ESRCF - Third Avenue International Real Estate Value Fund Q2 2023 Portfolio Manager Commentary

2023-07-20 10:30:00 ET

Summary

- Third Avenue Management is a New York City-based asset manager founded in 1986 that utilizes a disciplined, value-oriented, and asset-based approach to investing in publicly traded securities.

- The Third Avenue International Real Estate Value Fund reported a return of +2.79% for Q2 2023, outperforming the FTSE/EPRA NAREIT Global ex US Index which declined by -2.70%.

- The Fund's outperformance was driven by targeted investments in Europe, a large investment in industrial owner and developer 'Vesta', and investments in small/mid-cap Japanese real estate operating companies.

- The Fund increased its exposure to Mexican industrial real estate and initiated an investment in Canadian self-storage real estate owner and operator StorageVault.

Dear Fellow Shareholders:

Performance

We are pleased to provide you with the Third Avenue International Real Estate Value Fund’s (the “Fund”) report for the quarter ended June 30, 2023. During the quarter, the Fund generated a return of +2.79% (after fees) compared to the most relevant benchmark, the FTSE/EPRA NAREIT Global ex US Index (the “Index”), which declined –2.70% for the same period.

Performance and Excess Return

As of June 30, 2023

| Annualized |

| 3 mo |

| YTD |

| 1 yr |

| 3 yr |

| 5 yr |

| Inception* |

| Third Ave Int’l Real Estate Value Fund ( REIFX ) |

| 2.79% |

| 5.94% |

| 3.07% |

| 8.42% |

| 3.96% |

| 4.85% |

| FTSE EPRA/NAREIT Global ex US Index 1 |

| -2.70% |

| -4.32% |

| -8.51% |

| -3.29% |

| -3.78% |

| 0.71% |

| Third Ave Int’l Real Estate Value Fund Excess Return 2 |

| 5.49% |

| 10.26% |

| 11.58% |

| 11.71% |

| 7.74% |

| 4.14% |

| *Inception Date 3/19/2014. Source: TAM, Company Reports, Bloomberg. |

For the first half of 2023, the Fund generated a +5.94% return compared to the Index which declined by -4.32%. The outperformance of the Fund so far this year has resulted from three key areas, including the Fund’s: (i) targeted investments in Europe generated a 23% average return while the European component of the index declined 5%; ((ii)) large investment position in ‘nearshoring’exposed industrial owner and developer ‘Vesta’ which generated a 38% return; and ((iii)) two investments in small/mid-cap Japanese real estate operating companies that generated a 15% return while the Japanese component of the index declined -4%. These positive performance contributors were partially offset by weakness in the Fund’s Asian (ex-Japan) investments. Sentiment in Asia has been negatively impacted by geopolitical concerns, and a slower than expected post-COVID economic recovery. The Fund’s targeted investments in Asia have extremely attractive valuations, considering the high quality of the real estate they own, and could provide the Fund with good upside when sentiment eventually turns positive.

Activity

In May 2023, the investment and philanthropic community lost Samuel Zell (“Sam” or “Zell”), regarded as perhaps the premier U.S. real estate investor of the past 50 years. Sam was heavily involved in the formation of the modern-day public Real Estate Investment Trust (“REIT”) market, and a champion for corporate governance in public companies. Sam’s vibrant personality and thought-provoking insights will be sorely missed and his visionary views on international real estate investing will have a lasting impact on the Fund’s investment process, particularly as it relates to Latin America.

As outlined in Sam’s book Am I Being Too Subtle? (2017), as the child of immigrants, Sam was well known to have an international orientation. In the late 1990’s Sam expanded the highly successful U.S. business, creating ‘Equity International’, which sought to invest capital in international real estate companies alongside well-connected local partners. As noted in the book, Equity International’s primary premise in international investing was to benefit from the transformation of businesses into institutional platforms.

Sam was an early proponent of the ‘nearshoring’ trend whereby supply chains based in Asia should move closer to the consumption base after seeing the impact on Japan’s nuclear disaster back in 2011 (Fukushima), and witnessing multinational executives bemoaning the cost of supply chain delays out of Asia. Sam subsequently invested in a Mexican warehouse and logistics company, well before the nearshoring buzz became what it is today following the COVID and geopolitical led supply chain disruptions.

