VLO - The Wait Is Over: 2 Companies With Freshly Hiked Dividends

Summary

- This article is focused on two dividend stocks that had prolonged periods of zero dividend growth, which upset a lot of investors.

- I start with a theoretical introduction before I show you why Valero Energy and Public Storage finally hiked their dividends and what we can expect going forward.

- Both companies remain high-conviction dividend growth stocks, and I'm buying any weaknesses to add to my positions this year.

Introduction

It's time to talk about one of my favorite topics: dividend investing. In this article, I will give you two fantastic dividend stocks. However, I didn't just pick random stocks from my watchlist, but two stocks that haven't hiked their dividends for multiple years, which technically doesn't make them dividend growth stocks anymore. The stocks I'm talking about are Public Storage (PSA) and Valero Energy (VLO) . Valero ceased to grow its dividend when COVID hit, which did a tremendous number on its free cash flow. Public Storage stopped hiking in 2016 as the company started to focus on growing its business.

That said, both stocks just hiked their dividends. Valero reported a disappointing hike of just 4%, while Public Storage reported a 50% hike.

In this article, we're going to dive into the background stories to make sense of these numbers. I will explain why I'm a buyer of both stocks in 2023 and how investors should interpret dividend growth numbers in general.

So, let's start this article with some theoretical background.

What Dividend Growth Numbers Tell Us

It's more forward-looking than one might expect

What's the definition of dividend growth? It's obvious that it means growing dividends, but how can we define it?

The closest thing I could find to a definition is the explanation I found on Titan , which can be seen below.

Dividend growth investing is a popular strategy with many investors. It entails buying shares in companies with a record of paying regular and increasing dividends . An added component is using the payouts to reinvest in the company's shares-or shares of other companies with similar dividend track records.

A company that hikes its dividend by 2% per year is, technically speaking, a dividend growth stock. However, companies with low dividend growth rates often have higher yields as the market adjusts its expectations over time.

I think we can all agree that these stocks aren't dividend growth stocks.

A typical dividend growth stock tends to have a somewhat subdued yield with a higher annual dividend growth rate. The best dividend growth stocks have decent yields and satisfying growth rates.

As I mention in most of my dividend-focused articles, dividends do not create value. At least not directly. After all, it is just a cash transfer from a company's balance sheet to an investor's bank account. It even destroys value if we consider that taxes apply.

