WMT - The Tao Of The Dow Simple Self-Indexing Strategy

2023-03-19 06:15:45 ET

Summary

- This article covers a simple self-indexing fund management practice originally discussed in the early editions of The Intelligent Investor.

- The strategy covers the DJIA 30.

- With the Dow Index now owned by Standard & Poor's, the S&P 500 and DJIA 30 seem to mimic one another even more closely than ever.

Ben Graham's original advice

For those of you that have read Benjamin Graham's Intelligent Investor , there are many things to take away from the book. In most articles that I see referencing the book, most takeaways have to do with market psychology quotes like: "In the short run, a market is a voting machine but in the long run, it is a weighing machine."

These are all helpful, but few pay attention to the stock valuation sections or the indexing sections. While later additions have added diversified mutual funds and ETFs to the mix in the section that includes the "investors contract", much of the original language had to do with buying the Dow 30 as your index fund strategy. The contract, for those unfamiliar, is a dedicated part of the book where you write in your preferred mutual funds, sign it, and dedicate yourself to holding them for a minimum of 10 years to experience the compounding effect. You can only sell if you need funds to cover an emergency or planned expense.

The contract is a great psychological tool for those that are superstitious about wealth accumulation (I think we all are a little bit). However, most of the language in the early part of the chapter has to do with Ben Graham's indexing of the Dow 30. The index is unique in that it is price-weighted rather than market-cap-weighted. While some have ridiculed this index formation strategy, we need to understand that investors of that era had no access to complex allocation tools. Buying 1 share of each of the best blue chips of our economy, over and over again, was the way to go.

Boggle takes over

Expounding on the original Intelligent Investor , John Bogle steps in from stage right to say a smart portfolio is all diversified mutual funds with the more diversification the better. Common Sense on Mutual Funds is a good book that addresses this. Being that Bogle came along later, around the same time as Warren Buffett, he had more access to analytical tools and was able to establish the first true index fund while he was CEO at Vanguard. The goal was to track the 500 stocks of the S&P 500 like ( VOO ) or ( SPY ) does, in mutual fund form. Later this diversification grew to include a total stock market index like ( VTI ), which became the fan favorite of the Boggle Head index fund movement.

However, Bogle himself has said he disliked the ETF product versus the mutual fund product as it was extremely liquid. This led to shorter holding periods by investors versus their mutual fund predecessors. Love it or hate it, ETFs will certainly phase out mutual funds over time. Liquidity is king and patience is in limited supply.

