QVMS - This Rather Good Jobs Report Won't Change The Downtrend

Summary

- In this article, we discuss a rather bullish job report for December. Job gains and wage growth were strong, yet not too strong to pressure the Fed more than needed.

- Unfortunately, economic growth is slowing, while inflationary wage growth remains an issue. The Fed knows this and made clear that it will have to weaken these factors.

- Hence, I do not expect the market to be out of the woods yet. I'm prepared to buy the market more aggressively in the low 3,000 points range.

Introduction

It's the first Friday of the month, which means we need to talk about the job market, the Federal Reserve, and what this means for the market. In this article, we discuss a surprisingly strong jobs market, yet not strong enough to give the Fed the go-ahead for aggressive rate hikes. It seems to give the market some momentum for a rebound after a tough few weeks. Unfortunately, the labor market does not yet reflect ongoing economic growth as underlying fundamentals are too robust. It will keep the Fed from taking its foot off the brake, which remains a huge risk for the market, given the bigger economic trend.

As this might sound contradicting and confusing, allow me to elaborate!

December Was A Good Month

December was a great month for the job market. The numbers were strong but not too strong to trigger fear that the Fed may have to hike more aggressively than previously assumed.

US non-farm payroll gains game in at 223 thousand in December. This was higher than the consensus estimate of 200 thousand jobs. It is down from 256 thousand in November.

This is the weakest number since 2020, yet one of many gains close to 250 thousand since the start of 2021. It's hard to make this look like a bad thing.

ZeroHedge

The unemployment rate came in at 3.5%, which is down from 3.6% in November and below the consensus estimate of 3.7%.

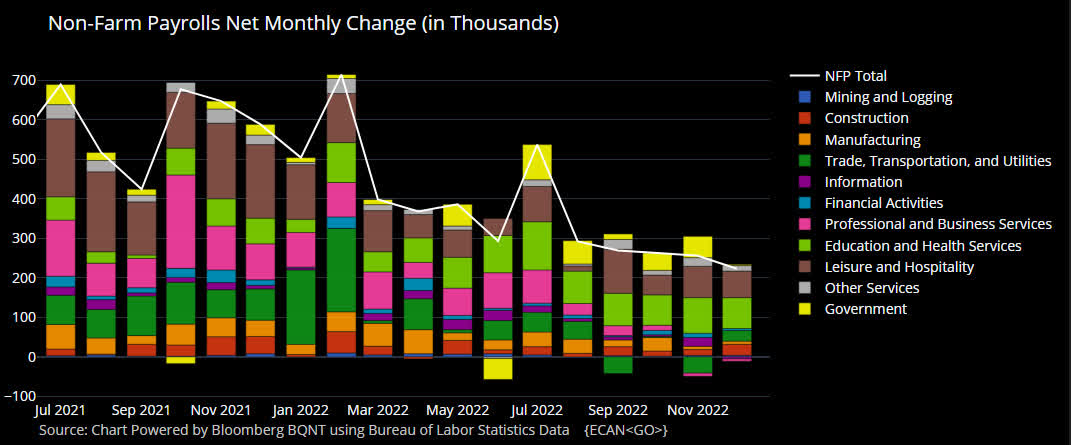

As the chart below shows, while job gains have slowed (as shown in the chart above as well), job gains were supported by most industries - even without government support, as we witnessed in October and November.

{kind=link}

All industries but "other services" saw growth in December. Even cyclical manufacturing jobs did well despite severe economic growth slowing.

{kind=link}

The overview below shows that in manufacturing, job losses in petroleum and coal, apparel, chemicals, and related were more than offset by gains in transportation equipment and nonmetallic mineral products - among others.

Looking at the overview below, there's a case to be made that economic growth slowing is hitting the labor market. However, there is simply not enough evidence to make the case that the job market is in a bad or even tough spot.

Bloomberg

The cyclical leisure and hospitality industry continues to add jobs, with total unemployment still 5.5% below pre-pandemic levels.

