TJX - The TJX Companies: Good Company But A De-Rating Is More Than Likely

2023-12-19 00:39:14 ET

Summary

- The TJX Companies is a leading off-price retailer that owns and operates several well-known retail chains in the U.S. and worldwide.

- Off-price retailers like TJ Maxx often perform well in recessions and economic slowdowns, but in positive environments can also continue to grow.

- EV/EBITDA ratio for companies like TJX and ROST has been around 10x. However, they are currently trading around 17.6x.

- A transition from defensive stocks to higher-risk ones could cause a return to the mean that would cause a painful drop in the stock price.

Investment Thesis

The TJX Companies (NYSE: TJX ) is a company that typically shines in the most challenging times, and even during periods of economic expansion, it tends to continue growing, making it a truly defensive stock and a reliable anchor for any portfolio.

However, over the last two years, the market, aware of these qualities and driven by fears of a recession, has heavily invested in stocks of this nature. As a result, the company is currently trading at historically high multiples of 17.6x EBITDA, significantly exceeding the average range of 10-12x. This, coupled with the shift in the FED's stance , now indicating potential rate cuts in 2024, might prompt the market to move from defensive stocks to higher-risk ones. This shift could make a return to the mean quite painful in the stock price if the valuation adjusts according to the historical average.

Considering these factors, despite finding the company interesting and of high quality, I have decided to assign it a ' sell ' rating.

{kind=link}

Business Overview

TJX Companies is a leading off-price retailer that owns and operates several well-known retail chains. In fact, the company owns so many brands within the off-price retailing sector that I would refer to it as an ' Off-Price ETF '. Some of the prominent brands under TJX Companies include:

- TJ Maxx is one of the largest off-price retailers in the United States. It offers a diverse selection of brand-name and designer apparel, footwear, accessories, home goods, and more at discounted prices.

- Marshalls is another major off-price retail chain owned by TJX Companies. Similar to TJ Maxx. Marshalls provides a variety of discounted products, including clothing, accessories, beauty products, and home goods.

- HomeGoods specializes in offering discounted home furnishings, decor, kitchen essentials, and other home-related items. It's a popular destination for customers looking to find affordable and stylish pieces for their homes.

- Sierra is an off-price retailer that focuses on outdoor gear, sporting goods, and apparel. It offers a range of products for outdoor enthusiasts at discounted prices.

As mentioned previously, TJX Companies follows an off-price retail model, sourcing merchandise from a variety of vendors and selling it at prices significantly below traditional retail prices. The company's success is often attributed to its ability to offer customers well-known brands at affordable prices, creating a unique shopping experience that emphasizes value and the thrill of finding bargains. Here's how the off-price model typically works:

- Closeout Purchases : TJX Companies often purchases merchandise from manufacturers and retailers that have excess inventory, canceled orders, or closeouts. These can be items that didn't sell well in traditional retail stores or are surplus from seasonal collections.

- Irregulars and Overruns : TJ Maxx may also acquire irregular or overstocked items. Irregulars are products with minor defects or imperfections that don't meet the brand's strict quality standards. Overruns are items produced in excess of what was ordered.

- Negotiation of Lower Prices : TJX negotiates with suppliers and manufacturers to buy products at a lower cost. Since they are often purchasing surplus or discontinued items, they can get these products at a significant discount. This is where the scale of the company comes into play, as greater scale allows for greater bargaining power.

- Lower Operating Costs : Off-price retailers typically have lower operating costs than traditional department stores. They may have less elaborate store layouts, invest less in advertising, and maintain leaner staffing levels, so they can afford to sell merchandise at a lower price without sacrificing their profitability.

By combining these strategies, TJX Companies can sell brand-name and designer merchandise at discounted prices while still maintaining profitability. Customers are attracted to the idea of finding quality products at lower prices, and the ever-changing inventory encourages frequent visits to discover new deals. Off-price businesses intentionally create an atmosphere that makes customers feel like bargain hunters .

In fact, this is a fundamental part of why off-price retailers like TJ Maxx often perform well in recessions and economic slowdowns. During tough economic times, consumers become more price-conscious, so offering brand-name and designer products at discounted prices provides a perception of value for money at times when consumers are more conscious of their expenses.

If we analyze the behavior of TJX Companies and a close competitor, Ross Stores, we can notice how during the great financial crisis of 2008 , both revenues and margins were not only sustained but also improved.

Performance During 2008 and 2009 (Author's Representation)

{kind=link}

Revenue per Segment

The company divides its revenue into four main segments: Marmaxx (a combination of TJ Maxx, Marshalls, and Sierra stores), HomeGoods (including HomeGoods and Homesense), TJX Canada, and TJX International. Each segment exhibits different growth patterns and margins, warranting a closer examination of each.