Regular readers of this letter will be familiar with our similar views on nearshoring of manufacturing all the way back to our initial investment in Mexican industrial owner and developer Vesta in 2015. Vesta is an example of a business that has grown into an ‘institutional platform’. A further step in Vesta’s institutionalization was evident during the quarter, as Vesta sought to raise equity through a U.S. initial public offering ((IPO)) of depositary receipts. The equity raise, totaling US$445mn, and about 20% of Vesta’s market cap, was well received given Vesta is a key beneficiary of the ‘nearshoring’ tailwinds which is positively impacting company fundamentals. Vesta will use the proceeds to accelerate its US$1.1bn development pipeline which should be a meaningful driver of earnings and value creation for the company over the next 3 years. Vesta remains a top holding in the Fund.

In addition, the Fund’s exposure to Mexican industrial real estate was increased further during the quarter through an initial investment in FIBRA Macquarie. Structured as a REIT, FIBRA Macquarie owns a portfolio of 238 industrial and logistics assets in Mexico. About 70% of the assets are located in northern Mexico where industrial real estate fundamentals are benefiting from an acceleration in the ‘nearshoring’ trend in North America. As evident from Tesla’s announcement of a new factory in northern Mexico (Monterrey) that could see a total US$10bn investment and likely spawn significant boost to logistics and industrial demand from suppliers and logistics companies. FIBRA Macquarie collects 78% of its rent in U.S. Dollars from multinational firms with a high credit quality portfolio.

Fund Management normally avoids externally managed REITs, given they can suffer from poor governance including lack of alignment, and have incentives skewed to asset growth rather than share price performance. In addition, many externally advised REITs suffer from a lack of value creation opportunities, given re-development exposure is limited, and high dividend payout ratios limit liquidity. This is not the case with FIBRA Macquarie where the manager (Macquarie) is compensated through a simple fee based on equity market cap, together with a performance fee linked to share price performance. Indeed, FIBRA Macquarie has a good track record of value creation from developing new logistics assets, and currently has about 6% of assets invested in development projects. Another positive capital allocation decision by management is executing share buy backs when shares trade at deep discounts. Despite having strong underlying real estate fundamentals, including high occupancy and rental growth, FIBRA Macquarie trades at an attractive price, with a 10% real estate yield (cap rate implied from current share price), an 11x earnings (Adjusted Funds from Operations 3 ) multiple, and a 7% dividend yield.

During the quarter, Fund Management took advantage of share price weakness across Asian markets to increase position size in three deeply discounted existing investments: ESR Group ( ESRCF ), Capitaland and Shangri-La Asia ( SHALF ). All three have attractive growth outlooks, well capitalized balance sheets, and proven management teams. Additionally, all three have substantial exposure to logistics, or lodging real estate, where near-term fundamentals are advantageous.

Some investors will argue against Fund Management’s view on value in Asia, suggesting that discounts are persistent, and rarely closed through positive events such as resource conversion activity. This is a common view, and is one of the key reasons for persistent discounts enduring in Asian public property companies. Fund Management argues that resource conversion activity has seen a notable uptick that has directly benefited shareholders, as shown in the numerous transactions highlighted in the table below. Deep discounts in Asian real estate companies will likely prove unfounded once sentiment turns more positive, in Fund Management’s opinion.

In the meantime, it was very positive to see the Fund’s investment in Swire Pacific ( SWRAY, “Swire”), a Hong Kong/China diversified company, announce a meaningful transaction. On our estimates, about 80% of Swire Pacific’s value is in its high-quality retail and office portfolio located in Hong Kong and China. The other 20% of the company includes segments such as the beverages division. Swire Pacific has made many accretive capital allocation decisions over the past few years, including selling non-core office assets at the most recent peak of the Hong Kong office market, divesting its legacy marine services business, and buying back shares at deep discounts (75% discount to book value 5 ). During the quarter, Swire announced the significant sale of the U.S. operations of its beverages business for US$3.9bn, at 4x book value and representing almost 40% of Swire’s equity market cap. Assuming the transaction is approved by shareholders, a 17% special dividend will be paid to B class shareholders representing half of the gains. When combined with a regular dividend of over 6%, shareholders will receive a 25% dividend over the next year. Importantly, given the transaction was at a 22x earnings multiple, there is limited earnings dilution. Needless to say, Fund Management will be very pleased to receive such dividends and retain an investment in a more focused and increasingly simplified real estate entity that owns, operates, and develops some of the best real estate in Asia. The Swire transaction was not the only significant Asian resource conversion in the quarter, with New World Development Company Limited (not owned by the Fund) also announcing the sale of noncore infrastructure assets as shown in the below Asian resource conversions table.

