PAXS - These 8%+ Yielding Income Pockets Remain Attractive Post-Rally

Summary

- The income market has rallied strongly over the past couple of months.

- We highlight securities that have lagged the rally and offer an opportunity in the current environment.

- Many of these securities can also remain resilient in case markets hit a bump in the road this year.

This article was first released to Systematic Income subscribers and free trials on Feb. 6.

The income market has enjoyed a torrid rally over the last month or so, with many sectors up by double-digit figures. In this article, we take a look at remaining pockets of opportunity and highlight securities that have lagged the rally.

Before we get on with the ideas, it's important to keep a couple of things in mind. First, a security that has lagged the broader rally may have been expensive to begin with. This means that the lag is just a kind of "catch-up" of its previously expensive valuation. Therefore, it's important to make sure that we focus on securities that look attractive on a standalone basis as well.

Second, securities that are lagging the market rally are likely doing so for structural reasons. For instance, floating-rate securities have not rallied as much as longer-duration assets for the simple reason that they don't benefit as much from the fall in yields. This doesn't make these securities unattractive, but investors should at least be aware of any structural features that explain recent moves.

Finally, securities lagging the broader market rally are also often lower-beta options either because of their higher-quality or shorter-maturity profile. The advantage of these securities is they can also be resilient on the way down if the markets hit another bump.

Let's have a look where the current rally stands.

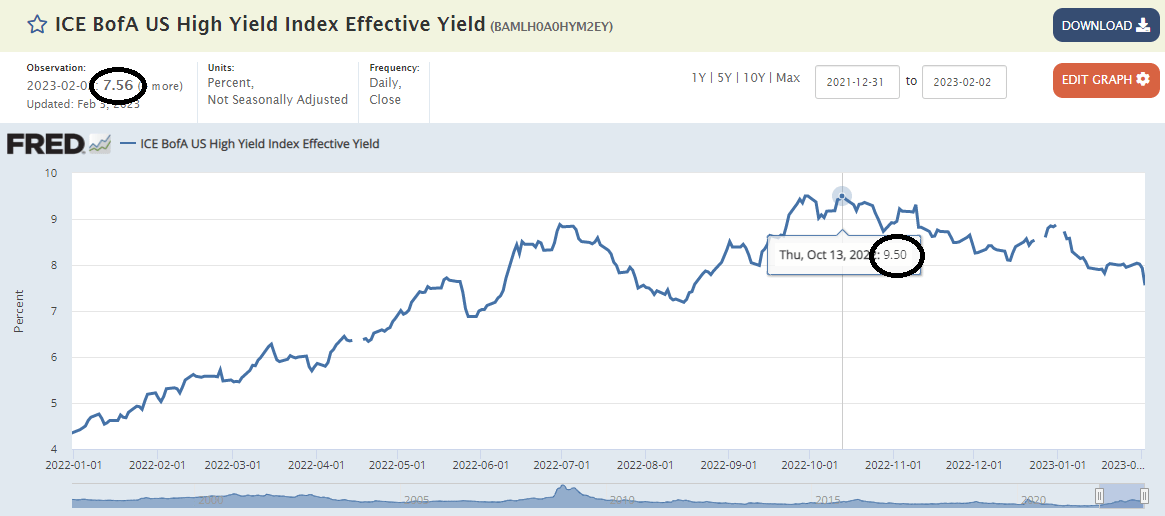

Our favorite proxy of overall income yields is the high-yield corporate bond sector which includes both Treasury yields and corporate credit spreads. By this measure, yields have fallen 1.94%, after rising 5.15% at the peak. In other words, 40% of the 2022 peak sell-off has now been reversed.

{kind=link}

If we look at the closed-end fund ("CEF") total return index below starting from 2022, we see that half the peak 2022 drawdown has been recovered.

Systematic Income

What's interesting about this recovery from the 2022 market bottom is that it has been as fast as the drop, which is relatively unusual for markets which tend to follow the dictum of "down the elevator, up the escalator." Such a fast rally has likely left some investors looking for opportunities where decent value remains, some of which we highlight below.

Some Ideas

Zions Bancorporation Series G ( ZIONO ) is rated BB+ and is set to move to a floating-rate coupon of 3-Month Libor + 4.24% next month, unless redeemed, which equates to a yield around 9%. There is some risk that the stock is redeemed. However, it's not trading much above its liquidation preference, so the negative impact should be minimal unless investors overpay.