Marmaxx

In the case of Marmaxx, it represents 60% of the revenue and has seen an increasing share in the revenue mix. However, there is limited room for further growth since there are already 2603 Marmaxx stores in the United States, and the long-term goal is to reach 3,000 . Over the last decade, the store count has increased by 2.3% annually, with revenue per store growing at a healthy 3.7%.

Note: Search for the "Stores by Concept" segment (page 9) in the 8-K to have more information about the current store count and the number of stores open during the year.

{kind=link}

Globally, revenue has grown by 6%, and while it is not the fastest-growing segment, it boasts the best margins due to a well-established concept and recognized brands in the United States.

{kind=link}

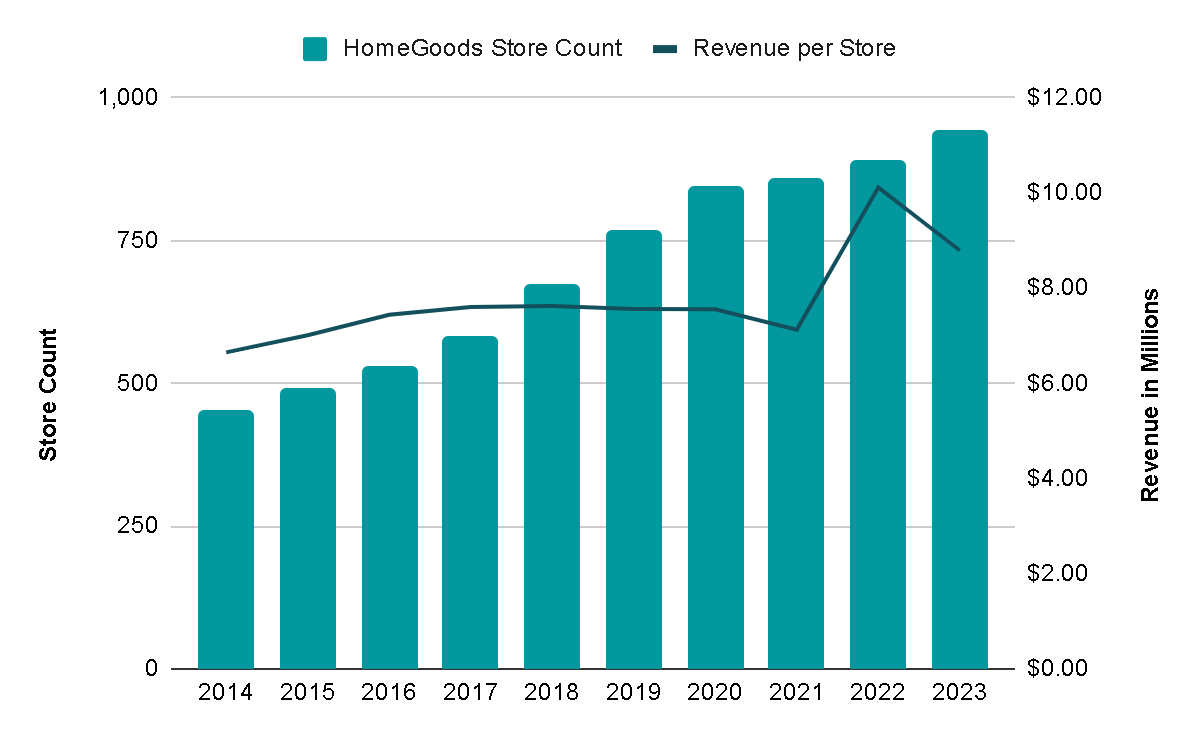

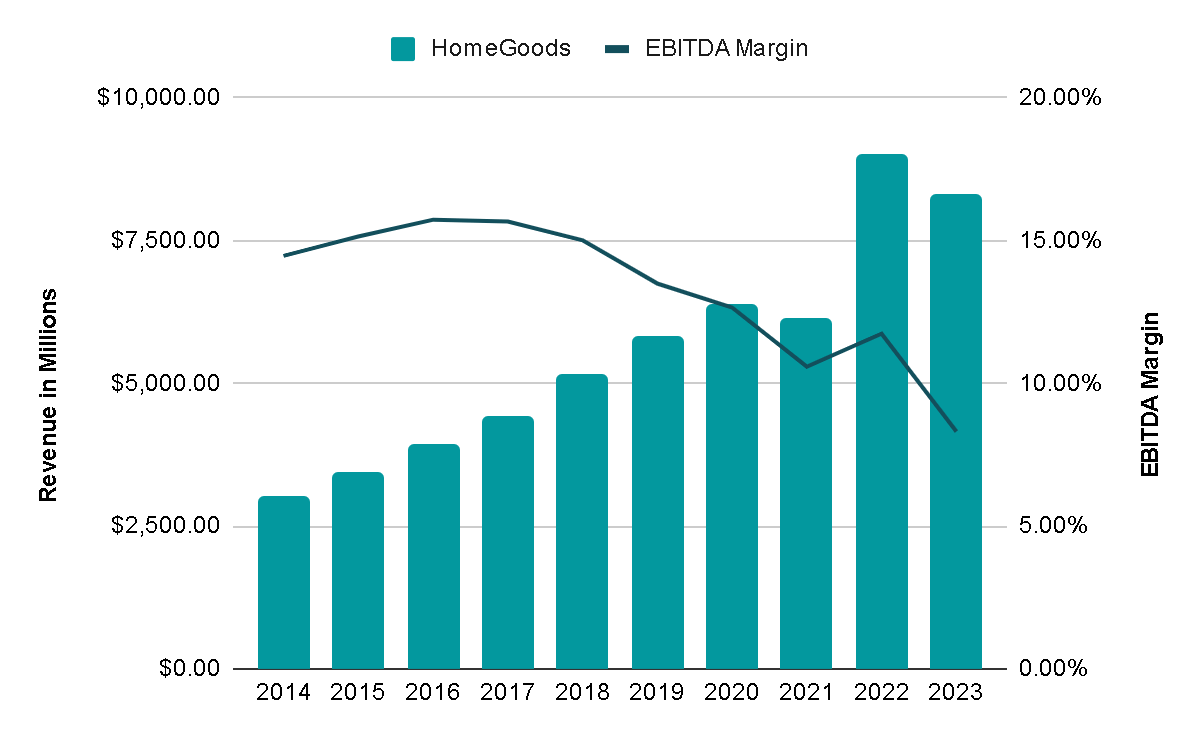

HomeGoods

Moving on to HomeGoods, it primarily sells home accessories and furniture, with 940 stores in the United States as of the end of FY2023. The store count has increased by 8.5% in the last decade, and revenue per store has also increased by 3%, similar to the Marmaxx segment.

Note: Search for the "Stores by Concept" segment (page 9) in the 8-K to have more information about the current store count and the number of stores open during the year.

{kind=link}

The company has managed to achieve a 12% annual revenue increase in the last decade with EBITDA margins around 14-15%. However, these margins were impacted by the COVID-19 crisis and have not fully returned to previous levels. Looking forward, there is optimism about a potential return to prior margins, particularly since certain products like large furniture items are less susceptible to disruption from e-commerce. Customers are likely to prefer in-person viewing before making significant investments in items like beds and sofas.