Resource Conversions in Asian Property Companies

As of June 30, 2023

| Company |

| Corporate Action |

| Annoucement Date |

| US Market Cap |

| Premium 6 |

| Swire Pacific Beverages* |

| Privatization |

| Jun ‘23 |

| 3.9 |

| N/A |

| NWS Holdings* |

| Privatization |

| Jun ‘23 |

| 4.5 |

| 15% |

| Swire Pacific* |

| Share buy back |

| Aug ‘22 |

| 0.5 |

| N/A |

| China Logistics |

| Public to public |

| Sept 21 |

| 2.5 |

| 17% |

| Daiburu |

| Public to public |

| Nov ’21 |

| 1.1 |

| 44% |

| Capitaland* |

| Restructuring |

| Nov ‘21 |

| 2.8 |

| N/A |

| Hongkongland |

| Share buy back |

| Sept’21 |

| 1.0 |

| N/A |

| Invesco Office |

| Privatization |

| Jun ‘21 |

| 2.0 |

| 19% |

| Tokyo Dome |

| Public to public |

| Jan ‘21 |

| 2.5 |

| 45% |

| Kenedix |

| Privatization |

| Nov’ 20 |

| 1.3 |

| 15% |

| Wheelock* |

| Privatization |

| Jun ‘20 |

| 5.8 |

| 51% |

| Unizo Holdings |

| Privatization |

| Jun ‘20 |

| 5.1 |

| 23% |

| NTT Urban |

| Public to public |

| Oct ‘18 |

| 1.6 |

| 32% |

| Wharf REIC* |

| Spin out |

| Nov ‘17 |

| 26.6 |

| N/A |

| GLP* |

| Privatization |

| Jul ‘17 |

| 16.0 |

| 89% |

| New World China |

| Public to public |

| Apr ‘16 |

| 2.7 |

| 33% |

| Source: TAM, Bloomberg, Capital IQ *REIFX Holdings. |

It's hard to ignore the deep value in Asian real estate in the context of potential ‘resource conversions’ as highlighted above. Along these lines, it was interesting to see in the quarter, the sale of a luxury hotel property that highlights some of the significant disconnects between public-and-private market value. The Mandarin Oriental in Barcelona, which is managed but not owned by Mandarin Oriental ( MAORF ), sold to a Saudi investment group for a reported US$2 million per room. The Fund made a special situation investment in Mandarin Oriental back in Q3 2022, as discussed in the Q3 2022 Shareholder Letter . At the current share price, on our estimates, Mandarin Oriental trades at about US$200 thousand per room. While each of Mandarin’s hotels would probably not sell for US$2 million per room, properties in major cities such as Hong Kong, London and Paris representing half the portfolio are equally as valuable as the Barcelona asset in our opinion.

