SQEW - Themes For Q2: Recession Chatter Weaker Job Market Declining - But Still High - Inflation

2023-04-21 11:47:00 ET

Summary

- April has started off on a fairly strong note, with equities and bonds both pushing higher over the past month.

- This comes at a time when Q2 is fraught with recession worries and a renewed potential for energy shortages.

- How have stocks managed to push out more gains in this environment? Investors are focusing on the good news. Earnings have been reasonably strong and inflation is on the decline.

Main Thesis & Background

The purpose of this article is to discuss the broader macro-market with a general focus on both stocks and bonds. The premise here is to discuss the resiliency of both these sectors in the face of what seems to be a difficult economic period.

While underlying conditions are not terrible, investors are bombarded every time with headlines of geo-political crises and of the impending recession. These themes have been consistent for over a year now, but here is a snapshot of recent news articles just this past week as examples:

News Headline (Morgan Stanley) News Headline (Yahoo Finance) News Headline (CNBC) News Headline (Bloomberg) News Headline (The Guardian)

{kind=link}

{kind=link}

{kind=link}

Yet, with all these headwinds, investors have been fairly complacent domestically. In this review I will examine some of the reasons behind this disconnect and also the likelihood on whether that can continue.

How Are Stocks (And Bonds) Going Up?

As I mentioned above, there is quite a bit to "worry" about in a global context right now. That may always seem like the case - but the world has changed very rapidly over the past few decades. It is difficult to see any local geo-political crisis as purely local. Whether there is a banking crisis in the U.S., a military conflict in Eastern Europe, or political unrest in China, all of these have potential for global consequences.

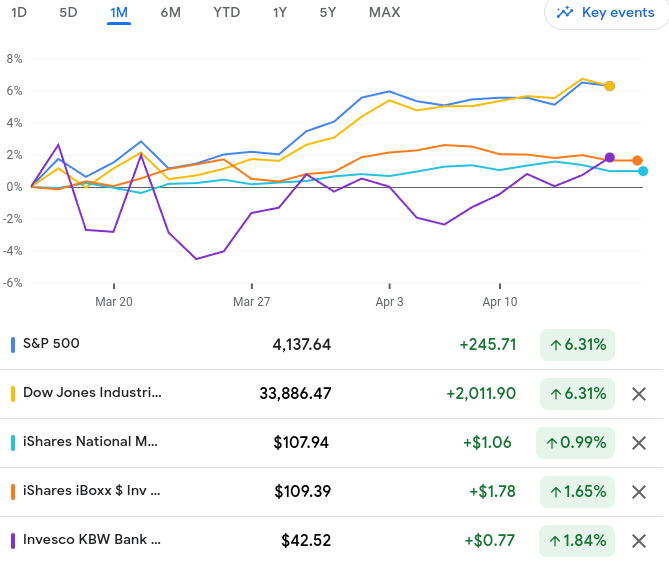

In may seem somewhat surprising then that despite all these headwinds, both stocks and bonds have been pushing higher in the short-term. If we look at the past month, we see equities have risen along with municipal bonds and corporate IG bonds. This has been an across-the-board bump, with even the banking sector seeing a healthy gain despite two bank failures!

1-Month Returns (Google Finance)

{kind=link}

This kind of dynamic is something to scrutinize. How can stocks and bonds be performing so well with so much uncertainty in the world?

The answer is multi-fold and not entirely straightforward. There are always a lot of moving pieces in the global and domestic economy and pinning down the reasons for short-term moves can be difficult to comprehend. Oftentimes markets behave irrationally anyway - so even if an explanation sounds plausible it may not be correct!

In this vein we have to consider a number of elements. One, many of these "headlines" have been issues for a long time. Think recession risk and Russian involvement in Ukraine. These are both stores that have garnered attention for over a year, if not longer. Yet, life goes on. It may very well be possible that investors are getting recession or Russian "fatigue". By that I mean the importance of these headlines is waning because we keep hearing about them and not much seems to change.

Two, let us remember how poor a year 2022 was. Both stocks and bonds took it on the chin (with notable exceptions like Energy). The significance here is that while equities and fixed-income assets may be rising in value now, they are still down on a longer term horizon. So that offsets some of the gains we are seeing now, especially for investors who held through last year's pain:

2022 Calendar Year Returns (FactSet)

What I am getting at here is that we started from a pretty bad place when 2023 got underway. So while positive momentum is a welcome sign, some of this can be attributed to a bounce off pessimism, rather than true optimism for the future. It is a slight, but important difference.

