O - These 3 Dividend Aristocrats Have Reached A Buy-Zone

2023-11-20 13:00:00 ET

Summary

- Of the three, Realty Income is probably the best opportunity at the moment.

- Clorox Company is a solid dividend aristocrat with a history of increasing free cash flow and dividends, though management's use of cash during the pandemic is questionable.

- T. Rowe Price Group is a resilient company in the asset management industry, with a history of increasing dividends and potential for undervaluation.

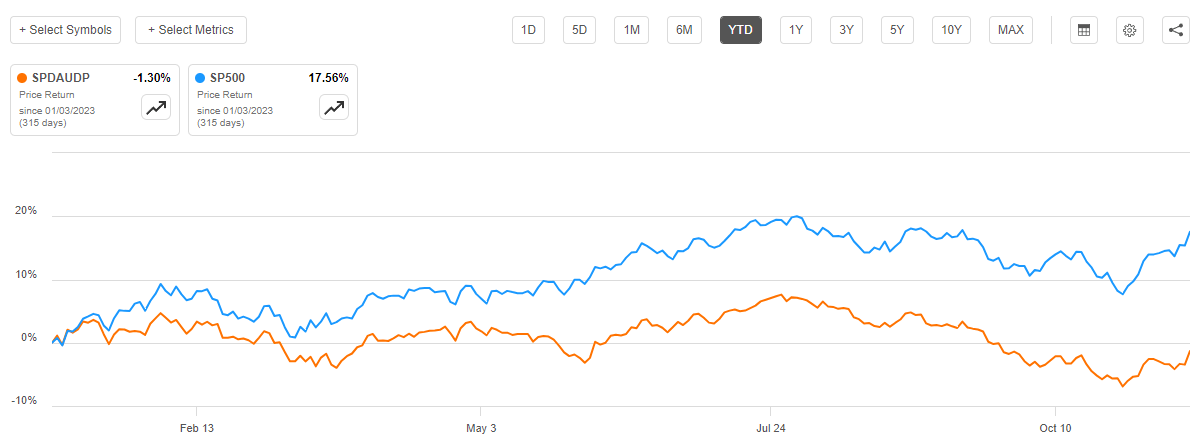

It has not been an easy year for dividend aristocrats, in fact the performance of the ProShares S&P 500 Dividend Aristocrats ETF ( NOBL ) has been significantly lower than that of the S&P500 ( SP500 ): -1.30% versus +17.56%, respectively.

{kind=link}

Seeking Alpha

The reasons for this divergence were, in my view, mainly two:

- The performance of the S&P500 has been driven by a few companies, but they have a significant weight within the index. Suffice it to say that the top 7 companies have a weight of 27% , so the return obtained is rather misleading. In fact, the YTD return of the S&P 500 Equal Weight Index was only +2.71%.

- The second reason has to do with the risk-free rate, which reached 5% and disincentivized the purchase of dividend companies. After all, coupons are certain while dividends are not, so for the same payoff I choose the less risky investment.

In any case, tech companies have already rallied a lot and the risk-free rate is gradually falling as a result of better-than-expected CPI data. So, it may be time to take advantage of the bargains in the market, I am talking specifically about dividend aristocrats that have lost a lot over the past year. In this article I will show you three of the companies that I consider most interesting at this time.

First company: The Clorox Company

The Clorox Company ( CLX ) is a company you probably all know since its products are used by millions of Americans every day. This company is a leader in the market for cleaning products, as well as disinfectant products. The operation also expands to other markets such as natural personal care products, water filtration systems, grilling products, and cat litter products. In short, Clorox is everywhere.

During the pandemic, this company found remarkable success since there was a surge in demand for disinfectants and cleaning products. In fact, 2020 and 2021 were great years for this company. However, once the Covid-19 alarm receded, the market gradually became disinterested in Clorox and the price per share began to plummet. After all, the golden years were behind us and there was more room to get worse than to get better. Regardless, Clorox remains a solid company, probably even more than in the past.

