PSA - This Is A PSA: Public Storage Is Undervalued

2023-06-21 10:32:11 ET

Summary

- Public Storage has shown consistent growth over the past 20 years, with only two years of negative FFO growth.

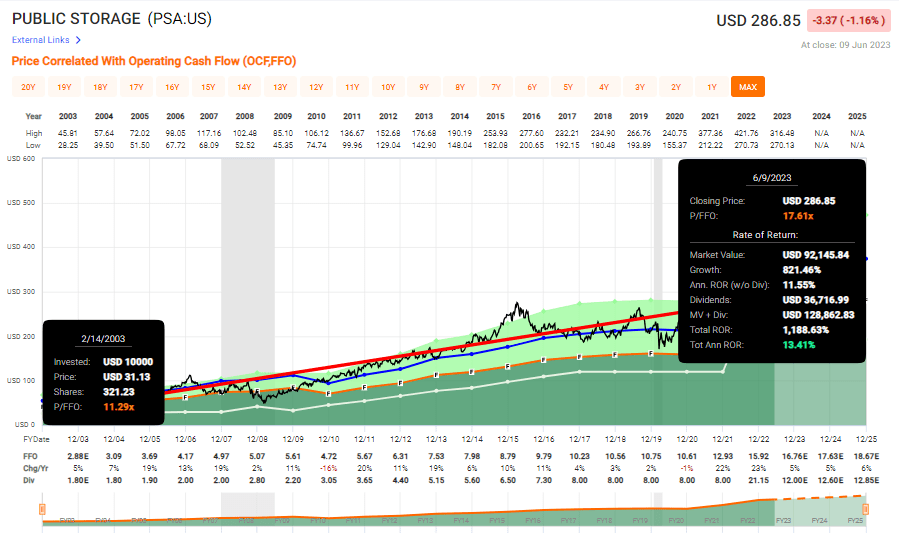

- PSA has averaged annual FFO growth of almost 9% per year, resulting in a market-beating 20-year RoR of 1,188%.

- The company is currently undervalued, making it an attractive investment opportunity in the storage industry.

Author's Note: This article was published on iREIT on Alpha in early June 2023

Dear subscribers,

The storage industry tends to be one of the safest havens of growth and quality in times of industrial turmoil. All you need do is look at the 20-year averages of a market leader, or perhaps better said "the" market leader Public Storage (PSA), in order to see this.

Why?

Because out of the last 20 years - the company had two years of negative FFO growth. One back in 2010, when it dropped 16%. The other in COVID-19 and 2020, when it dropped a whopping one percent. Aside from that, it's been growth, and even inclusive of those drops, PSA has averaged annual FFO growth of almost 9% per year which has rewarded investors with a market-beating 20-year RoR of 1,188% even after the decline from its premium over the past few years.

{kind=link}

That's why I consider it a bit of a "PSA" to tell you that Public storage, or PSA, is actually currently undervalued.

Let's dive in.

Public Storage - A class-leading REIT

While I have written about other companies in the space such as National Storage Affiliates (NSA), between NSA and PSA, PSA is the clear market leader. With 2,800 properties across the width of the nation, the business is large. Over 1,800,000 customers use the company's services and properties, and the company offers over 200M square feet of space in total.

The company has the sort of operational history you as a conservative investor really want to see. 50 years of operational safety, a REIT with an A-rating - not many REITs in the world can come to the table with an A-rating in terms of credit.

PSA IR (PSA IR)

PSA is a "better breed" than most REITs. Its profitability metrics are off-the-chart. It has a very low debt for a REIT, and if we look at the company with even remotely traditional fiscal metrics, some of these qualities shine through like through glass.

ROIC is going to be good for most self-storage REITs but the company has consistently, over the last 10 years managed to retain massive profitability in its investments and use of invested capital. During ZIRP, this went above double digits net of the cost of capital, and even now it's above 5%. This is impressive.

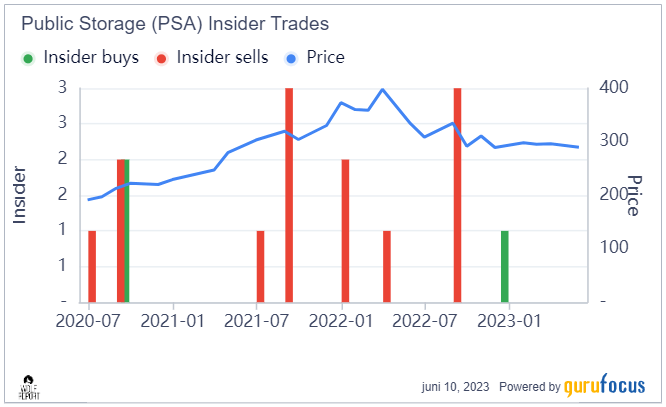

What's more and telling, since the company dropped back in early 2023, it's the first time in over 2-3 years that insiders have been adding shares. They did not add shares during all of 2021-2022, but they have been adding again now. In fact, insiders have been selling significant amounts of shares during the 2021-2022 overvaluation - as I myself would have done, if I held shares of the company at the time.

