SQM - The Theme For 2023 Is Energy Security So Buy SQM

Summary

- Sociedad Química y Minera is a low cost lithium producer currently benefitting from an explosion in demand for electric vehicles and battery storage systems.

- The underappreciated opportunity is grid storage investment in 2023 as countries look to make power networks more resilient.

- SQM is more diversified than most lithium producers with significant earnings from fertilizer, iodine and potassium making it less exposed to the lithium cycle.

- The valuation is attractive at current levels with a strong 9% yield and low multiples and is one of our key picks for 2023.

- We are buying now and below $90 per share.

The lithium opportunity for SQM is attractive

Sociedad Química y Minera (SQM) is a Chilean lithium and chemicals company. In particular, we believe that lithium battery demand will continue to explode due to EV (electric vehicle) and power storage demand. This makes SQM in particular one of our key picks for 2023, despite its 60% gain this year.

The case for SQM

- Lithium demand is booming now but prices have been cyclical in the past.

- Operational performance has been good for SQM and the future bright.

- SQM is a lead producer of iodine, potassium nitrate and fertilizer.

- Copper price weakness of early 2022 may return in 2023 as China construction eases further, and that is good for SQM's margins.

- Fully 80% of SQM's lithium is sold at market prices.

- The valuation for SQM looks attractive at current prices.

Recent weakness is a good entry point.

Many lithium miners have fallen in recent weeks and are now well off their highs for the year. This might be due to Tesla ( TSLA ) reported sales incentives or a small fall in lithium prices in China. Both can be explained.

Our opinion and some anecdotal evidence suggest that Tesla's democratic leaning customers are increasingly bothered by Elon Musk's Twitter controversies. Finding a new CEO will help . Further the massive COVID surge in China right now will temporarily crush both consumer demand and production until probably at least Chinese New Year in mid February.

So let's look past the short term noise moves to the bigger picture.

Lithium demand is booming but the price can cycle hard.

Let's put a key fear of bears up first. Lithium prices have crashed hard before.

As recently as 2020 lithium was in an awful bear market, down 70% from its peak in early 2018. Marginal producers went out of business.

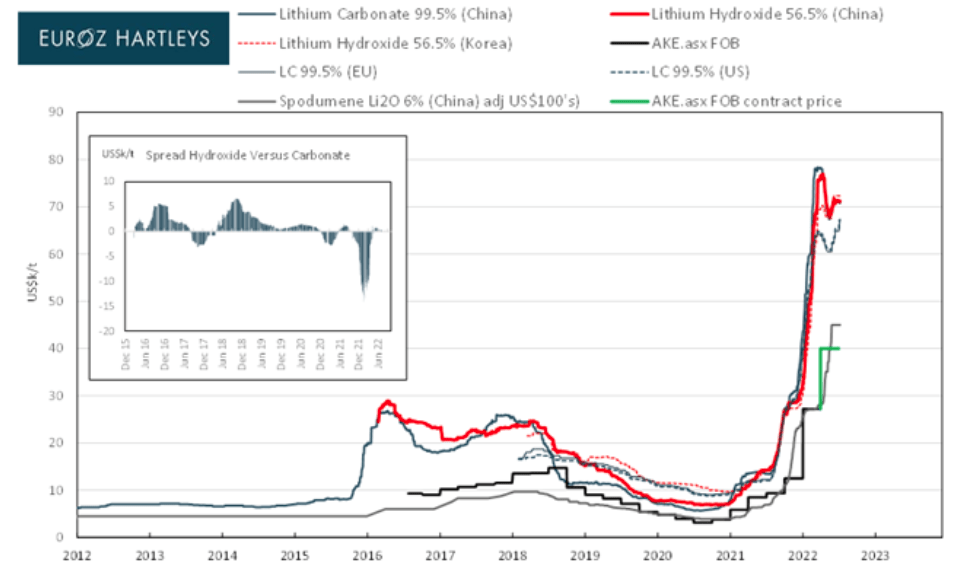

Lithium Price History (Euroz Hartleys)

{kind=link}

That was after a correction in 2016. Twice burned, three times shy?

Of course, the recovery since then has been astounding.

