AVUV - This Employment Report Is Pivotal: Bull Or Bear Trend At Stake

2023-03-09 11:20:25 ET

Summary

- US bond and equity markets are at a major crossroads.

- In this context, Friday's Employment Situation Report has extraordinary importance.

- Technical analysis reflects the complex evolution of macro-fundamental expectations since October 2022 and highlights the fact that the US equity market currently is at a critical junction.

- The direction of the primary trend of the US equity market is at stake.

In this article I will provide a preview of the Employment Situation Report released Friday, March 11, at 8:30AM EST, and explain why this report may prove to be pivotal for the future evolution of the US economy and financial markets.

Preview

According to Investing.com, the median forecast of surveyed economists is expecting an increase in non-farm payrolls of approximately 205,000. This would represent a major deceleration in job growth compared to the January figure of 517,000.

The median forecast expects the unemployment rate to hold steady at 3.4%.

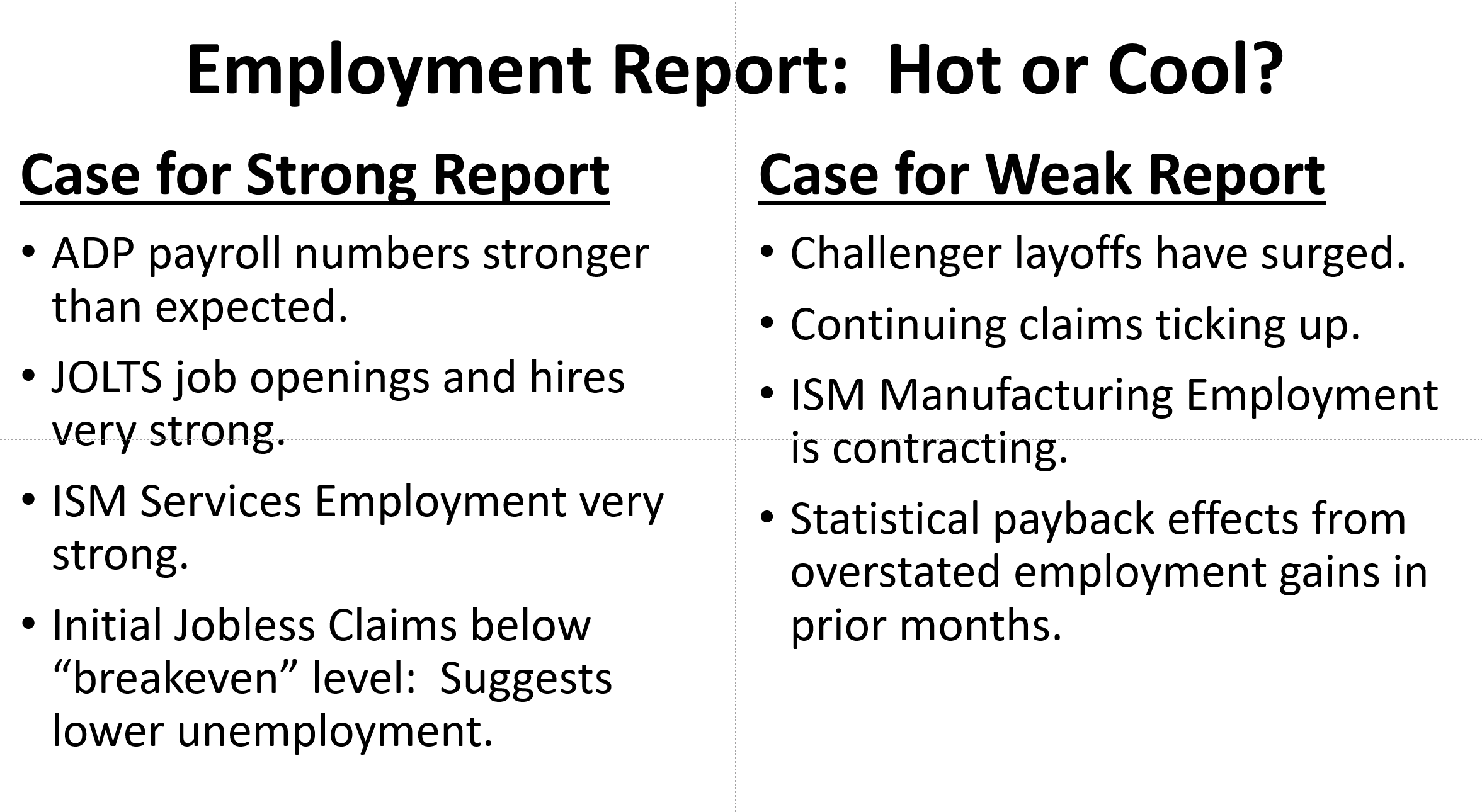

Will the employment numbers come out hot or cool? The following table lays out several contrasting arguments on both sides of the debate.

