NNN - There Might Not Be Another Chance Like This For Years

2023-08-17 08:05:00 ET

Summary

- Today, you have a rare opportunity to win big with REITs.

- REITs have crashed even as their cash flows rose.

- Let others panic. I explain why this is an opportunity.

Co-produced by Austin Rogers.

There is a crazy mismatch in the market right now as it concerns real estate investment trusts ("REITs") between weak investor sentiment and strong fundamental performance .

Second-quarter REIT earnings releases thus far have been almost uniformly strong, meeting or beating consensus estimates for funds from operations ("FFO"). Meanwhile, stock prices for many top-tier REITs have only barely budged higher, while the broader, tech-driven market is soaring.

Compare the 12-month performance of the Vanguard Real Estate ETF (VNQ) to that of the S&P 500 (SPY) and Nasdaq 100-Index (QQQ):

The market seems to be convinced that REITs are facing serious and long-lasting headwinds that will meaningfully damage their ability to grow in the long run. Therefore, many investors are avoiding REITs altogether rather than looking for value.

We think this pessimistic sentiment basically derives from three erroneous ideas:

- REITs are heavily invested in office buildings ("commercial real estate = offices")

- Rising interest costs are weighing on REITs' profits

- Elevated interest rates destroy REITs' business models.

Let's address all three points and finish by taking a look at five high-quality REITs trading at what we view as crazy discounts to their fair values and fundamental performances.

REITs Do Not Equal Office Buildings

On the first point, if you watch financial media for any length of time, you'll inevitably hear commentators equating "commercial real estate" with office buildings, and we all know the difficulties facing office real estate right now amid the new hybrid work environment.

Even industry insiders sometimes equate the two. See, for example, the title given to this sentiment survey from the Real Estate Roundtable:

Real Estate Roundtable

The survey is about all CRE, but stress in office CRE in particular appears to be dragging down sentiment for all CRE.

What about the idea that a big drop in downtown office utilization and values will have a negative effect on the cities in which they're located? Keep in mind that most non-office real estate properties, and most of the properties in REITs' portfolios, are located outside of downtown areas.

It isn't a big leap in the mind of the average investor to go from "commercial real estate" to "REITs." And yet, only about 5% of the REIT index consists of office REITs.

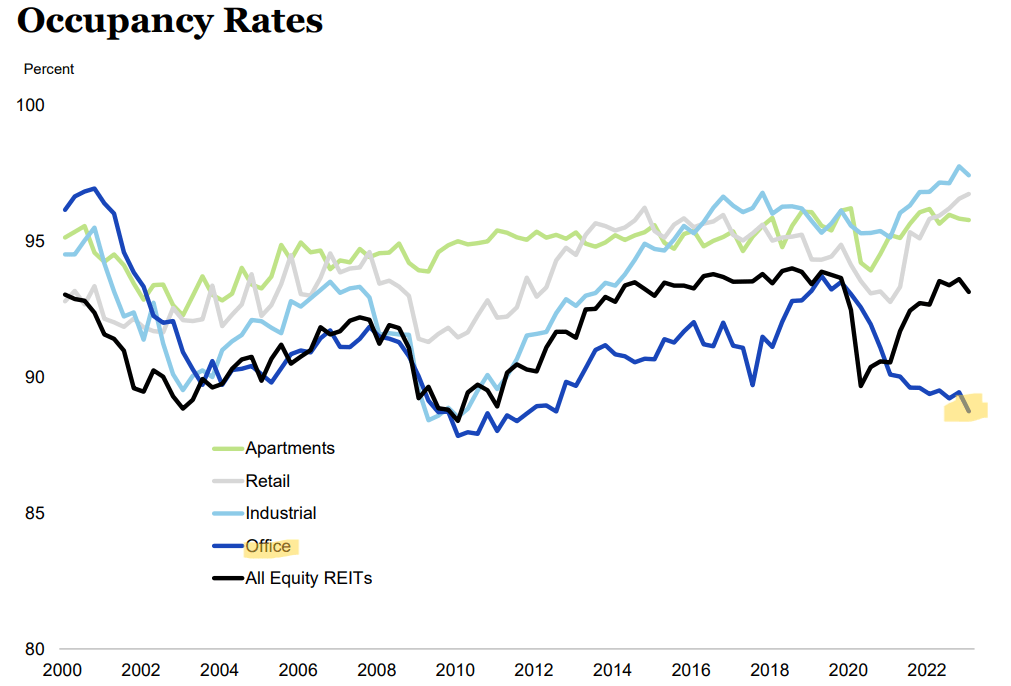

You need only look at the occupancy rates of the four main sectors of CRE to discover that REITs do not equal office.