{kind=link}

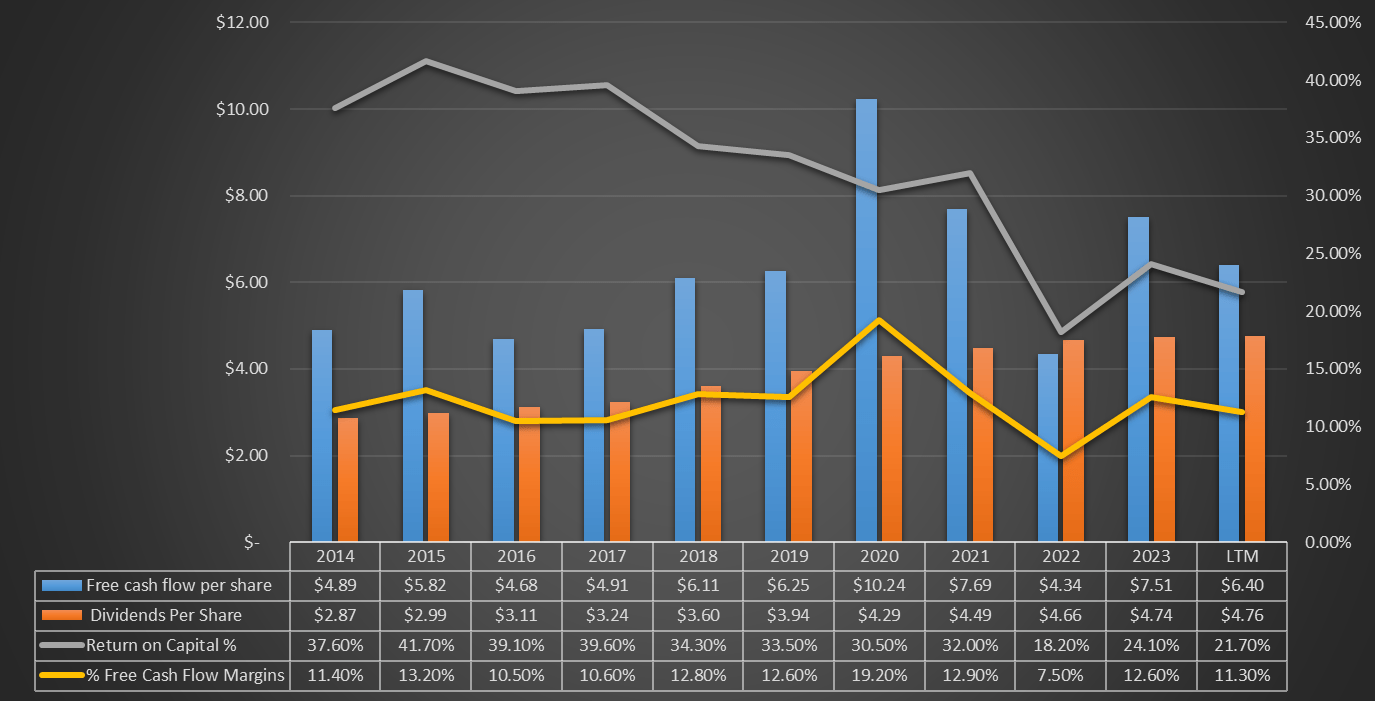

Chart based on Seeking Alpha data

As we can see from this graph, over the long run Clorox tends to increase its free cash flow per share as well as its dividend per share. When I invest in a dividend company this is the first thing I notice. Also, the return on capital tends to be above 20%.

Of course, the growth is not uniform, there have been better periods than others, but overall the trend is positive. Reaching the 2020 free cash per share again will probably take several years, but this is not a bad thing. Rather, I evaluate the pandemic as a period when Clorox made the most of an event of an extraordinary nature, so even though the company is less profitable today, it still benefited overall.

