ARDC - These High-Yielding CLO Securities Are Finally Worth Holding

Summary

- The CLO asset class is worth a look by income investors due to its strong historic profile, high yields and rising income levels.

- The asset class offers a wide variety of securities across the entire risk spectrum, with yields from mid-single-digit to double-digit levels.

- We take a look at some of the key dynamics of both CLO Equity and CLO Debt securities and highlight attractive funds.

This article was first released to Systematic Income subscribers and free trials on Oct. 17.

The recent spike in volatility across markets has pushed many income assets into very attractive territory. In this article, we highlight CLO securities for investors looking for both higher-risk/higher-yielding assets as well as those looking for more defensive assets. The sector has been historically resilient, even for its higher-risk part securities. The current market environment of high short-term rates and high volatility is also providing tailwinds to sector performance.

State of Play

The CLO space has recently become historically attractive. To illustrate this we can point to a number of different indicators.

First, CLO yields have not only moved significantly higher but have also moved above their levels during the COVID crash in some cases. This is due to the combination of high short-term rates (CLO Debt securities are typically anchored off Libor) but also relatively wide credit spreads.

{kind=link}

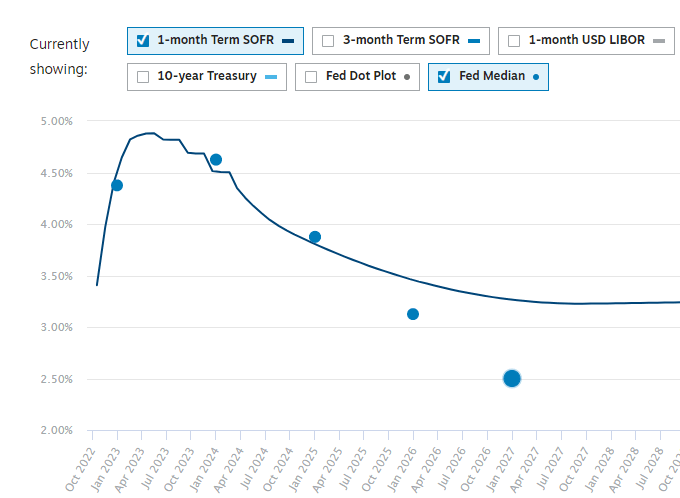

The current interest rate regime is particularly beneficial for the CLO sector. First, it takes advantage of rising short-term rates (both individual loans and CLO Debt security coupons are a function of short-term rates). Second, the inverted yield curve means CLO securities are now anchored off the part of the yield curve that is currently among the highest points on the curve and will very likely be the highest point in the curve once the Fed policy rate approaches its peak. And third, it is very unlikely that short-term rates will fully reverse their rise any time soon, allowing CLO income levels to remain elevated. The Fed has been very clear that they expect to keep rates higher for longer to rein in what looks to be very sticky inflation. The chart below shows that both the Fed and market expect short-term rates to remain above current levels for at least two years.

{kind=link}

The second reason why the CLO space has now become attractive is that, according to the WSJ, last week there was some technical pressure on the asset class via forced selling by a number of institutional investors, including UK pension funds on the back of recent UK government bond volatility. This has apparently pushed some CLO Equity securities below their liquidation value or NAV which adds a decent margin of safety to the asset. Many UK pension funds were forced to sell anything that was not nailed down and that included CLOs.

And third, valuations of some CLO CEFs have moved off their absurd levels towards something more reasonable.

Systematic Income

CEFs with partial allocations to CLOs such as ARDC and XFLT are also trading at attractive valuations and at discount percentiles of 16% and 17%. This metric shows the amount of time these funds have spent trading at wider than current discounts over the last 5 years.

Systematic Income

Thinking About Risk/Reward

There are a number of appealing aspects to the CLO space. Because CLO Equity and CLO Debt have such different risk/reward profiles it makes sense to look at them separately. Good primers on the overall CLO structure are here and here .

