QQEW - The Stock Market Faces An Even Steeper Decline In 2023

Summary

- If 2022 was about the Fed, 2023 is likely to be about the Fed and earnings.

- If the economy is heading for a recession similar to 2001 and 2008, the S&P 500 could fall below 3,000.

- If the economy is heading for just a period of slower growth, then the S&P 500 could head toward 3,100.

Past bear market cycles like 2001 and 2008 tell us that the bear market of 2022 is not over yet, and is likely just entering its next phase. The next part of the cycle involves slowing economic growth as the Fed reaches its peak terminal rate in early 2023. The path of the economy will determine how far the S&P 500 falls, and it could be by a lot.

Whether the US economy reaches a recession or sees prolonged and minimal growth may not matter. Because as inflation comes down, nominal growth should slow, negatively impacting sales and earnings growth for the S&P 500. What will matter, though, is how much those sales and earnings drop.

Bear Markets Of The Past

The 2001 and 2008 bear markets tell us we are still very much in a bear market in 2022 and are likely to continue to be in one in 2023. The 2001 and 2008 bear markets are similar to the 2022 market from an emotional and psychological standpoint because they both involve two things that tend to happen on the same cycle every year: Earnings and the Fed. It's also probably why the charts line up so nicely with each other.

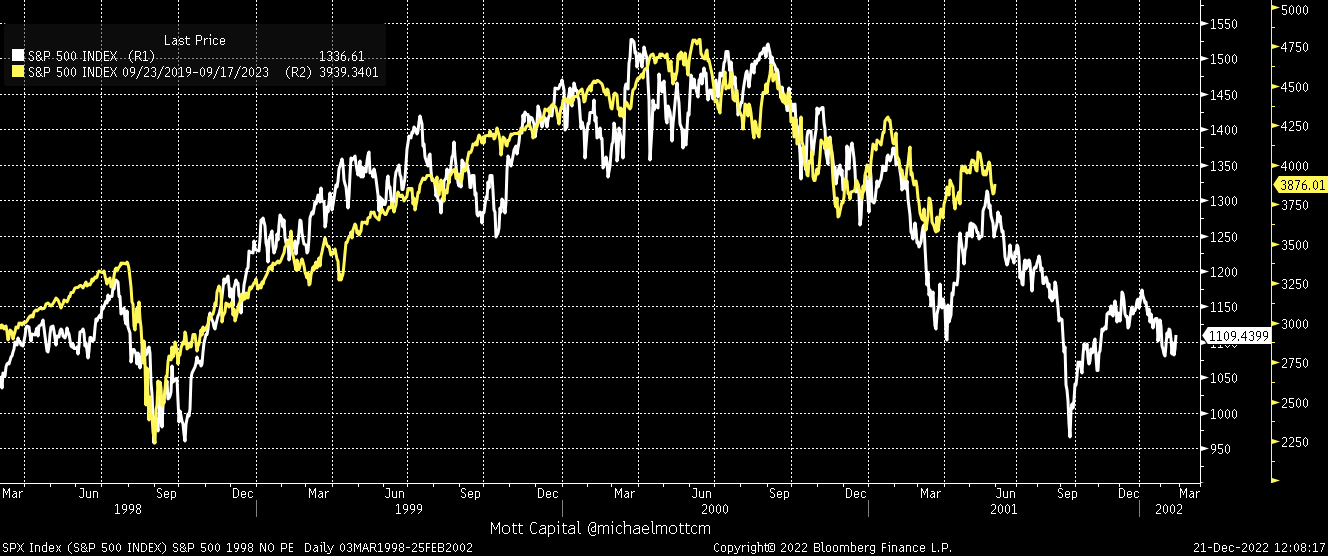

2001 Seems The Most Similar

In 2022, the bear market has been driven by the Fed. In 2023 it will likely continue to be caused by the Fed with the addition of earnings. It compares nicely to the bear market of 2001 and 2002 due to monetary policy, declining earnings, and very pricey valuations.

If we were to place the S&P 500 of today at a point in the 2001 bear market, it would line up with June 2001. The S&P 500 had just seen a monster rebound and was peaking, and about to head sharply lower as investors began to worry over earnings weakness, a slowing economy, and job cuts starting to mount.