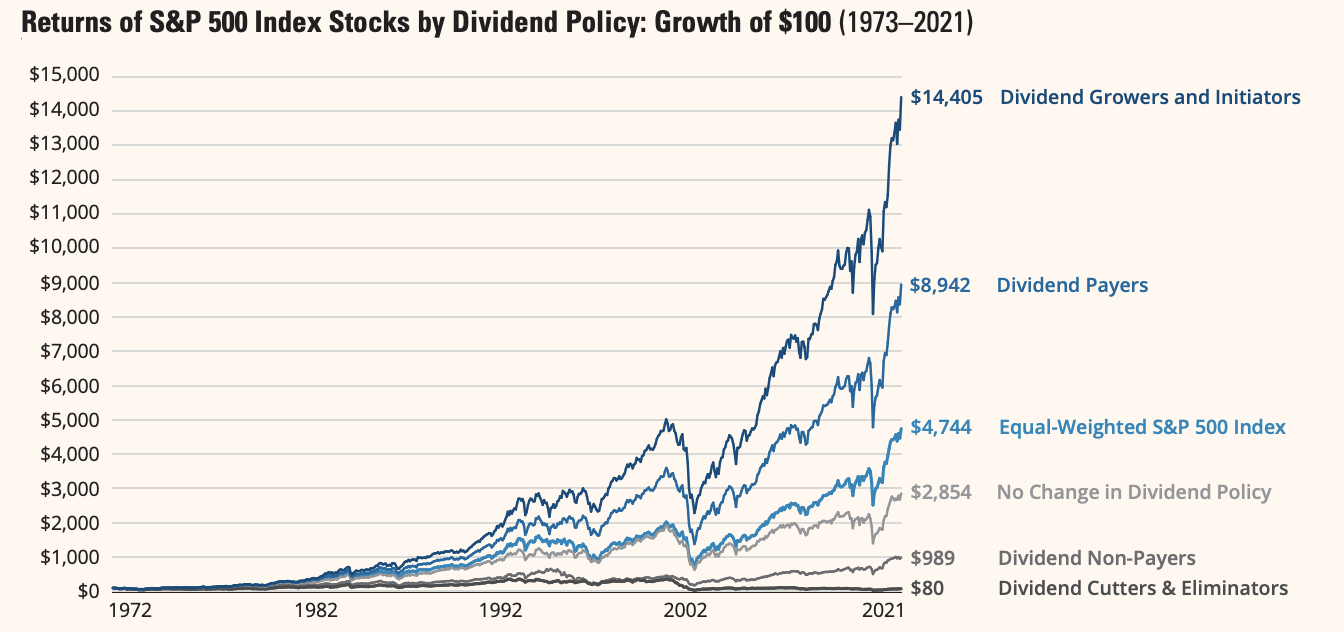

However, indirectly, dividends generate tremendous value. Dividend payers and dividend growers have outperformed the market by a mile in the past, as the chart below shows.

{kind=link}

The reason for outperformance is rooted in the factors that make dividends possible.

If we ignore companies that pay dividends with insufficient free cash flow, it's fair to say that companies that pay a dividend are profitable. Profitability sets a company apart from money-losing companies.

Moreover, paying dividends forces a company to be more rigorous when it comes to cash management. This tends to have a positive impact on the company and its decisions.

Also, companies that can consistently grow their dividend prove that they can stand the test of time. This is the reason why the average dividend growth strategy comes with both outperforming returns and subdued volatility. After all, high-quality stocks tend to sell off less than stocks from lower-quality companies.

With that said, this article focuses on two companies that had a prolonged period of flat dividends. This is often a reason for frustration, as investors often pick companies with consistent dividend growth - and I cannot disagree with that strategy.

However, when I invest in a company, I apply what I like to call an ownership view, where I place myself in the shoes of its management. I don't do that to come up with fancy reasons that justify poor dividend growth but to assess whether or not I should sell a stock after it continues to avoid new dividend hikes. I want to get to the root cause of the issue and determine if it impacts my plan to hold stocks for multiple decades.

With that said, both Valero and Public Storage hiked their dividends recently. Both hiked after a prolonged phase of no dividend growth and high growth in earnings. However, Valero hiked by only 4%, which caused some disappointment.

Hence, I also dove into reasons that determine a company's decision to grow its dividend.

In 2021, Michaely et al. published an article that focused on dividend growth and related issues like free cash flow growth.

{kind=link}

Below is my summary of the paper's abstract:

The central idea of the study is that there is no clear relationship between changes in cash flow (the amount of money coming in and going out of a company) and changes in dividends (payments made to shareholders). The study uses a method to analyze how changes in a company's financial performance are reflected in changes in its stock price. The study finds that:

- Changes in dividends or buybacks (when a company buys its own shares) signal changes in the expected future cash flow volatility (the amount of uncertainty around future cash flows).

- When there are bigger changes in cash flow volatility, there is a larger impact on the stock price.

- Changes in dividends do not have an impact on the discount rate (the rate used to calculate the present value of future cash flows), the level of cash flow news, or the overall stock market volatility.

The conclusion of the study is that changes in future cash flow are the driving force behind changes in dividends , not changes in the discount rate, and that changes in dividends give information about future cash flow volatility .

In other words, while free cash flow or net income growth may be high, it could be completely irrelevant to a company's dividend growth decisions, if it has other plans in mind like M&A or fears that economic growth may be weakening.

With that in mind, I will elaborate on this using Valero and Public Storage as examples. And, as I said in the intro, I will explain why I am buying these companies in 2023.

Valero - Going Beyond The Disappointing Hike

Valero has been a core holding of my dividend growth portfolio since 2020 when I bought the stock after COVID had done a number on global energy demand.