{kind=link}

While office occupancy has indeed plummeted since the onset of COVID-19, occupancy of apartments, retail, and industrial remains at or near their highs.

Rising Interest Rates Versus Rising Rents

The market treats REITs as totally helpless in the face of rising interest rates, almost mechanically discounting REITs as rates ratchet higher.

But the market seems to forget that REITs have professional management teams whose job it is to maximize rent and minimize interest costs. Most of them do a very good job at this.

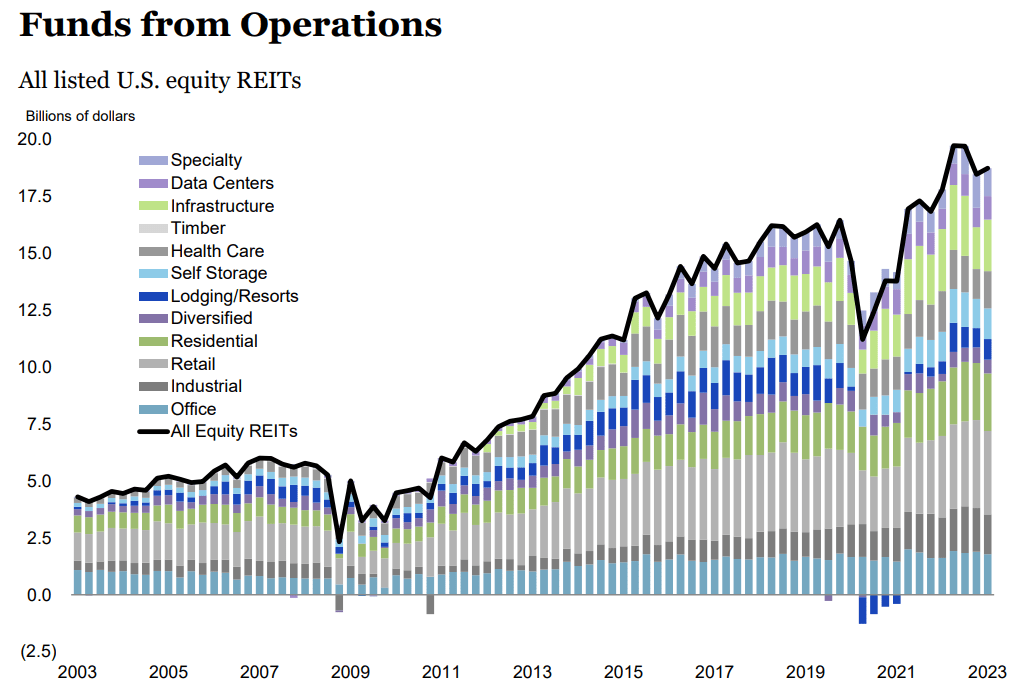

Hence we find that REITs' total FFO has surged higher since the onset of COVID-19:

{kind=link}

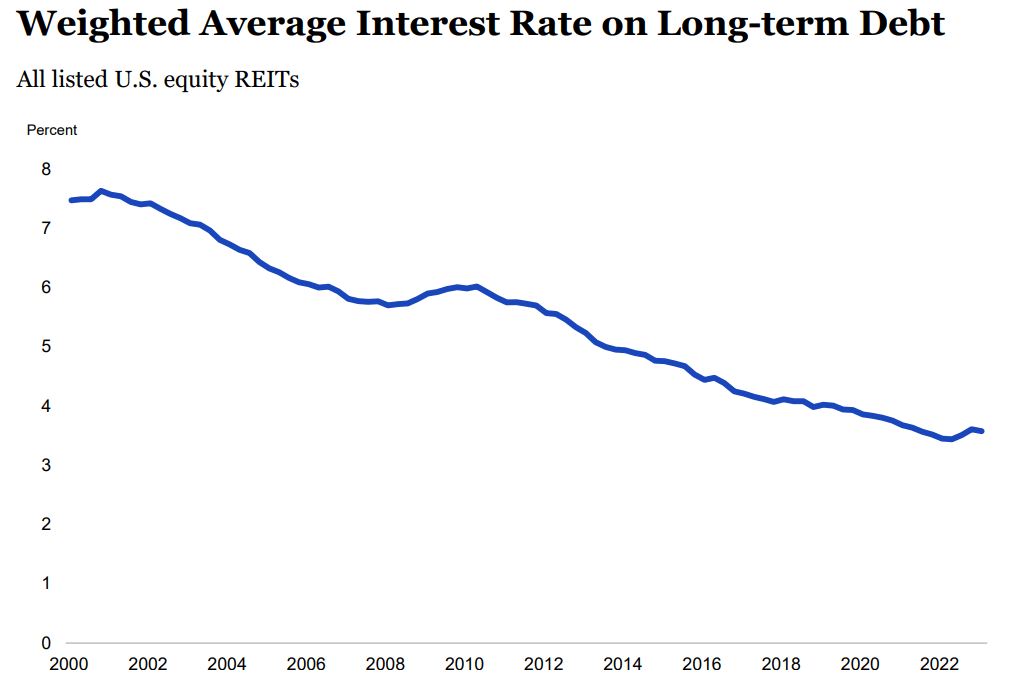

Moreover, REITs' weighted average debt maturity sits at about 8 years, and (generally speaking) relatively few of their loans mature and require refinancing on any given year. During the low interest rate period of 2020 and 2021, REITs very actively refinanced debt, pushing out maturity dates as far as they could. Many of them, like Alexandria Real Estate (ARE) and NNN REIT (NNN) refinanced expiring debt with 30-year bonds during that period.

That is why the weighted average interest rate on REITs' debt has only barely budged higher in the last year even as interest rates have surged.

{kind=link}

Of course, the longer interest rates remain elevated, the higher their weighted average interest rates will go. But while higher rates are a short-term headwind, they can be a long-term tailwind, because of the next point.

Higher Interest Rates Contribute To Less Future Supply Of Buildings

In the long run, higher interest rates (combined with higher labor and construction costs) act as a massive boon to commercial real estate and especially to REITs, because it will result in far fewer new development projects coming to market.

As we all learned in Econ 101, the economy is basically operated on supply and demand. If the supply of something stays flat while demand grows, the price typically goes up. This is true of real estate as much as for any other sector of the economy.

When interest rates and input costs go up, development of new real estate properties grinds to a halt, which leads to fewer new properties coming to market to compete with the existing stock a year or two down the road.

That's exactly what we've seen happening over the last year or so in the CRE development industry.

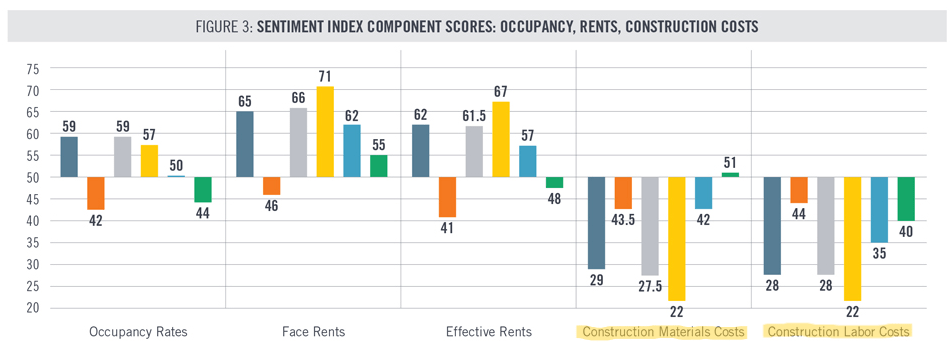

Here's a chart showing sentiment among CRE developers related to their views of whether various components will be higher or lower in 12 months' time.

{kind=link}

As you can see, over the past year, they have mostly viewed occupancy and rents as headed higher while construction and labor costs have likewise headed higher. Only recently have developers started to see the light at the end of the tunnel for construction costs -- envisioning an end to materials cost increases.

What does this do to development activity? It causes much less of it to be greenlit.

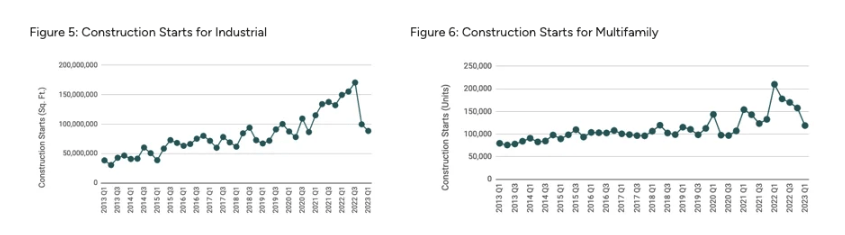

Take a look at this chart of industrial (on the left) and multifamily (on the right) construction starts going back 10 years:

{kind=link}

Although starts spiked in 2021 and early 2022, they have since collapsed to very low levels as the costs of land, labor, materials, and capital have soared. The same thing is happening all across the CRE spectrum right now. Very few new projects are breaking ground for any type of real estate.