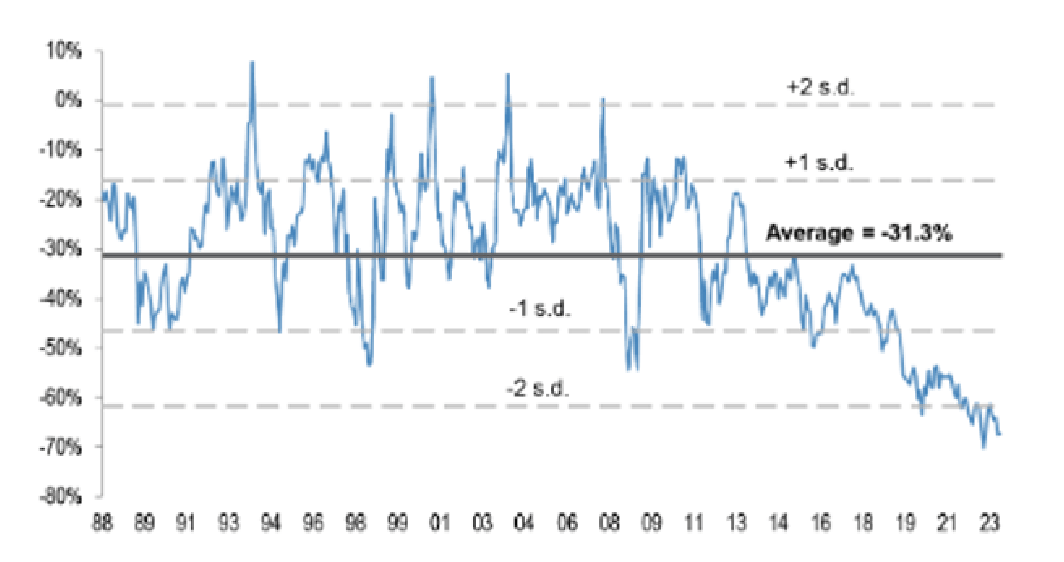

Hong Kong Landlords’ Discount to NAV

{kind=link}

In addition to the above investments, the Fund initiated an investment in Canadian self-storage real estate owner and operator StorageVault ( SVAUF ), Canada’s largest storage provider, owning and operating over 238 storage locations across Canada. StorageVault owns 206 of these locations, plus over 4,500 portable storage units representing over 11.4 million rentable square feet on over 665 acres of land.

The Fund’s investment in StorageVault adds to existing self-storage investments in Australia, the UK and Europe. Similar to these investments, StorageVault operates in a market with favorable fundamental drivers when considering that: ((i)) market supply and consumer penetration is very low compared to the more mature U.S. market; ((ii)) key cities where assets are held are benefiting from demand growth through population growth; and ((iii)) occupancy, rents and operating margins are low compared to the U.S., suggesting a long pathway of potential earnings growth.

StorageVault has been a rapid consolidator of the industry over the last 8 years, acquiring C$2 billion of assets, to become the largest operator in Canada, and has helped ‘institutionalize’ the self-storage asset class in Canada. One of the benefits that StorageVault has is that it is not structured as a REIT, and high levels of income statement depreciation help shield earnings from taxation. The dividend payout is insignificant, such that StorageVault is able to retain virtually all earnings for additional investments into acquisitions or development, which is highly accretive to earnings per share and a driver of net asset value growth. Key executives own over a third of StorageVault shares, and when including options, have a high degree of alignment with minority shareholders, such as ourselves.

Positioning

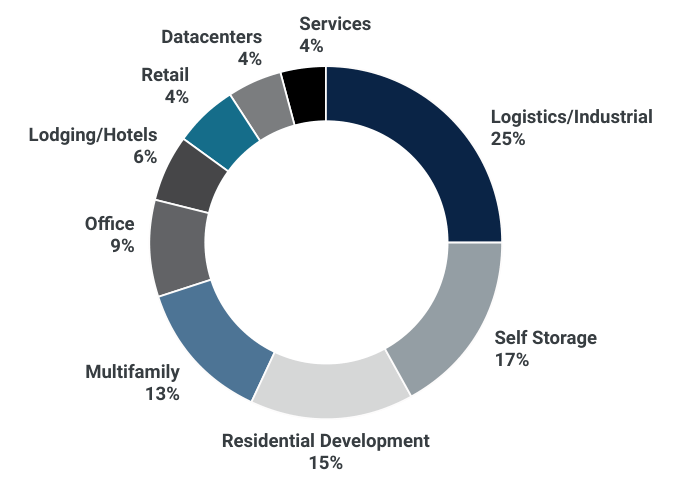

Following the addition of FIBRA Macquarie and StorageVault to the portfolio, at the end of the quarter, the Fund’s largest exposures were to logistics/industrial real estate at 25%, and self-storage real estate at 17% as shown in the following chart.