Three, perhaps things really aren't so bad as the headlines make them sound. This is central to any bull case at the moment and trumps the other two aforementioned points. If the headlines are noise and solely distracting us from the positive backdrop of the economy, then investors want to be buying. While I would hesitate to make this declaration across the board right now, I think it very well is the case in select areas. Namely this includes the banking sector - an area I am now a bull on.

This may seem counter-intuitive given the problems plaguing the sector of late. Recent bank failures have stung investors are shattered confidence. And banking stocks and the indices that track them have fallen hard. But I view that as an opportunity in large-cap banks especially. I personally believe those institutions are strong and will get stronger as a result of smaller bank failures. They will pull-in assets and face greater regulatory scrutiny - making them safer as a result.

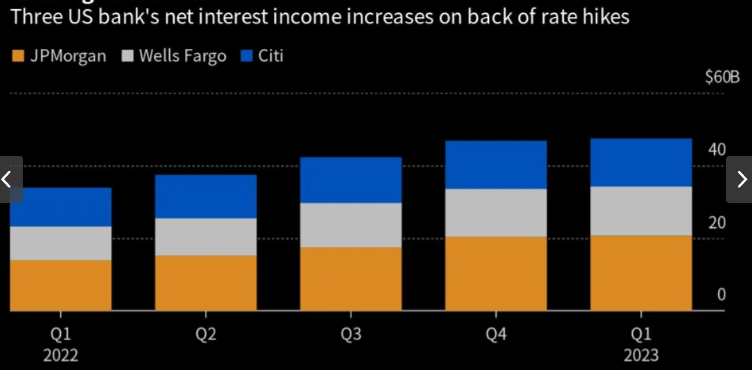

But don't just take my word for it. With earnings out last week from many of the nation's top financial institutions, we can see quite clearly have they fared in Q1 this year. Importantly they seem to be benefiting from the higher interest rate environment. This is a distinct competitive advantage they have over their smaller counterparts that haven't enjoyed the same level of success:

Net Interest Income (Federal Reserve)

{kind=link}

Put simply, the larger banks weren't impacted by the same pressures as failed institutions like Silicon Valley Bank and Signature Bank. They didn't go overweight treasuries and weren't forced to sell those assets at a discount. Instead, they have used higher rates for lending and loan growth. This has driven increased revenue from lending operations and trickled in to the net interest income growth the above graphic is highlighting.

This is just one example but it demonstrates why I like buying Financials / Banks despite the macro-issues facing the economy. This is a sound sector underneath the surface and although it will undoubtedly come under pressure when the U.S. hits a recession, current prices have dropped enough for me to give plenty of merit to buying now.

*I own JPMorgan Chase ( JPM ), the Vanguard Financials ETF ( VFH ), and the Invesco KBW Bank ETF ( KBWB ).

Investors Focusing On Inflation - In A Good Way

In the prior paragraph I ended with a discussion on the banking sector. But I opened up the review by mentioning how stocks have gone up across the board (in terms of sector performance). So it is not just banks or banks' earnings that have pushed equities higher. There is more to the story than that.

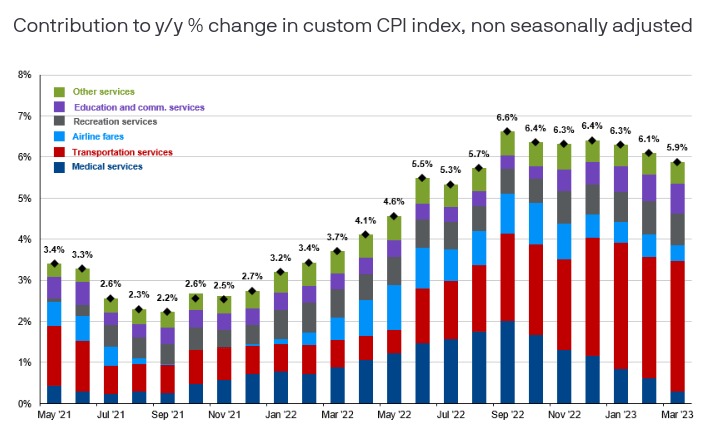

Perhaps chief among the reasons for recent gains is inflation. This may also sound counter-intuitive because any American knows prices are still quite high in both good and services. While we are starting to learn to live with it, it is not easy, especially for those in lower income brackets. If we look at CPI figures, we may see relief in sight, but the reality is that 5.9% growth in prices is very high historically:

{kind=link}

How can it be that this type of environment is leading to rising stock prices?