{kind=link}

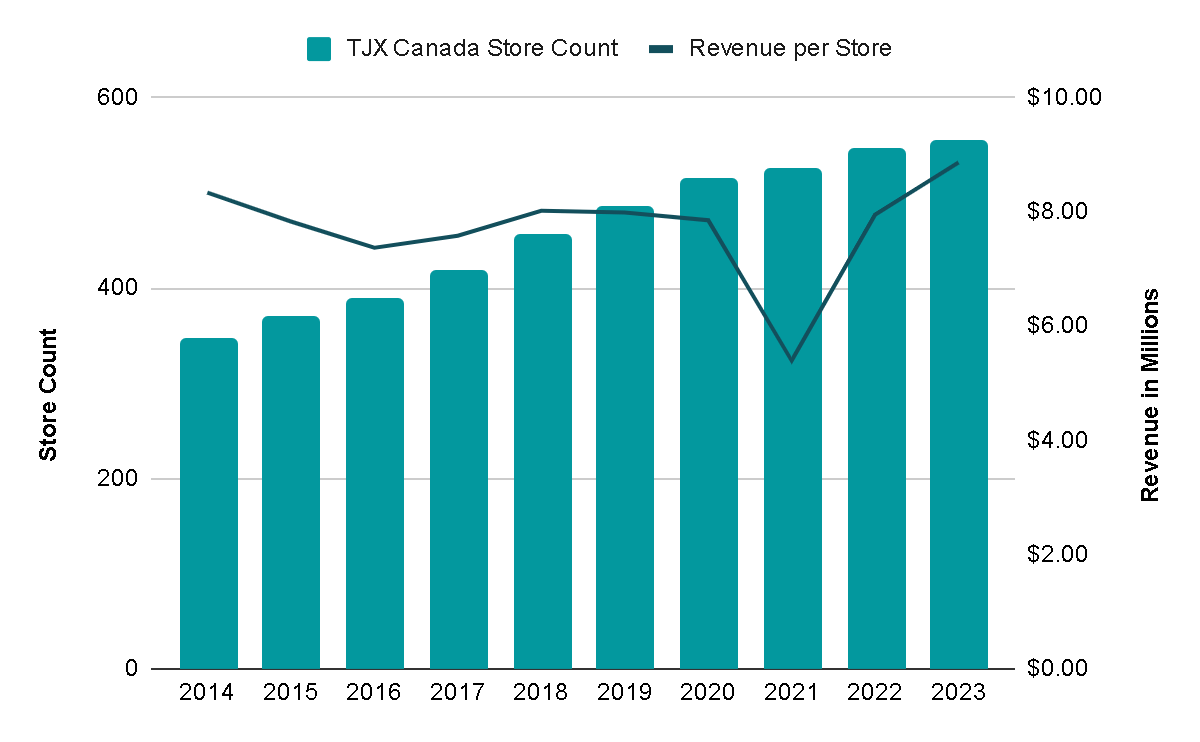

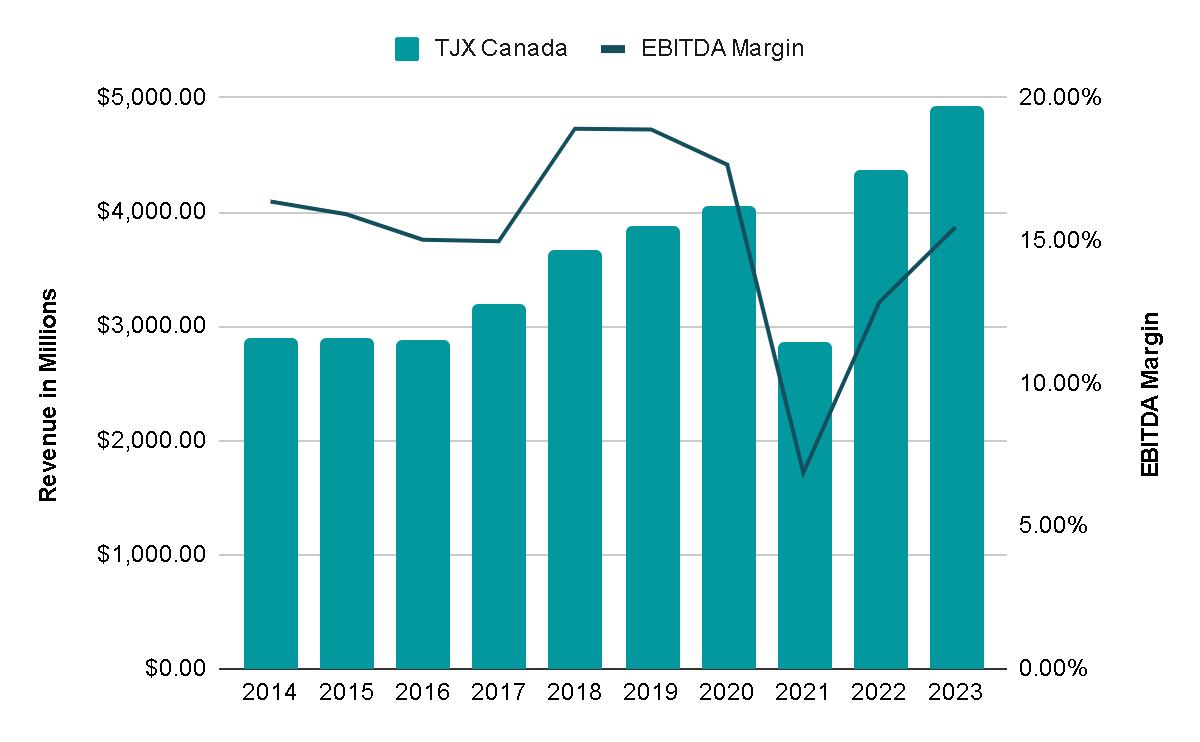

TJX Canada

TJX Canada is the first of the company's international segments, selling branded clothing, footwear, bedding, and including its own HomeGoods. As of the end of FY2023, there were 554 stores, with an additional 11 establishments opened in the first nine months of FY2024 . Over the last decade, the store count has grown by 5.4%, and revenue per store has seen a modest 0.7% growth.

Note: Search for the "Stores by Concept" segment (page 9) in the 8-K to have more information about the current store count and the number of stores open during the year.

{kind=link}

The total revenue of the segment has grown 6% annually in the last decade. Although the EBITDA margin currently stands at 15.5%, it is still well below the 18% it reached in the years prior to COVID-19. If the company manages to recover these levels of profitability, it could present an attractive expansion in margins.