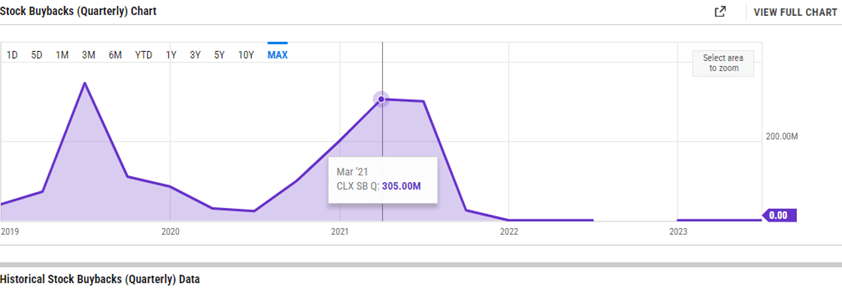

What I like less, however, is how management took advantage of the huge cash obtained during the pandemic: between September 2020 and September 2021, treasury shares worth $930 million were purchased.

{kind=link}

ycharts.com

Personally, I appreciate when a company does buybacks, as long as it is done when the price per share is below fair value. In this case the shares were bought back mainly around $200 per share, so the effectiveness of the buyback was minimal. If it had been done a few weeks ago, the timing would have been perfect.

In short, the pandemic revenues could have been better used, but that does not detract from the fact that this company remains a pillar for dividend investors.

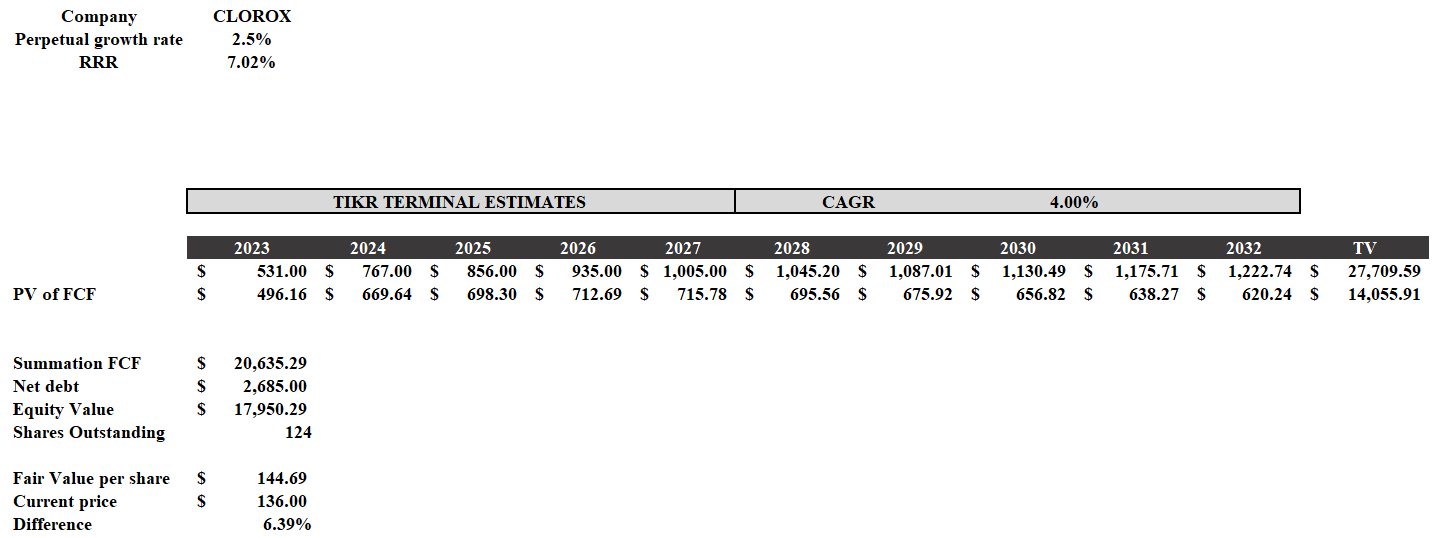

Currently, Clorox looks well priced based on my discounted cash flow. This model was constructed as follows:

- Expected free cash flow until 2027 is the analysts' estimate, from 2028 to 2032 I used a CAGR of 4%. Over the last 10 years the FCF CAGR has been 4.80%, so I am assuming slightly lower growth.

