TKR - The Timken Company: Steady Wins The Race

2023-12-01 10:26:36 ET

Summary

- The market mix that TKR has is impressive and has led to strong revenue growth in the last few years.

- With steady growth like it has had, I think a higher valuation makes sense.

- The upside here is in the double digits, and that leaves me to rate TKR a buy for investors seeking a well-run and well-diversified business.

Investment Rundown

The growth of The Timken Company (TKR) has over the last decade been quite strong but above all steady, ever since 2017 the revenues for the business have been climbing at a good rate, only ever dipping into 2020 but only by roughly 6-7%. What investors get with TKR is a well-diversified business that can efficiently tackle market challenges and still deliver value to shareholders.

One of the key factors in my opinion for the steady growth has been the well-diversified nature of the company, which enables them to benefit from several major trends, like improved infrastructure spending in the US or global initiatives to increase the reliance on green energy sources like solar, of which TKR supplies products for. The company is trading a fair bit below its sector average of 17 and below its 5-year average of 12 based on FWD non-GAAP p/e. With a dividend that has been increased for 10 consecutive years, I think that investors are both getting some immediate value here but also are getting in at what I find a discounted price with an adequate amount of margin of safety baked in too. With a quality business like this, I think a higher valuation is justified, and will be rating TKR a buy right now.

