VNQ - The Underperformance Of Dividend-Only-Focused Strategies

2023-11-16 01:32:42 ET

Summary

- Stock prices and returns are in part determined by net cash on the balance sheet and future expectations of free cash flow.

- Dividends are not a driver of valuation and actually decrease the value of a company because cash is paid out to investors.

- Over the past decade, dividend-paying stocks have underperformed compared to "growth" stocks with strong free cash flow generation and balance sheets.

- We hope this article changes the way readers view the dividend, and as a result, helps to better position retirement portfolios for continued wealth creation.

By Brian Nelson, CFA

Stock prices and returns are a function of the components of enterprise valuation, more commonly known as the discounted cash-flow method. Within this process, there are two primary cash-based sources of intrinsic value: net cash on the balance sheet and future expectations of free cash flow. When a company generates free cash flow through the course of the year, the free cash flow is added to cash on its balance sheet, and the value of the enterprise advances, all else equal. If expectations of future free cash flows increase, the value of the should stock increase, all else equal. If expectations of future free cash flows decrease, the value of the stock should fall, all else equal.

Note that the dividend is not a driver of the valuation equation at all. In fact, when a dividend is paid, the amount of cash a company has on its balance sheet is reduced, and the company is actually worth less because the investor now owns the cash, not the company. It's easier to view the dividend as if you were a business owner of a private company. As the full owner of the company, if you pay yourself a dividend in cash from your private company, the cash held in your business is less, and therefore the business is worth less, all else equal. This is why the stock price on an exchange is adjusted downward by the amount of the dividend on the ex-dividend date. That cash the company pays as a dividend is no longer in the business, and therefore no longer contributing as a component to the business' intrinsic value.

Investors focused only on the dividend have suffered underperformance the past 10 years. (The respective ETF sponsors. Image generated by Valuentum.)

During the past 10 years, the main cohorts of dividend-paying stocks, whether the SPDR S&P Dividend ETF ( SDY ), equity REITs ( VNQ ), mortgage REITs ( REM ) or master limited partnerships ( AMLP ) have vastly underperformed the market cap weighted S&P ( SPY ) as well as some of the strongest, net-cash-rich, free-cash-flow generating, secular growth powerhouses in the Schwab U.S. Large-Cap Growth ETF ( SCHG ). In some respects, empirically, the image shows the higher the yield, the lower the total return. Note that the image above is a total return comparison, which includes dividends and the reinvestment of dividends, meaning that the total return for high dividend-paying ETFs in the image above would have been substantially lower had dividends and dividend reinvestment been excluded from the comparison. It's clear that, despite the excitement surrounding dividends the past decade, many investors that focused only on the size of the yield haven't done all that great from a total return standpoint.

