KHC - The Terrific Ten: The Foundation For My Dividend Growth Portfolio (Part 3)

2023-05-31 07:00:00 ET

Summary

- The Terrific Ten’s average yield is 2.66%, and the average 5-year dividend growth rate is 17.52%.

- Every member of the Terrific Ten recorded total returns that beat the S&P over the last five years.

- The other eight tickers in the Terrific Ten are WSM, TSCO, HD, TSM, AVGO, SCHD, AMT, and PLD.

This article was published at iREIT™ on Alpha on Monday May 29, 2023. This article was written by Chuck Walston.

The Terrific Ten is list of companies that make up the foundation of my investment strategy.

Although I own approximately 125 stocks, these companies constitute over 20% of my portfolio .

With two exceptions (one of which is an exchange-traded fund, or ETF), the Terrific Ten are each rated as possessing a moat by Morningstar. Furthermore, each of the companies sports investment grade credit ratings.

If you choose to peruse each of the five articles in this series, you will see that the bulk of my selections dominate their respective industries.

While the stocks I highlight today, Lowe's Companies, Inc. ( LOW ) and The Kroger Co. ( KR ) are experiencing macroeconomic headwinds, I believe the growth runway for the two will provide me with market beating returns over the long haul. In fact, over the last five years, every single member of the Terrific Ten has total returns that beat the S&P 500 Index (SP500).

And in addition to the growth prospects for both stocks, you will find that they also exhibit the strengths I enumerated above.

Lowe’s Reported Earnings This Week

The middle of this month, rival The Home Depot, Inc. (HD) reported quarterly earnings that included a sales miss and weak guidance.

A couple of days ago, Lowe’s followed with its Q1 earnings report . Management also lowered guidance for the fiscal year, but unlike HD, the firm beat on sales . EPS of $3.67 topped the $3.45 consensus, while $22.35 billion in sales also beat the $21.68 billion analysts’ forecast.

Those numbers represented a 5.5% drop in revenue over the comparable quarter; however, bolstered by cost controls, net income fell just 3%. A fairly robust share buyback program was a factor in the improved EPS.

Comparable sales dropped 4.3%, largely due to unfavorable weather and lower prices for lumber. Management expects weather related headwinds to result in a bit of delayed demand that should bolster sales next quarter.

Gross margins were down 35 basis points to 33.7%, but operating profit margins improved by 70 basis points to 14.7%.

Management revised guidance for fiscal 2023 downward. Revenue is now projected in a range of $87 billion to $89 billion, a billion dollars below the previous forecast. Earnings are now expected in a range of $13.20 to $13.60, $0.40 per share less than the previous estimate. Same store sales are expected to fall by 2% to 4%.

Lowe’s boasted that Pro sales recorded positive comps. This builds on a 22% jump in Pro revenue in Q1 of last year.

The results of an April survey found 75% of Pros reporting healthy backlogs, although consumers are shifting to smaller projects.

…while we are seeing lower-than-expected DIY discretionary demand, we are also driving better-than-expected results in Pro and continued strength in our online sales and core categories like appliances and paint. This reinforces our confidence that we will continue to take market share and outperform the broader market.

Brandon Sink, CFO .

Perusing the earnings transcript reveals Lowe’s has the best employee staffing levels in three years, and that the company has the highest customer satisfaction scores in the firm’s history.

What Makes Lowe’s Stand Out

Lowe's, along with Home Depot, is a member of a near-duopoly. By contrast, Menard’s, the third largest home improvement retailer, only has about 350 stores in 15 states, less than a sixth of Lowe’s store count.

Lowe’s size provides a scale advantage that results in lower costs in products, advertising, and logistics. In turn, Lowe’s can undercut the prices of smaller rivals while at the same time reaping larger margins.

Lowe’s product lines are generally resistant to ecommerce competition. Even so, 10% of the firm’s sales in FY 2022 stemmed from ecommerce, up from 5% in 2018. The increased ecommerce sales largely consist of buy-online-pickup-in-store ((BOPIS)) products (estimated $1.2 billion in sales in Q3) that most ecommerce sites do not carry. However, BOPIS serves to drive additional store traffic.

