THO - THOR Industries: An Update After Fiscal Q4 2023 Results

2023-09-27 11:14:23 ET

Summary

- THOR Industries' Q4 2023 results were largely uneventful, as the industry digested elevated inventories and a sharp drop in final demand.

- However, THOR's balance sheet has improved significantly during the year and has positioned the company extremely well for a prolonged downturn, should one eventually materialize.

- THOR's valuation remains cheap. Although THOR expects only a modest recovery in 2024 given the uncertain outlook, for long-term investors THOR's current valuation (1.2x EV/NOA) portends strong future returns.

THOR Industries (THO), the leading U.S. manufacturer of recreational vehicles (RVs), released its full year results on Monday. As my initiation report was published almost a year ago, I thought it was timely to provide an update. For the sake of brevity, I will not rehash THOR’s competitive advantages or its history; I will only highlight the main developments of the last twelve months.

As was widely expected last year, 2023 has proven to be a challenging year for the industry. Although retail sales are expected to close around the 350k units (which is the level I took as reasonable to ensure reasonable profits for the OEMs going forward), dealers began the year with bloated inventories that had been coming down through the year, which means wholesale shipments (the number important for the OEMs like THOR) have been substantially lower. The industry now expects wholesale shipments of 297k units (249k in towables and 48 in motorized), with a modest rebound in 2024.

In line with the rest of the industry, THOR’s shipments fell sharply in 2023 (THOR’s financial year ends at the end of July). THOR’s shipments were 131k (versus 268k a year ago) and towables were the category with the largest relative decline (from 239k to 107k). As retail shipments were higher than wholesale shipments, this allowed dealers to reduce inventories, and although the level of inventories is still higher than seasonal norms, (for figures, see THOR’s 4Q’23 Investor Presentation, p. 5), a large part of the destocking process has already been completed. Average realized prices held up quite well, although THOR said in its Q&A commentary that it expects lower prices next year to address affordability issues and prop up overall volumes.

A bright spot was the performance of the European business, a segment which I had not given much weight in my original analysis. Although shipments in the European segment have fallen from 2022 levels and are only at 2020 levels (around 56k units), profitability has been strong due to the lack of chassis, which has constrained supply. THOR expects this momentum to continue over the next few quarters, keeping dealers’ inventories at low levels. Gross margins in this segment were 16.6%, the highest in history and even higher than those in the North American towable (12%) and motorized (13,4%) segments. Although I expect the European margins to revert in the future (for reasons I discussed in my original article, in particular the historically lower margins of the motorized segment compared to towables due to the higher value capture of the chassis manufacturer in the former case), this is still a very welcome development.

Finally, another bright spot was the deleveraging that took place during the year. Net debt was reduced from $1.4bn to $900M, in line with THOR’s strategic priorities. THOR has traditionally been a company with a conservative balance sheet , but this has changed somewhat as THOR completed the acquisitions of EHG (for €2.1bn.), Tiffin Group ($300M) and Airxcel ($750M) in 2018, 2020 and 2021, respectively. I expect further debt reduction in the coming quarters, as the company is less likely than in the past (due to the already high level of consolidation in the sector) to commit significant resources to M&A. This is a very welcome development, as in such a cyclical industry the main roadblock to long-term wealth creation is getting into distress when times are tough. THOR’s current balance sheet should allow it to withstand a prolonged downturn if, for whatever reason, it finally comes.

Valuation update

I would encourage readers interested in understanding the valuation framework to read the original article , where I explained in detail the residual income and its advantages in modelling cyclical businesses such as THOR. As the share price has barely moved (excluding the dividend), the forward opportunity of investing in THOR is essentially the same as it was a year ago.

Turning to fundamentals, the biggest difference from a year ago is the level of net debt, as discussed above. Although the deleveraging effort has roughly added a respectable 7$ per share of value over the year, as I argued above, the “qualitative” effects (reduced likelihood of distress) are even more important for long-term shareholders.