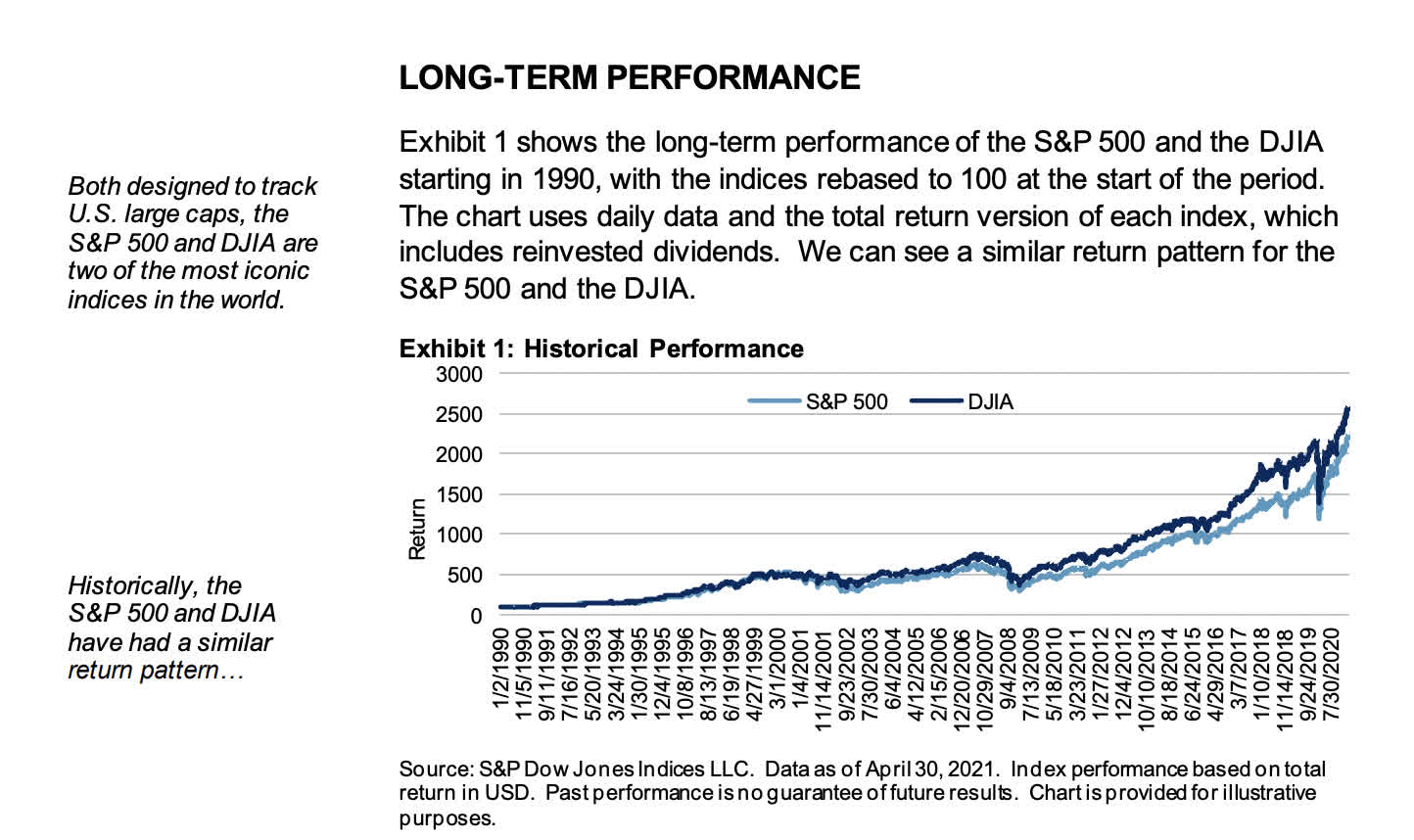

The performance

According to S&P Global ( SPGI ), the owner of many of the index creations, they had this to say about the S&P 500 versus the Dow Jones Industrial Average:

The S&P 500 and DJIA have similar long-term risk/return profiles, and their three-year rolling correlations are high. However, there are important differences between the two indices that investors should consider.

• Number of constituents

• Size of the component companies

• Weighting scheme

• Sector representation

• Fundamentals

• Factor exposures

We will start by exploring areas in which these iconic indices are similar and then delve into the differences.

{kind=link}

S&P Global

Cost vs market cap weighting

Nowadays, most brokerages have zero-commission trading. One of the prohibitive qualities of buying individual shares yourself used to be related to $6-$7 commissions per trade that would only be eliminated for very large portfolio sizes. That was also an awesome reason to advocate for mutual funds and ETFs, pay your commission once with one big trade, and get all your diversification in the same shot.

The above is one of my main arguments as to why everyday small investors may want to begin to dabble in individual names because the cost is no longer a factor. However, matching the S&P 500 is 500 stocks and market cap weighted. You would most likely need a computer program to advise you how to spread x amount of dollars across the 500 names to match the index. Even if you had the capital to do so, truly matching the index would need reallocation of capital from time to time to match the market cap weighting. A very difficult, if not impossible task for most of us.

The Dow 30 is comprised of the top 30 blue chip quality names weighted by price and diversified across virtually all US economic sectors. Therefore the stock with the highest price, as of today, March 18th, 2023, is UnitedHealth ( UNH ) at $469.5 a share and has the highest weight.

| MICROSOFT ( MSFT ) |

| 279.43 |

| WALMART( WMT ) |

| 139.4 |

| HOME DEPOT( HD ) |

| 288.39 |

| VERIZON( VZ ) |

| 36.79 |

| CISCO( CSCO ) |

| 50.19 |

| PROCTER AND GAMBLE( PG ) |

| 142.93 |

| VISA( V ) |

| 217.39 |

| NIKE( NKE ) |

| 120.39 |

| COCA-COLA( KO ) |

| 60.02 |

| UNITEDHEALTH GROUP( UNH ) |

| 469.5 |

| APPLE( AAPL ) |

| 155.00 |

| IBM( IBM ) |

| 123.69 |

| BOEING( BA ) |

| 201.05 |

| JOHNSON & JOHNSON( JNJ ) |

| 152.38 |

| 3M ( MMM ) |

| 103.02 |

| WALT DISNEY( DIS ) |

| 93.20 |

| INTEL( INTC ) |

| 29.81 |

| MCDONALD'S( MCD ) |

| 267.20 |

| CHEVRON( CVX ) |

| 152.34 |

| SALESFORCE( CRM ) |

| 184.85 |

| WALGREENS( WBA ) |

| 32.91 |

| CATERPILLAR( CAT ) |

| 215.01 |

| DOW( DOW ) |

| 50.02 |

| AMGEN( AMGN ) |

| 229.79 |

| HONEYWELL( HON ) |

| 184.64 |

| AMERICAN EXPRESS( AXP ) |

| 156.52 |

| MERCK( MRK ) |

| 104.10 |

| GOLDMAN SACHS( GS ) |

| 303.54 |

| JPMORGAN CHASE( JPM ) |

| 125.81 |

| TRAVELERS( TRV ) |

| 165.03 |

Above is the price for the DJIA 30 as of March 18th, 2023. The total amount it would take to buy all 30 names by price weight would be $4,831.37. Certainly, an amount most investors on Seeking Alpha can afford to match.