Notably, the structurally-challenged office asset class only accounts for 9% of the Fund’s exposure, whereas Fund Management estimates that the Fund’s benchmark has a 25% exposure to office real estate. Further, the Fund’s office exposure is through diversified real estate owners in key Asian cities such as Tokyo, Hong Kong and Singapore, where ‘work from home’ is not as desirable given small home sizes, coupled with efficient and safe public transport.

Current Asset Types

{kind=link}

Many of the Fund’s holdings are highly focused on both asset type and location. As such, they tend to have smaller portfolios of assets, and are often small- and mid-market cap companies as shown below.

Current Market Cap 6 Weightings

Source: FactSet, Company Reports, Fund Holdings.

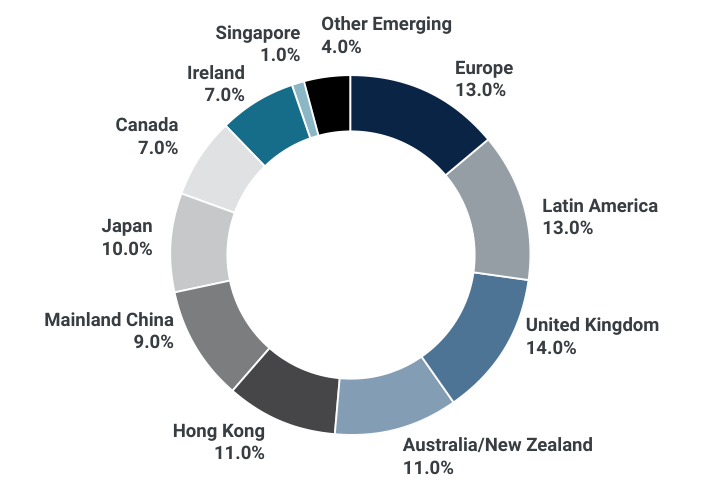

During the quarter the Fund’s exposure to geographic regions remained somewhat consistent to the prior quarter, with reduced exposure to the UK and Australia, in favor of Canada and Mexico.

Current Geographic Exposure

Source: TAM, company disclosures and Bloomberg, Fund Holdings.

{kind=link}

Fund Commentary

In the last two quarterly letters, Fund Management has spoken extensively on three key areas of return catalyst for the Fund in coming periods, notably: i) ‘nearshoring’ trends in Mexico and Eastern Europe, ii) China’s re-opening and its positive impact on consumption (hotels/shopping malls) across Asia, and iii) the deeply discounted valuations in the UK and Europe following last year’s equity market sell off.

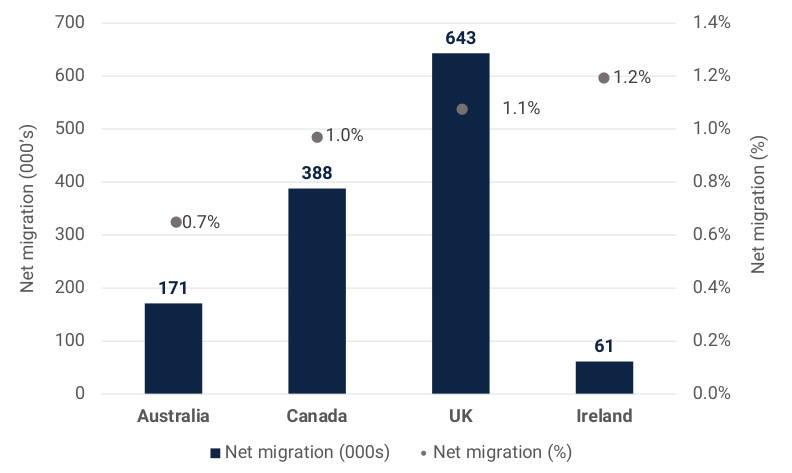

An additional area Fund Management is increasingly focused on is residential market conditions in countries where a big spike in immigration is serving as a positive catalyst. In particular, this is evident in English speaking countries, including the UK, Ireland, Australia and Canada.

High Levels of Immigration

{kind=link}

Combined, the fund has a 22% exposure to residential real estate in these markets in the form of both multi-family rental and residential development as highlighted below.