{kind=link}

Bloomberg

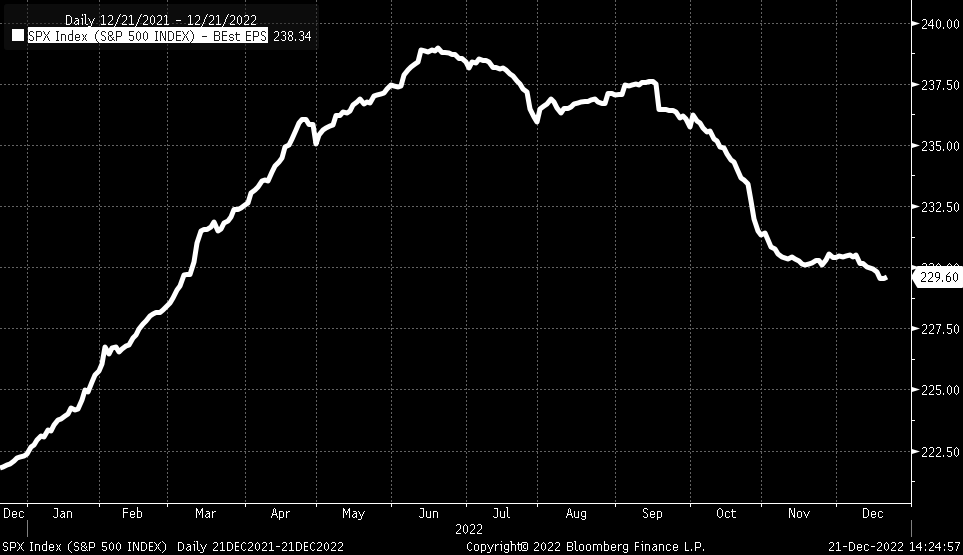

It compares to the move lower in 2022, mainly due to rising interest rates and a reset in market valuation. However, at this point in the 2022 cycle, earnings have been solid and, at least as of right now, are expected to stay very strong. Despite the market's worries about a potential recession, earning estimates are forecast to rise by around 5% over the next twelve months to about $230 per share, up from roughly $220 in 2022.

{kind=link}

Bloomberg

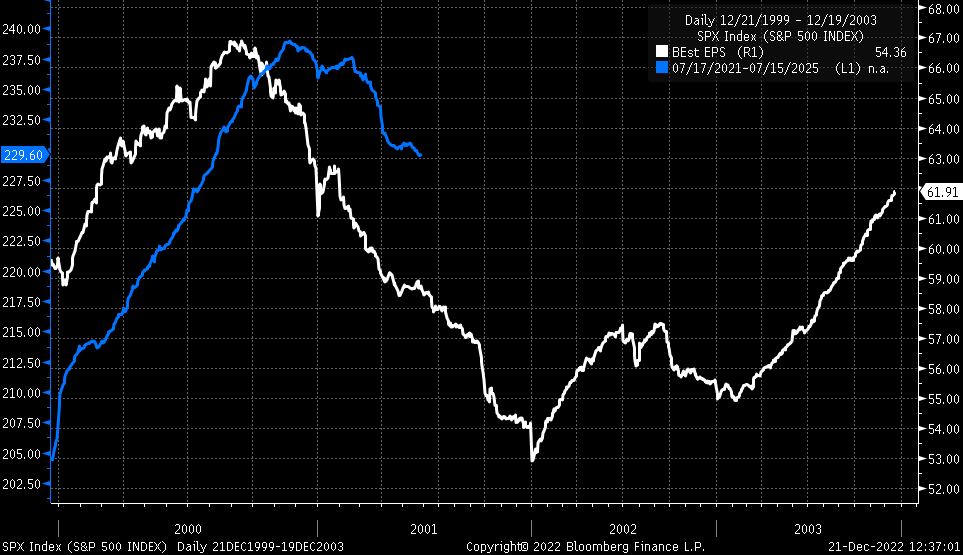

This is where the comparisons with 2001 start again because, despite the forecast for earnings growth in 2023, those estimates are trending lower and have fallen by around 4% since peaking this past June. This change in earnings estimates in 2022 and for 2023 is not dissimilar to what happened in 2001. Comparing the earnings estimate trends in 2001 and comparing them to 2022, we can see a similar type of move lower. The main difference is that the turn lower for earnings in the 2001 bear market started slightly sooner than the 2022 earnings trend reversal.