The strategies

Although we can all afford to match the index, the majority of us do not plunk almost $5 grand into the market on a weekly or even monthly basis. Here are a couple of good dollar cost-averaging strategies:

- Buy the most beaten-down names first. Open a year-to-date chart of the Dow 30 and find the names down the most. Buy those first as they are relatively cheaper from a technical perspective than the rest in that index at the time. If you already own all 30 in a portfolio, just sort them by the most negative return to the most positive and buy the most negative ones first.

- Buy the highest yields first. Similar to the Dogs of the Dow strategy, where you buy the top 10 yields in the Dow on an annual basis, you can also sort by yield which changes with price. As the yields change daily, focusing on the highest yields first is also a sound strategy.

I personally dollar cost average from the most negative names to the most positive. Either of the above two is advantageous over an ETF or mutual fund that is just trying to match the index with the funds rather than beat it. Slight tweaks to indexing such as this can result in Alpha to the index you are tracking.

Compounding periods

From Investopedia :

The effects of compounding strengthen as the frequency of compounding increases. Assume a one-year time period. The more compounding periods throughout this one year, the higher the future value of the investment, so naturally, two compounding periods per year are better than one, and four compounding periods per year are better than two.

This is what I love about the strategy and something very difficult to quantify. Mathematical formulas prove that the more compounding periods, the better. When you are invested in an ETF, the manager typically puts the dividends in a trust to be paid out quarterly rather than putting those dividends directly back into a reinvestment plan with the underlying holdings. You then have the option to reinvest those funds for which the manager can buy more shares of the index they are tracking with the cash you give back to them. But this only happens once per quarter in most cases. If you own all the shares, you will be reinvesting the dividends in real-time as they come in and increase your compounding periods.

As prices also dip when a dividend is distributed, that is also an optimal time to have a reinvestment. ETF index funds are at a disadvantage.

What to do with an exiting stock

Since this index is only 30 stocks, tracking new members coming in when there is one exiting is huge mainstream news. Very easy to track. You have a couple of choices in this instance, either A: liquidate the exiting stock and buy the new stock with the proceeds, or B, hold the stock if you still like it and just stop buying it on subsequent rounds, buying the new entrant instead.

Flexibility

A large majority of my portfolio follows the DJIA 30 self-indexing strategy. I also enjoy the flexibility aspect of it where if I want liquidity to buy something else, it's my choice on what I want to sell. Maybe I want some tax write-offs and sell my losers, maybe I think one name is too overpriced and needs to be sold and wrapped into a different name.

The options are as numerous as your creativity. If you like to write puts or calls, you also have more names you can write those puts and calls against with a wider variety of premiums. If you sell an index fund on the other hand, you are selling all the names at once and have no choice if you want to take gains or losses. The liquidation result is whatever the ETF is at the time of sale, in the red or the green.

Conclusion

Another issue that is worth discussing these days is, what happens if your mutual fund or ETF manager becomes insolvent. I've been laughed at for this question before, but with banks failing and some wealth managers being questioned about their balance sheets as well, this discussion comes back to my mind. SIPC insurance protects investors against fraud, whereas FDIC insurance protects against capital loss at a bank. One key difference between stocks and cash is, that cash is the bank's asset, and stock is your asset. Unless you give explicit consent for the bank to lend out your shares, that asset remains yours and should be yours in the account no matter what happens. In the case of insolvency, those shares should be directly transferred to a solvent institution unless the brokerage committed fraud and didn't buy the shares or lent them out without authorization.

The above is my understanding of how FINRA requires a wealth manager to handle insolvency, I could be wrong as this is a murky and untested area. However, if you owned an ETF run by a failed institution, what would happen? Would the pie be divided and shares given to investors? Would the ETF have to liquidate and send proceeds to investors? Hard to say. I do own a lot of ETFs but also feel that owning a lot of individual names not under a fund is also a hedge against any of the above-mentioned issues.

This self-indexing strategy is a favorite of mine and one that I hope novice and even advanced investors would consider. If you thumb through enough 13F forms of hedge funds and institutions over time, you'll realize even Berkshire Hathaway ( BRK.A )( BRK.B ), looks a lot like the DJIA 30.

For further details see:

The Tao Of The Dow, Simple Self-Indexing Strategy