SO - The Southern Company: A Solid Company But Still Overvalued

2023-11-16 05:05:09 ET

Summary

- Southern Company is quite forward-looking and appears far more attractive than many of the other utility providers I follow.

- They are nearing the completion of the Voglte Nuclear Plant and expect Unit 4 to come online in Q1 of 2024.

- The company's financials show growth in revenue and operating income, but it has high levels of debt and is currently overvalued.

- I currently rate SO as a Hold.

Thesis

Because of my background in energy production, I regularly follow several utilities. Most of them are currently taking advantage of the opportunity the Inflation Reduction Act is providing them to update their portfolios into ones that produce less greenhouse gas.

The Southern Company ( SO ) stands out from the crowd for me because they are currently working toward setting themselves up with several additional long-term revenue streams. They are also nearing the completion of a nuclear plant and are expected to experience an EPS increase as a result. This is an update to my last article on Southern Company. After looking over their financials and valuation, I presently rate Southern Company as a Hold.

Company Background

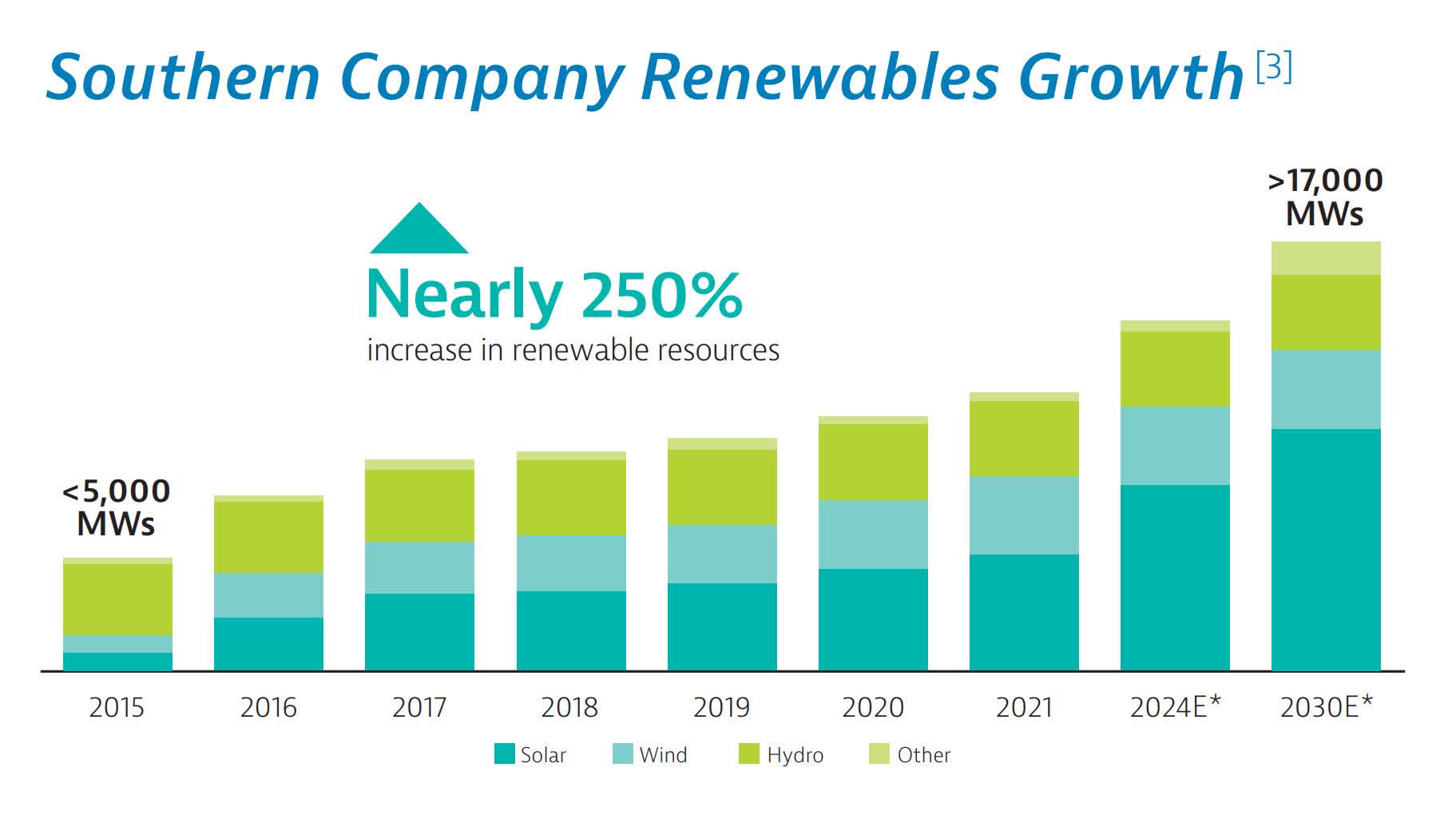

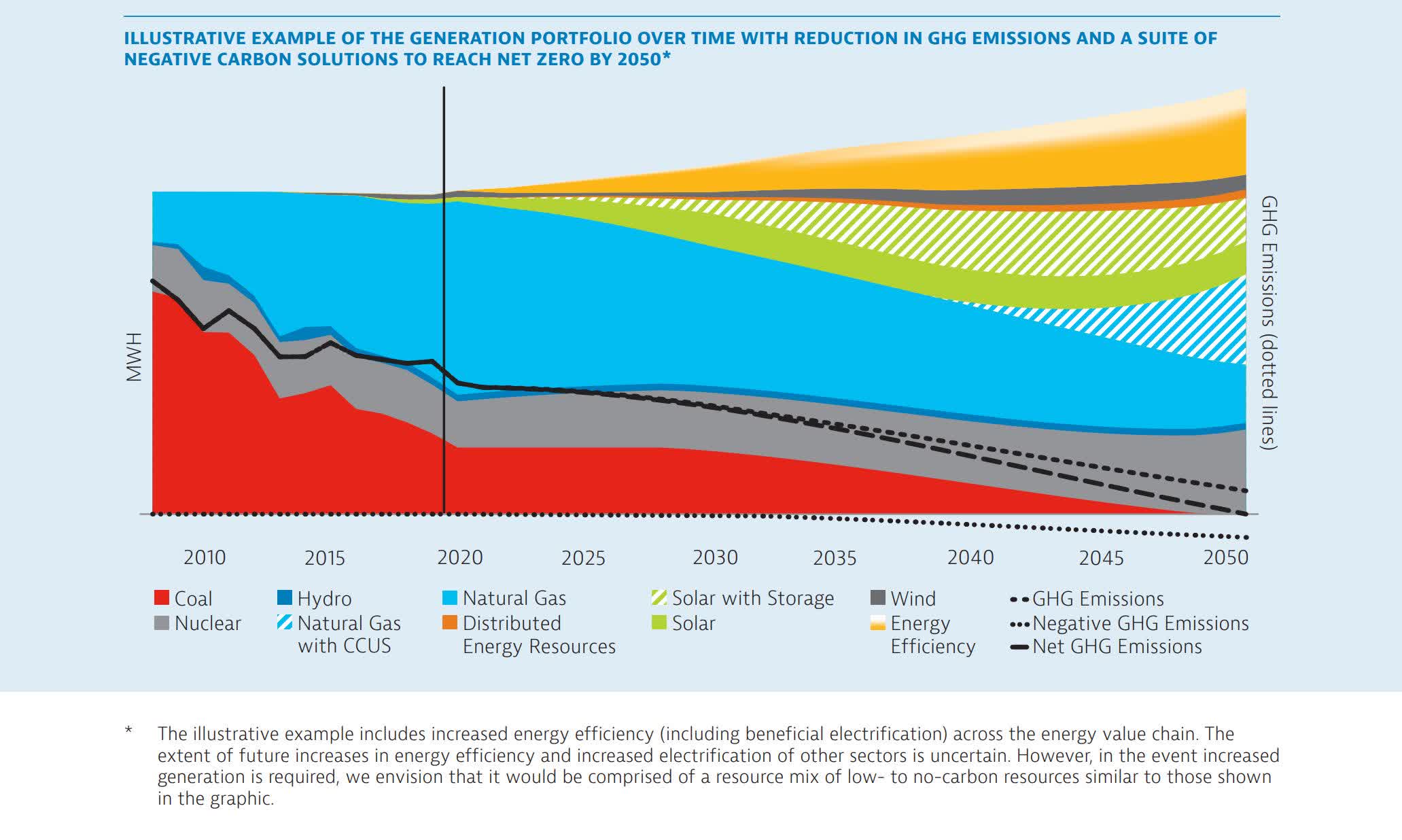

