TWI - The Toro Company Is Still Pricey Despite A Solid Earnings Beat

2023-12-21 09:00:00 ET

Summary

- The Toro Company's shares rose by 8.9% after reporting fourth quarter revenue and earnings that exceeded analysts' expectations.

- The company's Residential segment experienced a 33.6% decline in revenue, while the Professional segment saw a 12.3% drop.

- Despite the decline in revenue and profitability, management provided guidance for increased profitability in the 2024 fiscal year.

- But this still does not make the company a compelling opportunity because of recent weakness and how shares are priced.

December 20th ended up being a really fantastic day for shareholders of The Toro Company (TTC). Shares of the company, which focuses on the production and sale of professional turf maintenance equipment and services, irrigation systems, landscaping equipment, lighting products, snow and ice management products, and more, shot up, closing higher for the day by 8.9%. This came after management reported fourth quarter revenue and earnings that exceeded analysts' expectations . Despite difficult industry conditions, the company also provided guidance for the 2024 fiscal year that suggests increased profitability on an adjusted basis compared to what the enterprise saw in 2023.

As much as I like companies that focus on these types of goods and services, you would think that I would have been bullish on the stock leading up to this point. Unfortunately, that has not been the case. When I wrote about the enterprise back in May of 2022, I ended up assigning it a 'hold' rating despite the view that I had at the time that financial performance would continue to do well for the foreseeable future. This assessment was based on how shares were priced. Unfortunately, since then, things have gone far better than anticipated. While the S&P 500 is up 19.2%, shares of The Toro Company have increased in value by 29%. Even with robust performance, this move higher makes the stock a bit pricey. Even though I clearly missed out on an opportunity in the past, I would argue that a 'hold' rating is the most that makes sense.