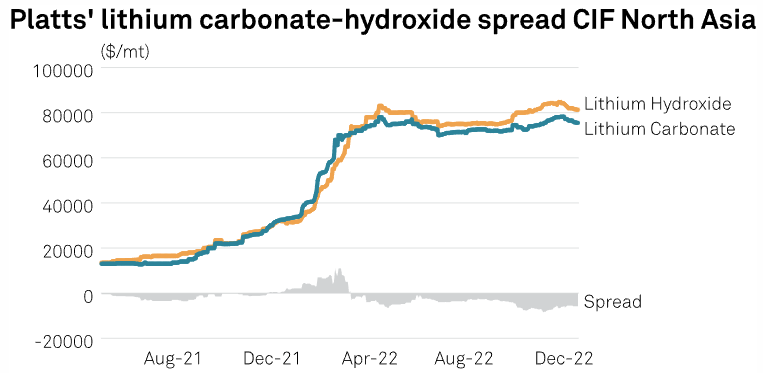

Lithium this year has risen and remained at exceptionally high (in historical terms) prices. Battery makes seem to be paying as much as they can bear.

Lithium Prices 2022 (SP Global Commodity Insights)

{kind=link}

Still, big rises in commodities should always be questioned. Is another crash coming? Eventually yes, but it's hard to see it in the immediate future.

Here is just one forecast from dozens available showing a shortages for years.

Lithium Supply vs Demand (Bloomberg)

Lithium forecasts are both difficult and controversial. Just last week the Australian government forecast a fall in price in 2024. But other forecasts are more bullish forecasting deficits for years.

In our experience most demand side forecasts start with a methodology of "demand similar to last year with incremental growth of a similar rate." This often means forecasts can be badly wrong when a market reaches a phase state change. When demand jumps due to broad market acceptance.

We are more bullish than forecasters because:

- EV sales might have reached a tipping point in the US.

- Governments are worried about energy security , and this will drive investment in green energy and storage to smooth supply.

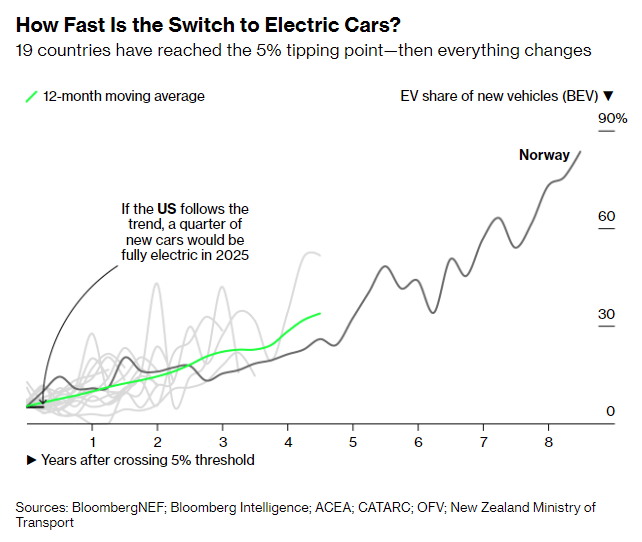

EV sales may have reached a tipping point

You don't need to be Malcolm Gladwell to know that markets can suddenly accelerate once they pass a tipping point. For EV sales, 5% of overall sales, like the US did recently pass, might be such a point.

EVs are reaching a tipping point (Bloomberg)

{kind=link}

Another trend that has been identified is that EV sales accelerate quickly for a car manufacturer once 10% of sales are achieved. Probably as a result of efficiencies of scale. Outside the US, many major automotive companies have breached the 10% mark and could reach 30-40% inside 2 years.

EV Car manufacturer Sales (Bloomberg)

{kind=link}

Energy security is driving grid storage demand

One of the key lessons of 2022 is that gas and energy supply is a key lever for some politicians, such as Putin , to intimidate and coerce. Europe has struggled to deal with its dependency on Russia's energy. Solving that will take billions of investment in both fossil fuels as well as well as renewables.

When you think of renewable investment like solar and wind you need to start thinking of grid scale batteries to smooth the flow. It's almost an understatement that the volume of batteries required could be vast. For this reason we think forecasts for battery demand in 2023 and beyond will underestimate grid storage battery demand.