{kind=link}

Bloomberg

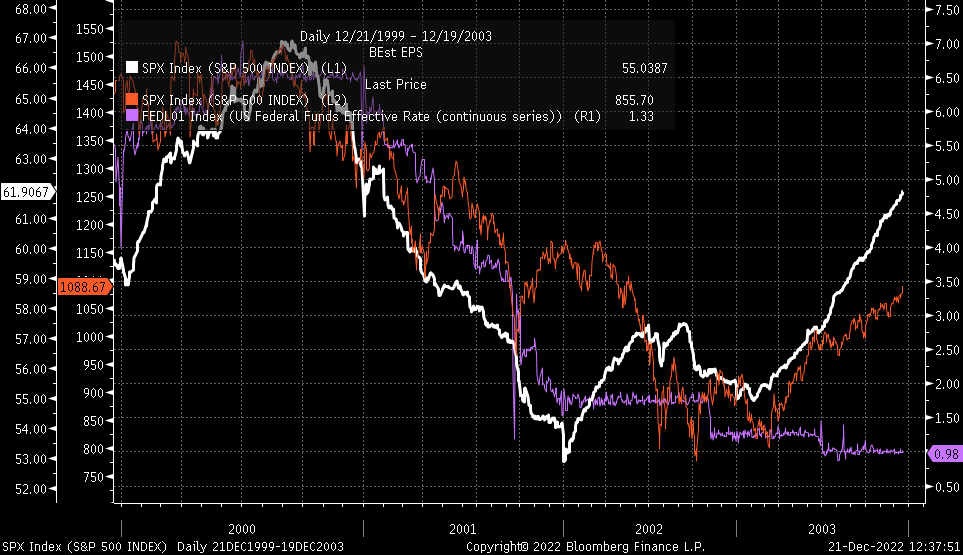

Additionally, it's worth noting that it wasn't Fed rate cuts that lifted the S&P 500 out of the bear market; it was a change in earnings estimates. The Fed cut rate multiples times during the 2000 bear cycle, but with earnings in a sharp decline, rate cuts did very little to change the direction of the S&P 500.

{kind=link}

Bloomberg

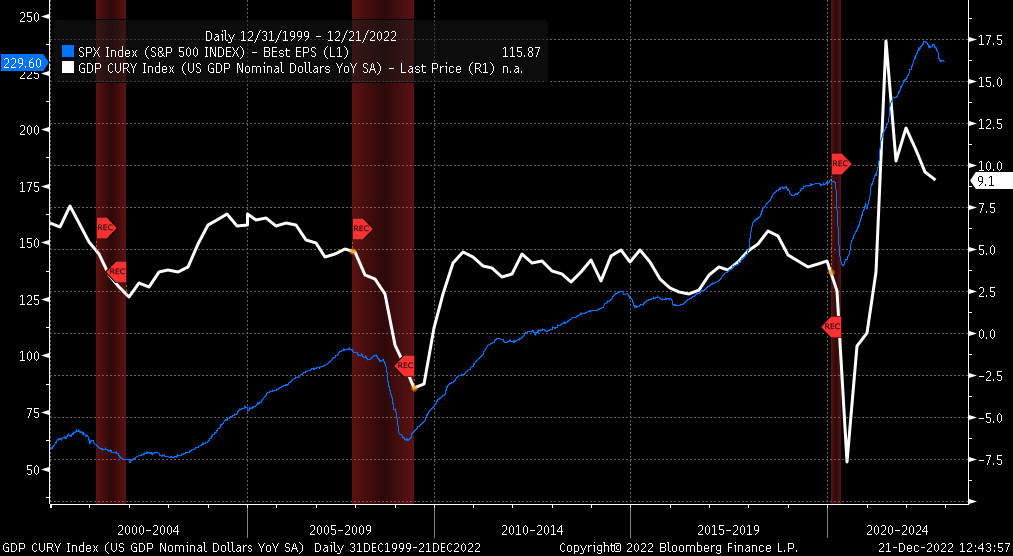

More surprising is that the recession in 2001 was pretty mild. Nominal GDP growth never even went negative. But it was a massive slowdown, with the nominal growth dropping from 7.6% in June 2000 to 2.2% by December 2001. But it still took a long time for earnings to rebound. Currently, nominal GDP growth in the third quarter of 2022 was around 9.1%; a similar slowdown in nominal GDP growth could profoundly affect earnings estimates for 2023.