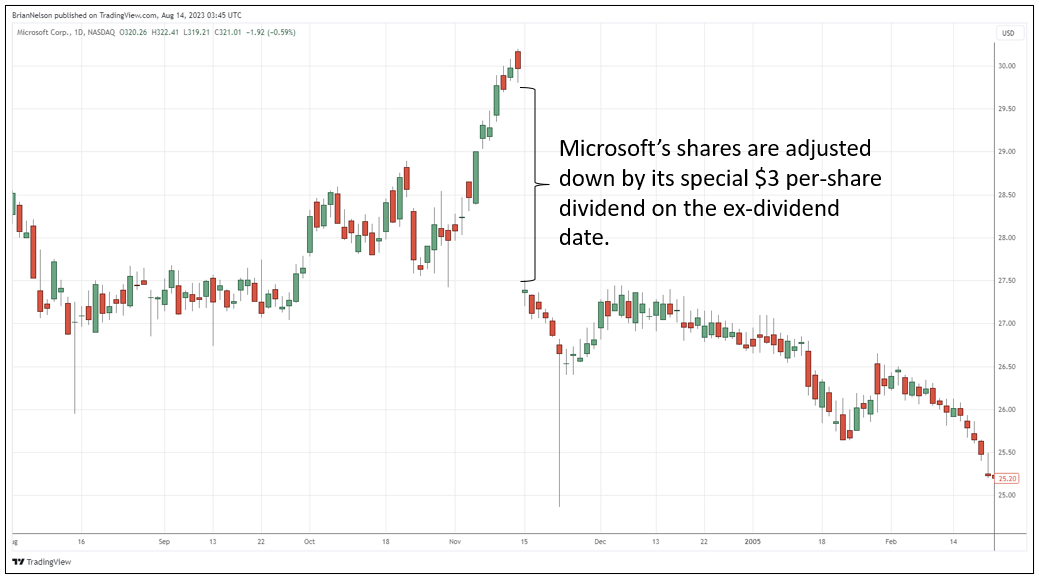

This article is not written to cast a cloud over dividend investing. Quite the contrary, it's to help investors make better decisions with their investment capital. I think it's vitally important that investors understand that the dividend itself is capital appreciation that otherwise would have been achieved had the dividend not been paid. This is why it is so important to add back dividends to capital appreciation in the total return calculation. As explained in the free dividends fallacy , if you have a $10 stock, and it pays $1 in dividends, you don't have a $10 stock and a $1 in dividends, you have a $9 stock and a $1 in dividends. Dividends are not additive like bond coupons, but rather the stock price is adjusted downward by the amount of the dividend on the ex-dividend date. We explain this concept in depth in the following article: " Should Microsoft Pay A Special One-Time Dividend (Again)? "

When a company announces a dividend, its share price is reduced by the amount of the dividend on the ex-dividend date. (TradingView)

{kind=link}

From what we can tell by the most popular articles on Seeking Alpha, many investors seemed to have chased dividends and high yields the past decade, and I guess for a large number of these investors, they likely achieved total return underperformance. Most of the excitement surrounding the dividend can largely be attributed to the ease at which monthly or quarterly income can be structured. However, because the dividend, itself, is not additive to a company's total return, but rather should be viewed as capital appreciation that otherwise would have been achieved had the dividend not been paid, many dividend-only-focused investors are largely chasing stocks that perhaps they never would consider if the stock didn't pay a dividend. This is nothing short of tragic. For investors, especially retirees, it's so important to focus on total return first, as dividends are paid out of total return and are not additive to it.

As a practitioner of enterprise valuation, the discounted cash-flow method, and having learned the ins and outs of the structure of the dividend payment, I've decided that when it comes to my retirement years, my goals will be focused almost exclusively on continuing to generate wealth. I plan to keep some emergency cash and sell off a portion of my portfolio each year in a dynamic withdrawal strategy so that a focus on total return can still be achieved over time. I won't ever fall into the trap of thinking that the dividend is additive to total return, because in reality the dividend payment is just taking away from the capital appreciation component. Again, that's why the dividend return needs to be added back to a firm's capital appreciation in arriving at total return calculations. Had the dividend not been paid, capital appreciation would be higher as more cash would accrue on the company's balance sheet over time. In my retirement years, I don't want to sacrifice the ability to continue to generate wealth by focusing only on the dividend alone.

Valuentum's Dividend Growth Newsletter portfolio. (Valuentum)

That said, we're okay with many dividend payers, but not for reasons that you might think. In our simulated Dividend Growth Newsletter portfolio, we include stocks such as Apple ( AAPL ), Microsoft ( MSFT ), Cisco ( CSCO ), and Oracle ( ORCL ), entities that pay dividends but also generate tremendous levels of free cash flow and have strong balance sheets; it's important to note that it is because of these characteristics that we like them. It bears repeating: We like them first because of their cash-based fundamentals and second because they pay a strong and growing dividend, fitting the profile for inclusion into the simulated Dividend Growth Newsletter portfolio. We're just not interested in lofty dividend yielders just for yield's sake because we know the mechanics of the dividend payment and how it fits into the total return calculation.

Again, this article is not to say that the dividend is something to avoid. That's not at all what I'm saying. Instead, this article is to encourage you to continue to learn about the cash-based components of valuation, what drives intrinsic value and what doesn't, and how to think about dividends in the context of the total return calculation. I want you to learn the ins and outs of the structure of the dividend payment, too. For one of your large dividend-paying stocks, please have a look at the price around its ex-dividend date. You'll notice it is adjusted downward, much like the share price in the example of Microsoft above when it paid a special dividend. Learning the key components of enterprise valuation and what a dividend is and is not could change your entire perspective on investing. Reading this article may not change your focus on dividends, but it might just change the types of dividend stocks that you like in your portfolio. You can find 3 stocks we like for total return that also pay a dividend in this article .

For further details see:

The Underperformance Of Dividend-Only-Focused Strategies