{kind=link}

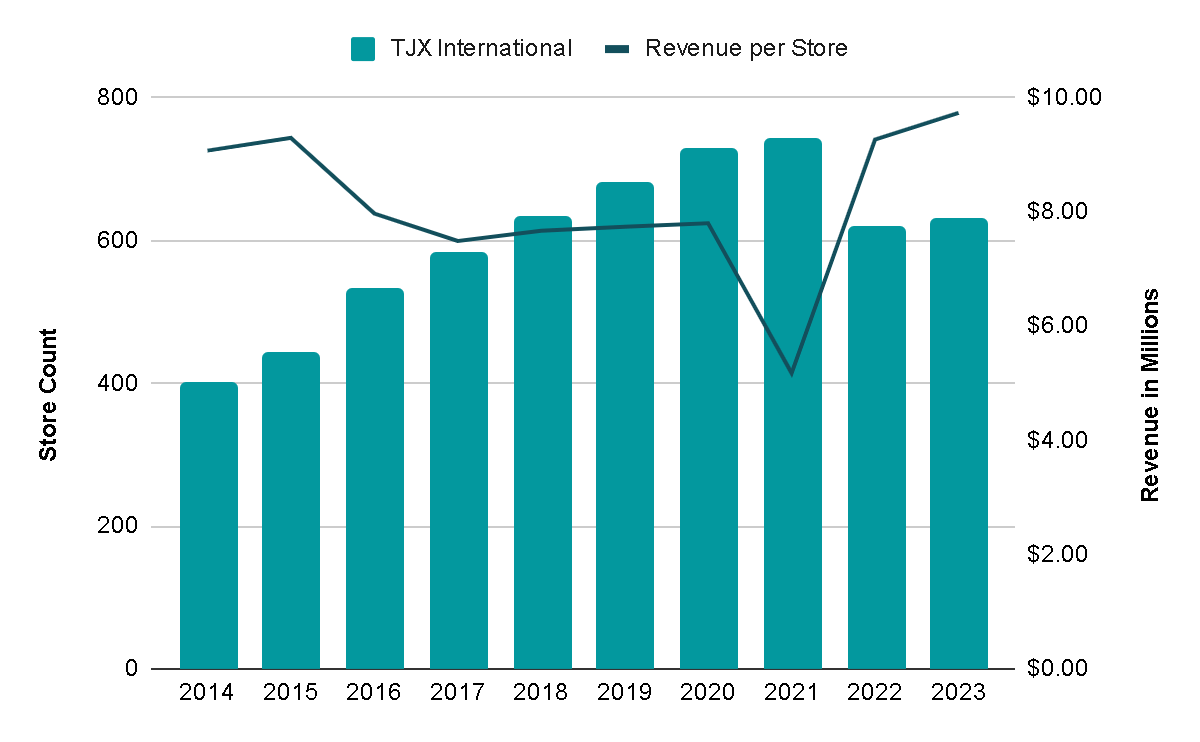

TJX International

In the international segment, the company operates a concept similar to TJ Maxx, but under the name TK Maxx in both Europe and Australia. The store count has increased by 5% in the last decade. During FY2024, the company reopened stores that it had been closing in recent years, reaching a total of 720 stores . Similar to the case with Canada, revenue per store has increased only 0.8%, which is quite poor. This could be due to the fact that in these geographies, the concept is not as consolidated as in the United States, resulting in less traffic in the stores and each store generating fewer sales. For example, the Marmaxx segment in the United States generates $12.4 million in sales per store annually, while TJX International only generates $9.74 million.

Note: Search for the "Stores by Concept" segment (page 9) in the 8-K to have more information about the current store count and the number of stores open during the year.