The whole "Invest-and-hold-forever" approach does work, and I don't want to bad-mouth it, but it's far more efficient and profitable, to stay valuation-conscious.

Insider activity usually doesn't say all that much, but in this case, I do believe it says quite a lot and it's worth taking a look at.

{kind=link}

The fact is, PSA is rarely below its typical premium of 20-22x to FFO. Whenever it is, it's something you should pay attention to, because historically, investing at this time has been something that has nearly always resulted in eventual profit.

PSA has outperformed the overall broader average of the Real estate sector for the past 18-20 years, averaging a CAGR NOI growth of 5.2% indexed to 2004, and around 146% cumulative. That's more than twice the cumulative NOI growth in the broader real estate sector - and I see no sign that this is changing on a forward basis, given that PSA is forecasting further growth.

The company's largest market is Los Angeles - and here is perhaps one of the challenges. if you're not a fan of the west coast and California, you may want to know that PSA has considerable exposure here - though the company has been growing significantly here as well, going against the grain in terms of how the sector of REITs has fared in the geography overall.

The latest results from PSA we have are the 1Q23 results, and this quarter more or less just confirmed the overall positive view we can have on PSA. The company's move-in volumes were up 13%, same-store NOI more than 11%, and acquisition and development NOI up 30%. The company is encountering very little headwind, focusing on the digital transformation of the operating model, and its size and over $50B worth of market cap gives it a unique position to execute where smaller companies may have more difficulty.

Any risks to the company are minor in scope - at least as I see it. Risks and considerations have to do with pricing sensitivity. In this market - as in many others - it's always about pricing, and seeing the first signs of softness both on a macro level and in certain geographies as well. The move-in volume strength the company currently sees dispels the notion of any massive softness in pricing. The company has also confirmed that this move-in strength has moved into 2Q23 as well, and the literal answer from management was that PSA has not seen anything concerning, currently, with regards to pricing softness or sensitivity.

The biggest issue at this time is how the macro uncertainty and the potential of a recession imply the development of 3Q and 4Q of this year, which in turn makes the full-year forecast somewhat uncertain still. I do not expect double-digit FFO growth in this environment, akin to the 2022 trends of over 20% in FFO growth. I do expect the company to manage 4-6% though, and the current FactSet forecast is also at around 5%.

The company remains in a strong position in terms of its balance sheet. The current debt is around 61%, with an average cost of prefs/debt of 2.8%, meaning there is a just-above 3x leverage. That's low - for REITs and for the sector, which means that the company can move forward on opportunities it considers attractive.

What I see here is that the near-term future implications are not tilted toward negative at all. The company is quite the contrary, strengthening its competitive advantages and holding on to a revenue and income stream that's well above the safety and quality of many other REITs. Current trends seen in 1Q do not suggest there will be any significant near-term downside to the company, and on the basis of this, I would say that there is a lot to like about this company at any sort of conservative valuation.

Let's look at where this valuation currently puts us.

Public Storage - The valuation is attractive, even if it's not triple digits

Public Storage won't generate triple digits in 3 years, like some companies that I've recently written about. That's not why we buy it, or the expectation we should have, unless we see massive overvaluation, which we have before.

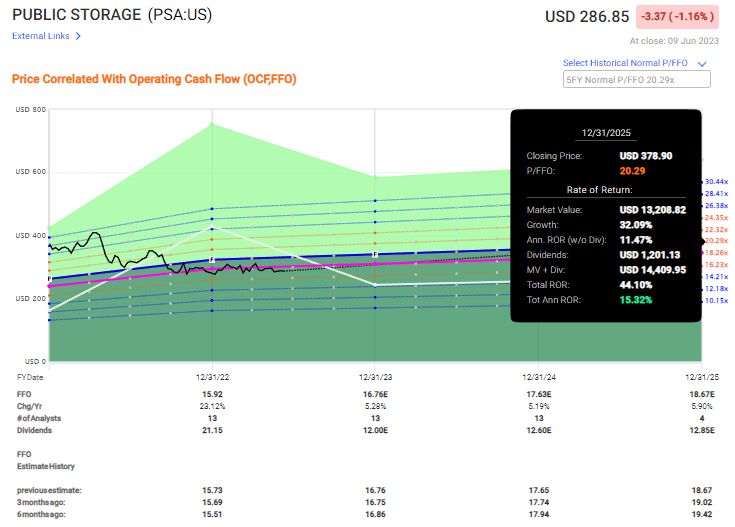

Current valuation trends put PSA at around 17.6x P/FFO, which is well below its historical average of about 20-22x P/FFO. Growth rates going forward are going to be more muted - expect 4-6%, with maybe 5% on average per year.