{kind=link}

Bloomberg

The 2008 Scenario Not Quite The Same

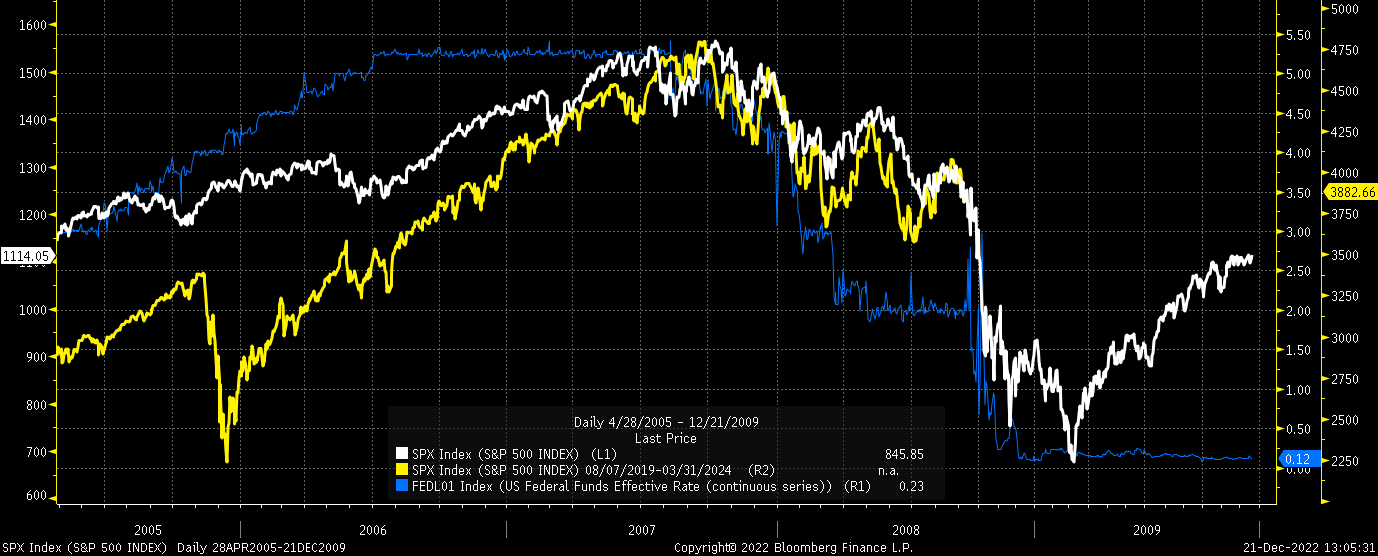

This differs significantly from the economic hit on the market in 2008, which was resounding, and the impact on corporate earnings was more significant. It was also different in that as the economy was slowing, the Fed was very slow through most of 2008 to respond to the slowing environment, resulting in the market moving lower as it was screaming for rate cuts which were slow to materialize from March 2008 until September 2008.

{kind=link}

Bloomberg

I discussed this topic regarding 2008 during an appearance on December 20, 2022, during an interview on Making Money with Charles Payne on the Fox Business channel.

2023 Will Be About Earnings

In 2023 the narrative is likely to shift from rate hikes and bad news being good news to bad news being bad news. Weaker economic data will not be positive because the market thinks the Fed will stop raising rates but will shift to the market demanding the Fed cut rates as corporate earnings decline.

The good news is that the Fed probably does bring inflation down in 2023. The bad news is that with falling inflation rates, nominal GDP growth will fall, and as a result, earnings will fall too.