Southern Company is a utility provider currently serving over 9 million people in the southern United States. They include natural gas, wind, solar, and nuclear in their portfolio. The company is in the process of transitioning its assets to cleaner ones and has set a goal to reduce its greenhouse gas emission levels to 50% of its 2007 levels by 2030. They have also set a goal to reach net zero by 2050 .

2022 Year In Review (Southern Company) 2020 Implementation and Action Toward Net Zero (Southern Company)

{kind=link}

{kind=link}

Southern Company is a forward-looking innovator . They formed a coalition to build out a hydrogen infrastructure. They are making efforts to develop a molten chloride reactor . They have joined with several others to further develop carbon capture technology . The company also began a program which has a goal of lowering waste and losses the natural gas leaks . These collective efforts have earned them a reputation for environmental transparency .

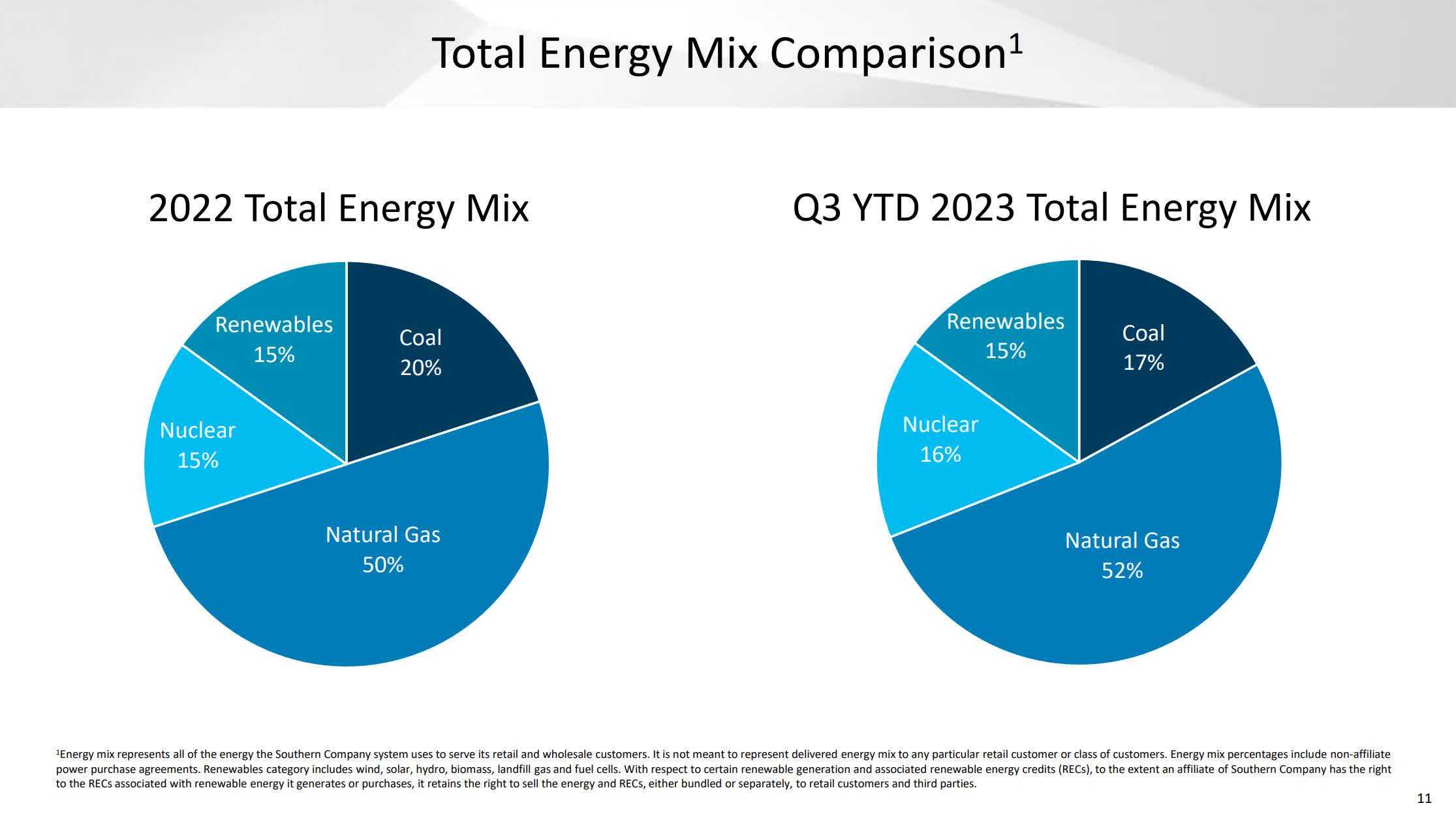

Total Energy Mix Comparison (Q3 2023 Investor Presentation Page 11)

{kind=link}

Long-Term Trends

The U.S. power market is projected to have a CAGR of 5.6% through 2028. The solar panels market is expected to have a CAGR of 25.7% until 2028. The global natural gas market is projected to experience a CAGR of 7.2% through 2032. Hydrogen as a fuel is expected to experience a CAGR of 5.2% until 2030. The U.S. nuclear market is expected to have a CAGR of 4.8% through 2027. The global coal market is expected to have a CAGR of 1.97% until 2031.

