QVMS - This Recession Won't Get The Fed To Back Off

- The odds for a technical recession appear to be very high.

- But a technical recession will not derail the Fed's mission to bring down inflation.

- The Fed will need to get the inflation rate below the nominal GDP growth rate.

Don't be surprised if the US is in a technical recession by the time July is over. The odds are high that second quarter GDP growth will be negative. The Atlanta Fed GDPNow model as of July 6 is at -2.1%. That would make for the second straight quarter of negative GDP growth. But that doesn't mean the Fed will back off.

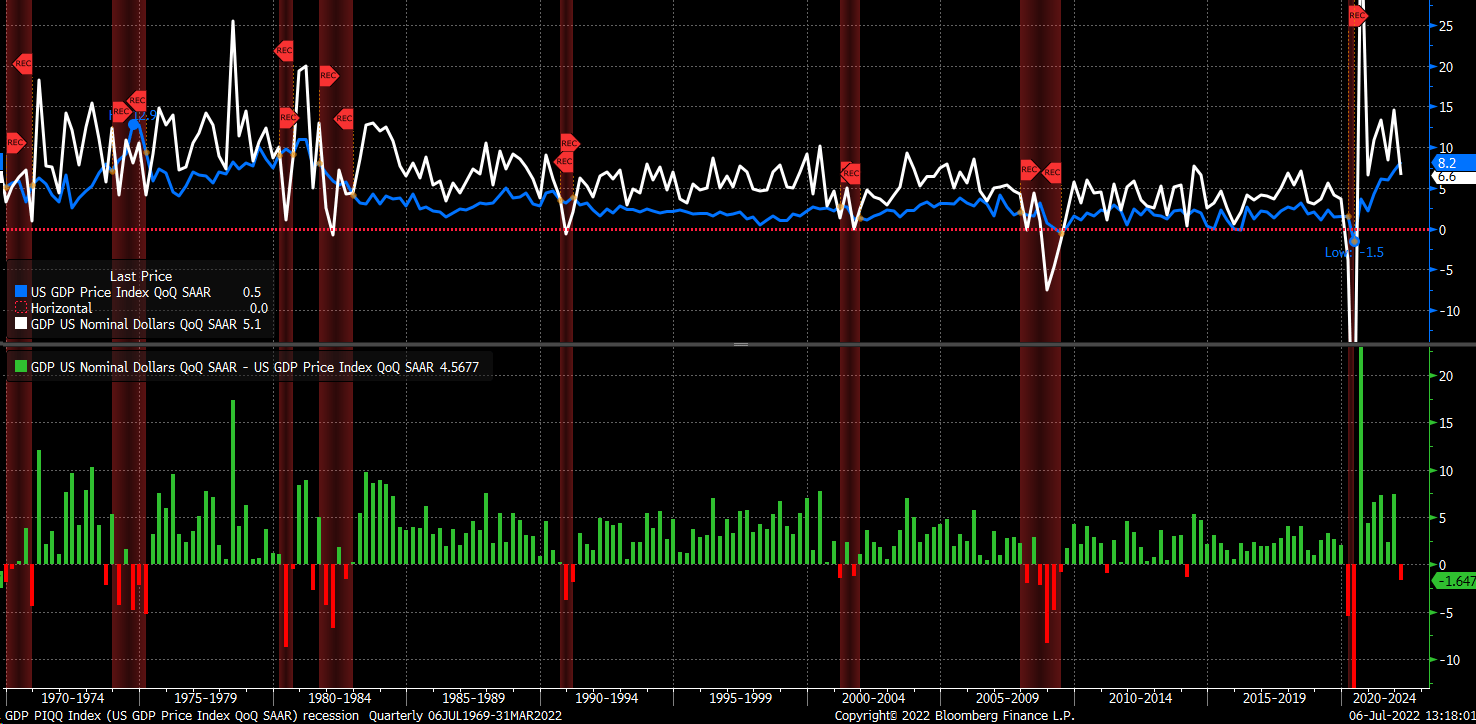

The Fed can't back off because GDP is likely to be negative in the second quarter because of high inflation. GDP has a price index, which tends to track CPI pretty closely over time. Given that CPI is likely to be over 8% in the second quarter, there's a good chance the GDP price index will be around 8%, which makes it very difficult for a positive GDP result in the second quarter.

Headline GDP is adjusted for inflation and referred to as real GDP. But to get real GDP, it starts with nominal GDP and then is adjusted for the inflation rate. In this case, a -2% real GDP print, with an 8% inflation rate, would imply that nominal GDP is growing around 6%.

Of course, the scenario creates a big problem for the Fed and the markets. Because the markets appear to be following the normal recession playbook of the past two decades, falling commodity prices and inverting the yield curve making everyone believe the Fed will soon back off.

But this is where the idea of the Fed backing off may be completely wrong. The economy may go into a technical recession in real terms , but it may not go into recession in nominal terms.

This minor subtlety has a significant implication because it's possible for a string of negative real GDP prints over the next few quarters. If the Fed does what it plans to do, which is slow demand, then nominal GDP growth and inflation should come down. But the Fed must bring the inflation rate back below the nominal GDP growth rate to push the real GDP growth into positive territory.

Historically, when nominal GDP is above the inflation rate, the economy is healthy. When the inflation rate rises above nominal GDP, the US economy tends to fall into recession. But during those recessions, nominal GDP and inflation rates tended to approach 0% slowly. It was only during the 2008 recession and the coronavirus recession that nominal GDP went profoundly negative.

The data also shows that the recessions of the 1970s and early 1980s tended to be long lasting. Certainly more so than the 1990 recession, 2000 recession, and coronavirus recession. It supports the idea that if there's a recession in 2022 and 2023, it will probably look more like the 1970s and 80s, and less like the ones witnessed in recent times. Inflation and growth rates today resemble those of the 1970s and 1980s.

{kind=link}

This is why the Fed is not likely to back off raising rates and keeping financial conditions tight just because there is a quarter or two of negative real GDP prints. It might be that there will need to be a few quarters of negative real GDP prints to bring the inflation rate back to the Fed's mandated average 2% target.

{kind=link}

If the Fed cannot bring the inflation rate down soon, then rates will have to go much higher. Historically, the 3-month Treasury bill has traded with a higher rate than the year-over-year CPI inflation rate. It has only been over the past decade that the inflation rate has run hotter than the 3-month Treasury bill rate. This would indicate that for inflation to start coming down again, the Fed would need to raise rates further to bring up the 3-month Treasury bill rate.

High inflation creates a new set of dynamics that markets haven't dealt with for a very long time and means that investors need to change their thought process to just how and when the Fed may blink. It may not come nearly as quickly as many believe and may require much more pain before resolving the issue.

For further details see:

This Recession Won't Get The Fed To Back Off