- The RRR was calculated using the CAPM formula. The latter takes into account a beta of 0.43, a risk-free rate of 4.44% and an equity risk premium of 6%.

{kind=link}

Discounted Cash Flow

Based on these assumptions, Clorox is slightly undervalued since its fair value is $144.69 per share.

{kind=link}

Seeking Alpha

Finally, the dividend yield is 3.48% and is widely sustainable as we have seen above. If we assume dividend growth over the next 10 years equal to that of the last 10 years, by buying Clorox now you would receive a dividend yield on cost of 6.13% in 2033. In my opinion, a decent yield for such a solid, low-risk company.

Second company: T. Rowe Price Group

The second company I want to discuss is T. Rowe Price ( TROW ), a company whose core business is to launch and manage equity and fixed-income mutual funds. Like all companies in this industry, earnings results are closely related to assets under management: the higher the latter, the higher the fees earned by T. Rowe Price.

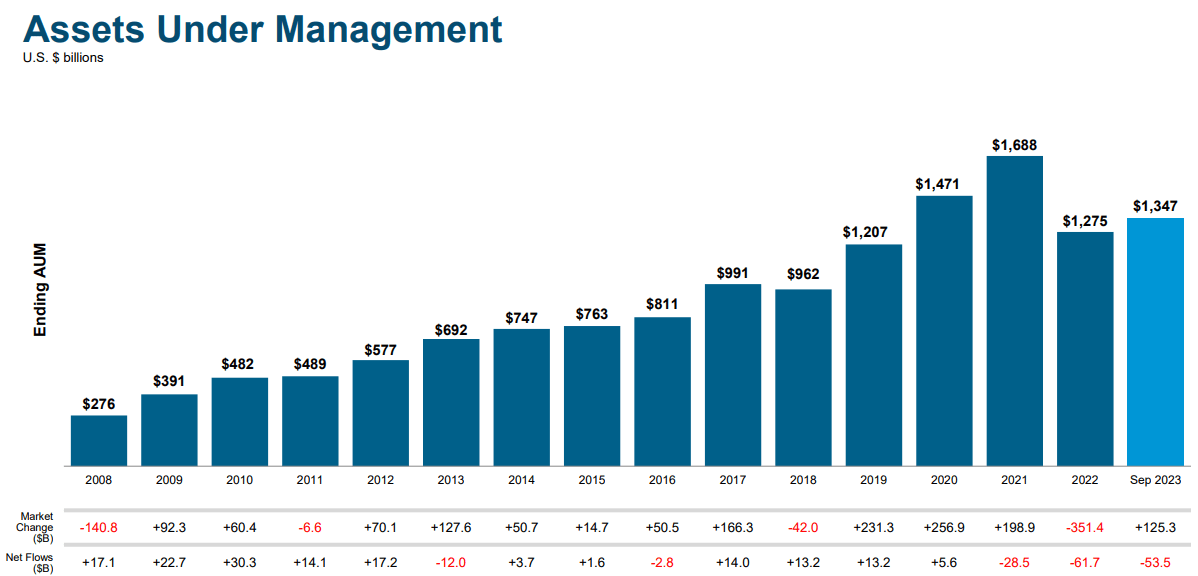

As in the case of Clorox, this company has also benefited from the pandemic, but as of today it is 55% off its all-time high. The continued fiscal stimulus in 2020 and 2021 has injected an immense amount of liquidity into the system, and some of it has poured into T. Rowe Price's AUM.

{kind=link}

T. Rowe Price Q3 2023

As we can see from this image , the growth achieved in the two-year period of the pandemic was abnormal when compared to previous years; the moment macroeconomic conditions deteriorated there was an immediate deterioration in AUM.