Guidance

Their most recent earnings call transcript revealed that the company is continuing its progress toward reaching net zero emissions.

SO Guidance 1 (Q3 2023 Earnings Call Transcript)

{kind=link}

They are also continuing their long-term plan to update their production capability into one which is carbon neutral by 2050.

SO Guidance 2 (Q3 2023 Earnings Call Transcript)

{kind=link}

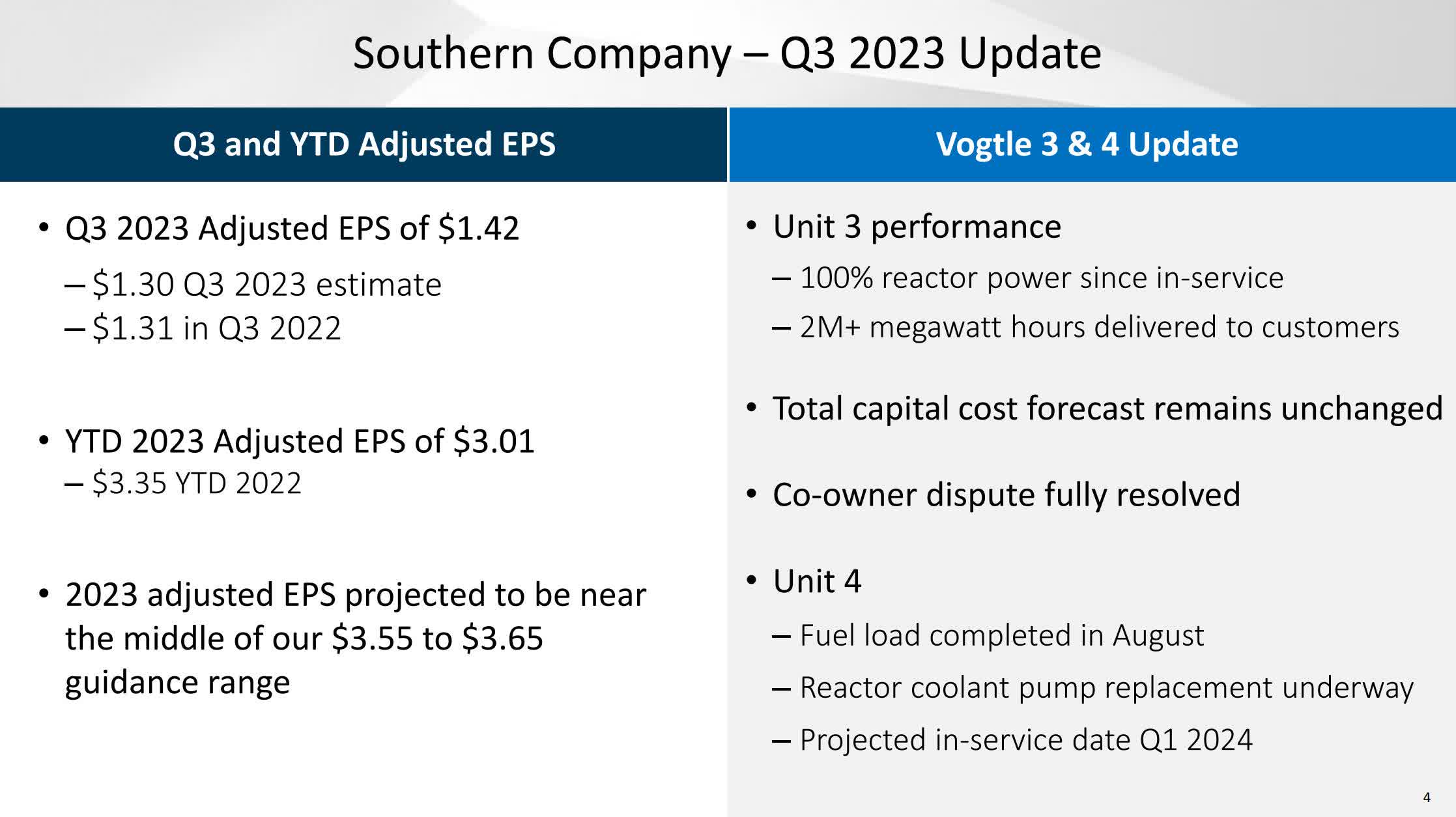

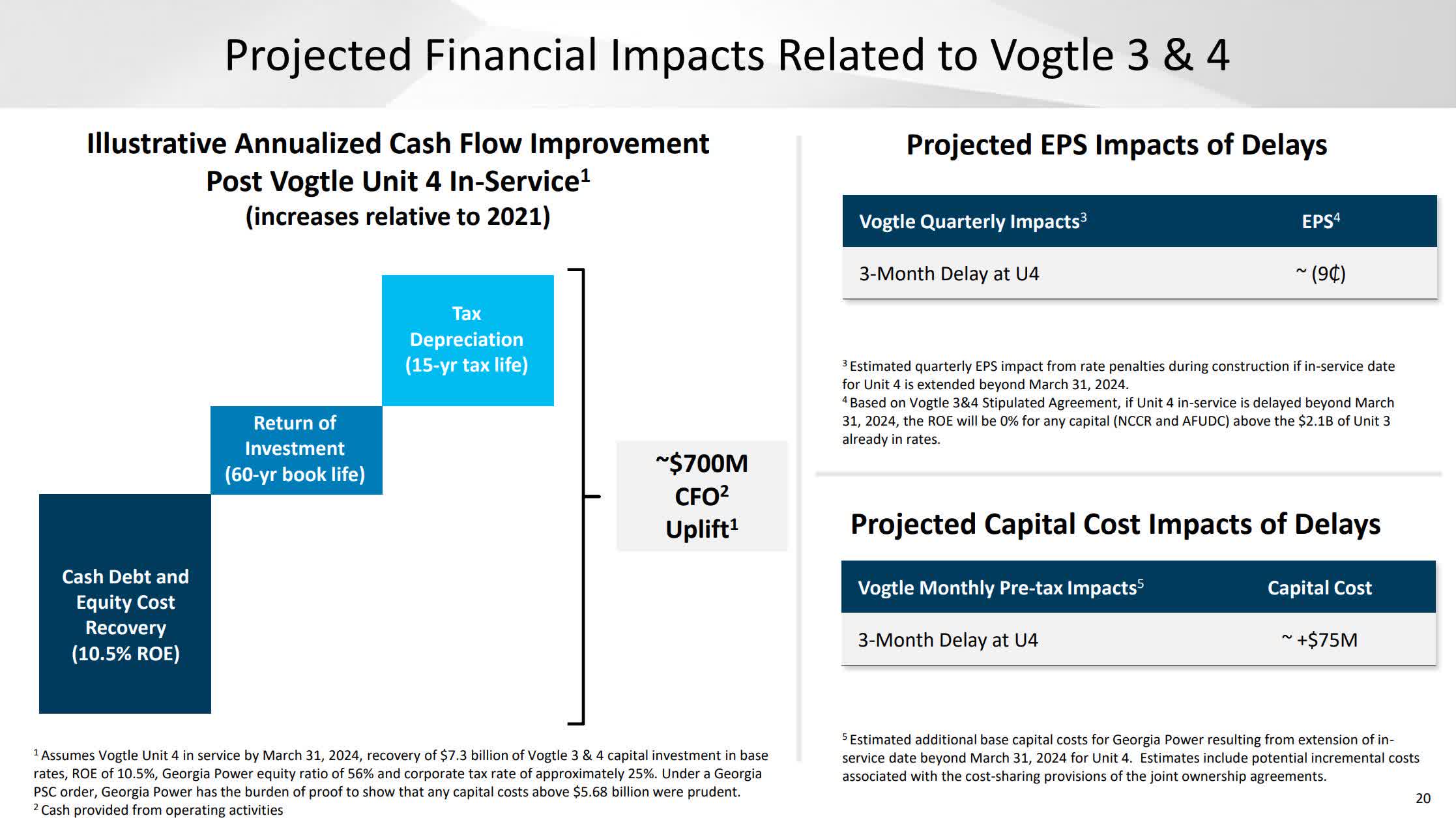