Mixed performance that exceeded expectations

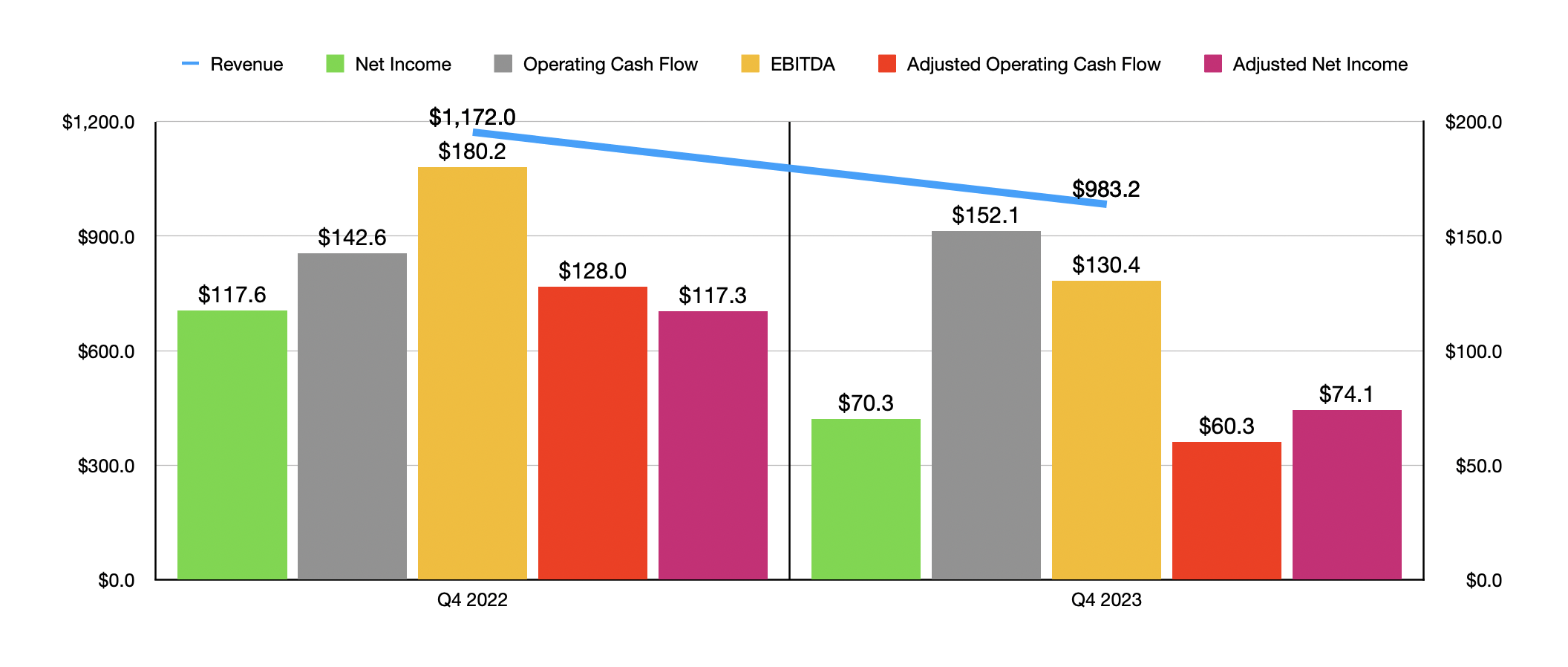

Whether you love it or hate it, there's no denying that the forecasts that analysts put out are important. They set expectations and when a company meets or exceeds those expectations, there is bullish sentiment that often forms. The opposite is true when expectations are missed. A company can even report a weakening in financial performance on a year-over-year basis and still be rewarded handsomely by the market if its results exceeded what analysts anticipated. And a great example of this can be seen by looking at The Toro Company. During the final quarter the company's 2023 fiscal year , revenue came in at $983.2 million. This represents a decline of 16.1% compared to the $1.17 billion generated one year earlier. In spite of this, sales still came in about $6.4 million above what analysts thought they would be.

{kind=link}

The largest chunk of this pain came from the company's Residential segment. This is the part of the company that sells walk power mower products, zero turn riding mower products, snow thrower products, and a variety of other offerings, through retailers, distributors, dealers, and other parties, that then get those products to the end users that are your typical homeowners or tenants. Revenue for the quarter totaled $148.4 million. That's 33.6% below the $223.5 million reported the same time last year. Management attributed this mostly to lower product shipments that were only marginally offset by higher pricing. It seems as though macroeconomic conditions, combined with elevated levels of inventory out on the field, are causing this pain. This pain was also far less than the 12.3% drop in revenue seen by the much larger Professional segment. Its revenue dropped from $944.7 million to $828.9 million thanks mostly to lower shipments of contractor grade lawn care equipment and snow products. Higher floor planning costs also played a role in this decline.

With the drop in revenue for the company also came a decline in profitability. Earnings per share totaled only $0.67. That was a little more than half the $1.12 per share reported the same time last year. This was actually about $0.11 per share higher than what analysts anticipated. Adjusted earnings per share, meanwhile, totaled $0.71, coming in $0.15 per share above what was forecasted. The earnings per share figures resulted in net profits falling from $117.6 million to $70.3 million. Other profitability metrics, however, were somewhat mixed. On the positive side, we had operating cash flow. It actually increased from $142.6 million to $152.1 million. But if we adjust for changes in working capital, we get a drop from $128 million to only $60.3 million. At the same time, EBITDA for the company fell from $180.2 million to $130.4 million. In addition to suffering from a decline in revenue, the company was hit by higher material costs, higher floor planning costs, and other issues. Management did claim that there were some improvements in productivity, as well as a shift in product mix that had a positive impact. But clearly, those were nowhere near large enough to have a material impact on the bottom line.