{kind=link}

Chart based on Seeking Alpha data

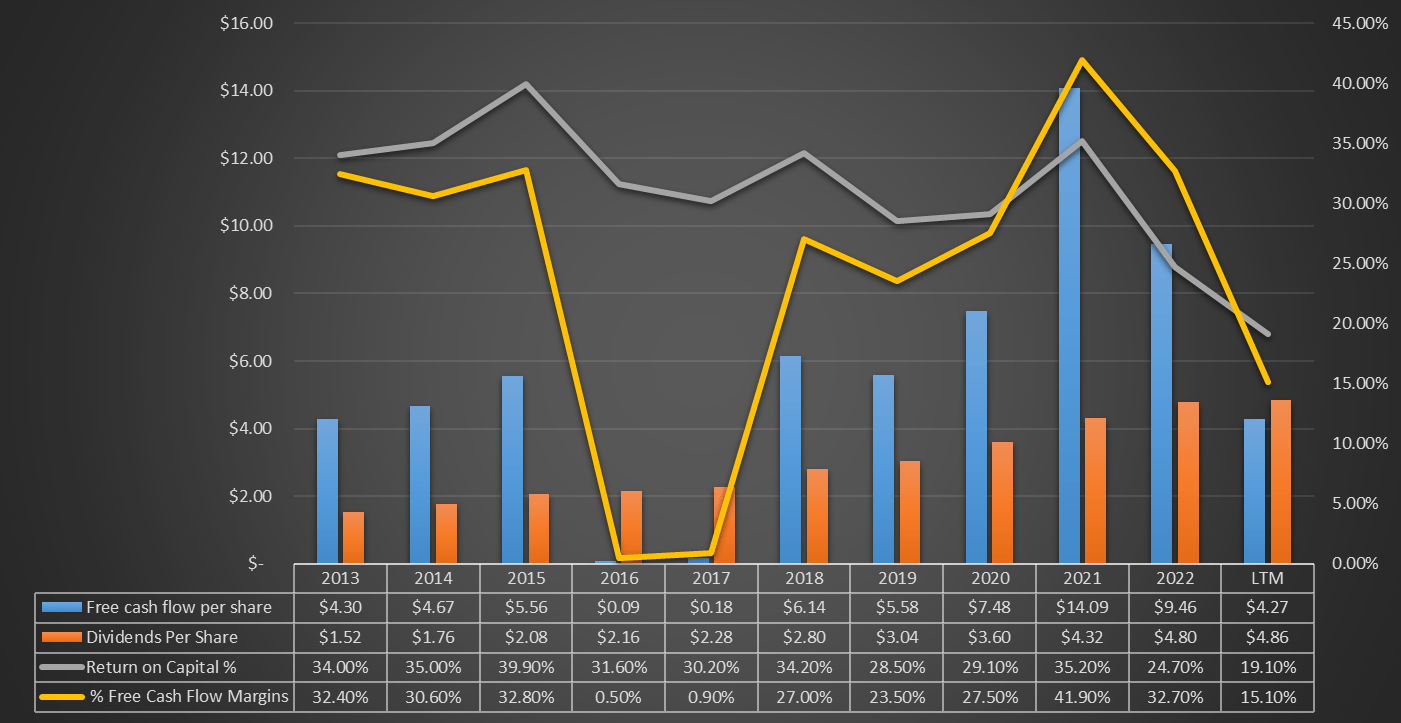

The last 12 months have not been easy and TROW has encountered some problems, but if we take a look at the long term we can see that this company has no growth problems. For completeness, the results for the two-year period 2016-2017 were affected by the change in trading of asset securities, but the profit for those years remains positive.

Excluding the last 12 months, both free cash flow per share and dividend per share found gradual growth; all with a rather high return on capital. In short, the latest results cannot overshadow what has been achieved over the past 10 years.

It is inevitable that there are negative moments; after all, AUM cannot grow all the time. During recessions it is logical to expect that investors' fear may lead them to withdraw their invested funds, and that is what happened in 2022 when everyone expected the worst after the rate hike. The same happened in 2008 and also other times in the past, but in the end T. Rowe Price always came out stronger than before. Let us remember that this company has almost 100 years of history; therefore, it is not new to operating during recessions. Also, I would like to point out that this company has negative net debt, -$2.68 billion. This means that the increased cost of debt will probably affect very little from an earnings perspective.