Fund Exposure to Residential Real Estate

Source: Company Reports, TAM

For example, the Fund’s investment in UK multi-family owner Grainger PLC is benefiting from accelerating rental growth, with growth of just under 7% in the most recent period (half year ending March 31, 2023), with management commenting that they have ‘seen an increase in migration into the UK, significantly post COVID, and there is a strong indication and prediction of good rental growth for the next five years’, elaborating that ‘…the structural drivers are the increasing demand for renting at a time when supply is shrinking.

The market for good quality rental homes has rarely been stronger and Grainger is in a good position to benefit. And this is leading to accelerated rental growth’.

A further example can be seen in the Fund’s investment in Boardwalk, an Alberta Canada based multi-family REIT, where new leases are being struck almost 14% higher than previous, and tenants renewing leases are having increases of almost 8%. The Province of Alberta and the city of Calgary are seeing outsized rental growth as a result of population and job growth, comprising both international and inter province migration.

Despite high rental growth, affordability is still reasonable with wage growth generally rising at similar levels to rents for both Grainger and Boardwalk. For instance, in Alberta, such high rental growth would normally be met with a quick increase in new multi-family supply, given improving economics and a relatively simple planning approval process. However, the new supply response is so far muted, with development only set to deliver enough supply for about half the expected population growth. The main reason for limited new supply is a combination of elevated construction costs and high interest rates. For new development to stack up financially, rents would still need to grow substantially. In the UK, and specifically London, given rents are 25% above 2019 levels, it is easier for development to make financial sense. However, new supply is limited, given a planning system and regulatory requirements that are notorious for increasing cost and delaying the commencement of projects.

For residential developers and homebuilders, the rapid increase in interest rates in these markets has obviously been a negative for housing affordability, and hence demand, particularly in the context of higher construction costs. One exception is in the Fund’s exposure to the Dublin, Ireland residential market through developer Glenveagh Properties Plc. There is such an acute shortage of housing in Dublin that the government has enacted several programs to assist homebuyers in purchasing new homes. Additionally, onerous planning restrictions appear to be easing, paving the way for developers such as Glenveagh to increase volumes, and thus returns for shareholders in coming years.

The Fund’s unique exposure to residential real estate in markets where demand exceeds supply bodes well for potential returns over a long-time horizon. With high interest rates, elevated construction costs, and difficult planning/regulatory issues, markets will likely fail to deliver sufficient supply to match high population growth, thus causing ongoing rental growth and high home prices despite high interest rates. In many ways, the positive long-term fundamental backdrop in the Fund’s exposure to residential real estate is similar to its other large positions in self-storage real estate, and industrial/ logistics real estate in ‘nearshoring’ markets. When complemented by well-capitalized balance sheets, aligned and experienced management teams, and attractive valuations, Fund Management remains positive on the outlook for the Fund.

We thank you for your continued support and look forward to writing to you again next quarter. In the meantime, please don’t hesitate to contact us with any questions, comments, or ideas at realestate@thirdave.com.

Sincerely,

The Third Avenue Real Estate Value Team

Footnotes1 The FTSE EPRA Nareit Global ex U.S. Index is designed to track the performance of listed real estate companies and REITS in both developed and emerging markets. By making the index constituents free-float adjusted, liquidity, size and revenue screened, the series is suitable for use as the basis for investment products, such as derivatives and Exchange Traded Funds (ETFs). Index performance reported since inception of Institutional Share Class. 2 Excess Return, Excess return refers to the return from an investment above the benchmark. Source: Investopedia 3 Small Cap is Equity Market Cap up to US$2bn, Mid Cap US$2bn-US$10bn, Large Cap >US$10bn. 4 Adjusted funds from operations (AFFO) refers to the financial performance measure primarily used in the analysis of real estate investment trusts (REITs). The AFFO of a REIT, though subject to varying methods of computation, is generally equal to the trust’s funds from operations (FFO) with adjustments made for recurring capital expenditures used to maintain the quality of the REIT’s underlying assets. 5 Book value is equal to the cost of carrying an asset on a company’s balance sheet, and firms calculate it by netting the asset against its accumulated depreciation. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Third Avenue International Real Estate Value Fund Q2 2023 Portfolio Manager Commentary