IMO - There And Back Again: A Texas Pacific Bubble Story

2023-05-30 15:15:26 ET

Summary

- Fundamentals always win out in the end, but price action can drive you crazy till then.

- The baby bubble of Texas Pacific Land Corporation matured into a fully-filled, helium offering in late 2022.

- But like the Bilbo Baggins story, we are now back to square one.

- We review where things stand and where we would deploy our long-short trade again.

`The Texas Pacific Land Corporation ( TPL ) thesis was based on some simple facts. We did not dispute that the company owned prime land for oil and gas. We were also not disputing its model was safer compared to the vast majority of oil and gas plays. What we did have a problem with was the stupid valuation.

When we last wrote about it, we did stick to that primary theme.

Since we started covering TPL, our calls on this stock have produced annualized returns well in excess of 100% while the stock is actually down by 12%. There is a lot of room for disappointment from these levels and if we consider the possibility of $80/barrel and $3.50 gas for one year, it is easy to make the case for a $1,000 stock. On the other hand, thanks to low expenses, TPL, like other royalty plays, remains a poor way to leverage triple-digit oil prices. Yes, we are still bulls on commodities for this decade, but TPL is now again, the last place to play it for us.

Source: Texas Pacific: Full Value

That confidence came back to bite and in a big way. Russia's invasion of Ukraine and the resulting oil price spike sent TPL from overvalued to bubble territory. Of course, like all bubbles, the euphoria did wear off, taking TPL right back to square one.

Full Value

We look at why this played out the way it did and where it goes next.

Q1 2023

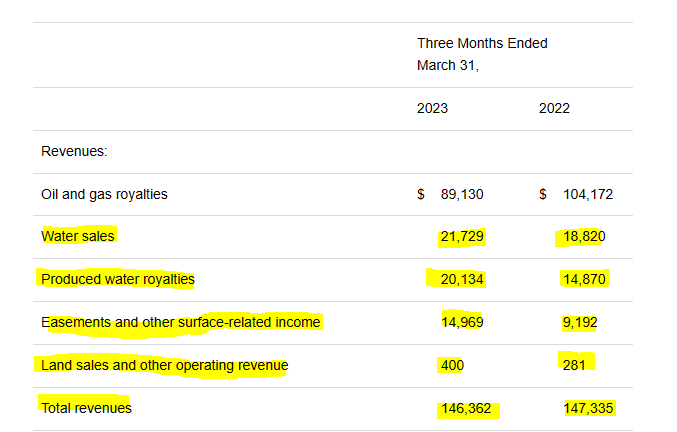

As oil prices went back down to pre-2022 levels, TPL faced tough comparatives in the first quarter. The company did get a small bump from volumes, and total barrels of oil equivalent per day (MBOE/D) did increase marginally. But it was all the lower-value natural gas and NGLs that pulled this up. Oil production declined marginally on TPL's lands.

TPL Q1-2023

Combined with the price decline of all three key commodities, TPL reported royalties that were 23% lower. A quick glance at the realized prices shows that the current strip is even lower and Q2 2023 numbers are likely to be lower than Q1.

TPL Q1-2023

While direct oil and gas sales off the land carry the day in the case of TPL, the secondary sources of income did step up remarkably to pull revenues almost as high as 2022. Note that the total for oil and gas royalties below contains an additional $8.7 million of one-time income that is not included in the royalty figures above.

{kind=link}

Sadly, earnings per share dropped from $12.65 per share to $11.25 as legal and professional expenses ballooned almost 10X from 2022 levels. This is due to ongoing litigation, and a great read on this can be found here .

Outlook & Valuation

While oil may dip below the $70/barrel mark, we think it is unlikely to average well below it in 2023 or 2024. The key reason is that any sustained move lower is likely to prompt a refilling of the Strategic Petroleum Reserves. On the upside, since we are likely already in a recession, we see $80-$85 capping the price for now. There is considerable uncertainty here as OPEC's spare capacity is thin and geopolitical factors can overwhelm small supply-demand imbalances at any time.