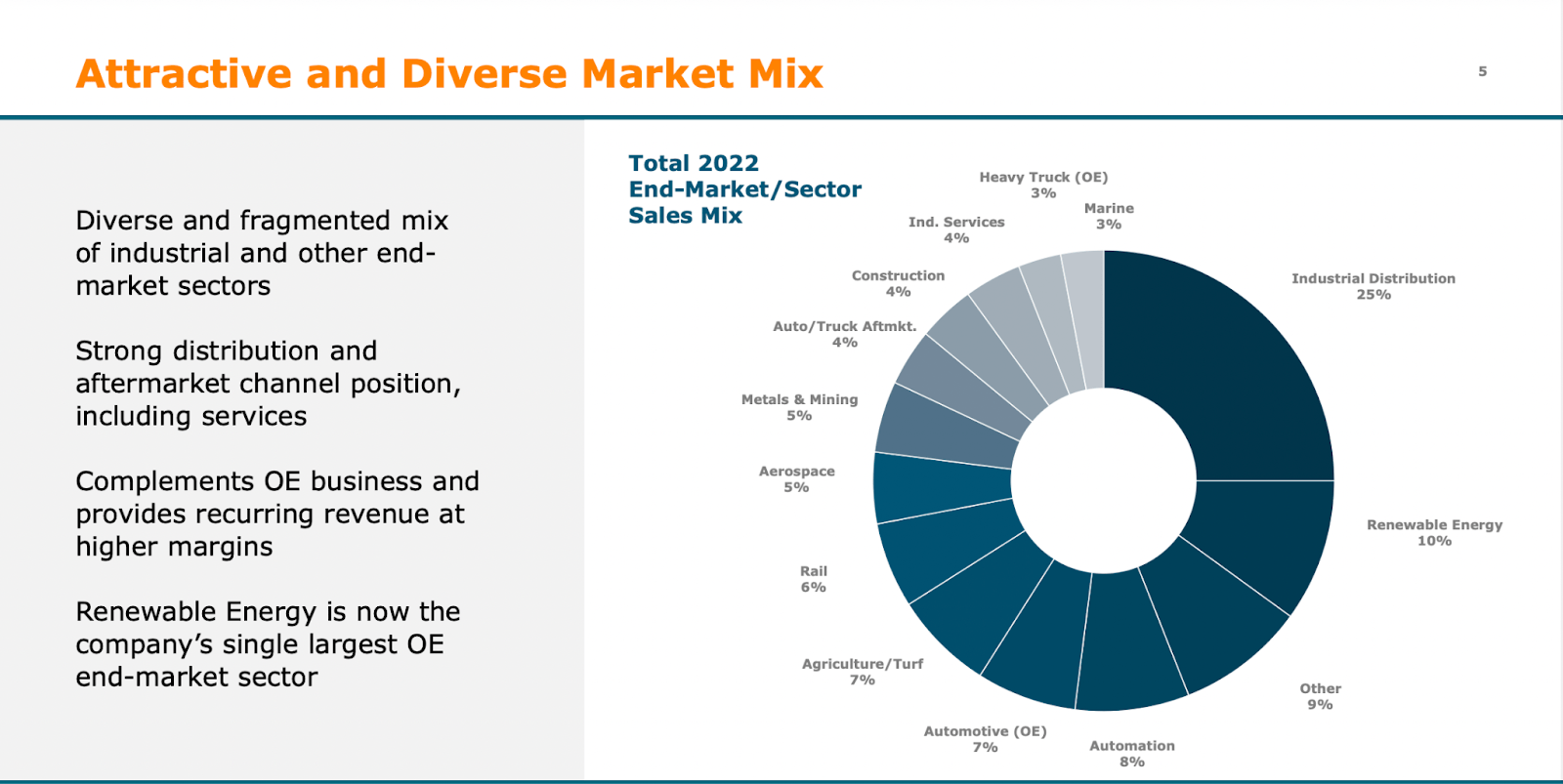

Company Segments

TKR is a global enterprise specializing in the design, production, and management of engineered bearings and industrial motion products. The company operates through two key segments: Mobile Industries and Process Industries. In the Mobile Industries segment, TKR provides a comprehensive portfolio encompassing bearings, seals, lubrication devices, systems, and various industrial motion components.

Market Mix (Investor Presentation)

{kind=link}

This strategic approach positions TKR as a leader in delivering solutions tailored to the diverse needs of mobile and process industries worldwide. TKR's extensive product portfolio finds applications across a broad spectrum of industries such as agriculture, construction, mining, power sports, passenger cars, and light trucks. Its diverse range of offerings caters to various applications and sectors, showcasing a strategic market presence.

Renewable Energy (Bloomberg)

Notably, TKR has a stake in the energy sector, particularly in green energy. This sector presents a compelling opportunity for TKR to explore further, potentially unlocking avenues for accelerated growth in the foreseeable future. Exploring deeper into green energy initiatives could position TKR favorably amidst evolving market dynamics and sustainability trends. I am not saying it's a pure-play green energy opportunity by any means, but it will likely benefit from those trends nonetheless. In the last 12 months, the revenues for the company have been over $4.7 billion and in the last 8 years, TKR has tripled its revenues from "new markets" which include the likes of renewable energy and automation. My point is that TKR already has a foot in the door in these markets and has not been afraid of investing to get ahead. 28% of total sales are now from these "new markets" and I wouldn't be surprised if it continues to increase and be a growth driver over the next decade. The automation market for example is set to grow by around 8.2% annually over the next decade.