Even in energy rich Australia, recent grid instability has caused household battery system demand to jump by a massive 400% in Q3 2022 over the previous quarter according to SolarEdge Australia and other suppliers.

Currently sales are four times [greater] than the second quarter of 2022 already and our third quarter allocations are already exhausted!

Australian household battery demand alone won't move the global needle but with one of the highest household solar installation rates in the world, we think it is a sign of things to come as grids come under pressure. In Europe, it is more likely to be governments and companies driving demand.

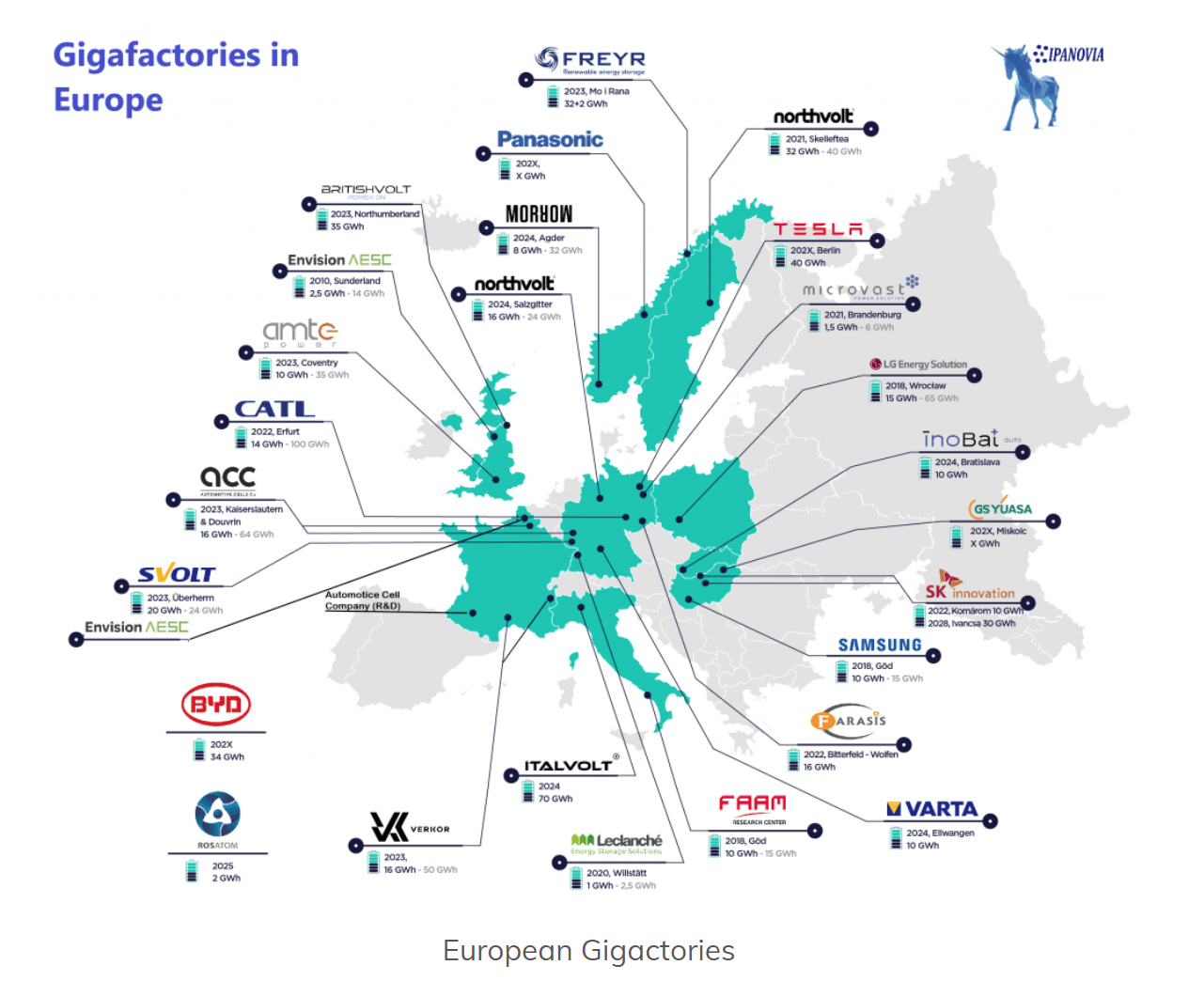

Just to focus on Europe for a second, it is investment into battery gigafactories and their capacity is the current limitation. For Europe more than 30 billion Euro of investment is planned with more than 200 GWh in annual capacity.