Aside from carrying a great deal of merchandise that is near ecommerce proof, about two-thirds of the retailer’s products are non-discretionary.

There are a number of factors that indicate Lowe’s has a lengthy growth runway. For one, the U.S. is chronically short of homes, which results in aging housing stock. Half of all U.S. homes are at least 41 years old. Homes reach their “prime” remodeling period when they are 20 to 40 years old. That translates into an estimated 24 million homes that are in need of repairs and/or upgrades.

Aside from the age of homes, there are other factors coming into play. The work from home movement is an impetus for home remodeling, as is the propensity for seniors to age in place. The first trend moves homeowners to remodel to accommodate an office environment. The latter has folks installing features that improve access.

There is also a large segment of the population that is locked into low interest loans and are reluctant to move from their homes while mortgage rates are on the rise. Many of those homeowners are motivated by robust home equity levels, $330,000 on average. In a trend known as “improve in place” a substantial percentage of those folks are taking out loans for remodeling projects.

"Remodeling is slowing, but there's a historic boom coming."

Eric Finnigan, VP at John Burns Real Estate Consulting.

Despite ranking as the second largest company in the industry, Lowe’s only holds 10% of the U.S. remodeling market. That alone translates into a potentially long growth runway, but Lowe’s exhibits additional strengths.

As FY22 came to a close, the firm owned 84% of its stores, including those on leased land.

Lowe’s also has a hearty appetite for its own stock: since 2013, the company repurchased 44% of the shares outstanding. The stock buybacks boosted EPS by 508% over the last decade. In FY 2022 alone, the firm bought back 71 million shares at a cost of $14.1 billion.

{kind=link}

Next up: Kroger

Like most of the stocks that comprise the Terrific Ten, Kroger has a scale advantage that gives the company leverage with suppliers and advertisers and also serves to lower logistics costs. Due to the very low profit margins endemic to the grocery business, adding scale provides a pivotal advantage.

Assuming the proposed deal to acquire Albertsons Companies, Inc. ( ACI ) is approved, Kroger’s scale advantage will improve significantly. Financed through cash on hand and a $17.4 billion bridge loan, the addition of Albertsons will result in a company with approximately 5,000 stores, 4,000 pharmacies, 2,000 gas stations, and 710,000 employees.

Adding Albertsons would also bolster Kroger’s omnichannel and fulfillment infrastructure by adding 2,100 curbside pickup locations and the 31 million members of Albertsons' loyalty member program.

Furthermore, KR can boast of additional strengths: the company has a wide ranging and growing private labels business. If Kroger’s store brands were a separate entity, they would rank as one of the largest packaged food companies in the U.S., on par with The Kraft Heinz Company ( KHC ).

However, the firm stands out in that unlike many retailers that provide in-store brands, many of Kroger’s private labels are produced by the company. KR now operates 35 food production or manufacturing facilities churning out private brands, and those products generate significantly higher profit margins.

Private labels now generate about 30% of the company's total food sales. That is well above the industry average of less than 20%.

I’m of the opinion that the current macroeconomic environment, marked by high inflation, will drive many consumers to adopt private label grocery brands. This could result in a long-term advantage for KR.

In terms of web sales, Kroger also ranks as the third largest e-commerce site in the U.S.

To evaluate the edge Kroger holds over the competition, one should compare the company’s results to Albertsons, the second largest pure play grocer in the U.S.

In 2021, Kroger reported $825 in sales per square foot to Albertsons’ $635, and KR’s top line is nearly double Albertsons’. You will also find that Kroger turned inventory close to 16 times in 2022 versus 11 times for Albertsons.

Kroger also owns about 45% of its stores, including ground leases.