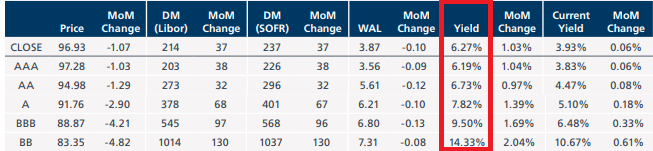

Let's look at CLO Debt first. In CLO Debt, yields are high both in absolute terms (nearly double-digit yields for investment-grade rated CLOs) and relative to their quality.

{kind=link}

For instance, while A-rated corporate bonds feature a yield of around 5.6%, A-rated CLOs feature a yield of around 7.8%. Investors who are skeptical of CLO credit ratings should know that CLOs have had a significantly lower default rate than similarly-rated corporate bonds.

For example, over the last decade out of all CLOs originally rated investment-grade zero have defaulted. Out of all rated CLOs (about 11,400), only five have defaulted as of early 2022 - those were originally rated BB and B. If we look further back from 1990 to 2009 out of the so-called CLO 1.0 tranches only 15 investment-grade CLOs have defaulted out of 800 transactions rated by the S&P. A quick comment on CLO vintage - CLO 2.0 and 3.0 are improved structures from a risk perspective and are the only vintages available now. The combination of higher yields and a stronger default profile versus corporate bonds makes for an attractive combination.

Part of the reason for their higher yield versus investment-grade corporate bonds has to do with the short call option embedded in CLO Debt (most investment-grade bonds are non-callable, unlike High Yield bonds). This call option allows the CLO manager to refinance CLO Debt after the non-call period at a lower cost. This typically happens when the macro environment is very strong and credit spreads are tight. It is akin to the embedded call option that is carried by many high-yield corporate bonds and which adds a yield premium over and above the yield linked to the credit risk of the issuer. One downside to CLO Debt holders is that their security can mature earlier than expected in an environment when credit spreads tighten. This can be annoying but recall that investors were originally compensated for this eventuality via a higher level of yield. It is also a scenario which few people are worried about right now. In fact, a sharp tightening in credit spreads would be very welcome given CLO Debt securities are trading below par these days as it would result in significant capital gains from current levels.

Two more general comments are worth making. First, CLOs are highly diversified with each structure holding hundreds of loans in its portfolio and each fund holding 25+ different CLOs. Clearly, there will be some overlap but the overall level of diversification will still be very high. For example, the CLO CEF EIC has exposure to 1,460 obligors - this is well above what you would find in a typical credit fund.

Two, CLO portfolios are of higher quality than the broader leveraged loan market. This has to do with the credit quality test which limits the amount of CCC securities in the portfolio. If this level is breached the assets are penalized which initiates a self-curing process that protects CLO Debt in the structure.

Turning to CLO Equity, default statistics are hard to come by. That said, we can provide some intuition by looking at how CLO 1.0 vintage structures performed over the GFC which is shown in the chart below from analysis done by Citi. Overall, the performance was quite strong for what is the highest-risk part of the CLO sector over what was a very difficult period for corporate credit.

Citi

Analysis by Wells Fargo which breaks down CLO Equity by year vintage shows a similarly strong result even for those issued right before the GFC.

Wells Fargo

Two reasons why CLO Equity returns can be strong in a difficult market environment have to do with the optionality in the CLO Equity structure. Recall that CLO Equity is an active strategy pursued by the managers of the CLO rather than a static portfolio. Specifically, when credit spreads rise and loan prices fall the manager can take the loan repayments from the portfolio and reinvest them into below-par priced loans. If these loans pay off at par the difference goes straight to the CLO Equity bottom line. Loans have been trading below par this year as the following chart shows and this has been generating value for CLO Equity.

TCW

The second way CLO Equity can take advantage of volatility is via the refinancing call option by refinancing the CLO Debt in the structure to lower-cost debt with the same maturity. A reset can also extend the maturity of the debt as well as the reinvestment period. A lower cost of debt goes straight to the bottom line of CLO Equity. In short, in a period of elevated volatility CLO Equity can take advantage of both rising credit spreads (via the reinvestment option) as well as tightening credit spreads (via the call option or reset).