As of this writing, the stock is trading at a stripped price of around $25.16 - an entry below a stripped price of $25.10 ensures less call price risk (i.e. a minimal loss in case of redemption). The stock accrues the dividend at its current 6.3% rate until 15-Mar from its previous dividend payment date of 15-Dec. ZIONO has not rallied as much as the rest of the preferreds space as its price is "pinned-to-par". This is because a sharp rise in price would create substantial call price risk in case of a redemption so investors are not willing to pay up for it, leaving its yield more attractive than it would be otherwise. The redemption possibility, in-effect, makes it a lower beta security.

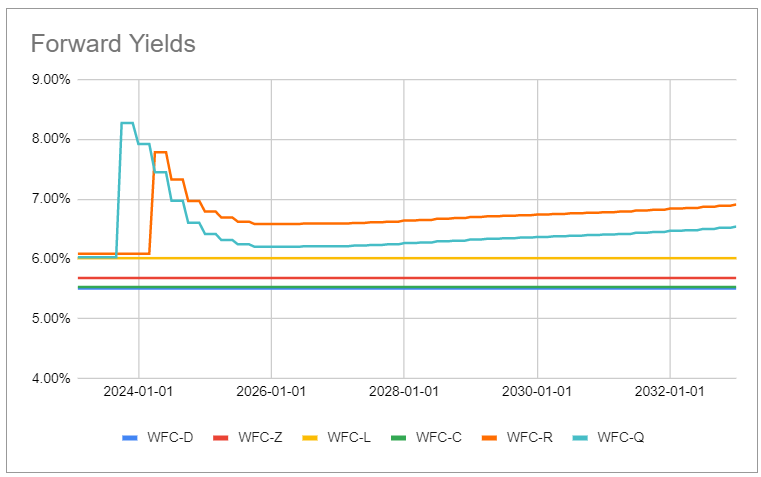

Another bank preferred worth highlighting is the Wells Fargo Series Q ( WFC.PQ ) which is also due to reset to a floating-rate coupon of 3-Month Libor + 3.09% in September. The stock is trading below $25, so a redemption would be a windfall. Once the stock resets to a floating-rate coupon, its yield (cyan line below) will significantly exceed that of the other preferreds, as the chart below shows.

{kind=link}

Mortgage REIT Arlington Asset 2025 bonds ( AIC ) are trading at a 8.95% yield. The bonds have about 2 years left till maturity. Due to its short duration, AIC is up only 1% this year. Over the past year, the bonds are up 2%, so they are very much a lower-beta, though not a lower-yield alternative.

Turning to CEFs, we would highlight the Nuveen Corporate Income 2023 Target Term Fund ( JHAA ). The fund holds short-dated high-yield corporate bonds. It has a low distribution rate of just 3.3%, however, there are additional less obvious sources of yield. First, its high distribution coverage equates to a "covered" yield of 3.6%, plus we have about 2% of pull-to-par (given weighted-average bond price is 98%) plus 3.5% of additional tailwind through discount amortization till the expected termination date at the end of this year. All of this equates to a true yield of around 9.1% and higher on an annualized basis. This fund is a great low-beta option as it maintains both a low-beta NAV via its short-dated bonds as well as a low-beta price through the control of its discount via its term structure.

For investors who like to maintain a higher-beta profile, we see value in PIMCO Access Income Fund ( PAXS ). We recently rotated into the fund from another PIMCO taxable CEF, as PAXS has lagged the rally somewhat. It is likely PAXS suffers from a lack of name recognition, being the most recently launched PIMCO CEF. It's currently trading at a near-record 20% wider discount than the average PIMCO taxable CEF. PAXS has an 11.5% yield.

Systematic Income

Finally, we highlight the Angel Oak Financial Strategies Income Term Trust ( FINS ), which has lagged the rally due to its predominantly floating-rate, higher-quality allocation. The net income profile of the fund has been improving sharply over the last few months, not only because of its floating-rate allocation but also because it has a mostly fixed-rate leverage cost.

Takeaways

Although securities that have lagged the sharp rally this year may sound unimpressive, they have two advantages. One is that their yields are higher than they would be otherwise had they rallied as much as the rest of the market. And two, many of these securities have lower-beta profiles, which means they can outperform in case prices turn lower over the rest of the year.

For further details see:

These 8%+ Yielding Income Pockets Remain Attractive Post-Rally