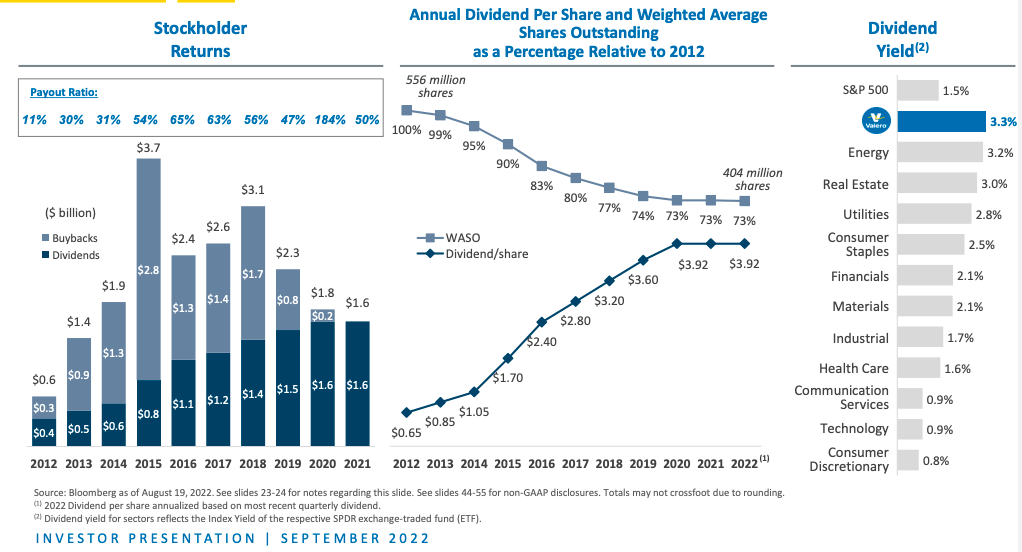

Before the pandemic, Valero had turned itself into a source of high dividend income, high dividend growth, and buybacks. If we ignore the recent hike, Valero has a 5-year average annual dividend growth rate of 7.0%, even though three of these five years had no dividend growth. Between 2012 and 2020, the dividend was hiked from $0.65 to $3.92. During this period, the company bought back 27% of its shares.

{kind=link}

Moreover, the company's dividend usually yields close to 3.0%, which makes Valero a great mix of a decent yield and decent dividend growth. Please note that VLO currently yields 3.2%, NOT 2.3%, as seen in the chart below .

In the case of Valero, there are (interrelated) reasons why the company refrained from hiking its dividend.

- In 2020, the company had negative free cash flow, meaning it had to borrow money to maintain its operations.

- In 2021, its business improved as vaccines provided a path back to normality (light at the end of the tunnel).

- In 2022, the company benefited from a massive surge in margins and volume growth as global supply was subdued after the pandemic when the demand came roaring back. The company did not hike its dividend as it had switched its focus to post-pandemic debt reduction.

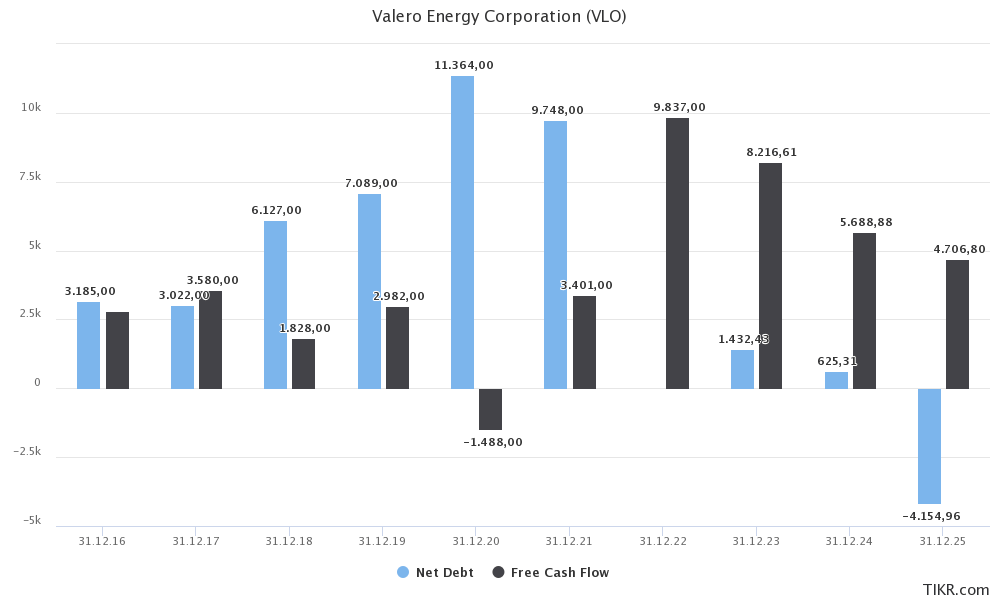

The chart below visualizes this. In 2020, the company had negative free cash flow. When adding dividend payments, we quickly get why net debt soared to more than $11 billion. 2021 was a year of gradual improvement. 2022 was the best year ever, resulting in close to $10 billion in free cash flow. It allowed the company to reduce net debt. This year, net debt is expected to be just $1.4 billion.