Hot vs cool factors February Employment Report (Investor Acumen)

{kind=link}

My own view regarding the likely outcome is neutral. For the BLS itself, the margin of error for estimating non-farm payrolls and total employment is very high and this margin has been rising in recent months. Forecasters trying to estimate the BLS’s figures are not only challenged to estimate the actual numbers, they also must estimate the errors in the BLS’s estimation of the numbers. The BLS reports that revisions are made more than 90% of the time. The estimated margin of error (confidence interval 90%) in its non-farm payroll estimates is roughly 130,000 while the margin of error in the estimate of the unemployment rate is roughly 0.20%.

In my view, there's a greater than average possibility of statistical “payback” this month as prior months were likely overestimated. This would imply a potentially soft number. On the other hand, the increased hawkishness of FOMC Chairman Jerome Powell in recent days – which seems to have come out of the blue – has caused me to wonder whether he may have received some sort of preview of the data (note that the BLS had more time to prepare this report than usual).

Why is This Month’s Employment Report So Important For the US Economy?

The US economy is currently at a crossroads. Mortgage rates have spiked above 7.0%. The 2-year Treasury yield is above 5.0% - a level not seen since 2006 (only briefly, at that) and which has not been consistently seen since the 1990s. The Fed Funds futures markets are currently estimating over a 75% probability that the Fed Funds rate will be in the 5.5%-5.75% range by June - and above a 40% chance that the rate will be in the 5.75%-6.00% range by July.

It is our view that these levels of interest rates - or anything higher - will strangle the US economy, if they're maintained for any length of time (say, three months).

Whether or not the Fed will raise interest rates significantly above and beyond their most recent median estimate of 5.3% is going to depend - perhaps more than anything else - on the level of tightness in the labor market. Indeed, I believe the Fed currently sees this as more important than CPI itself. This is because the majority of FOMC members (including Powell) believe that inflation will not fall back to their target 2.0% level unless unemployment rises fairly significantly (around 1.0%) from current levels. If the unemployment rate actually fell in February and/or payrolls grew significantly above the “breakeven” level (which is below 100k), then the Fed will be highly pressured to raise interest rates significantly above that which they had been contemplating until recently.

As I mentioned before, the US economy is very unlikely to be able to sustain an economic expansion with interest rates any higher than they are right now. A hot employment report could push US interest rates above and beyond the breaking point for the US economy.

Implications for Bonds and US Equities

Ever since the probability of a “no-landing” started to gather force roughly one month ago, the bond market has undergone a major correction. Estimates of the terminal Fed Funds rate have risen by roughly 75 basis points in less than a month. The 10-year treasury yield has increased by more than 60 basis points. 30-year fixed mortgage rates have spiked from roughly 6.0% to over 7.0%. This action indicates that participants in the fixed income markets are clearly very worried about overly tight labor markets, inflation and the potential path of interest rates.

The equity markets do not seem to believe that the situation as is as dire as the bond market appears to fear. Indeed, if US equity investors were as concerned as bond market investors, the S&P 500 might be re-testing the October lows right now. The last time 2-year Treasury Yields, 10-year Treasury yields and Mortgage rates were at current levels was when the S&P 500 was making its lows below 3500 in October 2022.

The divergence in expectations between the bond and equity markets have rarely been this extreme. The bond markets are expecting levels of interest rates that are likely to strangle the economy. However, equity prices, which rallied very substantially off of their lows in October 2022, clearly reflect substantial optimism about the prospects of a soft landing.