{kind=link}

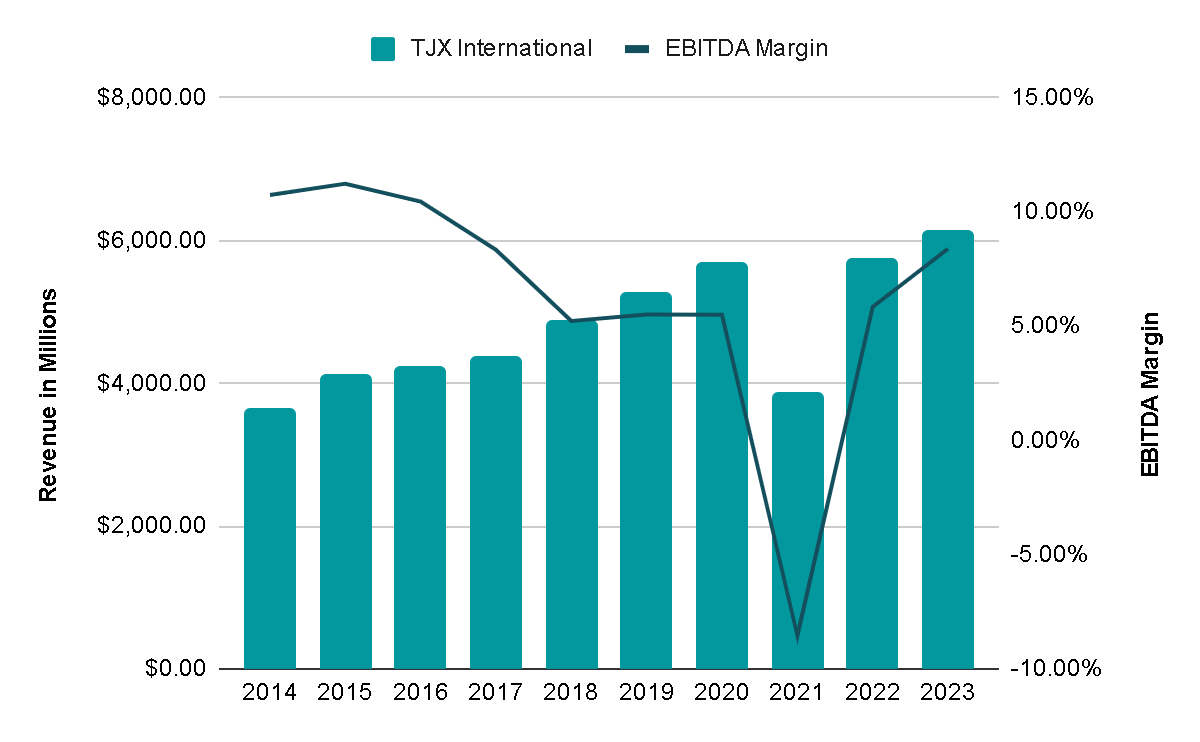

Although the total revenue has grown by 6% in this segment, the EBITDA margins are the lowest of all, ranging between 8% and 10%. Even in 2021, they were negative, demonstrating how less solid this segment is compared to the rest of the segments, where their margins remained positive even during 2021. This raises the question of whether the company should continue dedicating resources and efforts to growing a segment that is less solid and profitable than the rest of the segments.

{kind=link}

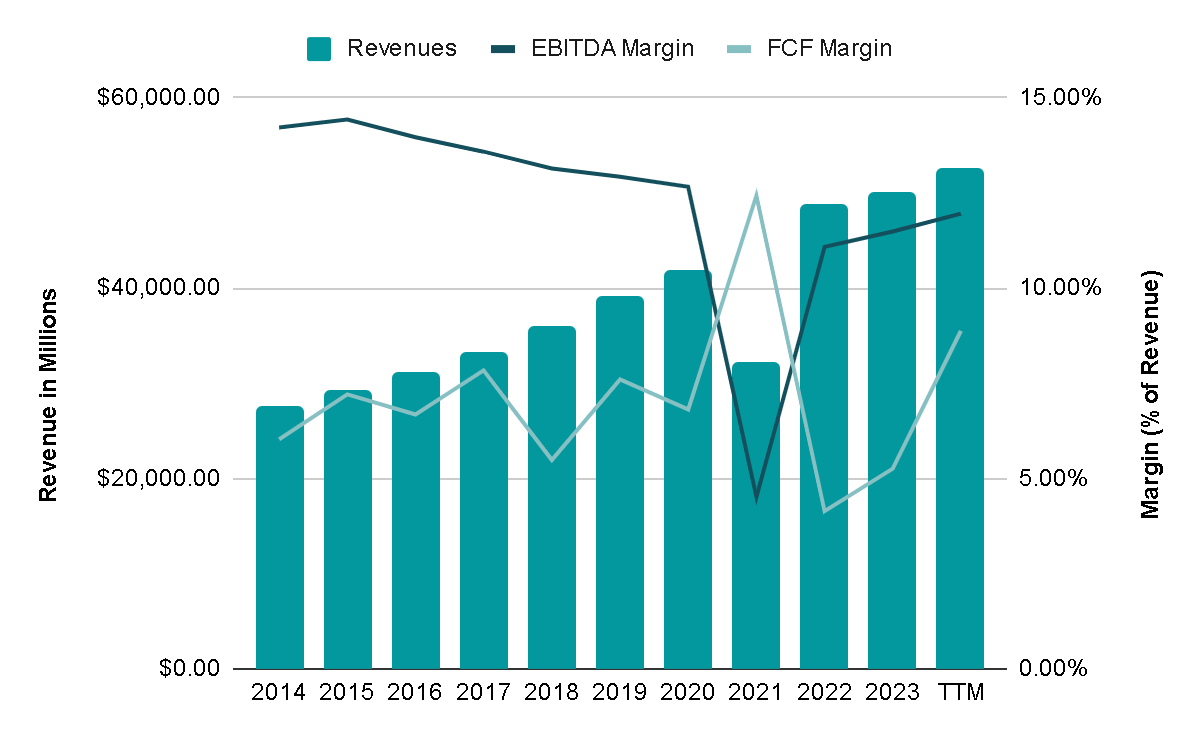

Taking all segments into account, TJX Companies' revenue has grown by 6.9% in the last decade, and the consolidated EBITDA margin has been around 13-14%. However, there is a negative effect since COVID-19, an effect that they have not yet been able to recover altogether. Considering the quality of the company and the business, I believe they will be able to recover their profitability in the coming years.