{kind=link}

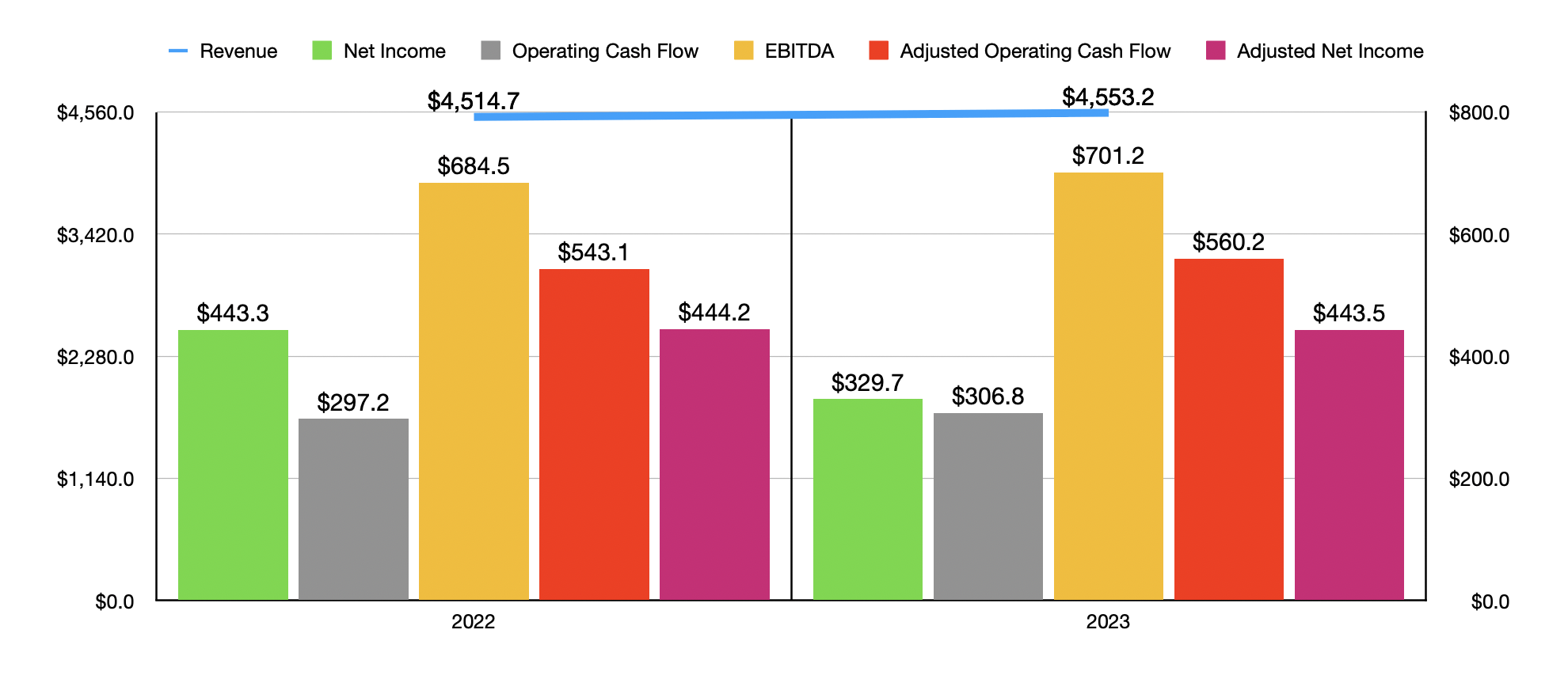

If you look at the chart above, you can see financial performance for 2023 and 2022, both in their entirety. With the exception of net profits and adjusted net profits, you can see that financial results for 2023 outpaced results for 2022. So the weakness experienced has definitely started toward the end of the year. Despite this pain, management believes that adjusted earnings per share next year will be between $4.25 and $4.35. If this comes to fruition, it would translate to a slight improvement over the $4.21 in adjusted earnings reported for 2023 and it would be above the $4.20 reported the year prior. Obviously, we are still into the early stages of the first quarter of 2024 for the business, so only time will tell if guidance will need to be adjusted in some capacity.

