VNQ - This Bull Market Is Still New; Outlook For 2024

2023-12-18 09:46:31 ET

Summary

- The Federal Reserve's dovish commentary on potential rate cuts has been a nice boost to the markets the past week or so.

- Low unemployment and higher wages are driving the U.S. economy, fueling growth in the nominal economy and what we think will be a strong 2024 in the stock market.

- Artificial intelligence (AI) and the Federal Reserve's potential rate cuts are two primary sources of upside for the U.S. stock market in 2024.

- We prefer the market-cap weight S&P 500 over the equal weight S&P 500 and don't like the 60/40 stock/bond portfolio, dividend growers, small cap value, and REITs.

- We continue to be huge fans of the net-cash-rich, free-cash-flow generating and secular growth powerhouses found in big cap tech and large cap growth.

By Brian Nelson, CFA

The Federal Reserve provided a nice boost to the markets the past week or so thanks to dovish commentary that noted the Fed may consider lowering rates to prevent overshooting to the downside with respect to its inflation target of 2%. This was new “news,” as markets can expect cuts even without an exact 2.0% inflation measure, but one that might even have a 2 handle. We loved the commentary as it paves the way for a resilient 2024, in our view. We think we’re in the midst of the Roarin’ 20s economy in the U.S., and we’ve never been more bullish on stocks.

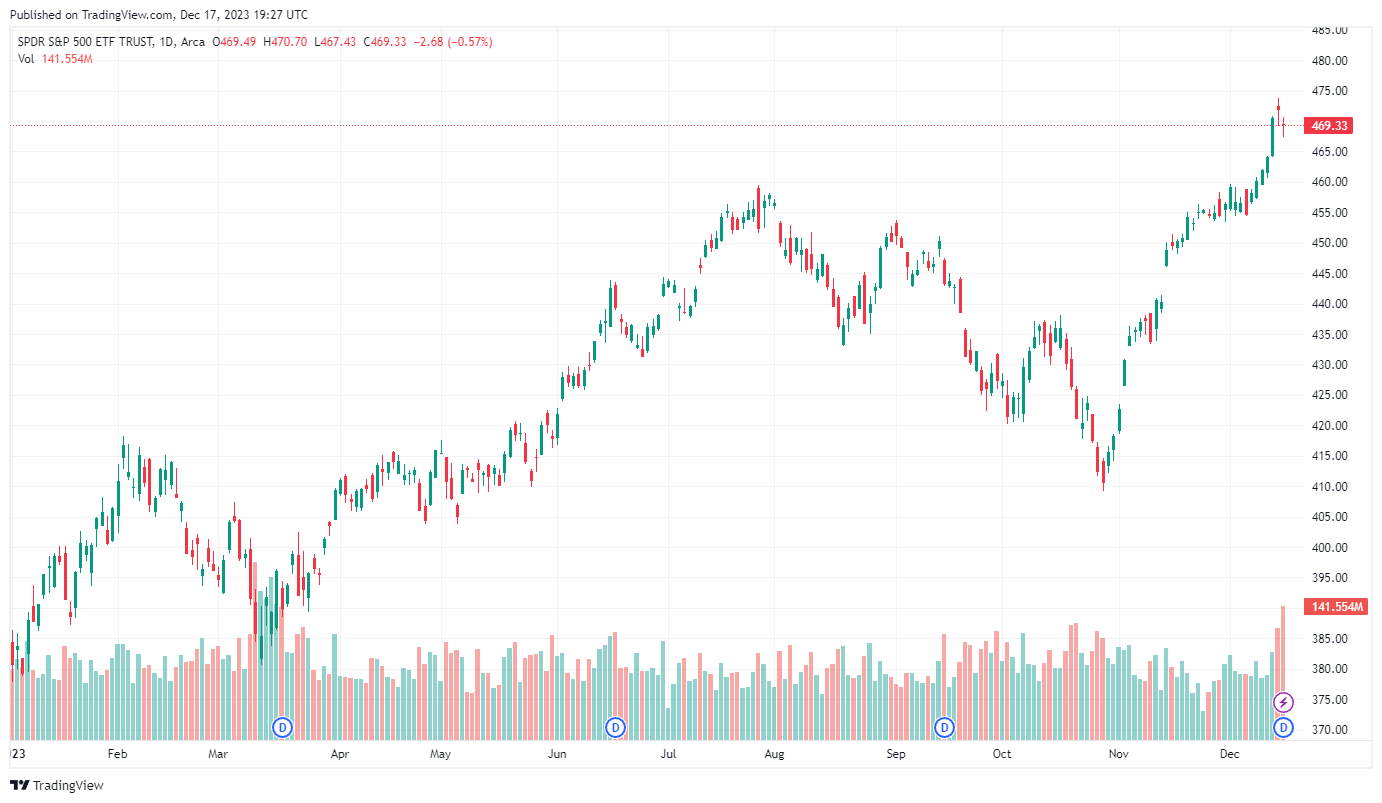

The S&P 500 has rallied considerably since the October lows, and we expect 2024 to be a fantastic year. (Trading View)