The answer resides in what investors are focusing on. It really isn't almost 6% inflation that they are concerned with. It is the fact that inflation is declining on a month-over-month basis for the fourth consecutive month. While I might argue that inflation is still too high and the drops on a monthly basis on not that meaningful, the market clearly disagrees.

The bullish case investors are deriving from this is that inflation has peaked and better times lay ahead. That could certainly be true. The only facet is that if inflation has indeed peaked and will continue its consistent decline, then the Fed is going to shift its stance to more dovish. This is probably the central tenement to why investors are viewing this positively. If the Fed has reached its peak rate, that removes one of the biggest headwinds for both stocks and bonds and could signal the start of a new bull market for both.

In fairness, we have to stay level-headed here. I am not going to suggest I know with certainty where interest rates are going to end up later this year. But let me remind readers that I loudly proclaimed my disagreement with the "transitory" messaging on inflation for years - and I was right. Similarly, I think I will be well served to not over-estimate a Fed reaction to a few months of declining inflation. They have not hinted at meaningfully cutting rates any time soon. So even if we see an end to hikes, rates are going to be elevated for longer than many think.

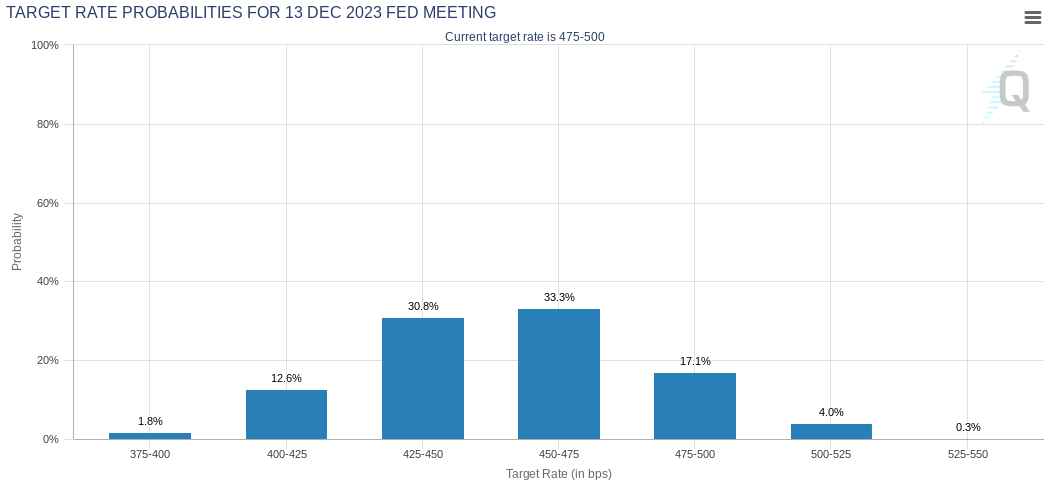

I'm actually not really going out on a limb by saying this. According to CME's FedWatch Tool, the bond market expects rates to end 2023 either a quarter point or a half point below current levels. While I think this may be a bit too optimistic, the premise of not expecting major cuts from the Fed is the same:

Target Fed Funds Rate (Dec '23) (CME Group)

{kind=link}

What I would urge here is caution. Don't buy in to the hype of a sharp change in tone from the Fed just because the CPI number fell under 6%. That is still a high number, and Fed officials agree, so I think the elevated rate is going to be in place for a while. This could pressure cyclical and longer duration sectors, so stay balanced and diversified.

Wages Rolling Over?

One of the pillars of this economy's resiliency (in the U.S.) has been the labor market. Since the Covid-19 pandemic turned the world upside down, one of the biggest surprises has been home quickly the professional world adapted. Companies shifted to remote and hybrid work roles and employees were more than willing to oblige. This kept the Covid-recession brief, wages high, and household spending at reasonable levels.

This being the case, why I am concerned now? Why the "weaker job market" in the title of this review?

The answer is that the labor market, while still strong, is showing signs of cracking. This is similar to the Fed-rate outlook in that there isn't a clear signal for a massive shift underway. But it does suggest we may have reached peak employment in the same way we have reached peak interest rates.