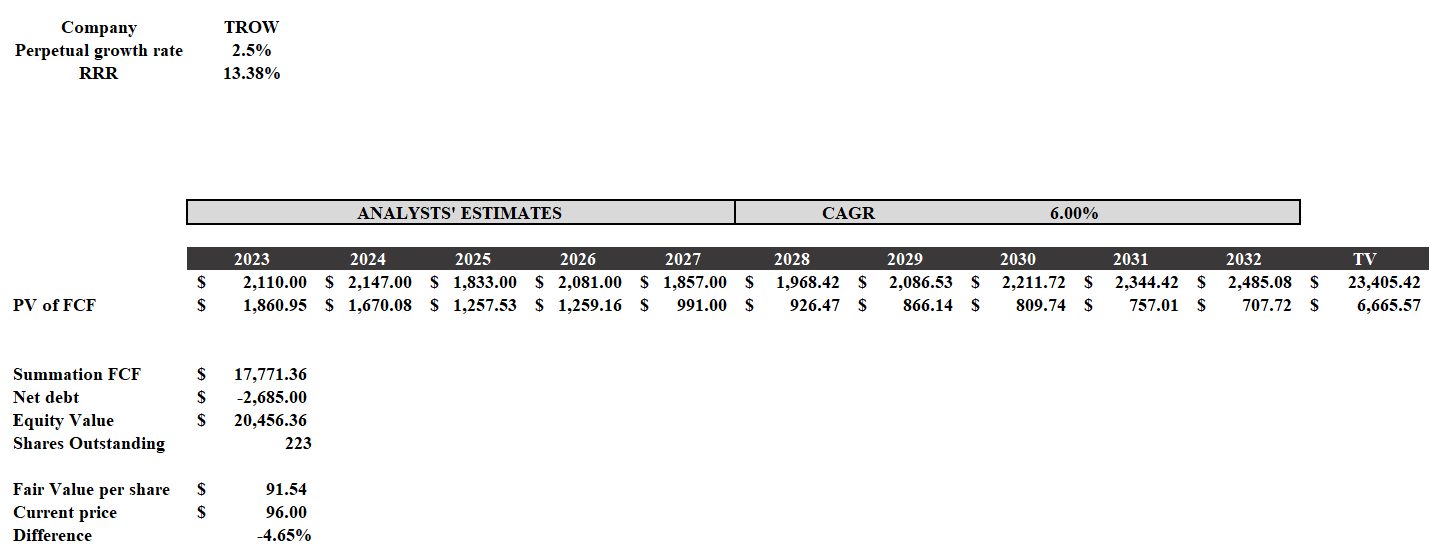

Also for T. Rowe Price I created a discounted cash flow model, and that model takes into account the following parameters:

- Free cash flow is what is estimated by analysts until 2027, from 2028 to 2032 I entered a CAGR of 6%. Consider that in the last decade the growth has been 6.50% per year.

- The RRR is equivalent to the CAPM. The latter was calculated using a beta of 1.49, a risk-free rate of 4.44% and an equity risk premium of 6%.

{kind=link}

Discounted Cash Flow

Based on these assumptions, T. Rowe Price is slightly overvalued since its fair value is $91.54 per share. In any case, I would like to point out that the discount rate calculated with the CAPM is very high, a whopping 13.38%, and this is because of the high beta. So, I consider a fair value of $91.54 per share a rather conservative valuation. Using a discount rate of 12% (still quite high), the fair value would amount to $103 per share, and in that case T. Rowe Price would be undervalued.

{kind=link}

Seeking Alpha

Finally, the dividend yield is currently 4.96% and is supported by increasing free cash flow over the long term. It has been 36 years in a row that the dividend has been increasing and the CAGR of the last 10 years has been very high, 12.63%. Projecting this rate even over the next 10 years, buying T. Rowe Price today, the dividend yield on cost would be 16.29% in 2032. This would be a great performance, and I personally would be satisfied even if it were a few percentage points lower.

Third company: Realty Income

The third company is a REIT, probably the most famous of all because of its dividends: Realty Income ( O ).