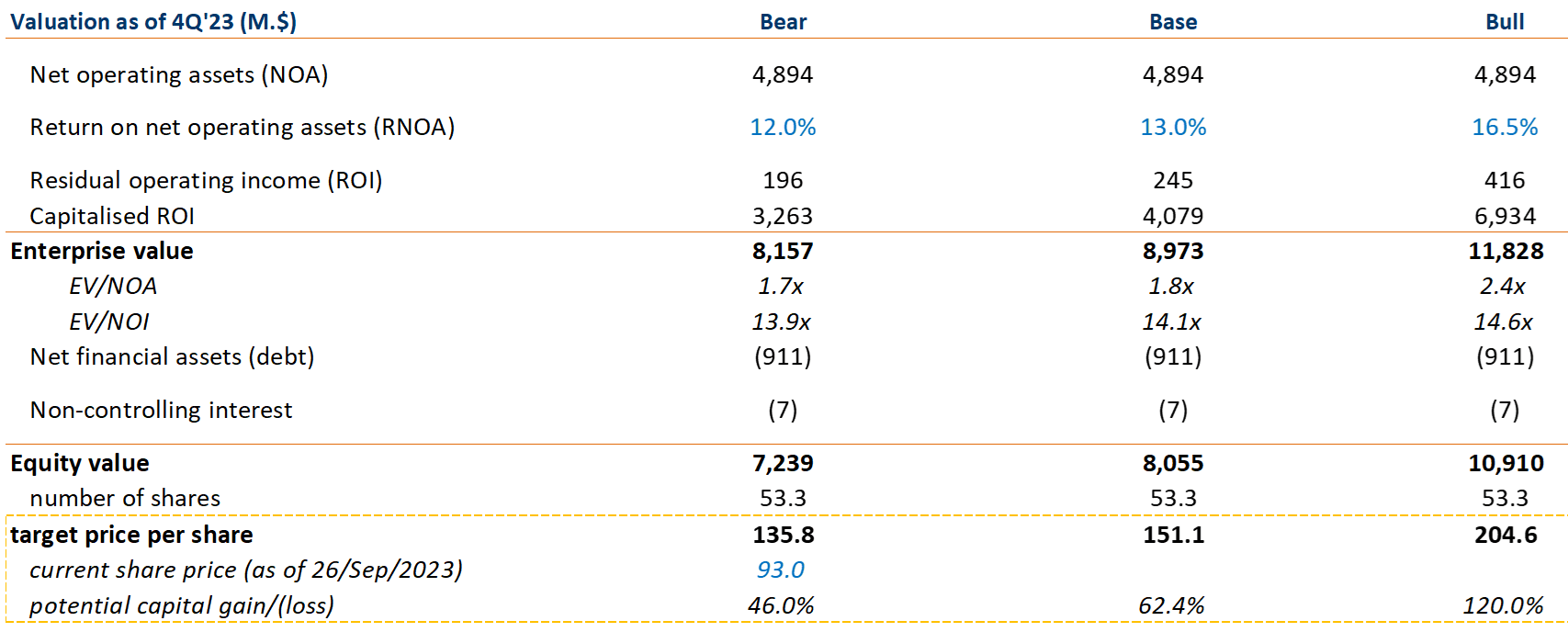

Given THOR’s asset base of $4.9bn as of 4Q’23 (largely unchanged from a year ago), and assuming a base case RNOA of 13% and a discount rate of 8%, this would translate into residual operating income (income above the cost of capital) of around $250M, which happens to be in line with THOR’s average earnings power over the last five years (which includes one boom but also two busts periods). For the bull case, I am assuming an RNOA of 16.5%, which is in line with THOR’s pre-Covid track-record, but which, as I explained in my original article, I view as hard to achieve as the capital intensity of the business has increased due to the recent spate of acquisitions.

{kind=link}

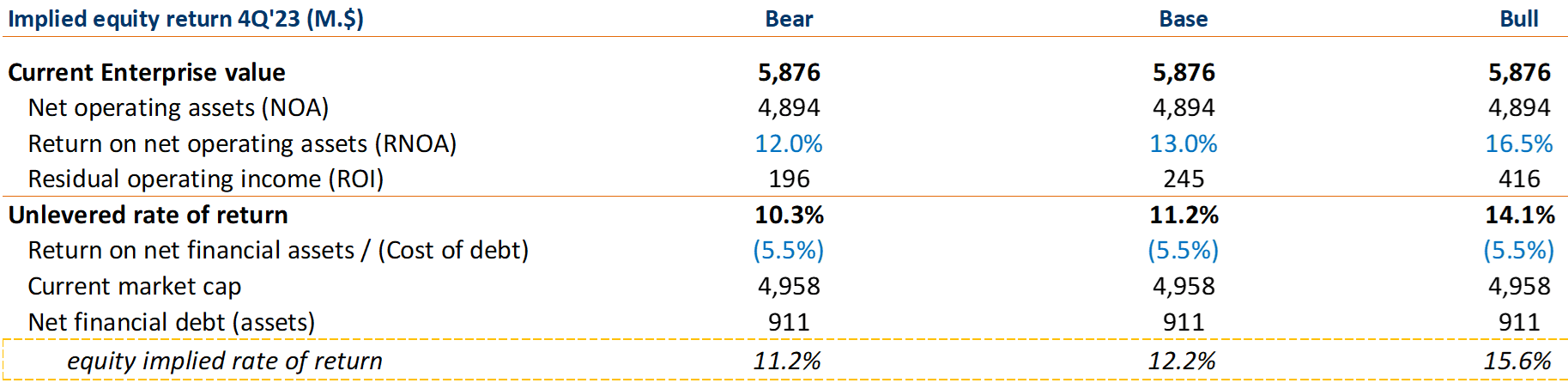

Finally, if we look at the previous assumptions in terms of IRRs, the results would be as follows. Given the current EV of $5.9bn. (EV/NOA of 1.2x), and assuming that our forward RNOAs are correct (12% for the bear case, 13% for the base case, and 16% for the bull case), future equity returns will be 11%, 12%, and 16% per annum respectively, offering thus strong return prospects for long-term investors:

{kind=link}

Conclusion

After one of the worst years in recent memory for the RV industry, THOR is ending the period on a stronger footing thanks to an improved balance sheet and the resilience and diversification provided by its European business. Although THOR has warned that 2024 will still be challenging (and a full year is a very long time for most “investors” out there), I expect THOR’s business to be largely unscathed when the next upturn comes. Given THOR’s dominant position in the industry, its sensible capital allocation policy (with a large share buyback authorization in place), the company’s reasonable returns on capital and its cheap valuation, I think the current share price level will provide solid future returns with an ample margin of safety.

For further details see:

THOR Industries: An Update After Fiscal Q4 2023 Results