Bloomberg

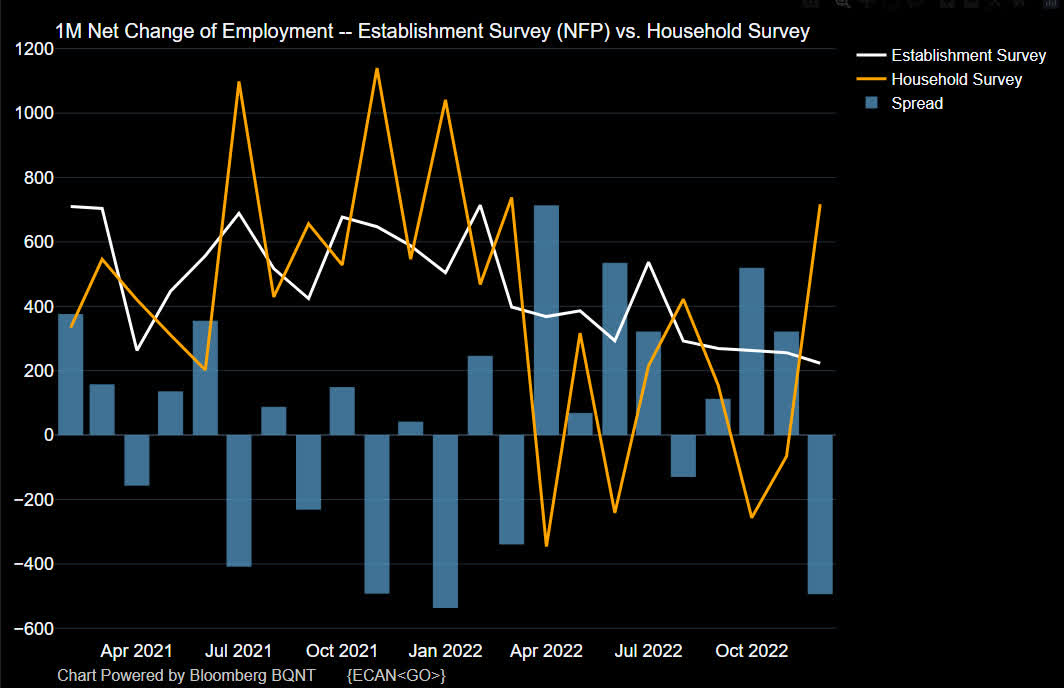

But wait! There's more. Even the household survey, which prevents duplication as individuals with multiple jobs are counted as one, showed a strong surge after underperforming the NFP report consistently in 2022.

{kind=link}

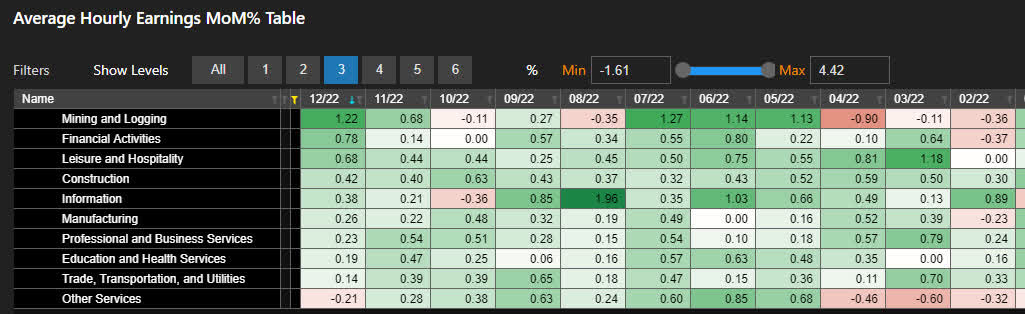

With all of this being said, the best piece of news for the market was wage growth.

Average hourly earnings improved by 4.6% year-on-year. That's below expectations of 5.0% and down from 4.8% growth in November. Wages rose by 0.3% compared to November. That is down from 0.4%.

Bloomberg

Wage growth is high enough to suggest that the worker is doing all right. However, it's not high enough to make the case that the Fed needs to tighten more aggressively than previously assumed.

Yet, there still are some issues.

Reasons To Be Worried

I just wrote an article with the following title:

{kind=link}

The thesis discussed in that article is based on a need for the Federal Reserve to weaken the labor market.

One of the things I have discussed in a lot of articles since December is my fear that the Fed will have to be aggressive when it comes to fighting inflation. For example, as Lawrence McDonald said last month, roughly $10 trillion in government debt is due in 2023 and 2024. Refinancing and adding new scheduled debt could increase debt servicing costs by $600 billion. That's a horrible development for a government that needs to maintain strong discretionary spending - especially going into a very important 2024 election year.

Hence, my thesis was - and still is - based on the following pillars:

- The Fed is feeling tremendous pressure to control inflation. That makes sense as the US economy is consumer-driven. Also, high inflation can quickly turn into lasting above-average inflation once wages and spending habits adjust. That's a no-go!

- Hence, I believe that the Fed will not be afraid to do damage to the US economy to achieve its target of lower inflation. This includes hurting housing demand/prices, unemployment, and consumer spending.