Over the past year there have been many REITs that have seen their price per share plummet, and this is because of rising interest rates. The real estate market is debt-based and operates with high leverage, which is why when interest rates rise this generates a growth freeze: buying a property at a 3% rate or at 8% makes a lot of difference.

In any case, while there are ultra-indebted companies that will suffer a lot from rising rates, there are also companies that have shown resilience even in difficult times, and the latter I think is the case with Realty Income. In other words, it is understandable that REITs have collapsed over the past year, but there has been excessive pessimism generated toward some of them.

{kind=link}

Realty Income Q3 2023

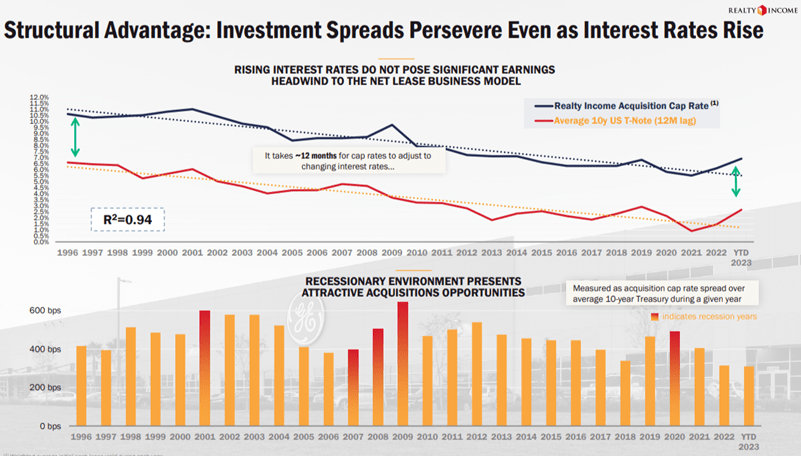

Realty Income is the seventh largest global REIT and has a credit rating of A3/A- : there are only seven other REITs with equal or better credit ratings. In addition, 91% of total rent is resilient to economic downturns and the company has been issuing increasing dividends for 29 years in a row. Since 1994, the dividend CAGR has been 4.30%, not very high, but at least steady and sustainable over time.

Anyway, beyond the long-discussed dividend, I would like to emphasize the resilience of this company even in difficult times.

{kind=link}

Realty Income Q3 2023

Investment spreads are high regardless of the business cycle, as the cap rate tends to adjust as the 10y U.S. T-Note yield changes. What's more, the times when the spread is highest is during recessions, where Realty Income takes advantage of attractive acquisition opportunities. Should 2024 be the year of the long-awaited recession, we can expect the investment spread to get better.