Investment Options

Investors who are tempted by the CLO space have a number of securities to choose from. The basic decision investors need to make is where on the risk/yield spectrum they want to allocate. Specifically, the key decision is how much allocation to hold in higher-risk/higher-yielding CLO Equity securities, if any.

Investors with a fully risk-on stance and who want to maximize their yield should have a look at the Eagle Point Credit Company ( ECC ) which is trading at a 16.12% yield. The fund is one of a trio with allocations primarily to CLO Equity. We prefer ECC to OXLC due to a longer average CLO reinvestment period.

A lot of investors get into a lather arguing about whether or not the double-digit yield of CLO Equity funds is "real" and/or whether it's fully covered or not. In our view, this is less important than it seems for the simple reason that CLO Equity is as much an investment strategy as it is a standard portfolio of securities. In a favorable market environment, i.e., when loans are trading well below par and default rates are low like the one we are living through now, CLO Equity securities can generate significant returns over and above their underlying income potential.

As of this writing ECC is trading at an estimated premium of 2.8% (1.9% versus the September official NAV) which is not cheap but is historically reasonable as the following chart shows.

Systematic Income

Investors looking for a lower-octane CLO allocation may want to consider a fund with a partial allocation to CLO Equity. Two funds in this bucket are the Eagle Point Income Company ( EIC ) and the XAI Octagon Floating Rate & Alternative Income Term Trust Fund ( XFLT ). XFLT is a much more attractive option in our view given its much more reasonable 4.1% discount versus an 18% estimated premium for EIC. XFLT trades at a 14.5% current yield. The fund is allocated to 36% in CLO Equity, 13% in CLO Debt and the rest primarily in first-lien loans.

Moving lower down the risk spectrum we have funds with a relatively low CLO Equity allocation such as the Ares Dynamic Credit Allocation Fund ( ARDC ) which has a 10% exposure to CLO Equity and 23% to CLO Debt. ARDC trades at a 10.9% current yield and a 14.8% discount. We hold ARDC in our High Income Portfolio.

Investors who are not comfortable with explicit leverage (all the CEFs above are fairly highly leveraged) or the exposure to CEF discount volatility may want to consider either CLO CEF bonds or CLO ETFs which offer a higher-quality way to allocate to CLOs.

In the CLO CEF bond space, we like the OXLC 6.75% 2031 bonds ( OXLCL ) which are trading at an 8.5% yield-to-maturity. OXLC bonds feature a high level of asset coverage. CLO CEF bonds and preferreds also get explicit support from fund managers in periods of sharp drawdowns through buybacks which are required in order to keep leverage from rising above the level at which it would be necessary to suspend distributions on CEF common shares, something the funds like to avoid.

There are also three relatively high-quality ETFs all of which allocate primarily to investment-grade CLO Debt securities. In this high-quality space, we like the Janus Henderson B-BBB CLO ETF ( JBBB ). The fund's current yield (based on the last distribution) is 6.72%, which actually understates its income profile in two ways. First, because short-term rates which drive CLO Debt income have continued to rise and will only peak once the Fed pauses. And second, CLO Debt securities are trading below par which means that the current yield metric ignores the additional yield tailwind of pull-to-par. If the Fed pauses its interest rate hikes where the market expects, the yield of the fund will likely rise closer to a double-digit level which is very attractive for a primarily investment-grade portfolio. We hold JBBB in our Defensive Income Portfolio.

Janus Henderson

Takeaways

The CLO asset class has finally become very attractive across both CLO Equity and CLO Debt securities. Apart from having a resilient track record, CLO Equity is attractive as it takes advantage of the current high volatility environment via its two options - the reinvestment and refinancing options which can deliver additional value over and above its already high-yielding profile. And CLO Debt securities are attractive given the sharp rise in short-term rates which will allow investment-grade securities to soon rise to a double-digit yield level. The attraction of the CLO space is that, unlike many other assets, it provides options across the quality and yield spectrum, allowing many different investors to both take advantage of high yields on offer and diversify their portfolios.

For further details see:

These High-Yielding CLO Securities Are Finally Worth Holding