- Once the Fed pivots (I still believe it will happen in 2023), the economy will slowly adjust to lower rates. Demand will come back. So will inflation.

- Given the aforementioned secular factors, I believe we are in a prolonged period of Fed hikes and cuts at above-average rates (versus 2009-2021).

Looking at leading indicators like the ISM production and new orders indices, we see that we're in an advanced growth slowing cycle.

Wells Fargo

The worst part is that the market still cannot expect the Fed to take its foot off the brake. After all, it is still dealing with a strong labor market.

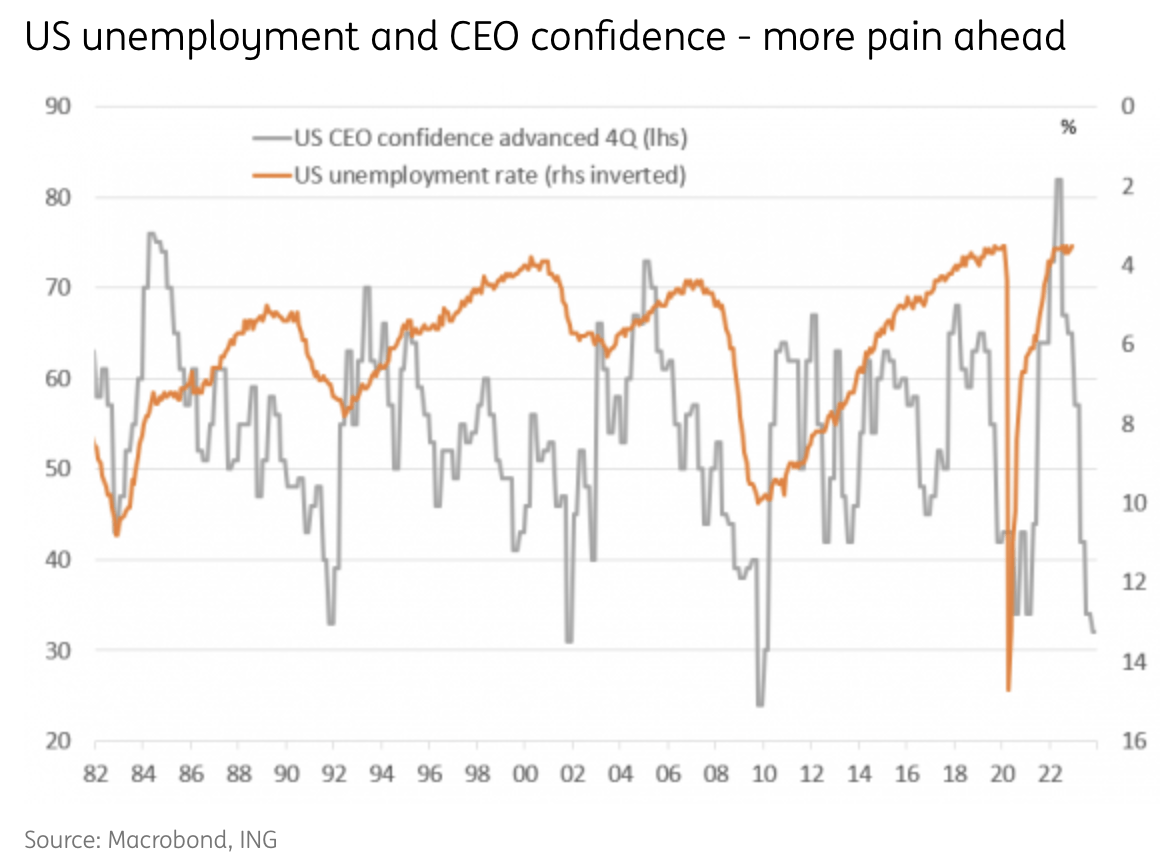

For example, using ING data, we see that the unemployment rate is completely ignoring CEO confidence, which is another popular leading indicator for economic growth.

{kind=link}

This makes sense as structural labor shortages are still a thing.

As discussed by Bloomberg , the labor component of consumer confidence remains very high as the quits rate in the US remains high.

Also within the JOLTS report, we got news that the Quits rate actually ticked higher, which again, is a sign that workers feel good about the state of the labor market. One of my favorite charts, which I've probably posted a few dozen times, is the Quits Rate vs. the Labor Differential Index of the Conference Board Consumer Confidence survey. One is hard data (the % of workers who quit) while the other is a sentiment measure (basically asking workers how they feel about the labor market). And yet the two lines move together really nicely. Both saw a jump in their latest reading.