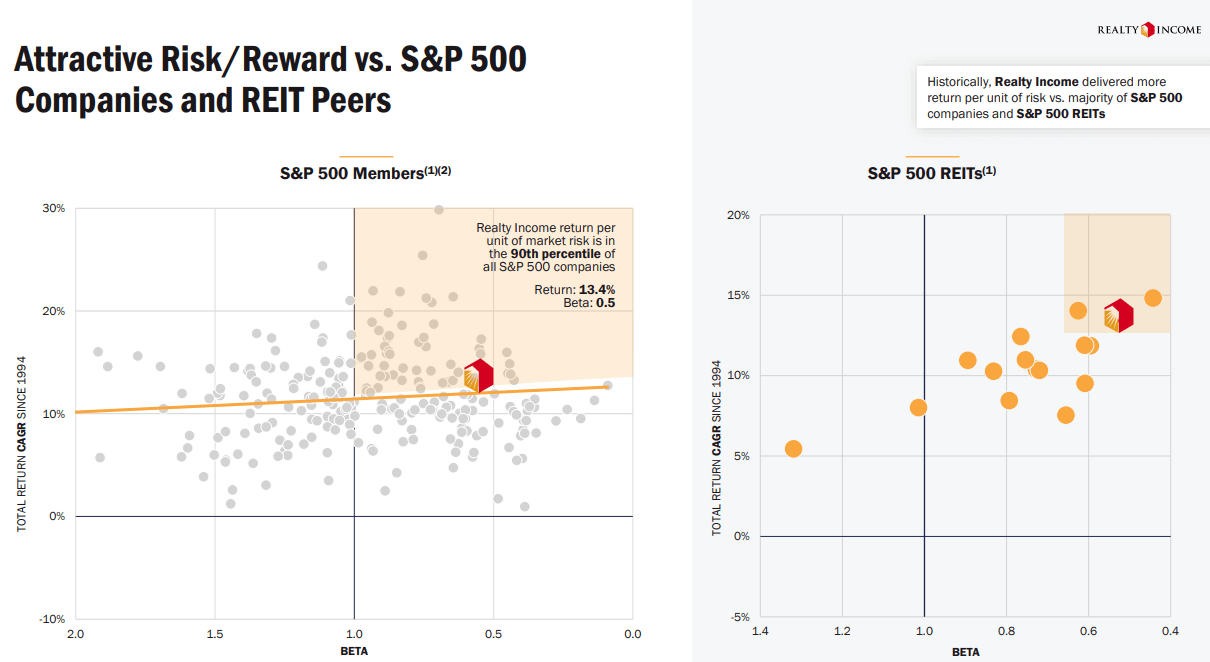

Now we come to another important aspect: volatility. Investing in this company means not only potentially getting a good return, but also not taking too much risk.

{kind=link}

Realty Income Q3 2023

As we can see in this image, Realty Income's risk/return ratio since 1994 is in the upper right quadrant; thus, where the return is highest but the beta is lowest. Based on this ratio, this company is in the 90th percentile among companies in the S&P500, with a return of 13.40% and a beta of only 0.50.

{kind=link}

Seeking Alpha

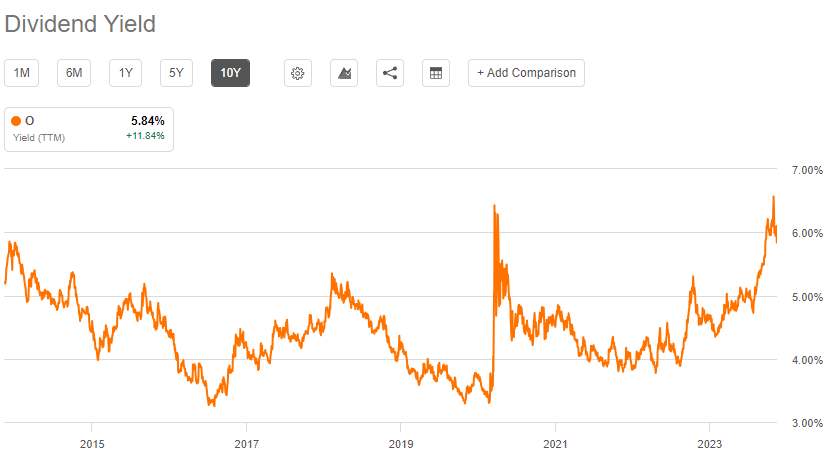

To conclude, the dividend yield is currently at 5.84%. This value is very high compared to the last 10 years, which is a sign of undervaluation. It is not common that it reaches figures around 6%, so when it does, one should take advantage of it.

{kind=link}

Seeking Alpha

Assuming that the dividend growth rate over the next 10 years is 4.03% as it has been over the past 10 years, buying Realty Income today will give you a dividend yield on cost of 8.76% in 2032. Potentially, I think this is a company to buy and forget about in your portfolio. You will surely remember it every month when you receive the dividend.

Conclusion

The negative performance of dividend companies has revealed a number of opportunities that the market did not previously offer. Dividend aristocrats are a certainty for dividend investors, and at the moment some of them are at a discount. In this article I have highlighted three of the companies that I consider most attractive at the current price, but there are others that deserve to be mentioned.

Regarding Clorox, T. Rowe Price, and Realty Income I think the latter is the most interesting but watch out for the first two. They have been very volatile in recent months and I would not rule out further major declines in the future. It will be important to take advantage of these opportunities if they arise.

For further details see:

These 3 Dividend Aristocrats Have Reached A Buy-Zone