{kind=link}

There are two foundational drivers behind the good times. First, after what was a scare to the job market in COVID-19, today, employers continue to hold onto their employees out of fear of losing their best talent. According to the latest tally by the Bureau of Labor Statistics, the unemployment rate fell to a structural low of 3.7% in November, and we doubt measures can get much lower than the mid-3% level given natural attrition in the economy. Striking workers are now back, and that was the big reason for the unemployment rate ticking down from October.

Second, employees perhaps have never had it better. Employers are starving for great workers. Entry level jobs are morphing into living wages these days, with perhaps the best example being McDonald’s ( MCD ), where the average crew member makes north of $14 per hour in Illinois , for example. This is a far cry from the minimum wage of 20 years ago, which was between $5-$6 per hour. Though higher minimum wage is showing up in the higher cost of a burger, consumers are stomaching the higher prices, and this is fueling considerable growth in the nominal economy, which is all that matters to stock prices. Employees across the board are holding on to the nice wage gains received during the past few years, while unemployment levels remain low.

With this economic foundation firmly intact, there are two primary sources of upside for the U.S. economy. The first is artificial intelligence [AI]. Microsoft ( MSFT ) has already found a way to monetize AI through Copilot, but we expect 2024 to be filled with announcements from other companies on how they are transforming AI from a concept to cold, hard cash. Clearly, Nvidia ( NVDA ) and AMD ( AMD ) will benefit by selling the picks and shovels of the AI revolution, but AI is probably the biggest source of productivity improvement since the dot-com boom 20 years ago. Unlike those days, however, companies are much better off than back then, particularly in big cap tech and the stylistic area of large cap growth, which are overflowing with net-cash-rich balance sheets and tremendous free cash flow generating capacity. We even think Nvidia’s shares are a bargain as we outline in this article .

The second source of upside for the U.S. economy will likely occur in the back half of 2024. Though the Federal Reserve receives a considerable amount of undue criticism, the reality is that the group is doing a fantastic job, in my view. Hats off to Chairman Powell and team. They managed to guide the economy through a once-in-a-century global pandemic, and now with employees better off than ever, they have managed to drive inflation down with rate hikes, with only a few casualties in the regional bank sector, an area that should probably have been avoided by most investors anyway. Once the Federal Reserve starts considering rate cuts next year, this market has tons more room to run, in our view. The crash higher that we wrote about in this article in early November is likely still ahead of us.

Let’s now talk strategies. First, we think the 60/40 stock/bond portfolio is just about the worst thing that investors have ever encountered. For starters, the majority of investors utilizing this allocation are generating the majority of their returns from equities anyway, and since that’s the case, why not just have equities and 12-24 months of expenses in a cash emergency fund. Investors can pursue a dynamic withdrawal strategy depending on market conditions. So many investors have lost out on the prospect of generational wealth due to these portfolio allocations that try to smooth out equity volatility, and we think investors are much better off in the long run with equities, especially for portfolios that eventually pass down to beneficiaries.

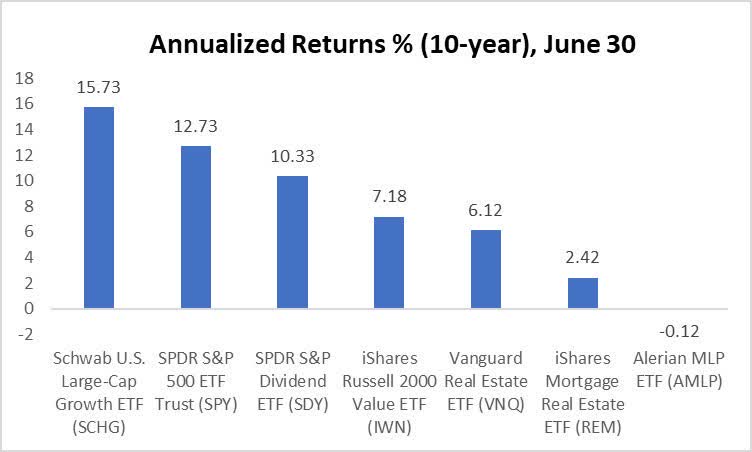

The total return of dividend growth stocks and high yielders has trailed that of the broader market and the stylistic area of large cap growth the past 10 years. (Valuentum)

{kind=link}

Second, we think dividend growth strategies will suffer during 2024. Many dividend growth strategies came into vogue in the near-zero interest rate environment, but such an environment is no longer the case, and dividend payers have underperformed, as shown above. We think investors falling into the trap of seeking yield for yield’s sake are probably moving into higher-yielding fixed-income alternatives these days, driving down equities used in this manner, and we doubt dividend growers will come back into favor again until the 10-year Treasury rate falls below that of the average S&P 500 company, which likely won’t be for some time. Investors shouldn’t forget either that the dividend is nothing like a bond coupon, as the free dividends fallacy outlines . It is what it is—the stock price is reduced by the dividend on the ex-dividend date.