Bloomberg

This is what economist Anna Wong had to say concerning strong labor demand:

"The stability in November's job openings defied consensus expectations and underscored the Fed's difficulty in bringing wage growth to a level consistent with the central bank's price target. The elevated quits rate should keep competition for labor supply intense, maintaining upward pressure on wages."

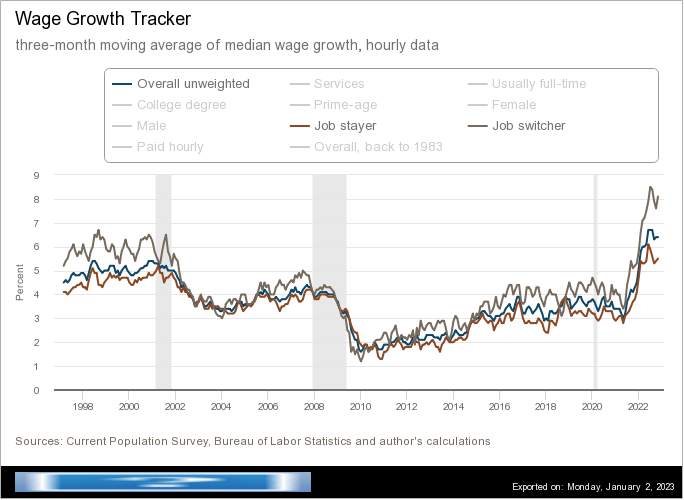

She is entirely right as wages for job switchers are rising by almost 8%.

{kind=link}

Hence, markets are extremely nervous as they know the Fed isn't afraid to go too far.

"A big concern of their messaging here is that the market is pricing in cuts by the second half of this year," said Michael Feroli, Chief US Economist at JPMorgan Chase & Co. With inflation too high, officials "realize that the risk of overtightening is just something that they have to swallow and stomach," he told Bloomberg Television.

Another quote from the article can be seen below, which I believe is so very important as it shows what Powell is concerned about:

He also described the labor market as "out of balance," and "extremely tight," and warned that restoring stable prices is likely to require some "softening" in job market conditions.

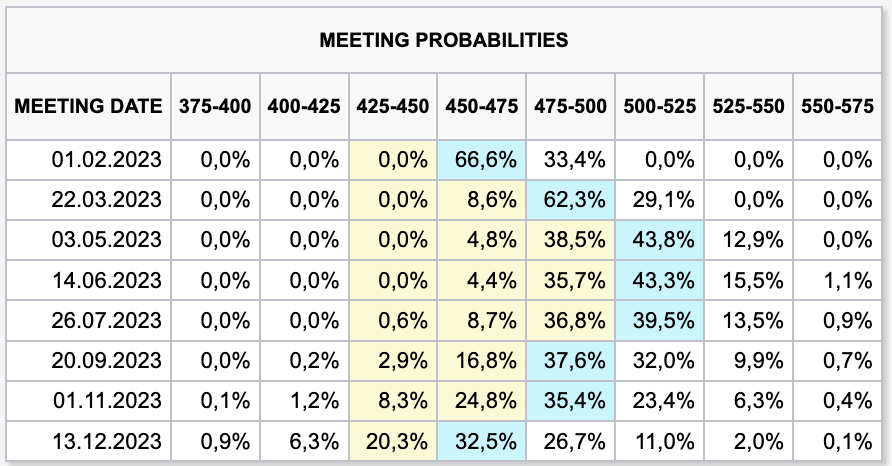

For now, the market expects the Fed to hike rates gradually to 5.25%. The current rate is 4.50%. In the second half of 2023, the market expects a pivot and rate cuts to the 4.50% to 4.75% range.

{kind=link}

Hence, I expect the market to remain in a volatile sideways trend with downside room to the low 3,000 range (3,300 being my first realistic target).

{kind=link}

In that area, I will be buying more aggressively as it means that a lot has been priced in. For now, I remain very cautious as I don't fully trust what some call a goldilocks jobs report.

Takeaway

In this article, we discussed the December jobs report and its implications on the market. While the jobs report is bullish, it is hard to make the case that we're out of the woods.

The economy is rapidly weakening, while inflationary factors like wage growth remain strong. It is highly likely that the Fed will have to do more damage than previously assumed to reach its target of 2% inflation.

I remain highly cautious and believe the market has more room to fall to the low 3,000 range.

(Dis)agree? Let me know in the comments!

For further details see:

This Rather Good Jobs Report Won't Change The Downtrend