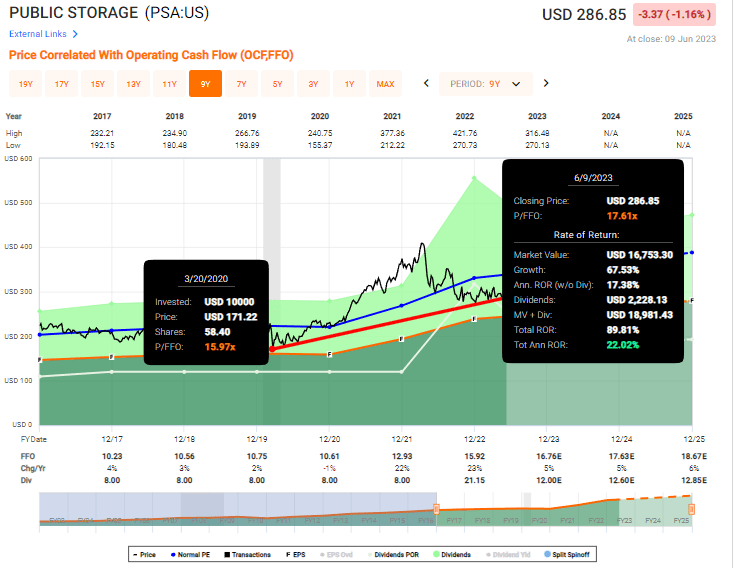

The current upside to Public Storage is high - especially considering that the company has been what I would consider highly valued for several years. To put it very frankly, PSA has not been this appealing since 2019-2020. That was the last time, and only for a short time when the company traded below 20x P/FFO. Anyone who invested during COVID-19 is now still in the positive to the tune of 22% annualized, even if you did not sell, or almost 90% total ROR. This shows the power of investing during periods of undervaluation.

{kind=link}

Do I consider it likely for the company to decline to this level again? We might see 15x, or we might not - but in any case, 17.6x is still a very good price, and it's good enough for me to invest.

The average S&P Global analyst targets come to a range of $294 on the low side and $370 on the high side, with a current average of $341. It's close to my target because I consider PSA to be a "BUY" at a price of around $340/share or lower. The upside here is high enough - outperformance to premium will mean impressive RoR atop of that. 11 Analysts follow the business, and out of 11, 9 are at a "BUY" - the signal here is very clear, and I tend to agree with it.

At 17.6x, we're not at 1x to NAV - we're still below 0.9x. Downward potential is obviously possible, but I have a hard time beyond geographic weakness or customer pricing softness being a catalyst for that sort of move - and that is not something that the company currently sees. Because that is not something we see, then I don't see much downward potential because the company's direction is, as forecasted, in the positive.

{kind=link}

With that in mind, my stance on PSA is positive, and I'm slowly starting to add to my position in the company. At this particular time, I have around 0.6% of my portfolio in the company, and my target is well beyond 1% eventually. While this company won't make you rich - at least unless you're already rich, the company will pay you a good dividend, should protect your capital, and gives you the advantage of some of the most recession-resistant cash flows out there.

There is so much to like about PSA, and part of what I like is that it isn't all that exciting. It's just "boring storage" - and that is, as I see it, an advantage in this environment.

For all of these reasons, I consider Public Storage to be a "BUY" here.

Thesis

- Public Storage is a sector outperformer. It's a solid business in a very solid sector, the self-storage sector. The company is fundamentally safe, A-rated, the biggest in its entire sector, which is a fragmented sector, to begin with and comes with to me undeniable upside at the correct valuation.

- I view the company as an absolute "BUY" at the right valuation, due to the safety of its cash flows and the resiliency, the proven resiliency, of its business model.

- Based upon this, I give the company a clear PT of around $340/share, allowing for PSA to trade at a premium which I believe that the company deserves.

- Because of this, PSA is a "BUY" here and I believe it warrants your attention.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria except it being currently cheap - I won't call it cheap at 17x P/FFO - making it relatively clear why I view it as a "BUY" here.

Thank you for reading.

For further details see:

This Is A PSA: Public Storage Is Undervalued