When a company announces a dividend, its share price is reduced by the amount of the dividend on the ex-dividend date. (Trading View)

Third, at the end of 2022, many investors may have been scared into the equal-weight S&P 500 ( RSP ), as 2022 was a miserable year, and the index was top heavy with big cap tech names. Now, at the end of 2023, many investors may be feeling the same way, but for a different reason, as those same top-heavy tech names have had a fantastic year in 2023. The equal-weight S&P 500 underperformed the market-cap weight S&P 500 ( SPY ) by a considerable margin in 2023. It seems that some investors just can’t get comfortable with the make-up of the market, but the market has always been top heavy throughout its history. We expect the strongest names to only get stronger as many such as Microsoft and Alphabet ( GOOG ) are heavily tied to trends in AI as they showcase pristine net-cash-rich balance sheets while throwing off considerable free cash flow.

Fourth, some investors are beholden to the view of reversion to the mean. While this works well in some cases in some areas of endeavor, in others such as investing, there are fundamental intrinsic-value drivers that often make this dynamic silly to believe in. In some cases, reversion to the mean, as it is used in traditional quant applications as in quantitative value, is no better than betting on black at the roulette table just because red has come up 10 times in a row. The reality with roulette is that each event is independent of the next, and that’s how we feel about groupings of stocks with low P/Es, low price-to-book (P/B) ratios, and other low statistical valuation variables as in most traditional value indices. Valuation multiples, themselves, just aren’t indicative of intrinsic value in most cases and are largely unreliable in others.

These days, with the abundance of available information, stocks often have low valuation multiples for good reasons. They could be facing deteriorating revenue trends, have large net debt positions on their balance sheets, be facing a heightened competitive environment, or have exogenous considerations such as contingent liabilities. Given the arbitrary nature of book value these days with the number of companies having negative book value and how easily it can change with capital structure shifts, value indices relying heavily on book value are almost purely random, in our view. From our perspective, investors should know what they are getting into when they are betting on quantitative value, and we expect continued deterioration in troubled, low-quality equities in indices such as small cap value relative to strong, net-cash-rich, free-cash-flow generating powerhouses found in the areas of big cap tech and the stylistic area of large cap growth.

