VEOEY - The Upside Is Still There For Veolia Environnement

2023-10-11 10:04:34 ET

Summary

- Veolia is a French water and waste management company with stable inflation-protected business operations and strong revenue growth.

- Veolia has had a successful first half of the year with organic revenue growth, strong net income, and a decrease in net debt.

- I present my updated outlook and upgrade the stock to a BUY.

Dear readers,

Veolia ( VEOEF ) is a French-based water and waste management giant with global operations and annual revenues of over EUR 40 Billion. The company operates infrastructure which is absolutely necessary to our society and has traditionally been operated by governments. This is exactly the kind of stable business that I like to invest into, especially when 70% of revenues have CPI-linked indexation, the company is well managed and has proven to be resilient to inflation and cost increases.

I've covered Veolia before on Seeking Alpha, gave a brief introduction to the business and issued a HOLD rating at EUR 27.50 for the EUR-denominated native share - ticker VIE on the Paris stock exchange. Note that there are also ADRs available under tickers VEOEY and VEOEF.

The reason for not buying then, was the steep 50% rally which the stock had just experienced from the October 2022 low. Frankly, I was expecting a pullback, which never came. Following the recent selloff in utilities, however, we are once more given a chance to load up on shares of this quality business around EUR 27.00 which is why I want to publish an update to my thesis.

{kind=link}

Business overview

To recap, Veolia operates in three main segments: (1) water, (2) waste, and (3) energy.

The water segment, which is the largest of the three and represents roughly 40% of Veolia's business has seen its revenues increase by 8.4% YoY over the first half of the year to EUR 8.8 Billion. The increase was equally attributable to higher volumes (mainly in the US) and higher prices due to tariff indexation in most geographies.

{kind=link}

The waste segment accounts for nearly 40% of Veolia's business and primarily consists of solid waste and hazardous waste. The latter is especially interesting here, because Veolia is the only global player in hazardous waste which happens to be a very profitable business with outsized growth prospects.

Over the first half of the year, waste revenues increased by 3.3% YoY, on a constant FX and scope basis, to EUR 7.3 Billion. The increase was driven almost exclusively by price increases in the hazardous waste segment, especially in North America where growth reached double-digits.

{kind=link}

Finally, the smallest energy segment saw the highest growth of 41% as revenues reached EUR 6.6 Billion, driven almost entirely by significant heat price increases in Europe.

{kind=link}

Financials

Combined, Veolia has had a very good first half of the year with organic revenue growth of 14.2% YoY and 5.2% YoY excluding energy prices. Net income has grown even more as the group has realized about EUR 200 Million of synergies from the Suez merger, with additional EUR 280 Million expected for the rest of the year.

Veolia is profitable and their revenues have proven to be very resilient to inflation and cost increases, but one thing worth noting is that margins are quite low - EBITDA margin of 13% and profit margin of under 3%. Such low margins mean a low margin for error. And since this is a relatively cyclical (and leveraged) business with revenues dependent on commodity and energy prices, it is quite possible that net income will temporarily turn negative at some point in the future. Note that Veolia does hedge energy prices, but not too far into the future as only 50% of 2024 electricity consumption is hedged.

{kind=link}

But so far, despite a tough macro-environment, results have been great and management has confirmed their full year guidance for net income of EUR 1.3 Billion (EUR 1.85 per share), up double-digits from last year.