European Gigafactory investment (Ipanovia)

{kind=link}

Keep in mind north Asia including China is at least the same size as Europe when it comes to batteries. There are also some forgotten investments in South East Asia .

Back to fundamental demand drivers. Russia blocked most gas exports to Europe from September. For Germany, a country that relies on both Russian gas and almost 50% of its power supply on renewable power , investing in everything is required. Storage to balance renewables in 2023 and beyond must be part of the solution.

EV supply constraints will be unwound soon (probably)

Supply disruptions have reduced EV supply and thus also lithium demand. The mass outbreak of COVID since the abandonment of COVID zero will temporarily reduce both supply and demand in China. But given how quick the spread has been (practically every China based contact of ours has had COVID in the month since mid November), a version of normality for the Chinese economy may return as soon as after Chinese New Year in mid February. This will be quite the confidence boost after years of living under the cloud of testing, lockdowns and fear of forced quarantine under the zero COVID policy.

For the wider EV market a chip shortage has crimped production and thus demand for lithium batteries. These may have started to ease as soon as the second half of 2022 according to Volkswagen although Bosch, a large automotive parts supplier, expects bottlenecks to continue into 2023 . Either way, demand is delayed and supply will eventually bounce back.

Bottom-line: We believe demand will continue to absorb lithium supply. EVs have reached a tipping point ready to grow fast, yet supply constraints have actually constrained EV consumption of lithium. Meanwhile the energy turmoil is driving investment in the backup power sources to avoid an unstable grid.