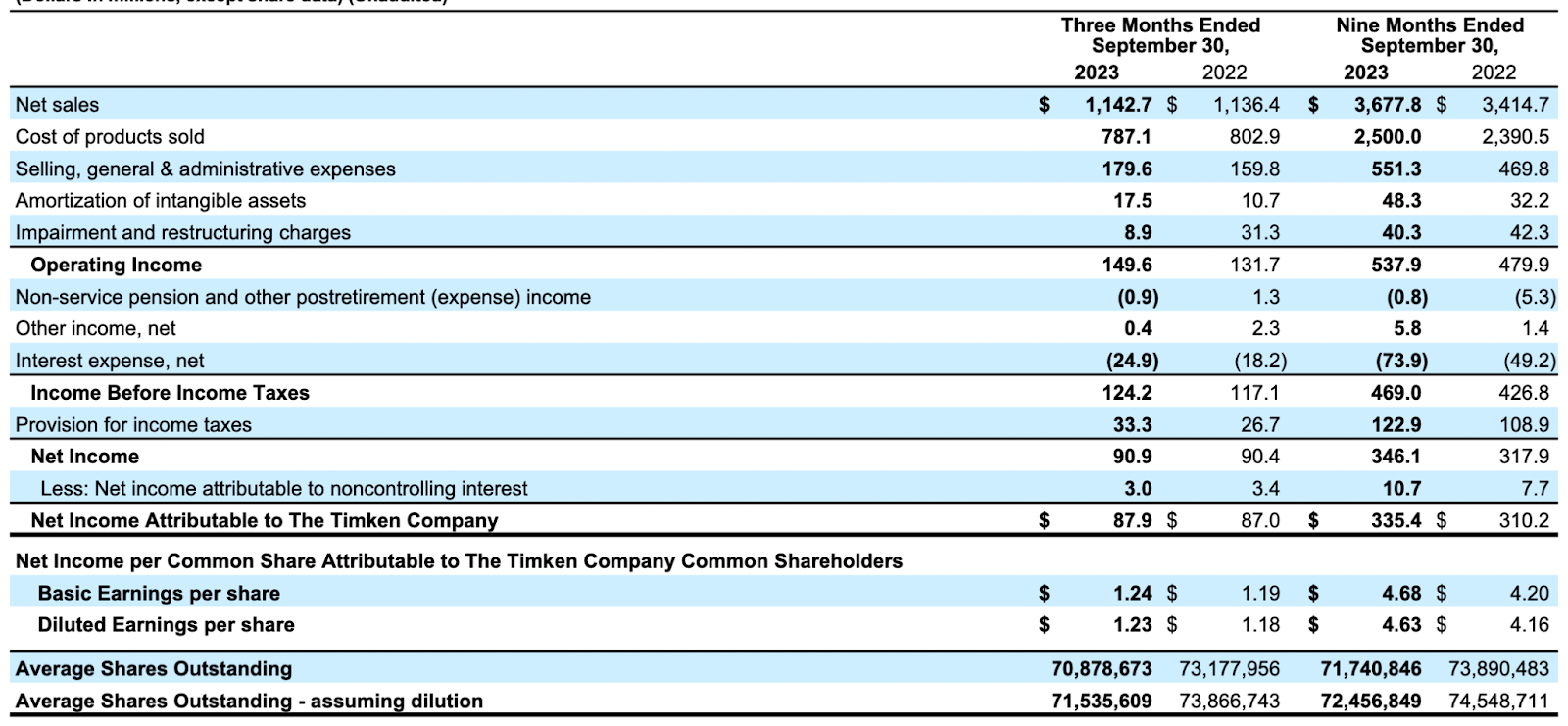

Earnings Highlights

Income Statement (Earnings Report)

{kind=link}

Looking at the last report that the company had on November 1, 2023, we saw a slight increase in the revenues by 1% YoY, landing at $1.14 billion. This all trickled down to a slight $500,000 increase in earnings. To be honest, I think this is quite impressive seeing as the interest expenses rose by over $6 million YoY as well. Some of the key reasons why TKR was still able to post a YoY EPS increase was how the impairment and restructuring charges the company had last quarter were vastly lower than in FY2022 Q3, decreasing by over $20 million to $8.9 million. Part of the reason for the higher charges in 2022 was in relationship to its sale of ADS, which was previously announced. I don't think such high restructuring charges will occur in 2023 or the coming few years, either.

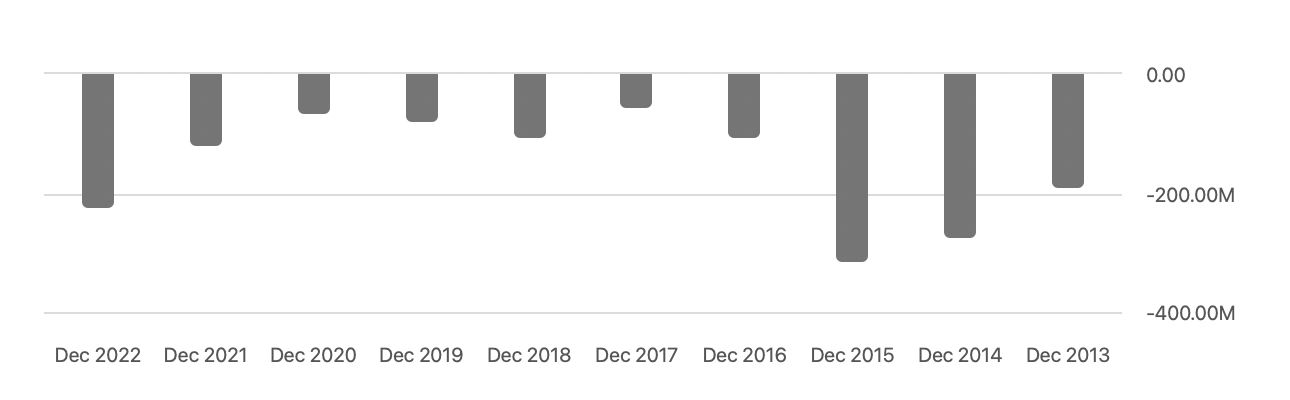

Buyback Spendings (Seeking Alpha)