{kind=link}

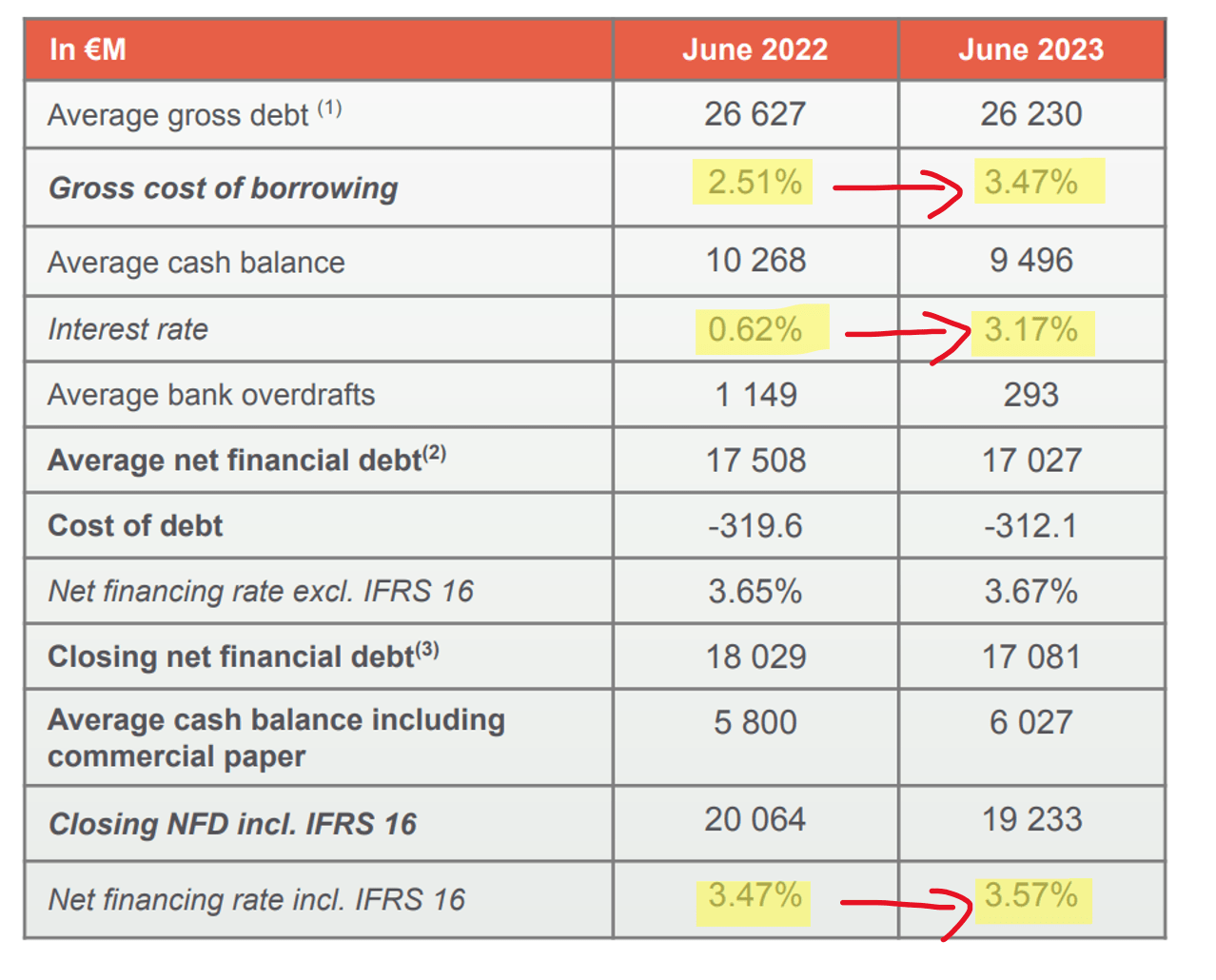

Moreover, net debt has decreased to management's target leverage ratio of 3x and currently stands just under EUR 20 Billion. One thing worth noting is that while the company has a lot of debt, they also have a nearly EUR 10 Billion cash position which now earns interest 5x higher than last year. As a result, despite a 1% increase in the cost of debt, the net financing rate has only increased by 10bps YoY.