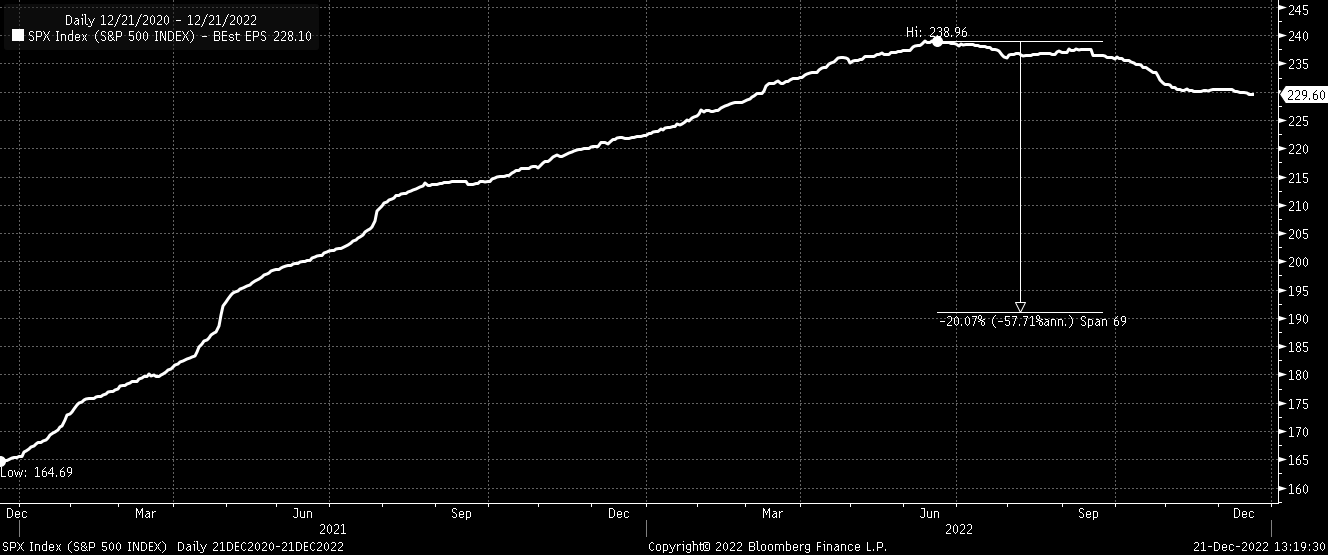

How much earnings truly fall is anyone's guess. But from the peak in September 2000 through December 2001, earnings estimates for the S&P 500 dropped by around 19%. That would equate to earnings in 2023 falling from around a peak of $238.96 in June 2022 to about $191.22 in 2023.

{kind=link}

Bloomberg

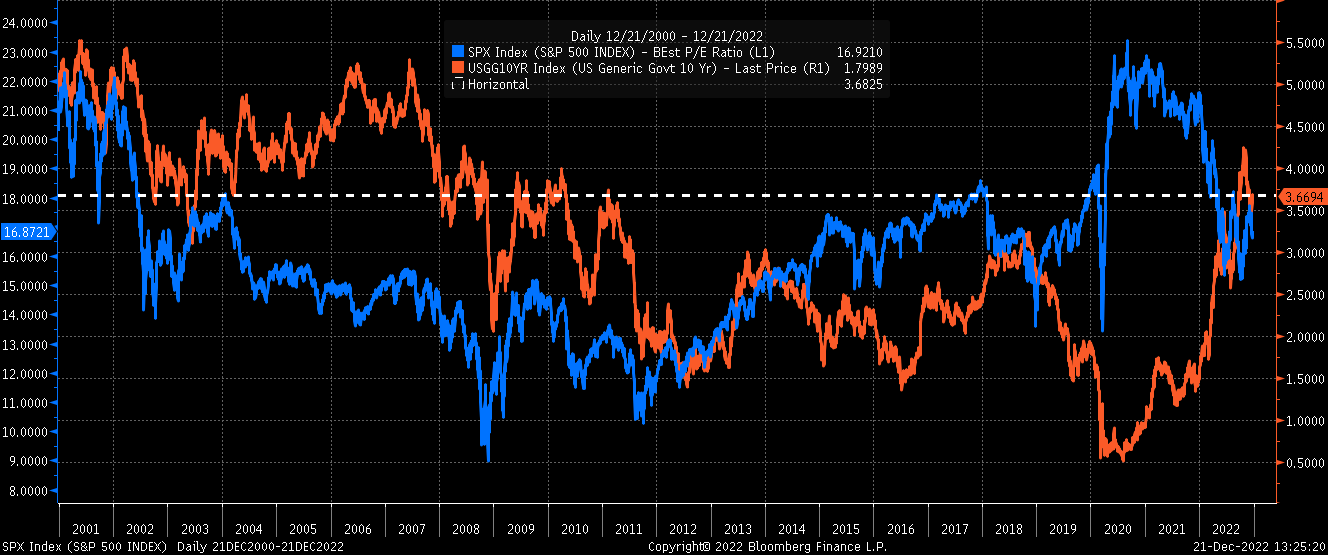

Without getting overly complex on the earnings and using the current 2001 analog, it would suggest we probably see the S&P 500 bottom around 14 times its 12-month forward earnings estimates. When accounting for rates, that is easy, too, because it may come as no surprise that the 10-Year rate in 2001 was around the same level as in 2022 and could very well be throughout a good portion of 2023.

{kind=link}

Bloomberg

So assuming earnings of around $195 per share by the time we get to the end of 2023 and a 14 PE ratio, the S&P 500 could end up bottoming out somewhere around 2,700, assuming earnings come in that low.

But if there's no recession, and we are just entering this period of slow to no growth, where the nominal GDP growth cools, and earnings are flat and stay around $220, you're still looking at an S&P 500 that trades somewhere around 3,000 to 3,100 given a 14 PE.

The most important thing to think about at this point is that from a valuation perspective, the market isn't cheap trading at 17 times the next twelve months' earnings estimates, especially given the lack of clarity on where those earnings will be and, more importantly where Fed monetary policy will be.

So if the bear markets of 2000 and 2008 continue to play out as they have thus far through 2022, then there seems to be a good chance that 2023 may be worse than 2022.

For further details see:

The Stock Market Faces An Even Steeper Decline In 2023