{kind=link}

On January 31, I wrote an article titled The Valero Dividend: Time For Takeoff , where I explained that I expected the next dividend announcement to be a hike.

Luckily, that's what happened. The company hiked its dividend by 4.1% a few hours after my article went online (I got lucky, I have to admit).

Anyway, 4.1% is a low number in light of everything we've discussed so far. However, I believe the paper I discussed in the first part of this article explains why that is. Despite Valero's massive success in 2021 and 2022, it is somehow not willing to significantly hike its dividend - despite having a dividend payout ratio of just 13%.

I believe the company is preparing for a poor economic situation. Leading economic indicators are pointing at high recession chances, which will hurt gasoline and energy demand in general. While I expect margins to remain strong due to low supply, it seems like management does not want to commit to higher quarterly obligations (which is what dividends are, more or less).

However, that isn't a huge issue. After all, the cash it generates will still end up as cash, which can be used as buybacks or to give the company even more room to aggressively hike once demand growth returns.

During the Great Financial Crisis, the company cut its dividend. That won't be on the table this time - unless things get incredibly bad, which I don't expect.

Moreover, as the scientific article explained, the dividend decision doesn't have a major impact on the stock price in the mid-term. Even though the company has just hiked by 4% since early 2020, the stock price is back to doing what it does best: outperforming the market.

For now, I am glad that VLO's stock price is weakening again. As I wrote in my prior article, these corrections are common. Especially in this case, investors are implying that poor dividend growth is some form of guidance, which may very well be true.

VLO is now down almost 15% from its recent highs if we ignore the spike caused by the NYSE glitch earlier this year.

FINVIZ

I am a buyer below $120 again, as VLO will be offering a juicy yield. I also expect that long-term dividend growth will remain close to 10%.

However, be careful, as the stock is very volatile. Do not go overweight in cyclical energy stocks.

Onto number two.

Public Storage - This Hike Changes Everything

On January 9, I wrote an article titled Why I'm Aggressively Buying Public Storage This Year . So far, I have indeed significantly expanded my position, and I'm not done yet.