{kind=link}

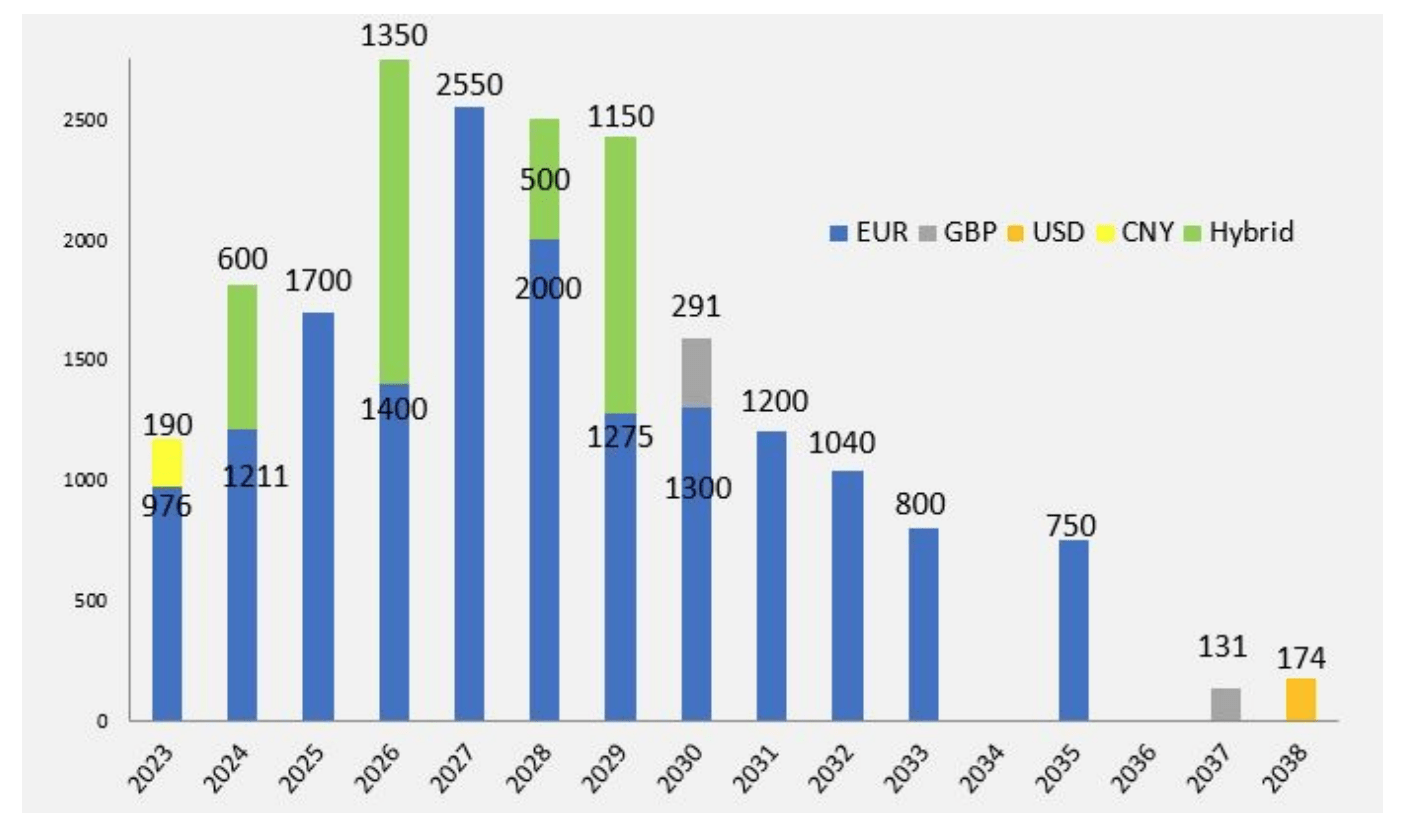

Beyond this year, as long as interest rates remain high, the increase in cost of debt is likely to out-pace the increase in interest income, resulting in increase in net interest expense.

But here's the thing.

Revenues (and earnings) are expected to grow by double digits until at least 2025, which will add roughly EUR 150 Million in additional earnings each year.

Debt, on the other hand, is 80% fixed-rate and maturities until 2025 total EUR 4.8 Billion. Assuming a further 1% increase in interest rates, the net interest expense would increase by roughly EUR 90 Million. Therefore, higher interest rates aren't really a worry for Veolia, because higher cost of debt will get offset by higher earnings.

{kind=link}

This year, Veolia paid a EUR 1.12 per share dividend, which represented a 12% increase over last year and translated into a yield of about 4.1%. For next year, management has declared that the dividend will continue to grow with EPR growth, meaning that another double-digit increase is likely.

Frankly, Veolia faces relatively few risks. The two main ones worth mentioning are (1) high interest rates, which would increase the company's interest expense over time and (2) a decrease in utility/energy prices which could negatively impact revenues (I see this as highly unlikely in the current inflationary environment).

Valuation

The stock currently trades at 14.6x forward (2023) earnings, which the company is well on track to meet. Beyond this year, consensus is for 15%+ EPS growth until at least 2025.

In my last article, I explained why I see a P/E multiple of 18x as justified, for a company of this caliber. At 18x earnings and assuming just 10% EPS growth (which is about 50% below consensus) I get a 2025 price target of EUR 40 per share. That's a 17% return per year, on top of the dividend, from a reputable well-managed company which has proven resilient in the current tough macro-environment.

{kind=link}

Even if the stock trades flat at 15x earnings for the next two to three years, we should earn 9% per year from price appreciation + 4% dividend yield = 13% total annual return.

That's compelling to me, which is why I upgrade Veolia to a BUY here at EUR 27.00 per share.

For further details see:

The Upside Is Still There For Veolia Environnement