{kind=link}

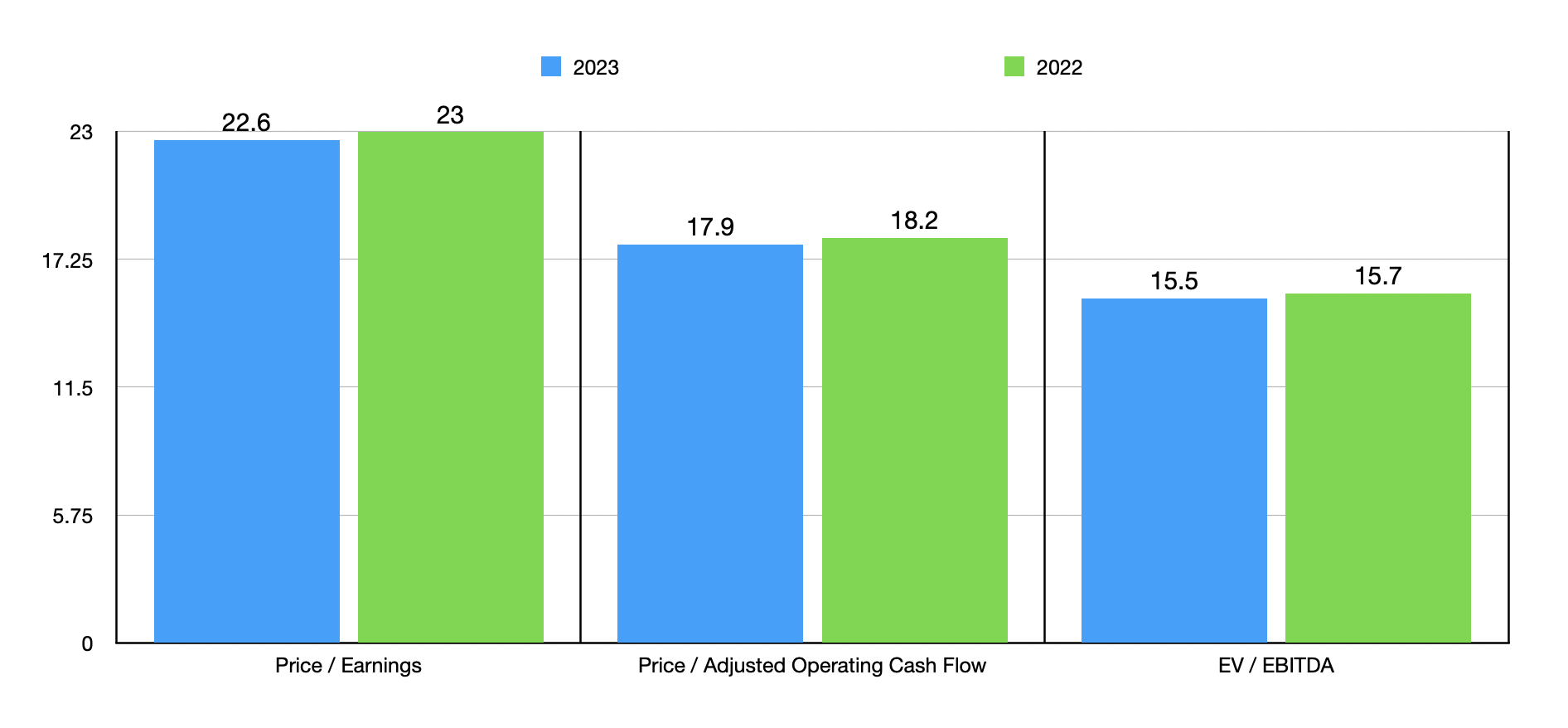

If we assume that management is correct for next year then, using midpoint guidance, we should end up with net profits on an adjusted basis of $451.1 million. This should translate to adjusted operating cash flow of around $569.8 million and EBITDA of approximately $713.2 million. Using these figures, I was able to value the company as shown in the chart above. I also valued it using data from 2023. To me, this looks like a company that is, at best, fairly valued. I then compared the enterprise to five similar firms as shown in the table below. As you can see, on a price to earnings basis and on an EV to EBITDA basis, The Toro Company ended up being the most expensive of the group. And when it comes to the price to operating cash flow approach, we can see that four of the five firms are cheaper than it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| The Toro Company |

| 23.0 |

| 18.2 |

| 15.7 |

| AGCO Inc. ( AGCO ) |

| 7.8 |

| 6.8 |

| 5.8 |

| Titan International ( TWI ) |

| 7.5 |

| 4.7 |

| 5.5 |

| Deere & Co ( DE ) |

| 11.2 |

| 13.3 |

| 9.5 |

| Alamo Group ( ALG ) |

| 18.7 |

| 22.2 |

| 11.0 |

| Lindsay Corp ( LNN ) |

| 20.0 |

| 12.1 |

| 11.2 |

Takeaway

As things stand today, I must say that I am happy that management exceeded forecasts. But it's not like the firm achieved attractive results. Revenue and profits still fell significantly year-over-year, as did cash flows. Perhaps some of the optimism was around not only management exceeding forecasts, but also the statement by management that their new multi-year initiative will result in around $100 million worth of annualized cost savings by 2027. If this does come to fruition, it could definitely have a materially positive impact on the company. But you can't imagine the number of times I have heard management teams prognosticate about cost cuts only to fall far short of what had been forecasted. So until we see actual progress on that front, I don't believe that a premium on the stock makes sense at this point in time.

For further details see:

The Toro Company Is Still Pricey Despite A Solid Earnings Beat