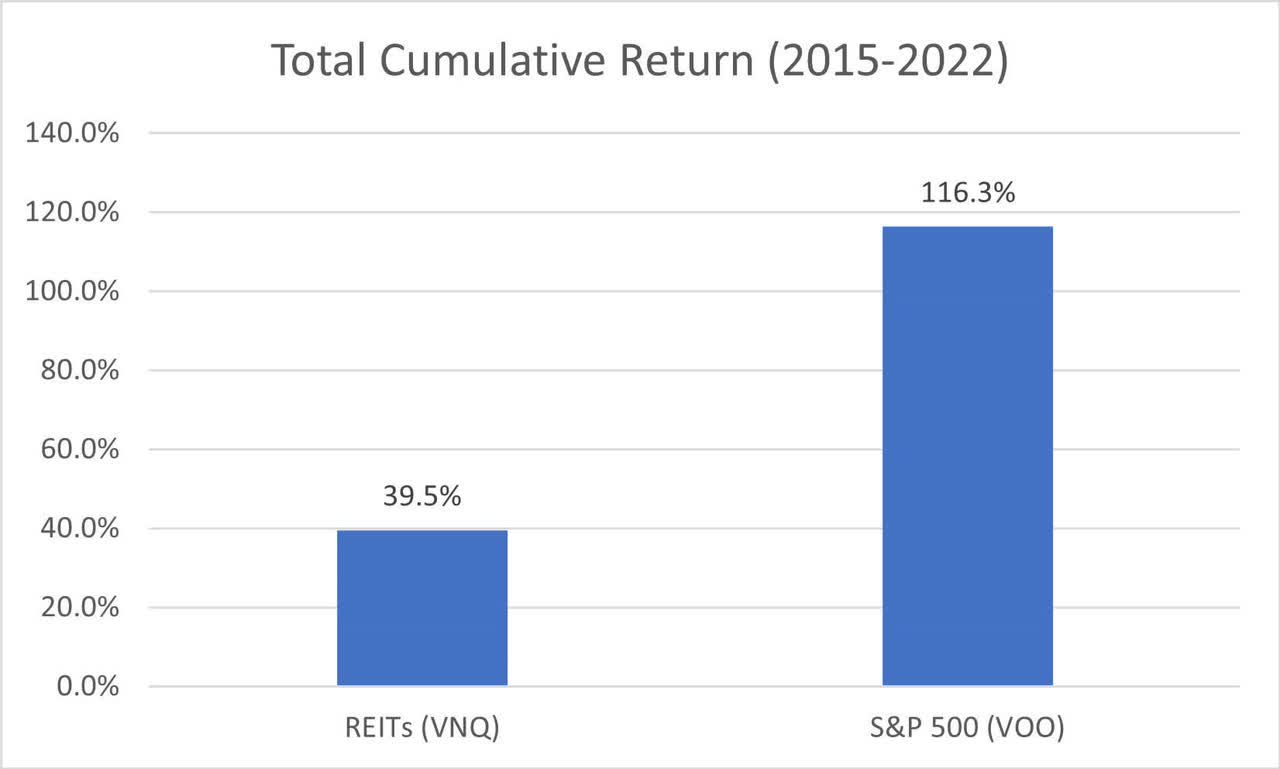

REITs have not performed as well as one might have thought. (Valuentum)

{kind=link}

Fifth, we think equity REITs ( VNQ ) are dead in the water. They may do okay in 2024 as interest rates remain calm after a difficult year in 2023, but chasing their yields for yield’s sake hasn’t been a great proposition the past decade, and we don’t think that will change. We wrote about how we don’t like REITs that much in this article , and the secular trends working against them aren’t going away. Most office REITs will likely be in a world of hurt as working habits change because of work-from-home trends, and many retail REITs will likely struggle to grow much, outside of deal-making, given the proliferation of e-commerce. We expect REITs to remain sketchy income generators, and that they are required to pay out almost all their earnings as dividends--precluding them from building up net cash on the balance sheet--makes them precarious stocks to hold through the course of the economic cycle, in our view.

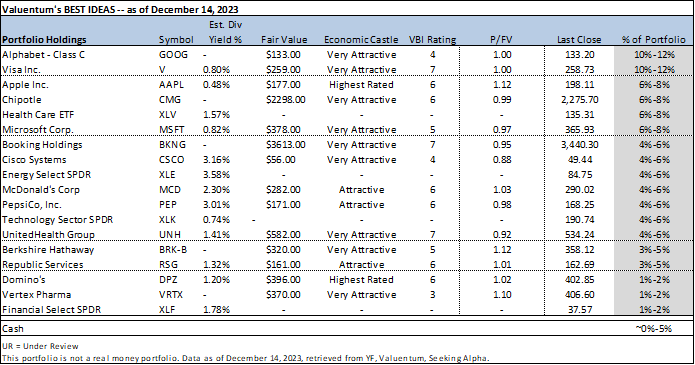

Valuentum’s simulated Best Ideas Newsletter portfolio, as of December 14, 2023. (Valuentum)

{kind=link}

With all of this said, what does that leave left? Well, we love stocks for the long haul, and we continue to be huge fans of the cash-based sources of intrinsic value: net cash on the balance sheet and future expectations of free cash flow. Stock prices and returns are in part a function of these two dynamics, so it should not be surprising why we like them so much. A stock with net cash on its balance sheet is worth more than a stock with net debt on its books, all else equal. If expectations of a company’s future free cash flow increase, so should the stock price, all else equal. If expectations of a company’s future free cash flow decreases, the stock price should fall. Investing is never this easy, of course, as there are a lot of moving parts, but focusing on the cash-based sources of intrinsic value is a great place to start.

Looking forward, we believe 2024 will be a great year for stocks thanks to foundational drivers in the employment market and sources of upside in AI and the Federal Reserve. We expect the areas of big cap tech and the stylistic area of large cap growth to continue to lead the markets, if not during 2024, this decade. We expect any rotation into low-quality stocks to be short-lived in nature, as the appetite for any investor in small names in energy and regional banks that dominate small cap indices these days is a misguided one, in my view. REITs may recover a bit on lower interest rates in 2024, but we expect continued underperformance of the sector relative to the S&P 500 over longer-term time horizons. Save for dividend-payers in big cap tech and large cap growth that are paving the way for innovation this decade, we think the heyday of strong total returns for dividend growers is over, at least in the coming years. All told, we’re sticking with what has worked the past decade and a half, and that remains big cap tech and large cap growth. Back in July, we highlighted 5 stocks for a new bull market in this article , and these remain among our favorites.

For further details see:

This Bull Market Is Still New; Outlook For 2024