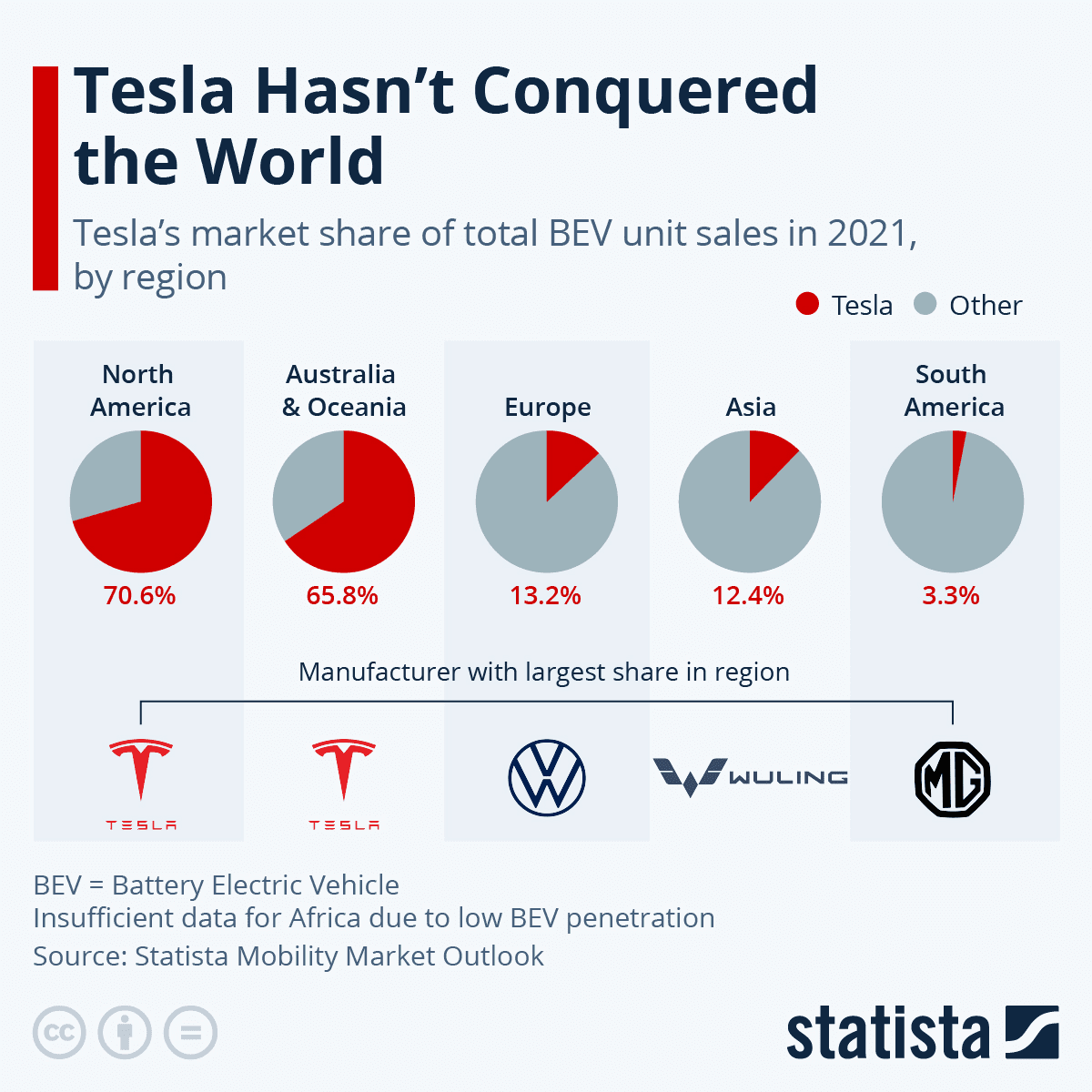

Tesla is not a great proxy for EV demand

It seems that recently many investors use Tesla EV demand as a proxy for the overall EV market. That might work for US EV demand where Tesla remains dominant. It is badly misleading when it comes to global demand for EVs, which dwarfs the US market.

In China, Tesla trails BYD, which is the largest market by sales. Close behind is Europe and although Tesla still has the largest selling models. It isn't dominant. Individual models have just 4 at most but competitors have dozens of models with a long tail of those selling 2-3%.

Tesla hasn't conquered the world (Statista)

{kind=link}

So anyone selling SQM and lithium producers because Tesla announced incentives to meet Q4 goals is looking at a tree in the forest of global demand.

SQM operational performance has been good and growth looks set to continue

Lithium is as much a chemical processing business as it is mining. This means inexperienced operators, such as the Bolivian government , can struggle to get operations going.

However SQM is experienced with a good track record of increased capacity.

Lithium Production and Prices ((SQM))

{kind=link}

SQM's immediate expansion and investment plans for 2023 and 2024 represent a further significant jump in capacity.

- Mt Holland, Western Australia. SQM has a 50:50 joint venture with large Australian conglomerate Wesfarmers ( WES ) to mine and refine battery grade lithium hydroxide. This is expected to open in late 2024 and produce 50,000 tonnes per annum.

- Carmen Lithium Plant, Antofagasta, Chile. SQM will expand capacity to produce 210,000 MT (metric tonnes) of lithium carbonate and 40,000 MT of lithium hydroxide. Forecast to open in 2024.

- Pampa Orcoma Project, Tarapaca, Chile. This project is forecast to increase iodine capacity by 2,500 MT and nitrate salt production by 320,000 MT.

Each lithium project is roughly equal to current production. So assuming smooth development then lithium production could triple by early 2025.

Continued investment in other specialty chemicals also reminds us that SQM isn't just a lithium miner and has other significant sources of growth.

SQM is big in iodine and potassium nitrate

Besides lithium, SQM is a world leader in iodine and potassium nitrate and all these combined make up around 25% of sales.