{kind=link}

Debt, And Dividend

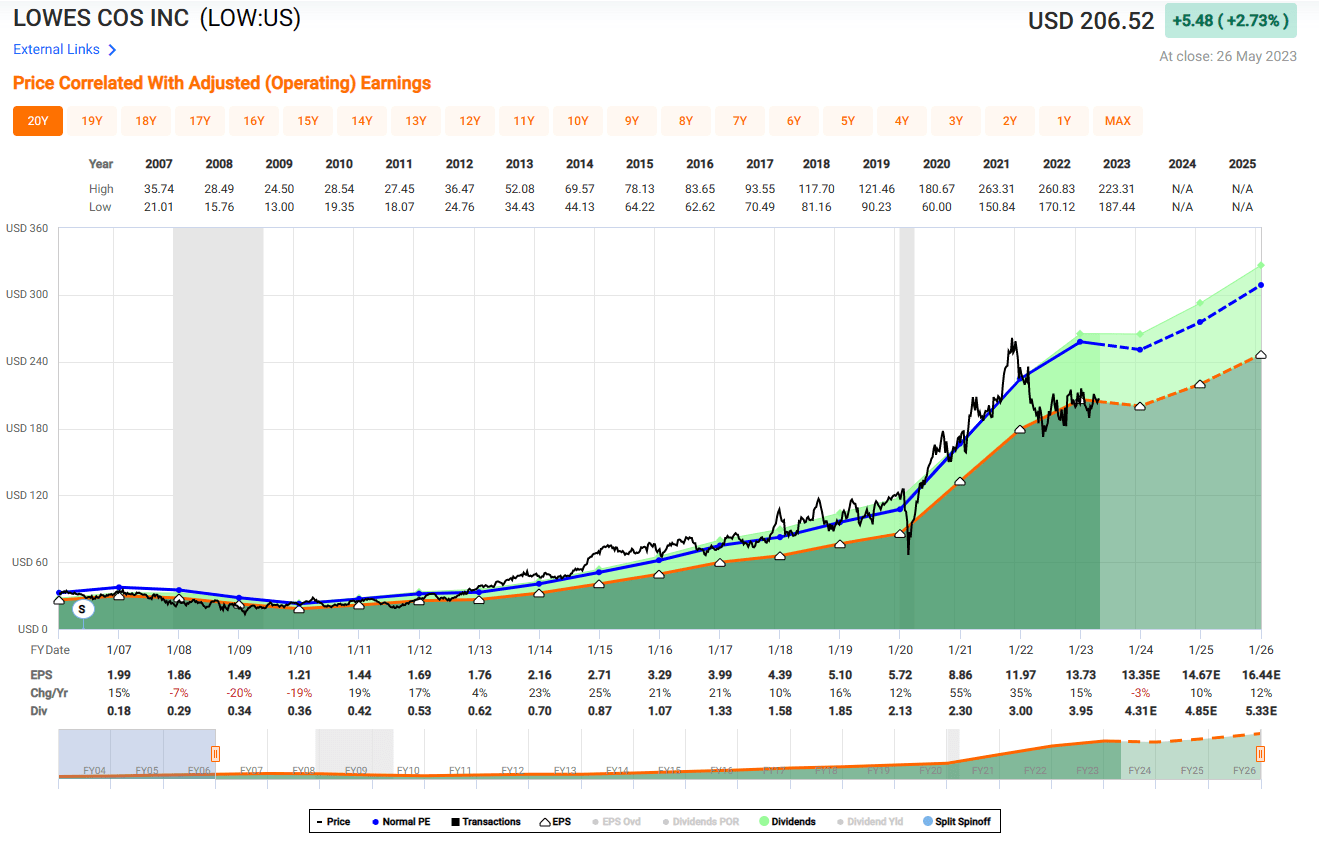

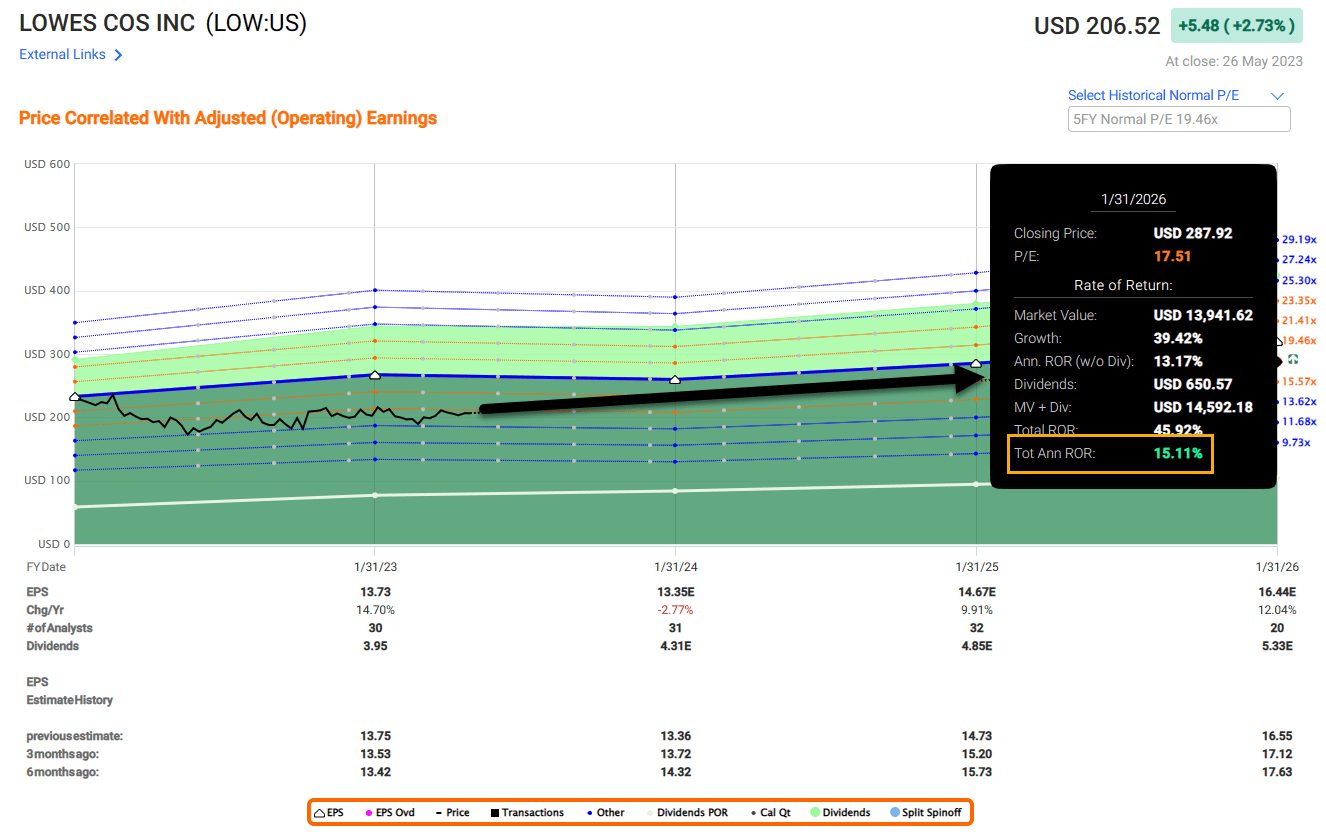

Lowe’s yields 2.06%. The payout ratio is a tad above 30%, and the 5-year dividend growth rate is 20.69%.

Lowe’s 5-year PEG stands at 1.24x versus the 5-year average PEG for the stock of 1.04X. The forward P/E for Lowe’s is 15.23x, well below the average P/E over the last 5 years of 18.42x.