What does this mean for REITs? It means that after the (manageable) wave of new supply of properties comes to market this year and next year, there will be a steep drop-off in 2025-2026 and potentially beyond that.

Less supply combined with growing demand should result in rising rent rates.

Five Examples Of Performance-Sentiment Mismatches

Let's briefly look at five REITs that we believe exhibit this huge mismatch between strong fundamental performance and weak investor sentiment. To illustrate, we'll just use one valuation metric: price to operating cash flow (or "CFO"), because cash flow is one of real estate's primary channels of delivering returns.

First off: Agree Realty Corp (ADC), a triple-net lease REIT focused on investment grade, single-tenant retail properties leased to the nation's leading retailers like Walmart (WMT), T.J. Maxx (TJX), Tractor Supply Co. (TSCO), and Home Depot (HD).

ADC enjoys a BBB credit rating, very little debt maturing before 2028, the highest quality tenant roster in the net lease REIT space, and a skilled management team. And yet, ADC is near its cheapest valuation of any time in the last five years.

At a price of around $69, ADC trades at a price to AFFO of 17.5x, compared to its 5-year average of 19.6x.

Next up, consider Alexandria Real Estate Equities (ARE), the only pure-play life science REIT that owns and develops state-of-the-art, Class A research & development properties in the nation's most innovative research clusters. The REIT just reported an earnings beat on continued strong demand for its top-tier lab space, even if leasing and rent rate growth is normalizing from its elevated, COVID-era levels. ARE also enjoys a BBB+ credit rating and no debt maturing before 2025.

And yet, partially in response to activist REIT investor Jonathan Litt's short report, the REIT trades near its lowest valuation in 5 years.

At a price of $127.50, ARE trades at a price to AFFO of 16.9x, compared to its 5-year average of 25.5x.

Much the same could be said about US-based telecommunications REIT Crown Castle (CCI), which owns a vast network of wireless towers, small cells, and fiber across the country. The market seems to be focused on the fact that management slightly trimmed AFFO per share guidance for 2023, lowering their growth estimate from 3% to 2%.

Moreover, the market also seems pessimistic about management's repeated assertion that CCI will be able to return to growth after 2025, when the last of Sprint's lease cancellations take effect. Given the huge rise in mobile data usage and carriers' need to continue investing to facilitate that traffic, I believe management in their assertion that dividend growth will return to 7-8% annually in 2026 and beyond. In the meantime, CCI's BBB credit rating and modest debt maturities in 2023-2024 exude strength.

And yet, CCI's valuation has gone off a cliff:

At a price of $112.50, CCI trades at a price to AFFO of 14.9x, compared to its 5-year average of 23.0x.

Turning to the self-storage space, we believe one of the strongest names in this area is Extra Space Storage (EXR), which recently solidified its scale advantage by acquiring peer Life Storage. EXR now commands the #1 market share in U.S. self-storage at 13.2% of the market. Like ARE, EXR's ultra-strong pandemic-era performance is in the process of normalizing, especially as the housing market cools and fewer people are moving. EXR also enjoys a BBB credit rating and a manageable amount of debt maturing this year and next year.

And yet, the market is valuing EXR lower than it did prior to COVID-19.

At a price of $144.50, EXR trades at a price to AFFO of 17.0x, compared to its 5-year average of 22.3x.

Finally, in the industrial space, consider Rexford Industrial Realty (REXR), the premier owner of high-quality, infill industrial properties in the extremely supply-constrained Southern California market. Management calls the industrial supply shortage in Southern California "virtually incurable," and this shortage has spurred peer-leading rent and NOI growth. Over the last five years, REXR's NOI has grown at a CAGR of 39%, and after Q2 2023, in-place rents on its existing portfolio remained 50% below market, implying significant organic growth ahead.

REXR is truly firing on all cylinders while also enjoying one of the strongest balance sheets in REITdom with a BBB+ credit rating, and yet the market is pricing it significantly lower than it was before COVID-19.

At a price of $56.75, REXR trades at a price to AFFO of 26.0x, compared to its 5-year average of 39.5x.

Bottom Line

REIT fundamentals across almost all sectors remain strong, and the decrease in development activity today implies that a favorable supply environment will be in effect in a few years' time. And yet, the market is pricing many top-tier REITs as if growth is coming to an end and temporarily elevated interest rates will permanently eat into REITs' profits.

As for us at High Yield Landlord, we will follow the fundamentals, not investor sentiment.

For further details see:

There Might Not Be Another Chance Like This For Years