{kind=link}

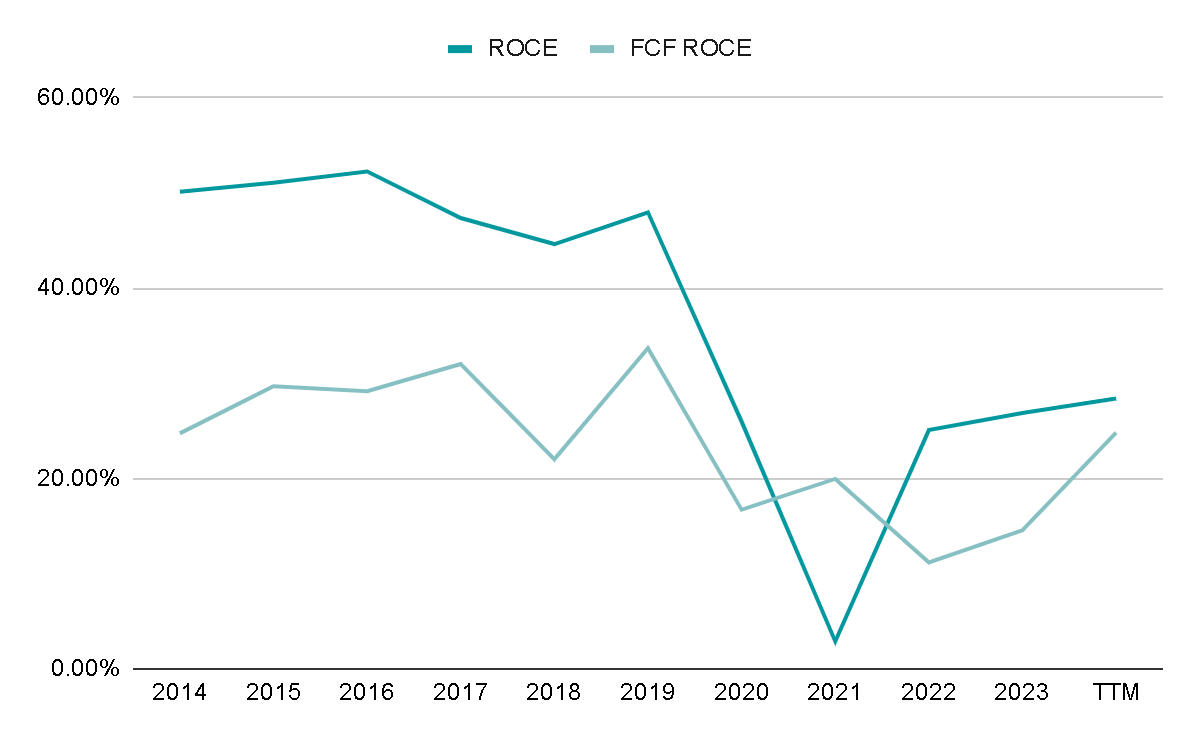

In fact, if we exclude the post-COVID years, the return on invested capital was above 40%, indicating an extremely profitable business and the data for the last twelve months indicates that profitability seems to be returning to that of previous years.

{kind=link}

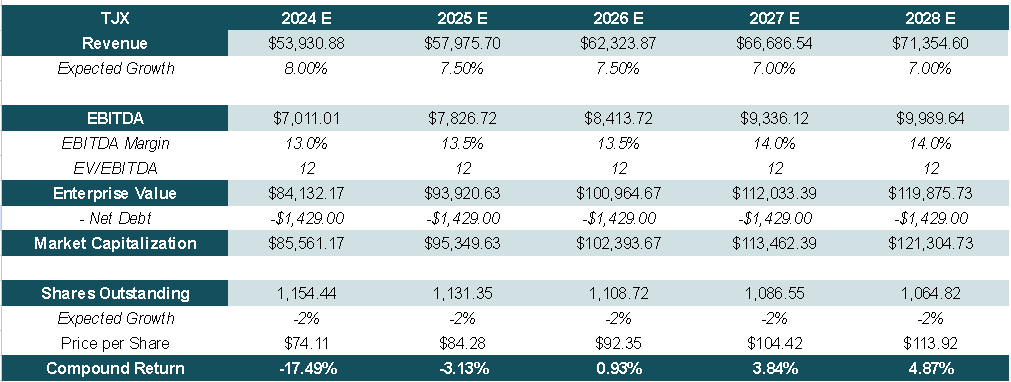

Valuation

Although we could perceive it as an extremely solid and defensive business, doubts arise about whether it is a good idea to be positioned in the company when considering its valuation.