Their most recent investors presentation indicated that Unit 3 is still operating at 100%. Unit 4 is projected to come online in Q1 of 2024.

Update (Q3 2023 Investor Presentation Page 4)

{kind=link}

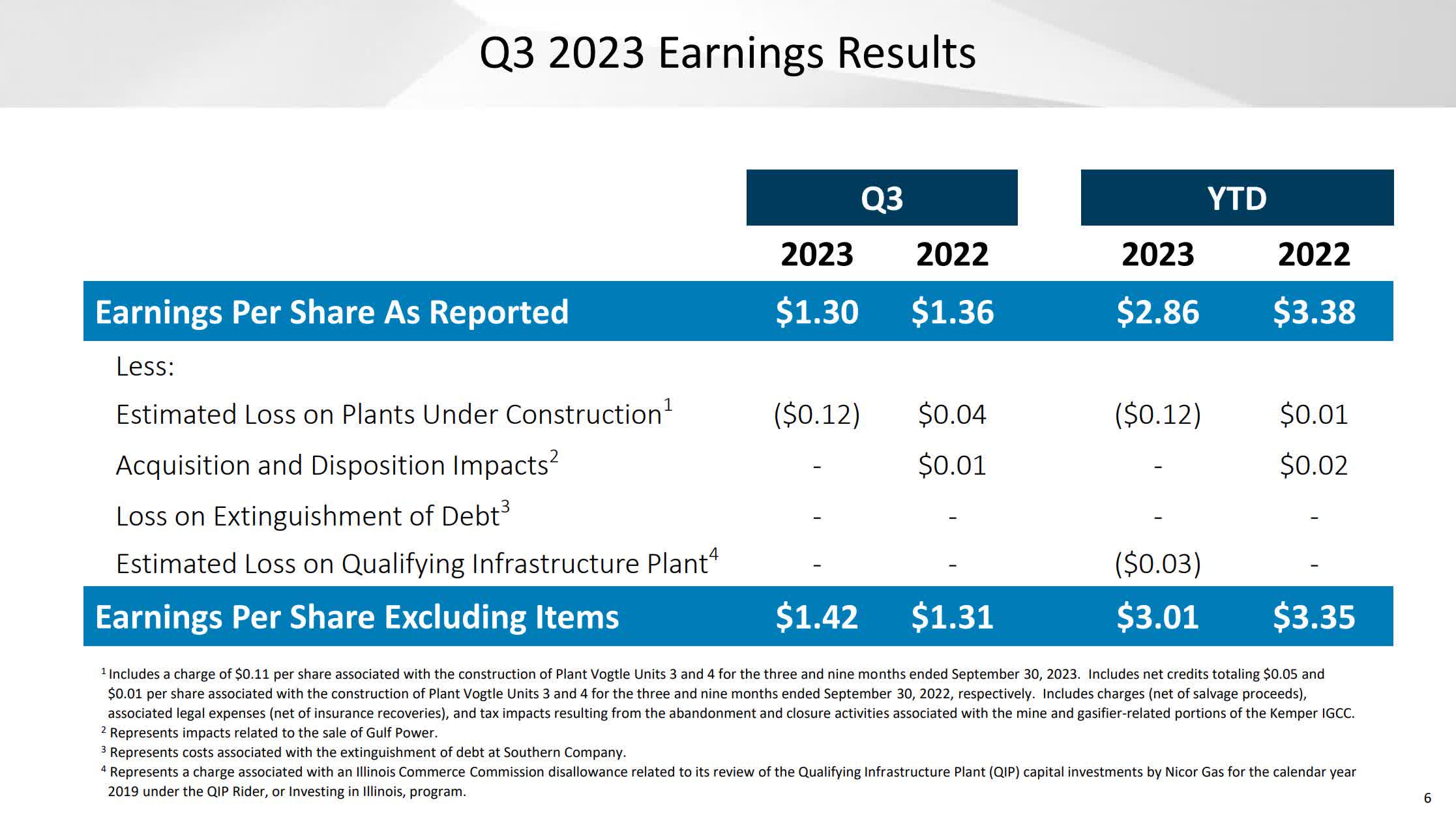

The company is currently spending $0.12 per share on new plant construction. They cite that approximately 11 of the 12 cents are related to construction at Vogtle 3 & 4. So once work on Unit 4 is complete, the company is expecting an earnings per share improvement of approximately $0.11.