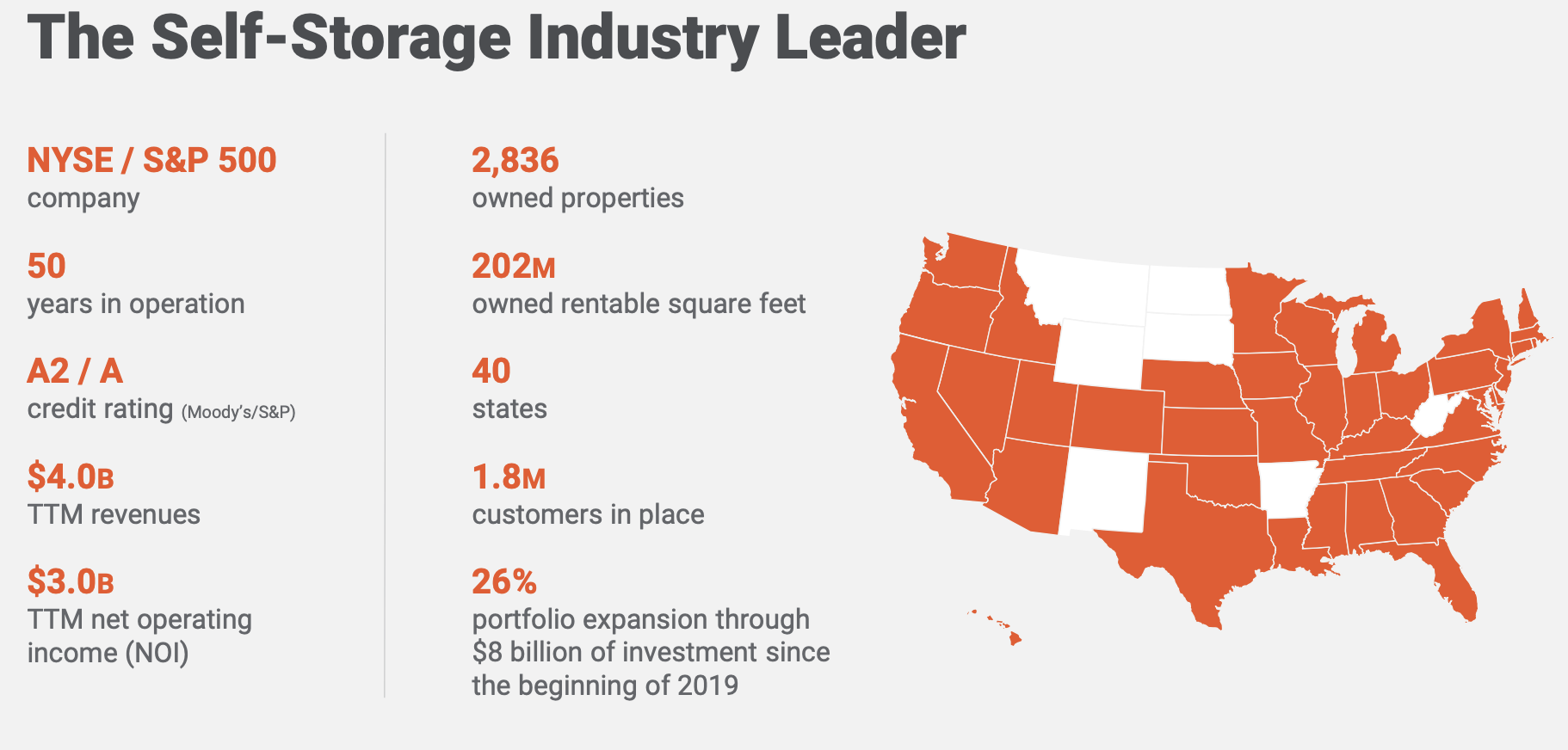

My American readers may be more familiar with the company than my "foreign" readers. Public Storage is a self-storage leader, dominating 10% of the self-storage market in the US. The company is an S&P 500 member with an A-rated balance sheet, owning more than 2,800 rental properties in 40 states.

{kind=link}

The worst thing about PSA is (or was) the fact that it hadn't hiked its dividend since 2016. In 2016, the dividend got stuck at $2.00 per share per quarter. The spike in 2022 was a special dividend related to the sale of PS Business Parks. That does not count as a hike.

Needless to say, investors have not been keen to invest in PSA. After all, better alternatives were on the market that offered a higher yield and consistent dividend growth.

However, I stuck with PSA as I liked what the company was doing. After all, it wasn't actively annoying investors. No, PSA was massively investing in its business.

Since early 2019, PSA has invested $8 billion in external growth, meaning acquisitions, development, and redevelopment of properties. This has increased the portfolio size by 26% (more than 40 million square feet), making it one of the biggest expansions in the company's history.

In other words, the decision to not hike the dividend after 2016 was based on its plans to expand, not the strong financials that would have allowed it to hike. Again, it's what the theories in the first part of this article confirm.