In a scenario where we estimate that revenue will grow by 7% annually, and the EBITDA margin will return to the 14% it had reached in previous years, the expected return would be an unattractive 4.9% compounded annually . A substantial portion of this unimpressive return is attributed to a potential de-rating. We could envision a scenario where the growth is healthy, the company engages in share repurchases, and there is a slight expansion of margins. However, this may not be sufficient if the valuation multiple experiences a reduction.

{kind=link}

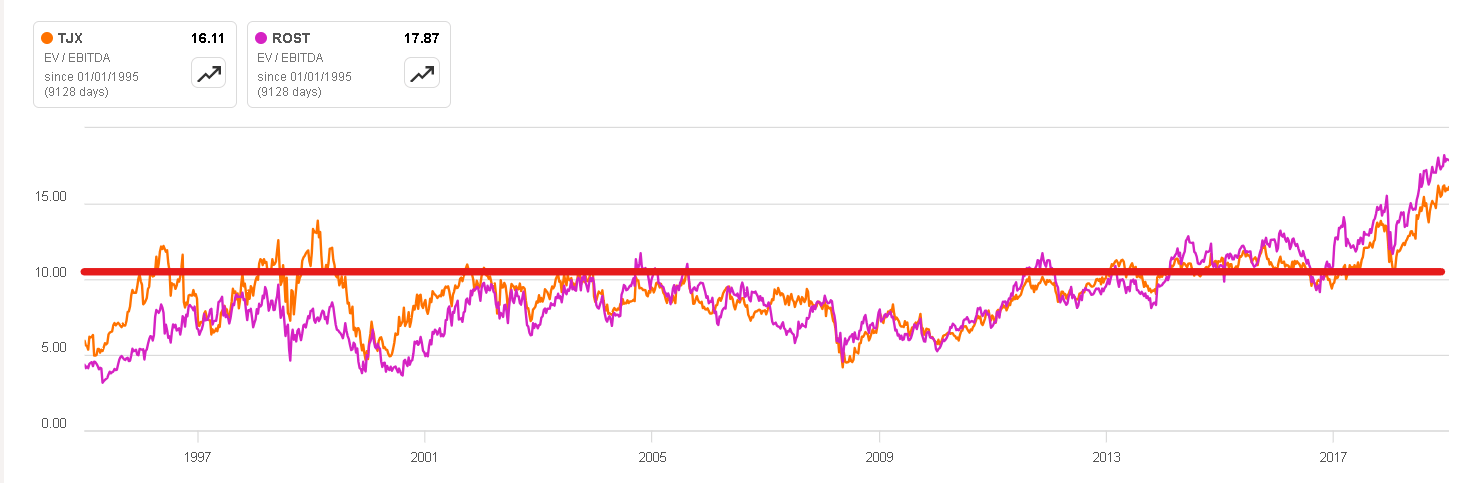

Looking at the chart below, we can observe that between the beginning of the 90s and 2019 (before COVID-19 because during 2020-2021, the multiple was distorted), the EV/EBITDA multiple for companies like TJX and ROST has been around 10x. However, they are currently trading around 17.6x . The explanation I find is that the market has been cautious about the entire issue of high interest rates and the possibility of a recession. Hence, investors have been positioning themselves in defensive companies such as TJX Companies, Ross Stores, or Burlington. Now that the FED has adopted a more dovish stance , with the message that there will be interest rate cuts in 2024, consumption could stabilize, and the market might rotate towards less defensive and riskier stocks. This shift could result in less demand for defensive companies and, consequently, a lower valuation multiple assigned.

{kind=link}

Final Thoughts

After a thorough examination of the business model, I have no doubt that TJX Companies is an excellent company with a bright future . The company spans various businesses across different geographies, all centered around the Off-Price Retailer concept. This led to the analogy I made at the beginning of the article, likening TJX Companies to an ETF of the Off-Price sector. Furthermore, as an anti-cyclical company, it can perform well in both economic expansion and recessionary environments, potentially outperforming during periods of economic downturn.

However, the current market seems to have already factored in any future growth, and stocks appear expensive considering the macroeconomic environment we appear to be heading into. Therefore, I have decided to give it a ' sell ' rating. This is not due to any structural problems in the business; on the contrary, it is based on the likelihood of a de-rating, which could make companies in the sector stagnant for a while.

In my opinion, it would be a favorable purchase if the stock reached around $60, as long as the company continues its historical growth.

For further details see:

The TJX Companies: Good Company, But A De-Rating Is More Than Likely