Estimate Loss From Plant Construction (Q3 2023 Investor Presentation Page 6) Projected Impacts of Vogtle 3 & 4 (Q3 2023 Investor Presentation Page 20)

{kind=link}

{kind=link}

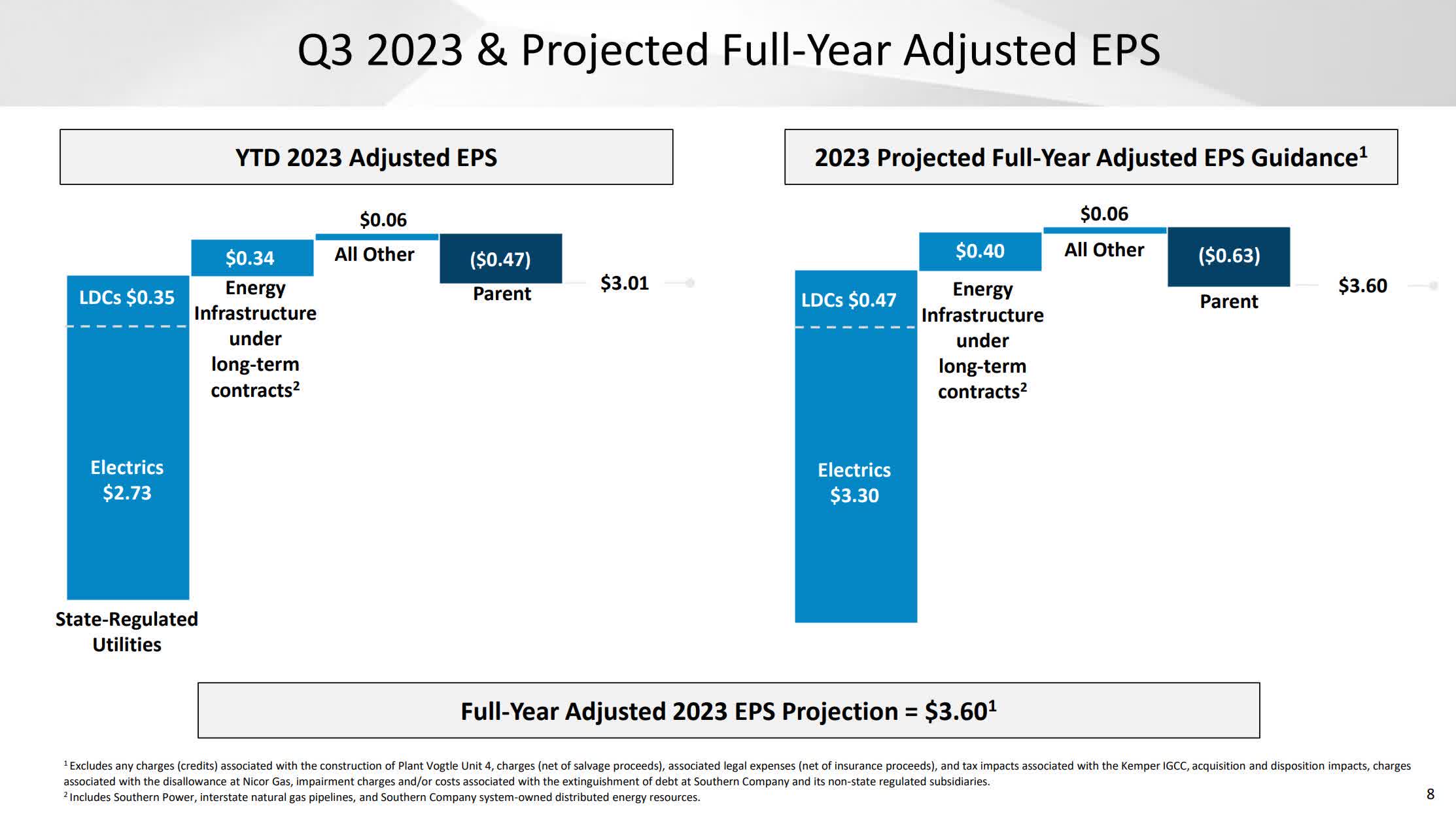

By the end of Q3, they have already earned an adjusted EPS of $3.01, and expect full year adjusted EPS to end up around $3.60.

EPS Guidance (Q3 2023 Investor Presentation)

{kind=link}

Annual Financials

The company has been increasing its revenue over the last decade. In 2013 they had an annual revenue of $17,087M. By 2022 that had increased to $29,279M. This represents a total increase of 71.35% at an average annual rate of 7.93%.

{kind=link}

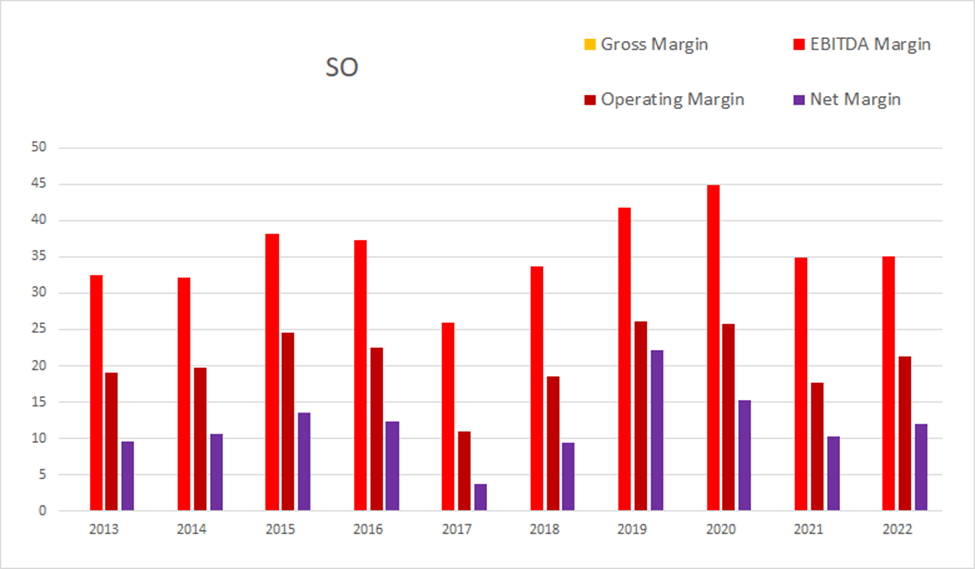

Southern company has maintained fairly stable margins over the last decade. As of the most recent annual report, EBITDA margins were 35.12%, operating margins were 21.24%, and net margins were 12.04%.

{kind=link}

Their income has been growing at a significantly faster rate than their dilution. Total common shares outstanding was at 887.1M in 2013; by the end of 2022 that had risen to 1,088.8M. This represents a 22.74% rise in share count, which comes out to an average annual rate of 2.53%. Over that same time period operating income rose from $3,255M to $6,220M, a 91.09% total increase, at an average rate of 10.12%.

SO Annual Share Count vs. Cash vs. Income (By Author)

{kind=link}

As of the 2022 annual report, they only had -$2,033M in net interest expense, total debt was $59,437M, and long-term debt was $50,600M.

{kind=link}

As of this most recent annual report, cash and equivalents were $1,917M, operating income was $6,220M, EBITDA was $10,284M, net income was $3,524M, unlevered free cash flow was $130.5M, and levered free cash flow was -$1,140.1M.