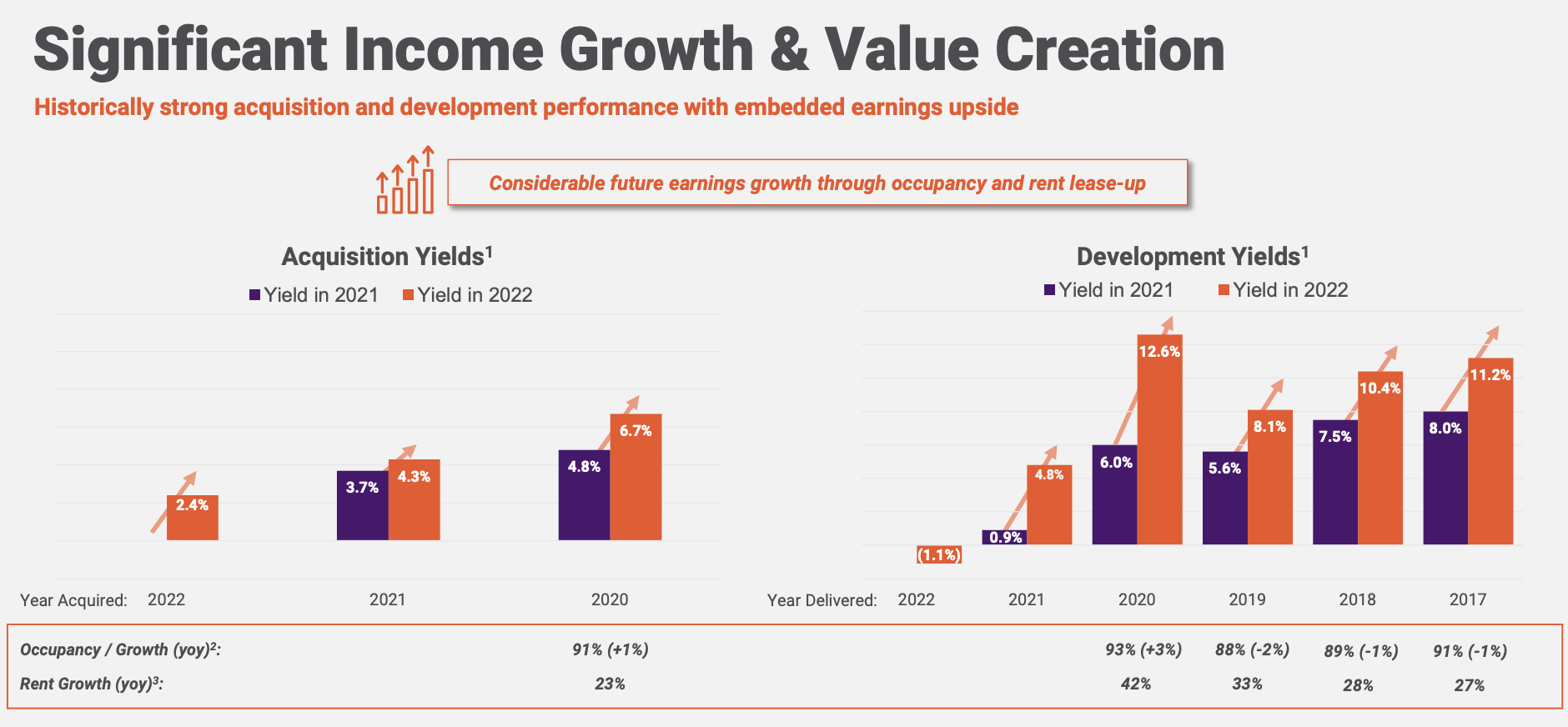

Now, the company is achieving strong rent growth and high yields on acquired and developed assets.

{kind=link}

Moreover, the company's net debt ratio is just 3.3x EBITDA, which includes $4.4 billion in preferred equity.

As a result, Public Storage just hiked its dividend by 50%. The company is now paying $3.00 per share per quarter. This translates to a yield of 3.9%, which is a game changer.

With renewed dividend growth commitment and a high likelihood of long-term annual dividend growth in the mid-to-high single-digit range, I believe PSA will be able to outperform the real estate sector going forward.

That said, I hope to buy more PSA stock at a yield of more than 4.0%.

FINVIZ

I believe that PSA will give us that opportunity, as it will likely have to step up its bid for Life Storage ( LSI ). Life Storage has a market share of roughly 4% and a focus on technologies that will allow using self-storage for last-mile logistics and micro-warehousing.

As I wanted to buy LSI anyway, I think that the PSA/LSI combination is a no-brainer deal.

However, I agree with Seeking Alpha author Matthew Smith that PSA might have to step up its offer. I believe that would push the PSA share price down a bit more.

However, with the parameters and construct of the deal, Public Storage might need to offer a cash component to the deal to take it to around $140/share or increase the equity offer so that Life Storage shareholders receive approximately 0.4539 shares of Public Storage - which would also take the deal value to about $140/share based off of Friday closing prices.

On top of that, I'm still in the camp that believes that the market is too dovish when it comes to Fed expectations. I explained this in great detail in a recent gold-focused article .

Long story short, PSA is back. The hike showed new shareholder commitment. And, based on what we discussed in the first part of this article, I believe there's a high chance that PSA will dial down its aggressive buying strategy for new assets, especially in light of the high-rate environment, which will put a focus on organic growth. That's good news for shareholders.

I'm buying PSA on any weakness this year.

Takeaway

This article was dedicated to two well-known dividend stocks that had prolonged periods without dividend hikes. I used the opportunity to start with some background info, which shed light on how we should interpret dividend announcements.

I also wrote this article because Valero and Public Storage are two of my all-time favorite dividend (growth) stocks. They both offer a decent yield, satisfying (future expected) dividend growth, and fantastic business models.

I'm buying both on weakness this year, as I add more high-yield to my portfolio.

(Dis)agree? Let me know in the comments!

For further details see:

The Wait Is Over: 2 Companies With Freshly Hiked Dividends