.23% payout ratio. If SHW's dividend continues to grow at this rapid pace, your yield-cost-cost will double every 5 years.

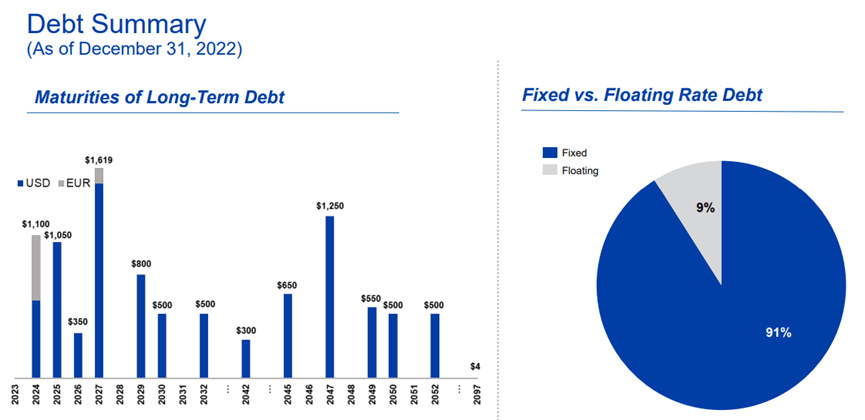

3) A Fair Balance Sheet

A solid balance sheet is also critical to consistent dividend payments and continuous expansion of the company.

SHW has no debt maturities until 2024, and 91% of its debt is fixed interest rate, which is beneficial under a high-interest rate environment like now.

{kind=link}

SHW owns $9,593.1 million in long-term debt in the latest financial quarter, which is slightly more than the company's tangible asset value. Investors should regularly monitor the company's debt-to-asset ratio to check its financial health. A summary of financial strength ratios is tabled below for easy reference.

| Current Ratio |

| 1 |

| Debt to Asset Ratio |

| 0.56 |

| Debt to Equity Ratio |

| 4.11 |

| Equity to Asset Ratio |

| 0.14 |

Overall speaking, the balance sheet of SHW is fair and without significant risk.

Qualitative Analysis

1) Home improvement spendings expect to peak in 2023

Peaking home improvement and maintenance expenditures would adversely impact SHW.

The high-interest rate environment has led to declining existing home sales and home improvement incentives. Existing home sales data fell in 14 out of the last 15 months since February 2022. And The Leading Indicator of Remodeling Activity expected home improvement and maintenance expenditures to peak in the third quarter of 2023 and start to decline subsequently.

Leading Indicator of Remodeling Activity (LIRA)

The housing market already showed signs of distress in 2022, but for the Paint Stores Group (previously named as the Americas Group), same-store sales in U.S. and Canada paint stores still grew 11.7%.

As mentioned in its 2022 Annual Report :

All Pro market segments increased by double digits, led by property management and followed by commercial, residential repaint and new residential, respectively. Sales in protective & marine and DIY also increased by double-digit percentages... We also enter this year with a higher percentage of "recession-resilient" business in our portfolio than we did in prior downturns.

It shows the preparation and resilience of SHW amid tough operational conditions.

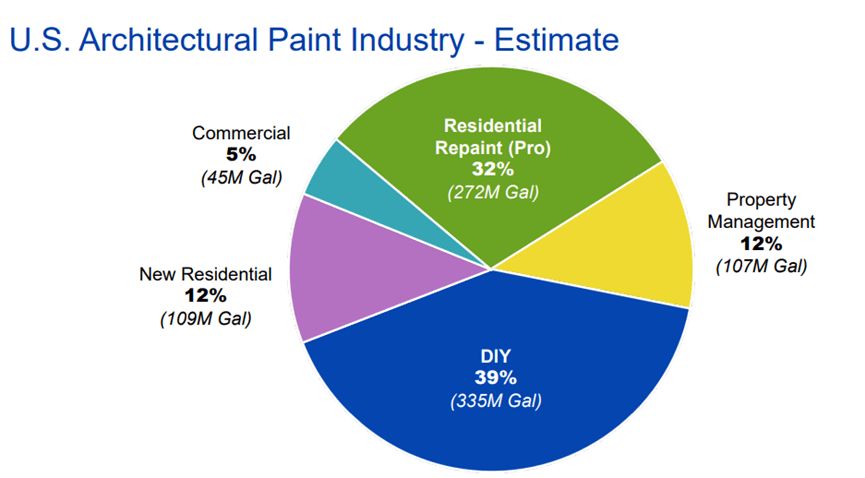

2) Paint is Not Fully Discretionary

It is a common belief that SHW's performance is very much reliant on the housing market and the economic backdrop.

This is not entirely true.

SHW estimated that a significant part of architectural paint is sold retail for DIY or for professionals in home improvement projects. New residential projects are only accountable for 12% of architectural paint usage in the U.S.

SHW 2023 Investor Presentation

{kind=link}

Emulsion paint usually only last less than a decade, while some higher quality paint (E.g. Polyurethane or silicone paint) may last more than a decade. In exposed conditions, the lifespan of paint will decrease. It means that everyone is returning to purchase SHW's products regularly to keep their premises attractive.

Of course, expenses on this would not be one's priority in an economic downturn, but some may still consider spending $2000 to renovate the house to lighten up on themselves.

SHW also has a solid competitive advantage in "recession-resilient" businesses like Residential Repaint, Property Maintenance, Automotive Refinish and Packaging.

3) A Rapid Expanding Business

SHW expanded its production line and explored new market opportunities over the years.

During 2022, SHW invested $1.003 billion to complete five acquisitions. One example is the acquisition of Sika AG's European industrial coatings business to expand the exposure to oil and gas, water and wastewater, and fire protection applications. Sika AG is a world-leading manufacturer of industrial coating. This strategic acquisition should add magnificent value to SHW's portfolio and drive margins higher.

Also, the company expected to open 80-100 new paint stores while adding sales representatives and new territories in 2023. By the end of 2023, SHW will have 5,000 stores in America, Mexico, Canada, South America, etc.

Sherwin-Williams is not Cheap

Sherwin-Williams has great long-term value as it has strong profitability and rewards its shareholders by consistently paying dividends and buying back shares. Thus, its valuation would be the key to determine if it is the time to buy on SHW.

As the performance of SHW is anticipated to stay stagnant in 2023, I believe the market is likely to give the stock lower multiples. Thus, I will apply a 10% discount on the 10-year average for valuation purposes.

SHW traded at $229.14 as of 26 May 2023, implying a PE ratio of 27.84.

Below displays my bullish and bearish cases of valuation for Sherwin-Williams, assuming the stocks return to 90% of the current 10-year average PE ratio.

| Bullish Case |

| Bearish Case |

| 2023 Growth in EPS |

| 10% |

| -10% |

| Fair Value |

| (7.72*1.1)*(29.41*0.9) = $224.77 |

| (7.72*1.1)*(29.41*0.9) = $183.91 |

| Implied Growth |

| -1.9% |

| -19.7% |

As the downside risk of SHW is obvious at current valuation, I will give SHW a "hold" rating entering the second half of 2023.

Please feel free to leave a comment below to share your view.

For further details see:

The Sherwin-Williams Company: Solid Dividend Portfolio Pick With No Upside