SO Annual Cash Flow (By Author)

{kind=link}

Their total equity has been slowly increasing over the last decade.

SO Annual Total Equity (By Author)

{kind=link}

This trend also showed up in their margins; the company had below-average returns in 2017 and above-average returns in 2019. As of the most recent annual report ROIC was 0.62%, ROCE was 4.93%, and ROE was at 10.21%.

{kind=link}

Quarterly Financials

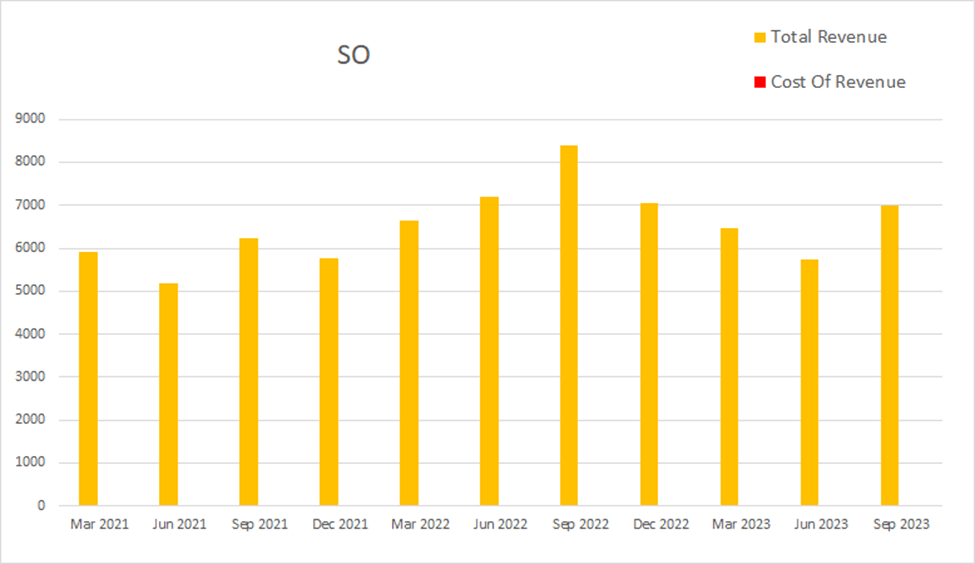

Their quarterly financials are showing some seasonality. Compared to their other quarters, they experience lower revenue every Q2 and elevated revenue every Q3. Eight quarters ago Southern Company had a quarterly revenue of $6,238M. Four quarters ago that had increased to $8,378M. By this most recent quarter that had dropped to $6,980M. This represents a total two-year increase of 11.89% at an average quarterly rate of 1.49%.

SO Quarterly Revenue (By Author)

{kind=link}

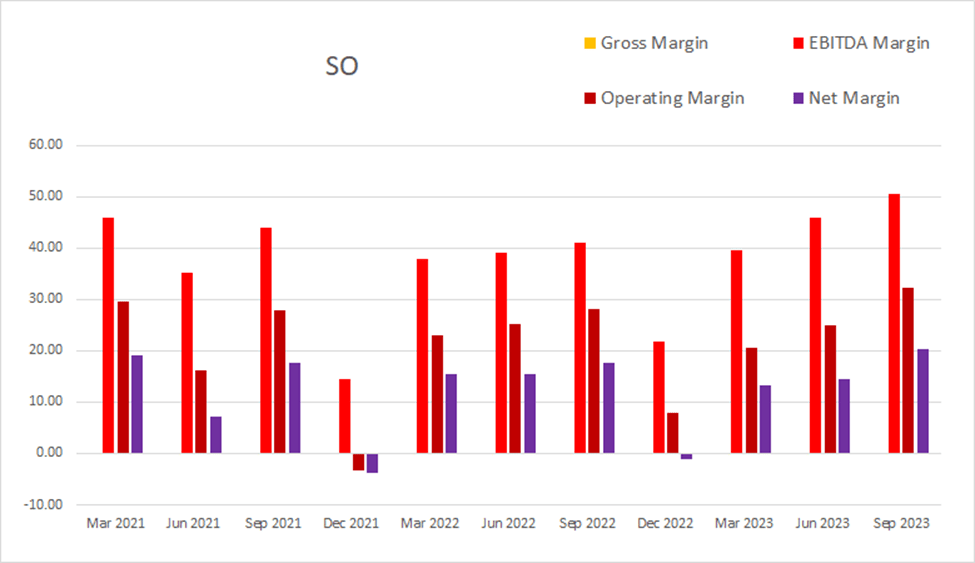

As of the most recent quarter, EBITDA margins were 50.47%, operating margins were 32.38%, and net margins were at 20.37%.

SO Quarterly Margins (By Author)

{kind=link}

Their pace of dilution has slowed over the last year. The sum of their last eight quarters of dilution comes to 2.89%; over the last four quarters this has risen/dropped to 0.27%.

SO Quarterly Share Count vs. Cash vs. Income (By Author)

{kind=link}

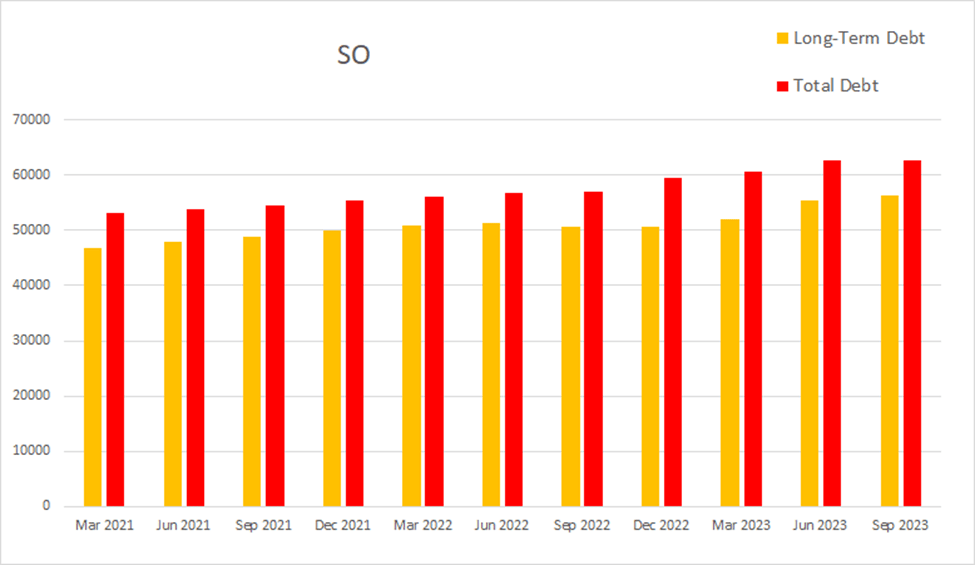

Their debt continues to slowly rise. This most recent quarter, Southern Company had -$620M in net interest expense, total debt was at $62,577M, and long-term debt was at $56,274M.