For support let us look at a few factors. One in particular is the high-level layoff announcements we have seen pretty consistently over the past 3-6 months. This originated in the Tech sector and has ballooned to banking, retail, and others:

Job Losses (Wall Street Journal)

{kind=link}

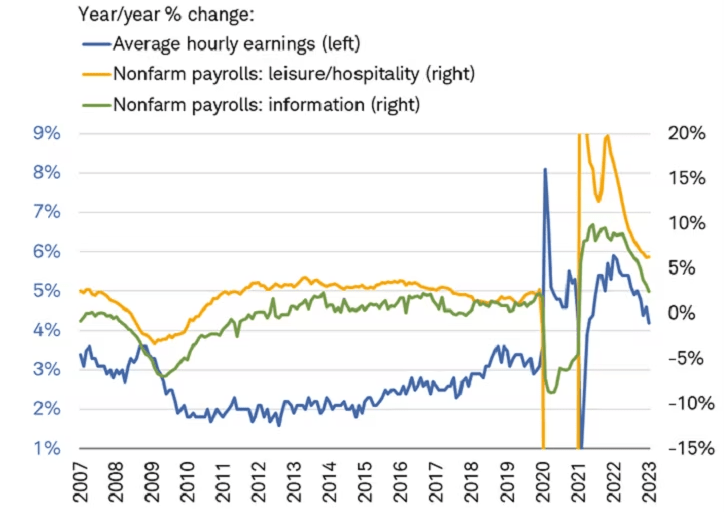

Perhaps as a result of these cuts, wages are starting to feel the pressure too. Again, similar to inflation metrics, wage gains are still high historically speaking. But if we look forward it is hard to notice that wage gains are slowing down in a measurable way:

Wages (YOY Change) (Charles Schwab)

{kind=link}

This is sure to have ripple effects in areas like consumer confidence and retail spending. It could also pressure lenders and credit card delinquency metrics. This is not meant to sound alarmist - YOY growth in wages is a positive thing. While the slowdown is concerned, I wouldn't start outright selling any positions on this metric alone. But it is something to monitor, and makes me reluctant to build on my positions in consumer-dominated funds like the S&P Retail ETF ( XRT ), or other cyclical areas.

*I own a position in XRT and recommended it in March. After a 3% gain, I am more neutral on the fund until a catalyst emerges to change that outlook.

How To Position For Q2 And Beyond

There is a lot to digest at the moment. The good news is we have seen stocks and bonds rally a bit and savings rates are much higher now than they have been in a long time. This means investors who are worried about short-term prospects can lock-in some gains and protect their cash while earning a reasonable return. That is something I did in February and will likely do again if stocks keep rising. I recently made the case for putting cash to work, and I did. But I will shift back to cash if stocks and bonds keep rising while the broader economic cycle weakens. That is the prudent move.

For others who want a more proactive approach, consider specific sectors like banking. Or look overseas. While growth in the U.S. is anticipated to slow in 2024, the same isn't true for the rest of the world:

Economic Growth Projections (IMF)

This means those who expect a slowdown domestically can look outside U.S. borders for value. I am one such person, and have built positions in the developed markets of Canada, the U.K., and Ireland, with a focus on some emerging markets like China as well. That is a theme I think is relevant at this very moment, but will continue to be relevant in to next year too.

*I own positions in the iShares MSCI Canada ETF ( EWC ), the iShares MSCI United Kingdom ETF ( EWU ), and the iShares MSCI Ireland ETF ( EIRL ). I have also written positive on emerging markets recently and am considering a position in the Schwab Emerging Markets Equity ETF ( SCHE ).

Bottom-Line

I often say to ignore headlines but that isn't always the case. I think when the market gets disconnected from reality, monitoring headlines is very important. That is the case now, with a lot of pressure on the U.S. economy being simultaneous with positive market moves. While I enjoy the profits - that makes me cautious.

Looking ahead I see reasons to be very tactical with new positions, including the U.S. banking sector and global developed and emerging markets. I also see a lot of merit to locking in higher yields in both savings accounts/CDs and bond funds, as the Fed is probably at peak rates, or will be very soon. This means investors have a lot of options and shouldn't be mindly sitting in the S&P 500 waiting for a correction. Be proactive now and welcome any forthcoming volatility, rather than fearing it. With Q2 underway, I expect an uptick in volatility soon, and I hope this review helps readers plan for it.

For further details see:

Themes For Q2: Recession Chatter, Weaker Job Market, Declining - But Still High - Inflation