Pivotal Moment in Economy Reflected in Technical Conditions

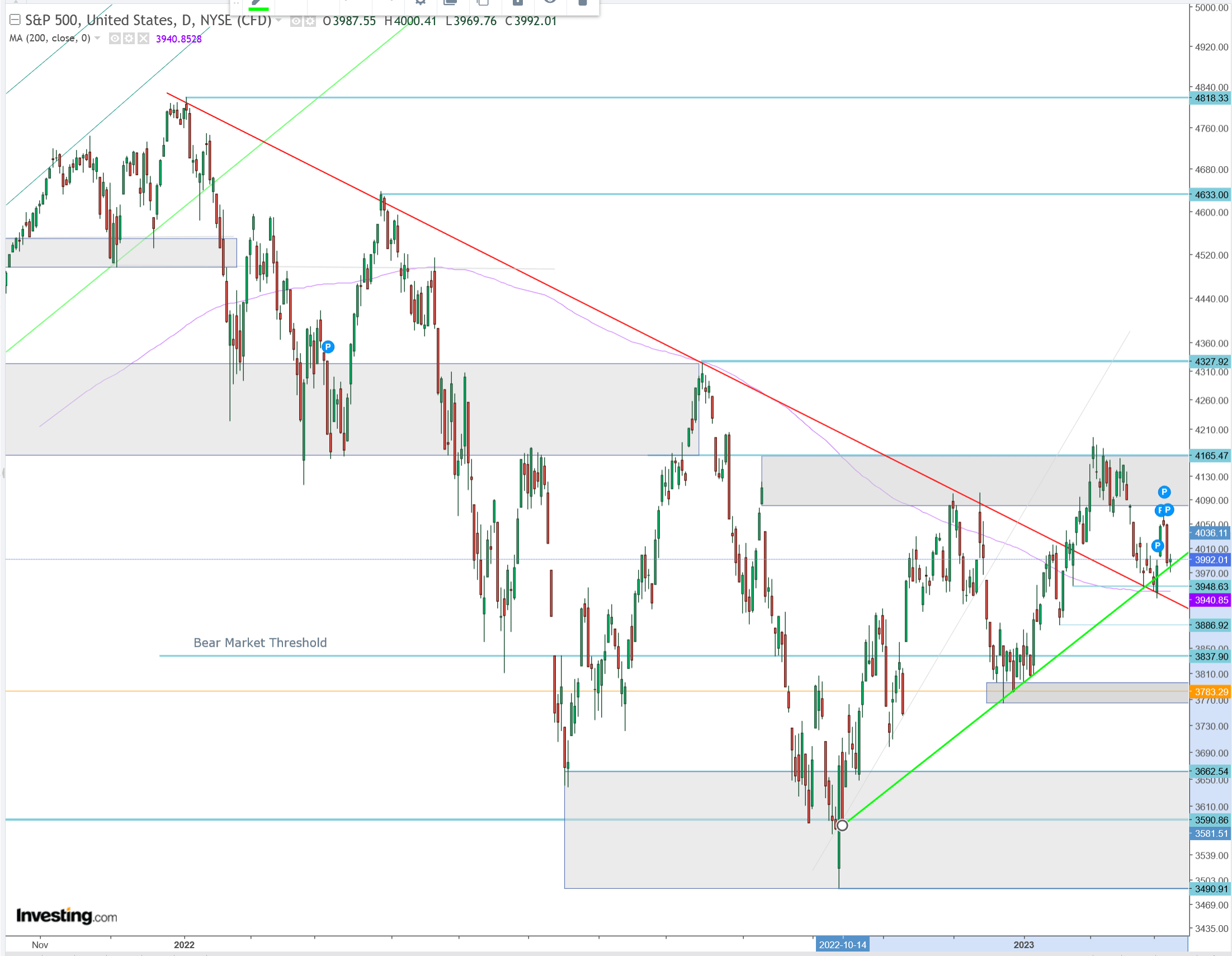

As can be seen in the graph of the S&P 500 index below, the US equity market is literally at a crossroads, represented by the red downward trend line (old bear market) and the green upward trend-line (potential bull market). Furthermore, the S&P 500 is retesting the 200-day moving average and some horizontal support (albeit minor).

{kind=link}

S&P 500 Technical Analysis (Investor Acumen, Investing.com)

If the S&P falls back down below the bear market down-trend and breaks down below the up-trend that has been in place since December – plus violating the other two support elements - the chart pattern is pretty clearly sending a warning about where the primary trend could be headed from here.

The current uptrend, in place since December 2022 would be broken if the SPX fell below the 3760 level. Indeed, this would set up a potential test of the October 2022 lows. On the other hand, a bull market would be confirmed if SPX managed to rise above the recent high of around 4200 and then above final key resistance at 4330.

In terms of how this ties in with the evolution of the macro-fundamentals discussed in the previous sections, the price action on the chart can be related to the macro-fundamentals as follows: The initial up-move off of the October lows reflected expectations that any US recession would likely be mild (see my report “ The Most Highly Anticipated Recession in History ”). The up-move from December through February reflected expectations of increased probability of a soft landing. However, ever since the probability of a “no-landing” scenario started to increase substantially since the beginning of February, the US equity market has been struggling. And, as things currently stand, the market is now facing the real possibility that the “no-landing” scenario could cause the Fed to raise interest rates so high that it kills the economic expansion.

Conclusion

The US equity and bond markets are at a significant crossroads.

Bond markets are at or near levels of yields that could strangle the US economy.

The US equity market, as can be seen from our analysis of technical conditions, is at a crossroads between resumption of the old bear market trend (January to October 2022) or confirmation of a new bullish trend that has been in place since October 2022.

Given how the market is currently positioned from a technical standpoint, Friday’s Employment Situation Report could potentially trigger the unfolding of decisive price action that clarifies the likely direction of the primary trend in the US equity market for most or all of the rest of 2023.

For further details see:

This Employment Report Is Pivotal: Bull Or Bear Trend At Stake