{kind=link}

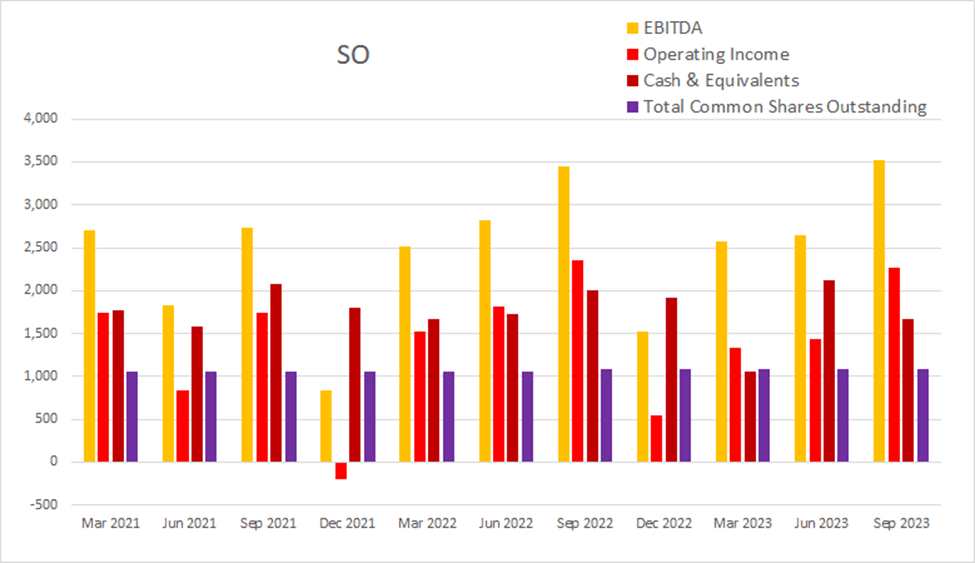

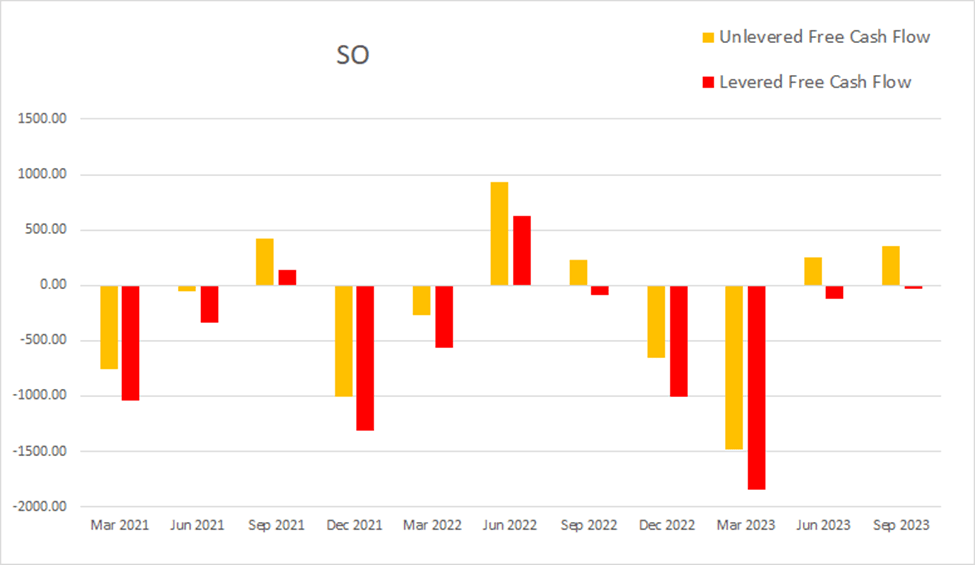

The seasonality which shows up in their revenue also shows up in their cash flows. As of the most recent earnings report, cash and equivalents were $1,676M, quarterly operating income was $2,260M, EBITDA was $3523M, net income was $1,422M, unlevered free cash flow was $352.5M, and levered free cash flow was -$35M.

SO Quarterly Cash Flow (By Author)

{kind=link}

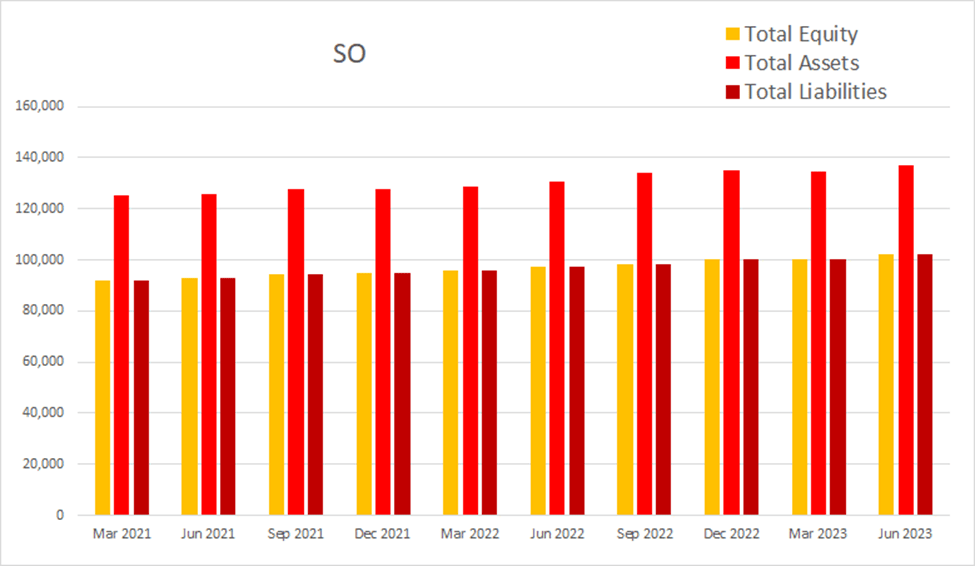

Total equity has been steadily rising.