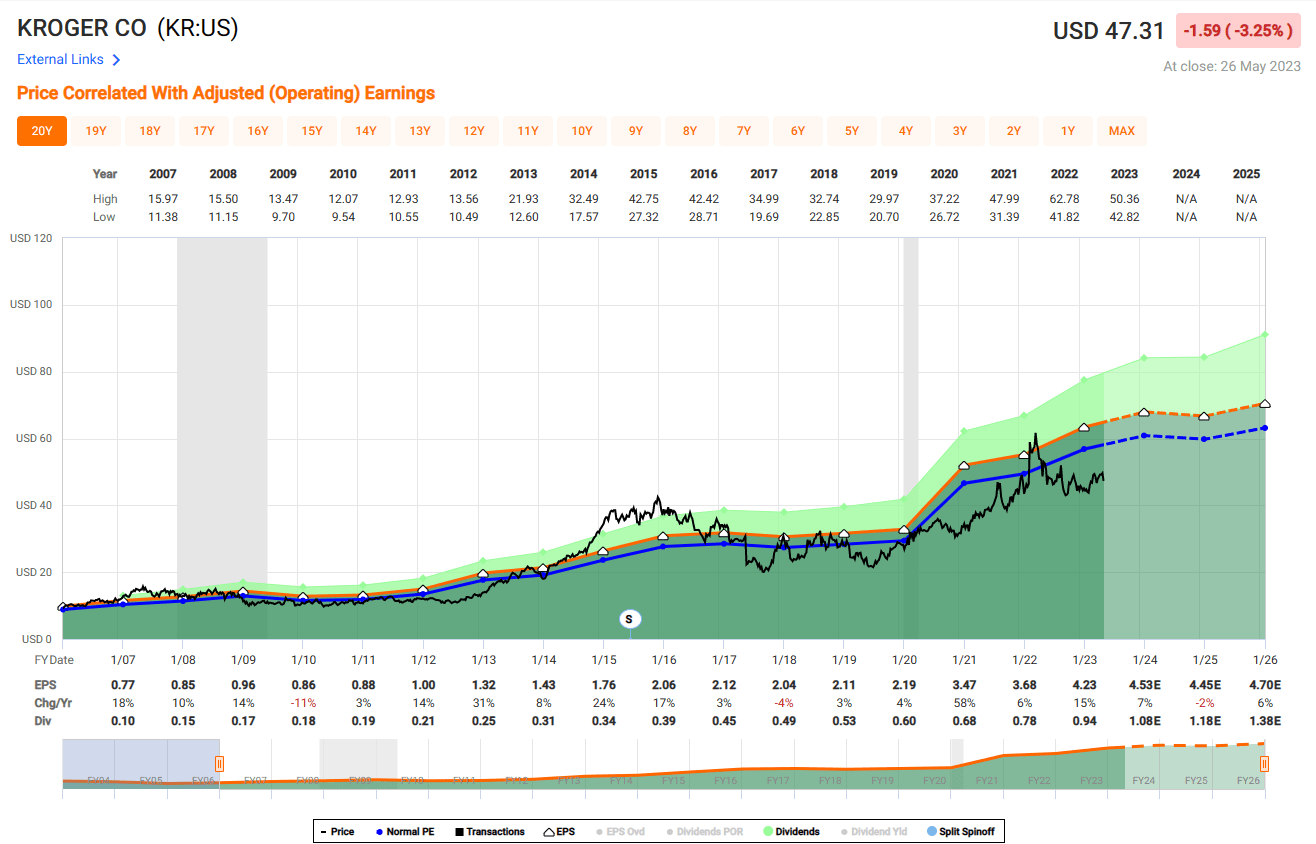

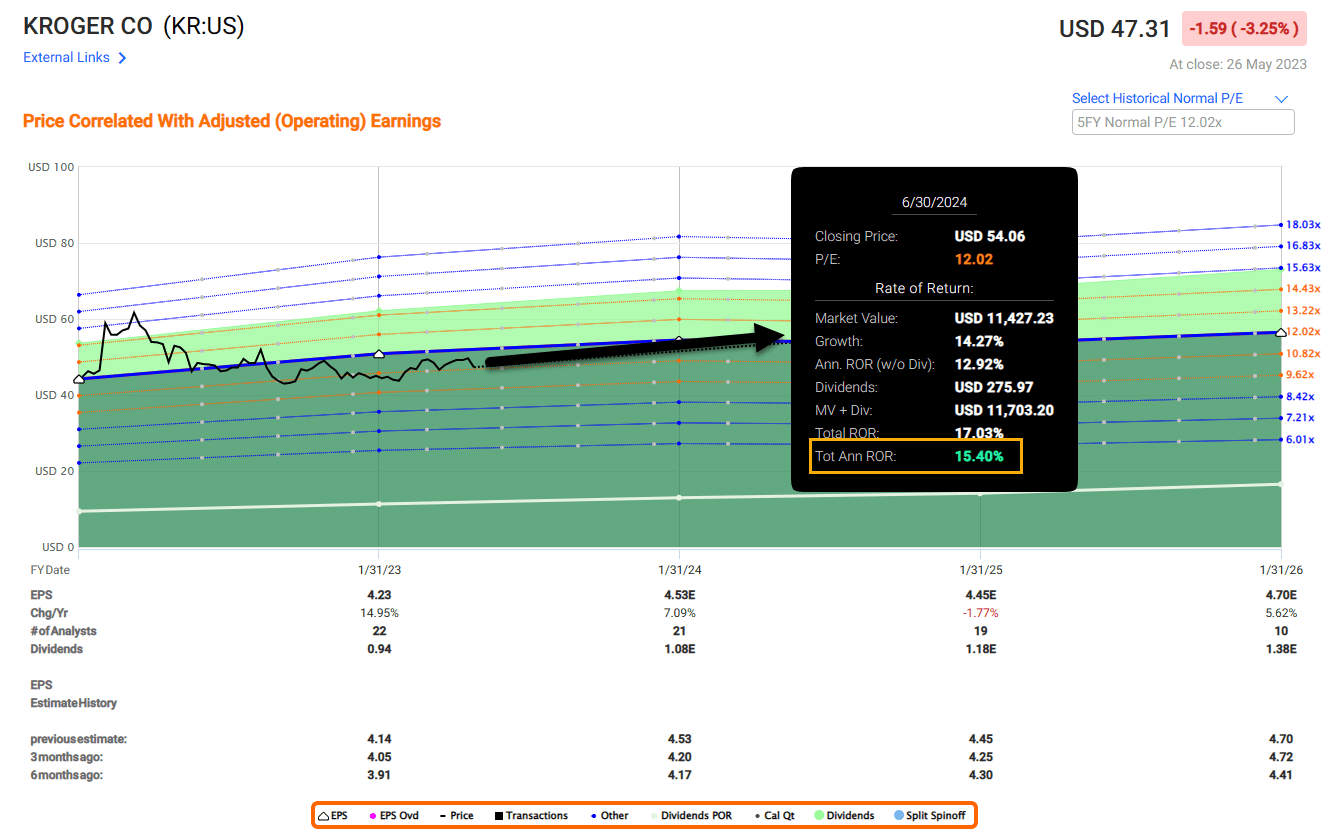

KR has a 5-year PEG of 1.74X, on par with the 5-year average for the stock of 1.80x. Kroger’s forward P/E is 11.07x, a bit below the 5-year average for the stock of 12.44x.

Summing It All Up

I rate both Lowe’s stock and Kroger stock as reasonable buys. This is based on the strengths of both companies, the prospects each has for continued growth, and the current valuations of each stock.

Readers may note that I rated almost all of the Terrific Ten as buys. Perhaps that comes as a surprise considering I and others believe a recession is on the horizon.

{kind=link}

However, despite the current and likely future macroeconomic headwinds these firms are experiencing, I readily acknowledge that I cannot predict the movements of the stock market, nor of future share valuations of individual companies.

What I can accomplish with some degree of success is to identify top-notch businesses with valuations that are well below historic norms.

So I must ask myself, should I wait for a bull market to buy? To do so may mean that I end up investing in the same companies at roughly equal or even less attractive valuations.

{kind=link}

Count me as one that is willing to invest in solid businesses that are experiencing transitory headwinds, be they company specific or of a macroeconomic nature.

That's my story…and my investment philosophy, and I’m sticking to it.

For further details see:

The Terrific Ten: The Foundation For My Dividend Growth Portfolio (Part 3)