On natural gas, current supply levels are overwhelmingly bearish and at a minimum should cap the price under $3.50/MCF (on average) over the next 12 months. Based on our outlook, TPL should deliver about $50 of earnings in 2023 and perhaps $55 in 2024. This is lower than consensus, but then again, we barely have anyone covering this stock.

Based on those numbers, TPL does not look very expensive relative to its own history. Using another metric, EV to EBITDA, also shows the company at the lower end of its relative valuation.

Verdict

While moving to the lower end of its valuation might seem like a positive thing, there are 4 key reasons we would stay away at this point.

1) The first being that the bulk of that 10-year chart shown above was with 0% interest rates. Don't expect previous troughs to hold when 5.25% is being offered risk-free.

2) Extreme overvaluation tends to end with extreme undervaluation. So even assuming oil prices stay firm, we could see a 10-12X EV to EBITDA multiple in 1-3 years. That would forecast a very poor total return from here, even accounting for buybacks and dividends.

3) Texas Pacific Land Corporation is still in a mini bubble of sorts relative to other royalty plays. We have shown Freehold Royalties ( FRU:CA ) and Viper Energy Partners LP ( VNOM ) as comparatives. There is still a comical difference here and one that could be a headwind.

4) Finally, TPL faces increasing competition from traditional exploration and production plays. The royalty model has long been hailed as lower risk and a better return setup. That might have convinced the masses in the past, but we will note that the bulk of the oil companies have really cleaned up their balance sheets. They still trade incredibly cheap relative to TPL.

These numbers make a huge difference in the free cash flow yields you generate. Imperial Oil's ( IMO , IMO:CA ) market capitalization and buybacks in Canadian dollars over the last 12 months are shown below. For comic relief, we have shown the same for TPL.

One could argue for perhaps a 2-3 multiple premium, that we see with Freehold or Viper Energy, but it is hard to envision paying 10-12 extra turns of EBITDA for TPL over quality exploration and production companies.

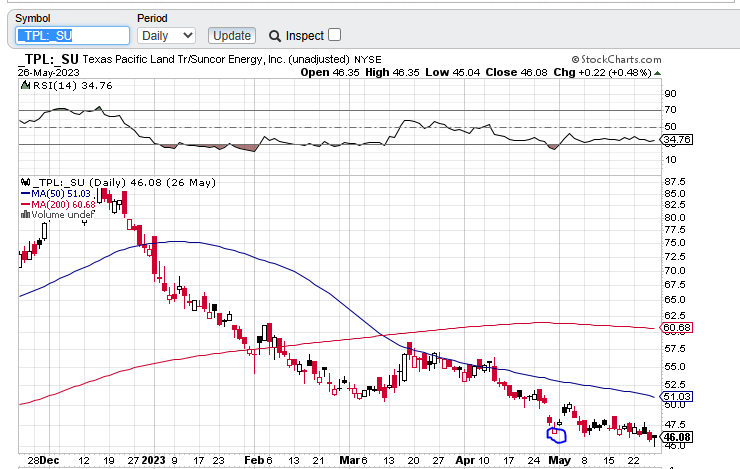

We actually did play this thesis out with Long-Short plays. We were long both Suncor Energy Inc. ( SU ) and Whitecap Resources ( WCP:CA ) against TPL. Those were closed out profitably as the two eventually outperformed TPL. It was not a pleasant experience as the TPL bubble went further than our wildest expectations. We closed the Short Texas Pacific Land Corporation-Long Suncor Energy Inc. trade on April 27 (circled) and we use their ratio as a guide here. We would look to reenter this paired trade if the TPL:SU ratio hit the 200-day moving average line.

{kind=link}

Till then, we don't plan on trading Texas Pacific Land Corporation stock.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

There And Back Again: A Texas Pacific Bubble Story