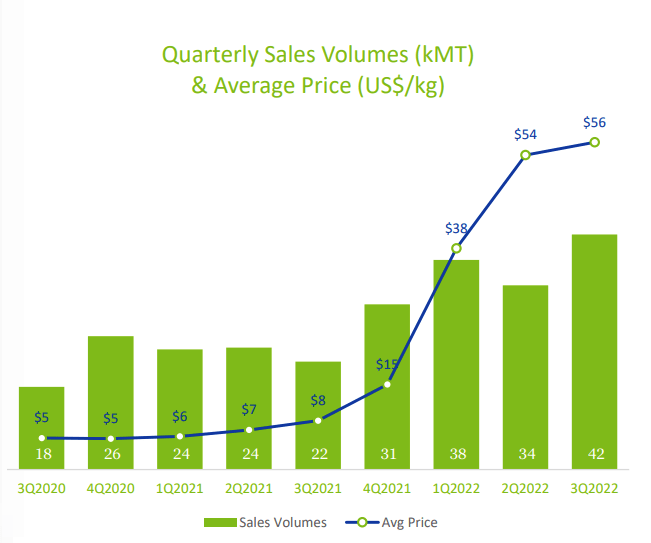

First up, here is iodine, which had an excellent first quarter although even then it still produced only 7-8% of revenues.

Iodine Production and Prices ((SQM))

Demand for iodine comes from many sources, but the biggest growth is its use as a contrast agent for x-ray imaging. Many analysts put growth at around 5% per annum due to its ability to help identify cancer in images.

High prices aren't likely to increase the supply of iodine raw material shortly. As SQMs Executive Vice President for Iodine and Nitrates, Pablo Altimiras explained during the Q3 2022 earnings call , " ...regarding to the supply, well, today, we have not seen more supply coming. Next year, we know that some new capacity could arrive, but still we need to see finally that happen. "

Prices may stay elevated into early 2023, but are likely to cool longer term. SQM themselves will likely be part of the reason.

SQM is on target to increase production by 1,000 tonnes in 2023 and 2,500 tonnes in 2024. That's a 33% and 62% jump for SQM respectively. The good news is that during 2022 prices continued to rise despite rising volumes, indicating strong and price-insensitive demand.

Longer term SQM will become the dominant and lowest cost producer at such a scale. However such a large production increase will likely limit prices.

SQM is also the global number 1 in Potassium Nitrate

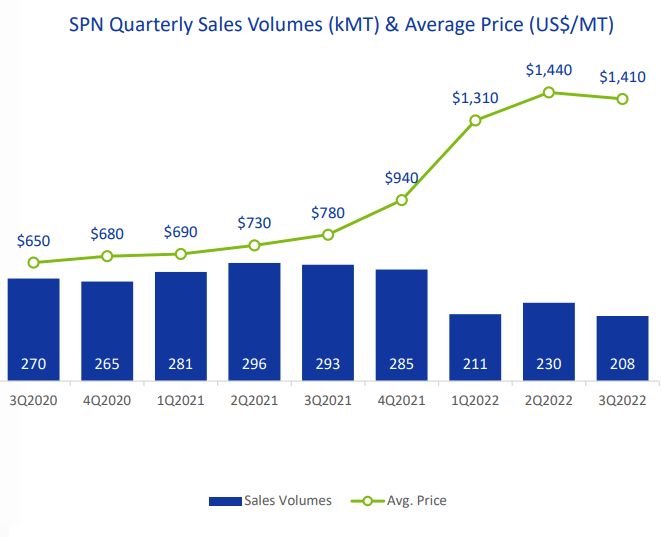

At about 18% of SQM's revenues comes from SNP (Specialty Plant Nutrition) and Potassium Nitrates.

SPN Sales and Prices ((SQM))

{kind=link}

Both can be seen as fertilizers. The price spike however commenced in Q3 2021 suggesting that supply was tight even before the Russian invasion of Ukraine crimped Ukrainian and Russian exports.

Potassium Volume and Prices ((SQM))

{kind=link}

Few expect a prompt end to Russian/West tensions. Supply is likely to remain tight and prices firm. Although demand destruction from high prices has been in evidence. Prices of $960 USD/T up from $440 USD/T the previous year caused volumes to more than halve.

Still, despite this strength and diversification of SQM's business it is healthy to keep it in perspective. It's a small added strength and not the main game. Lithium was 77% of SQM's gross profit for the first 9 months of 2022. Similar levels will likely prevail into 2023.