{kind=link}

TKR actively engages in share repurchases, exemplified by its substantial buyback initiative. Since September 2020, the company has repurchased $419 million worth of its shares, effectively reducing the share count from 76.3 million to 73.4 million within this period. These shareholder-friendly practices, coupled with a respectable dividend yield, contribute to a favorable investment outlook. If the company can sustain its upward trajectory in revenues and EPS, there's potential for a valuation boost. Currently trading over 12% below its 5-year average p/e ratio, there appears to be ample room for upside potential, presenting an attractive opportunity for investors. Monitoring the company's commitment to returning value to shareholders and its impact on financial metrics will be key considerations for potential investors. I think a fair p/e is around 13 for the company, and that leaves an immediate upside of 22% based on the current share price of around $73. The price target I therefore have for TKR is $89 based on the estimated EPS of $6.89 for 2023. Much of the reason for the 13x earnings multiple comes back to where it has been trading before, which is around 12.6. I am willing to take a slight premium based on that because of the stability and strong growth I see ahead. The company works with a broad set of markets and I think next year will see an uptick in demand as interest rates could go lower, opening up more spending, both from consumers but also businesses. At the end of the day, I think this will aid TKR in posting strong double-digit YoY growth in the top line for 2024. With both a well-established dividend and a strong history of buying back shares, I am also perfectly fine sitting and waiting to hit that price target because I know I am getting some value during that as well. All in all, the discounted price together with broad sector tailwinds is making TKR out to be a buy in my view.

Another similar company is Chart Industries ( GTLS ) which right now trades at a higher p/e than TKR, around 20 on an FWD basis. This number is still below where GTLS has been before, around 33% below based on p/e. Despite these higher valuations, I still find TKR to be the superior option here, seeing as the margins are better. It seems the market is accounting for GTLS to perhaps grow revenues quicker than TKR, which it has done over the last decade. I am not convinced though that GTLS would be better because of the large amount of weight the debt is having on earnings. Interest expenses have skyrocketed to $246 million for the company, up from $19.9 million in 2021. I think this me indicates that TKR may have a less volatile road ahead, as their interest expenses haven't risen as drastically.