SO Quarterly Total Equity (By Author)

{kind=link}

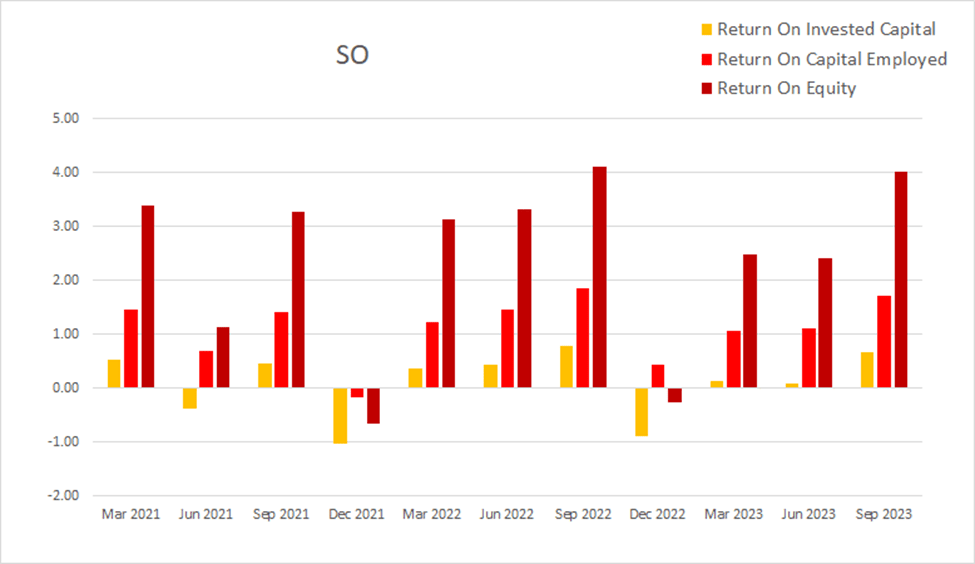

They experience significantly lower than average returns every Q4. As of the most recent earnings report ROIC was 0.67%, ROCE was 1.71%, and ROE was 4.03%.

SO Quarterly Returns (By Author)

{kind=link}

Valuation

As of November 14th, 2023, Southern Company had a market capitalization of $74.27B and traded for $69.21 per share. They do not pay a dividend, so using their forward P/E of 19.02x, and their EPS Long-Term CAGR of 5.66%, I calculated a PEGY of 3.36x and an Inverted PEGY of 0.298x. This PEGY estimate implies intrinsic value is currently around $20.62 per share.

{kind=link}

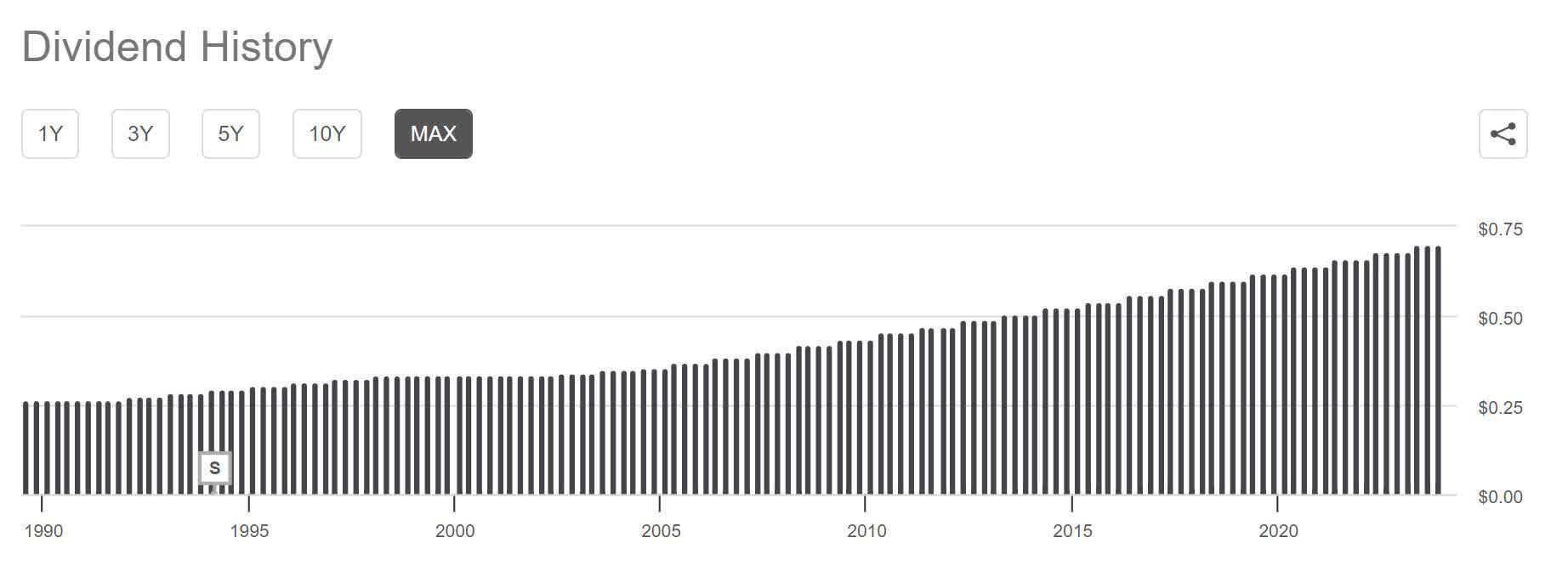

If I instead choose to use a discounted cash flow calculator to value the company based purely on its dividend, I get a noticeably different result. This is referred to as a Dividend Discount Model since it looks at the present value of its projected yield over longer timeframes. The company has achieved a 10 years dividend growth rate at a CAGR of 3.30% . Using the current annual dividend of $2.80 per share , a dividend growth rate of 3.3%, a discount rate of 9%, and assuming they can maintain this dividend growth for 20 years, a discounted cash flow calculator produces a fair value estimate of $44.04 per share.

SO Dividend History (Seeking Alpha)

{kind=link}

Risks

Southern Company is in the middle of altering its portfolio to one which produces less greenhouse gas. They clearly have a plan, and appear to be on track to meet their net-zero target by 2050. However they could fail to meet this goal, or the resulting portfolio may be less profitable than they expect.

The Inflation Reduction Act is currently encouraging utilities to modernize. If it were repealed or revised, the subsidies helping all these separate utilities may disappear.

Both natural disasters and malicious intent are constant concerns for our energy grid. I expect that most disruptions will be temporary and are unlikely to cause permanent damage to the company's financial health.

Catalysts

Southern company altered the rate of its dividend growth around 2005. After restructuring their portfolio, their revenue and margins may improve enough that they increase the rate of their dividend growth.

They have entered into a coalition with several other companies. As the coalition continues to build out their hydrogen infrastructure, it has the potential to grant Southern Company an additional source of revenue.

Conclusions

Overall, Southern Company appears far more attractive than many of the other utility providers I follow. Unlike most of the others, this company has garnered a reputation for being extremely forward-looking. Also, beginning in 1948, they paid a dividend that was either equal to or greater than the previous year, every year.

Utilities are often slow growers with large debt burdens so they are typically incapable of producing attractive PEGY values. This is why I also view their yields through discounted cash flow estimates. So if the share price ever falls to a price where I would consider it undervalued from a DCC point of view, I will be tempted to step in and begin buying purely for the yield it produces.

For further details see:

The Southern Company: A Solid Company, But Still Overvalued