Copper weakness is good for SQM

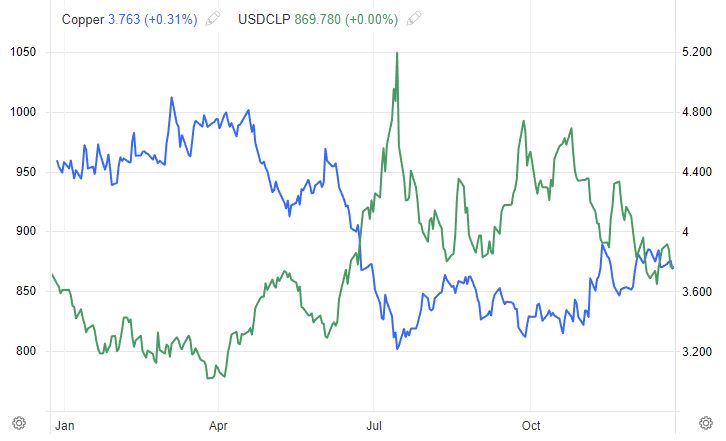

Chile is the home of operations for SQM, so most ongoing costs are incurred there, whilst sales are in USD. A weak Chilean Peso [CLP] is good for SQM.

The CLP had a weak start to 2022 culminating with a mid year panic before a recovery to roughly where it began the year. This recovery might be temporary if our theory on Chinese construction driven copper demand is correct.

{kind=link}

First, let's understand the bigger picture. Fully half of Chile's exports are copper and its ores. Not only that, but Chile is the easily the largest global copper producer, twice second place Peru. Thus, where the copper price goes, the Chilean peso follows.

The world's single biggest market for copper is China; specifically the property and construction industry. That sector is in a worsening mess. The government has provided some help with lower financing and support to finish construction of existing projects. However this support won't return China to the construction boom conditions of the 2012-2020 period.

A key goal of Xi Jinping has been to cool the overly large construction industry tied to property speculation. This was the purpose of the "3 red lines" on developer finance that led to current situation. Easing should thus be seen an attempt to prevent a true crisis, not a complete reversal.

Early in 2022 copper fell hard as fears around a property collapse grew. This dragged down the Peso (to near crisis in July) before a steady recovery since. This graph has USDCLP so you see the inverse correlation.

Copper vs CLP (Trading Economics)

{kind=link}

Thus, we expect a return to both copper and CLP weakness as the market realizes the China support package is a cushion, not a return to boom times.

But what about copper's bull forecast?

Yes, eventually, copper will go on a huge bull run as Glencore recently warned . Large miners are loading up on copper mines for this, but that environmental investment driven boom run is still a couple of years away.

However keep this copper surge risk in mind for SQM in the medium term. Our belief is that short term weakness in China will be more important but demand growth will change the dynamic from 2025 or 2026 onwards. A rise in copper will definitely push up the Chilean Peso. This will hurt SQM's cost advantage.

Bottom-line: the Peso should remain weak in 2023 helping SQM's profits but be careful holding for longer timeframes.

80% of SQM's lithium is sold at market rates

In the early years of lithium, many producers signed multi-year fixed-price off-take agreements with large battery manufacturers. This provides the certainty needed to raise finance to build the mine and refining facilities.

What this also means is that some lithium miners don't always fully benefit from higher prices, at least in the early years. It's always a question worth exploring before you invest.

In the last earnings call, Filipe Smith, Executive Vice President for Lithium confirmed...

...approximately 50% of our sales are contracted with fully variable price indexes. Around 30% of our sales are still open and about 20% with capped.

That makes SQM's results well correlated with the lithium price. That's good news, at least while prices remain elevated.

SQM is fairly valued given growth potential

The following points make the decision straightforward.

- PE of 7 across last 4 quarters of earnings.

- Most recent quarter cash flow of $1.25 b, if sustained, gives cash flow multiple of 4.7 against market cap.

- Dividend yield of 9.2% at current levels

- Conservative balance sheet with minimal debt. Total debt $2.6 b vs current assets $4.6 b gives complete safety.

- Investment in new capacity easily covered by cashflow.

The market clearly doesn't expect strong conditions to continue. We believe this view is mistaken and are buying now and below $90 per share.

Editor's Note : This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

The Theme For 2023 Is Energy Security So Buy SQM