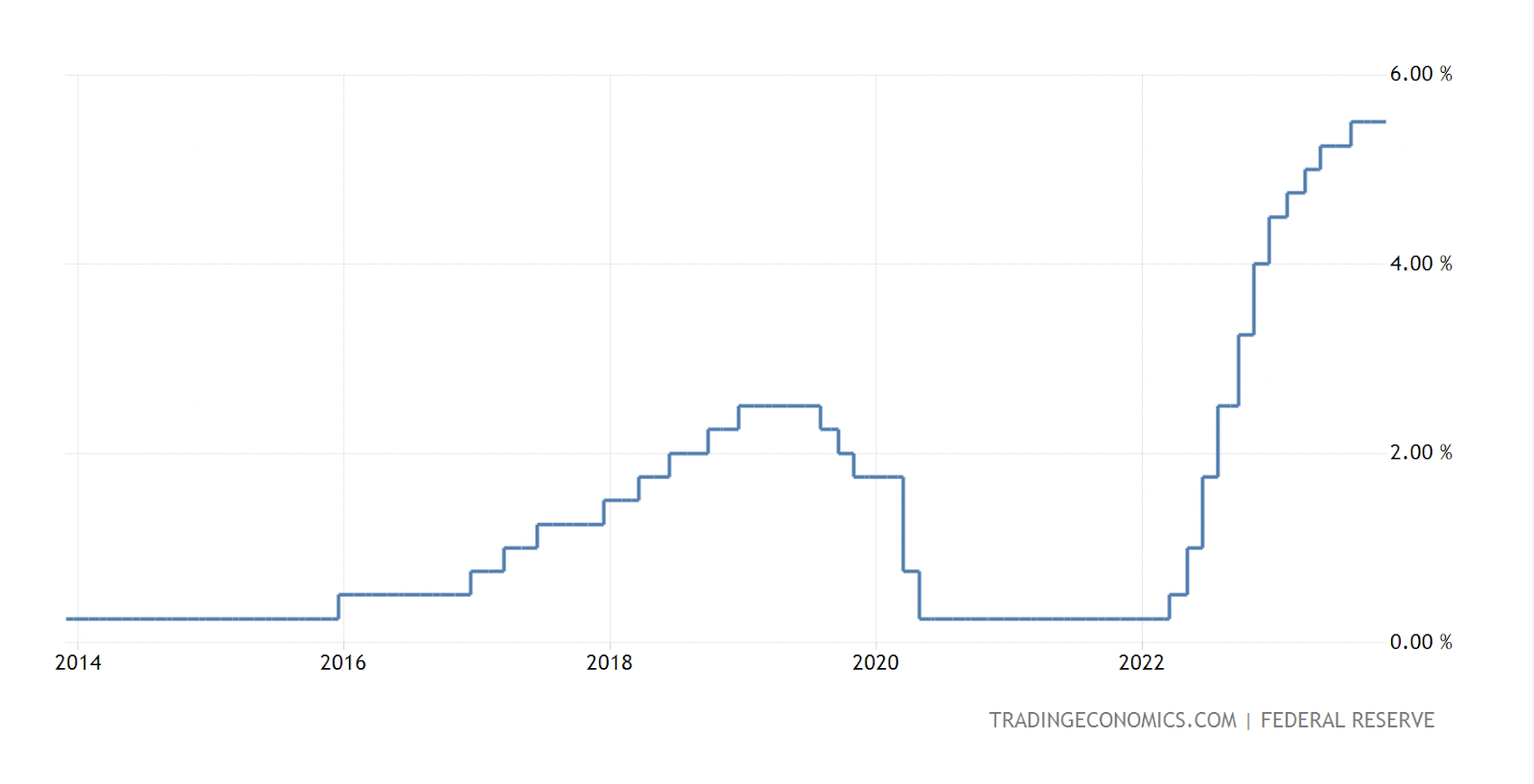

Risks

TKR faces certain notable risks, and one key concern is the potential impact of prolonged periods of higher interest rates. Elevated interest rates tend to make borrowing more expensive, which, in turn, could dampen demand for TKR products as customers become more cautious with their spending.

US Interest Rates (Tradingeconomics)

{kind=link}

However, it's crucial to note that this appears to be a short-term headwind, and recent reports have not indicated a widespread prevalence of this issue. TKR managed to achieve a modest 1% year-over-year revenue expansion in its most recent financial results, suggesting resilience amid potential economic challenges. Monitoring the interest rate landscape and its effects on customer behavior will be essential for assessing the company's future performance.

{kind=link}

On the debt side of things for the company, they do hold a decent amount, which could take a toll on earnings as interest expenses rise. With over $1.5 billion in debts, this has resulted in $102 million in TTM interest expenses. Seeing as the rates are higher now than 12 months ago, I do think it's reasonable to assume that this amount may rise further. If TKR does continue its rapid repayment of debt which has since the end of 2022 gone down over $400 million then a higher interest rate environment may not pose such a major threat to the earnings of the company in the end, but perhaps more to the demand they are seeing for their products as customers may be affected more widely.

Final Words

TKR is a very well-diversified business, and the last 12 months have seen the stock price largely flat. TKR has not been that affected by higher interest rates, as they are paying back debt at a very fast pace right now. We set out some price targets and I think that there is a 22% upside in the short-term, which is sufficient to make the stock a buy. Investors are getting the benefit of being exposed to a broad set of industries and sectors which has benefitted TKR over the last decade, steady wins the race here.

For further details see:

The Timken Company: Steady Wins The Race